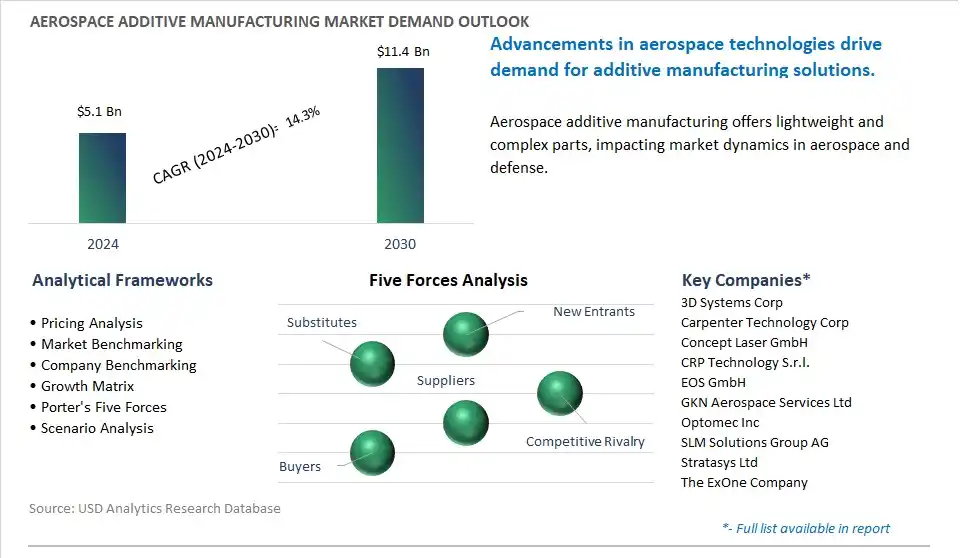

The global Aerospace Additive Manufacturing Market is poised to register a 14.3% CAGR from $5.1 Billion in 2024 to $11.4 Billion in 2030.

The global Aerospace Additive Manufacturing Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Material (Metal, Plastic, Rubber, Others), By Technology (3D Printing, Laser Sintering, Stereolithography, Others), By Platform (Aircraft, Unmanned Aerial Vehicle).

An Introduction to Global Aerospace Additive Manufacturing Market in 2024

The aerospace additive manufacturing market is experiencing growth driven by the increasing adoption of 3D printing technologies for rapid prototyping, production tooling, and end-use part manufacturing in the aerospace and defense industry. Key trends shaping the future of the industry include advancements in additive manufacturing materials, processes, and design optimization techniques to meet aerospace performance requirements, regulatory standards, and cost constraints. Innovations such as high-temperature alloys, composite materials, and metal additive manufacturing technologies enable the production of lightweight, complex, and high-performance aerospace components with reduced lead times and material waste. Moreover, the integration of generative design, topology optimization, and simulation tools optimizes part geometries, material usage, and performance characteristics, enhancing the efficiency and competitiveness of additive manufacturing in aerospace applications. Additionally, the adoption of in-situ monitoring, post-processing techniques, and certification processes ensures quality control, traceability, and compliance with aerospace industry standards and safety regulations. As aerospace manufacturers embrace additive manufacturing as a disruptive technology for aircraft design, production, and sustainment, the market is poised for continued growth and innovation as a key enabler of next-generation aerospace systems and components.

Aerospace Additive Manufacturing Market Competitive Landscape

The market report analyses the leading companies in the industry including 3D Systems Corp, Carpenter Technology Corp, Concept Laser GmbH, CRP Technology S.r.l., EOS GmbH, GKN Aerospace Services Ltd, Optomec Inc, SLM Solutions Group AG, Stratasys Ltd, The ExOne Company.

Aerospace Additive Manufacturing Market Dynamics

Aerospace Additive Manufacturing Market Trend: Adoption of Advanced Materials and Processes in Aerospace Additive Manufacturing

A prominent trend in the aerospace additive manufacturing market is the adoption of advanced materials and processes. As the aerospace industry continues to push the boundaries of innovation and performance, there is a growing demand for additive manufacturing technologies capable of producing complex geometries and high-performance components. Manufacturers are increasingly leveraging advanced materials such as titanium alloys, nickel-based superalloys, and carbon composites to meet the stringent requirements of aerospace applications. Additionally, advancements in additive manufacturing processes, including laser powder bed fusion, electron beam melting, and binder jetting, enable the production of lightweight and durable aerospace parts with improved mechanical properties and performance characteristics. This trend reflects a broader shift towards the adoption of additive manufacturing as a transformative technology in the aerospace sector, driving innovation and efficiency in aircraft design and production.

Aerospace Additive Manufacturing Market Driver: Need for Lightweight and Cost-Effective Aerospace Components

A key driver for the aerospace additive manufacturing market is the need for lightweight and cost-effective aerospace components. In the aerospace industry, there is a constant demand for lightweight materials and structures to enhance fuel efficiency, reduce emissions, and improve aircraft performance. Additive manufacturing offers unique advantages in this regard by enabling the production of complex, lightweight components with optimized geometries and material properties. By utilizing additive manufacturing technologies, aerospace manufacturers can design and fabricate parts with reduced weight, improved structural integrity, and enhanced functionality, leading to fuel savings, operational efficiencies, and overall cost reductions throughout the aircraft lifecycle. The quest for lightweight and cost-effective aerospace components drives the adoption of additive manufacturing as a strategic manufacturing solution in the aerospace industry.

Aerospace Additive Manufacturing Market Opportunity: Integration of Additive Manufacturing into Aerospace Supply Chains

An opportunity within the aerospace additive manufacturing market lies in the integration of additive manufacturing into aerospace supply chains. While additive manufacturing technologies have made significant strides in recent years, there is still untapped potential for broader adoption and integration within the aerospace ecosystem. Aerospace companies can capitalize on this opportunity by investing in additive manufacturing capabilities and expertise to streamline production processes, reduce lead times, and enhance supply chain flexibility. By integrating additive manufacturing into their manufacturing workflows, aerospace OEMs and suppliers can overcome traditional manufacturing constraints, accelerate product development cycles, and respond more effectively to market demands for customized and on-demand aerospace components. This strategic integration of additive manufacturing into aerospace supply chains presents opportunities for enhanced competitiveness, innovation, and value creation across the aerospace industry.

Aerospace Additive Manufacturing Market Share Analysis: Metal segment generated the highest revenue in the industry

The metal segment commands the largest share in the aerospace additive manufacturing market for diverse compelling reasons. The metals offer superior mechanical properties, including strength, durability, and heat resistance, making them well-suited for aerospace applications where components must withstand extreme conditions and high stress environments. Additive manufacturing technologies, such as selective laser melting (SLM) and electron beam melting (EBM), enable the production of complex metal parts with intricate geometries and precise specifications, fulfilling the demanding requirements of aerospace manufacturers. Secondly, metal additive manufacturing allows for the production of lightweight components without compromising structural integrity, contributing to fuel efficiency and Over the forecast period aircraft performance. By utilizing advanced alloys and optimizing design for additive manufacturing (DfAM) principles, aerospace engineers can achieve significant weight reduction while maintaining safety and performance standards. Thirdly, metals exhibit excellent compatibility with post-processing techniques such as machining, heat treatment, and surface finishing, enabling further customization and optimization of additively manufactured aerospace components. In addition, the continuous advancements in metal powder formulations, process parameters, and quality control measures enhance the reliability, repeatability, and scalability of metal additive manufacturing in aerospace applications. Over the forecast period, the superior mechanical properties, lightweighting potential, and post-processing capabilities of metals position them as the largest segment in the aerospace additive manufacturing market.

Aerospace Additive Manufacturing Market Share Analysis: Unmanned Aerial Vehicle (UAV) Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The unmanned aerial vehicle (UAV) segment is experiencing the fastest growth in the aerospace additive manufacturing market due to diverse key factors. The the rising demand for UAVs across various sectors, including military, commercial, and recreational, is driving the adoption of additive manufacturing technologies for their production. UAVs offer unique advantages such as surveillance, reconnaissance, cargo delivery, and aerial mapping, among others, leading to increased investments in UAV development and manufacturing. Additive manufacturing enables the rapid prototyping, customization, and production of UAV components with complex geometries and lightweight structures, meeting the specific requirements of diverse UAV applications. Secondly, the miniaturization trend in UAV design, driven by advancements in electronics, sensors, and propulsion systems, creates opportunities for additive manufacturing to fabricate small, intricate parts with high precision and efficiency. Additive manufacturing processes like laser powder bed fusion (LPBF) and fused deposition modeling (FDM) enable the production of miniaturized UAV components such as housings, brackets, and connectors with minimal material waste and reduced lead times. Thirdly, the versatility of additive manufacturing allows for the integration of advanced materials, including lightweight alloys, composites, and hybrid materials, into UAV designs to enhance performance, durability, and functionality. Additionally, additive manufacturing facilitates the production of UAVs with reduced assembly complexity and fewer individual parts, leading to cost savings and improved manufacturing efficiency. Over the forecast period, the growing demand for UAVs, coupled with the unique capabilities of additive manufacturing to address UAV-specific design challenges, positions the UAV segment as the fastest-growing segment in the aerospace additive manufacturing market.

Aerospace Additive Manufacturing Market Report Segmentation

By Material

Metal

Plastic

Rubber

Others

By Technology

3D Printing

Laser Sintering

Stereolithography

Others

By Platform

Aircraft

Unmanned Aerial Vehicle

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Aerospace Additive Manufacturing Companies Profiled in the Market Study

3D Systems Corp

Carpenter Technology Corp

Concept Laser GmbH

CRP Technology S.r.l.

EOS GmbH

GKN Aerospace Services Ltd

Optomec Inc

SLM Solutions Group AG

Stratasys Ltd

The ExOne Company

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Aerospace Additive Manufacturing Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Aerospace Additive Manufacturing Market Size Outlook, $ Million, 2021 to 2030

3.2 Aerospace Additive Manufacturing Market Outlook by Type, $ Million, 2021 to 2030

3.3 Aerospace Additive Manufacturing Market Outlook by Product, $ Million, 2021 to 2030

3.4 Aerospace Additive Manufacturing Market Outlook by Application, $ Million, 2021 to 2030

3.5 Aerospace Additive Manufacturing Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Aerospace Additive Manufacturing Industry

4.2 Key Market Trends in Aerospace Additive Manufacturing Industry

4.3 Potential Opportunities in Aerospace Additive Manufacturing Industry

4.4 Key Challenges in Aerospace Additive Manufacturing Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Aerospace Additive Manufacturing Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Aerospace Additive Manufacturing Market Outlook by Segments

7.1 Aerospace Additive Manufacturing Market Outlook by Segments, $ Million, 2021- 2030

By Material

Metal

Plastic

Rubber

Others

By Technology

3D Printing

Laser Sintering

Stereolithography

Others

By Platform

Aircraft

Unmanned Aerial Vehicle

8 North America Aerospace Additive Manufacturing Market Analysis and Outlook To 2030

8.1 Introduction to North America Aerospace Additive Manufacturing Markets in 2024

8.2 North America Aerospace Additive Manufacturing Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Aerospace Additive Manufacturing Market size Outlook by Segments, 2021-2030

By Material

Metal

Plastic

Rubber

Others

By Technology

3D Printing

Laser Sintering

Stereolithography

Others

By Platform

Aircraft

Unmanned Aerial Vehicle

9 Europe Aerospace Additive Manufacturing Market Analysis and Outlook To 2030

9.1 Introduction to Europe Aerospace Additive Manufacturing Markets in 2024

9.2 Europe Aerospace Additive Manufacturing Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Aerospace Additive Manufacturing Market Size Outlook by Segments, 2021-2030

By Material

Metal

Plastic

Rubber

Others

By Technology

3D Printing

Laser Sintering

Stereolithography

Others

By Platform

Aircraft

Unmanned Aerial Vehicle

10 Asia Pacific Aerospace Additive Manufacturing Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Aerospace Additive Manufacturing Markets in 2024

10.2 Asia Pacific Aerospace Additive Manufacturing Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Aerospace Additive Manufacturing Market size Outlook by Segments, 2021-2030

By Material

Metal

Plastic

Rubber

Others

By Technology

3D Printing

Laser Sintering

Stereolithography

Others

By Platform

Aircraft

Unmanned Aerial Vehicle

11 South America Aerospace Additive Manufacturing Market Analysis and Outlook To 2030

11.1 Introduction to South America Aerospace Additive Manufacturing Markets in 2024

11.2 South America Aerospace Additive Manufacturing Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Aerospace Additive Manufacturing Market size Outlook by Segments, 2021-2030

By Material

Metal

Plastic

Rubber

Others

By Technology

3D Printing

Laser Sintering

Stereolithography

Others

By Platform

Aircraft

Unmanned Aerial Vehicle

12 Middle East and Africa Aerospace Additive Manufacturing Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Aerospace Additive Manufacturing Markets in 2024

12.2 Middle East and Africa Aerospace Additive Manufacturing Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Aerospace Additive Manufacturing Market size Outlook by Segments, 2021-2030

By Material

Metal

Plastic

Rubber

Others

By Technology

3D Printing

Laser Sintering

Stereolithography

Others

By Platform

Aircraft

Unmanned Aerial Vehicle

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

3D Systems Corp

Carpenter Technology Corp

Concept Laser GmbH

CRP Technology S.r.l.

EOS GmbH

GKN Aerospace Services Ltd

Optomec Inc

SLM Solutions Group AG

Stratasys Ltd

The ExOne Company

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Material

Metal

Plastic

Rubber

Others

By Technology

3D Printing

Laser Sintering

Stereolithography

Others

By Platform

Aircraft

Unmanned Aerial Vehicle

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)