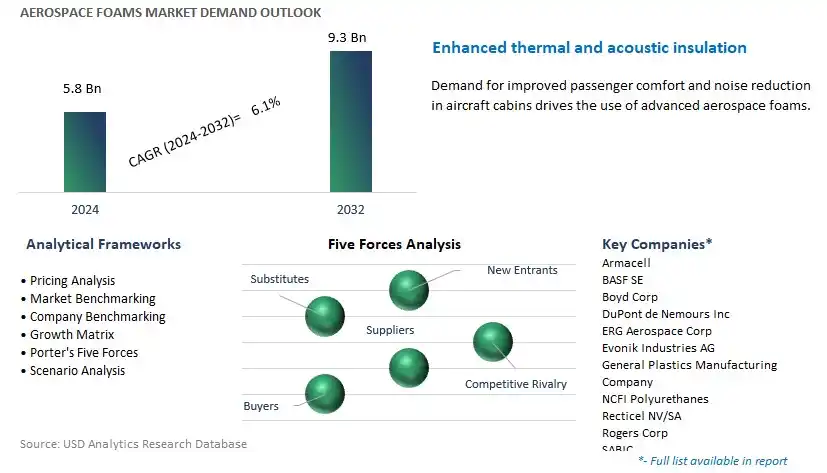

Global Aerospace Foams Market Size is valued at $5.8 Billion in 2024 and is forecast to register a growth rate (CAGR) of 6.1% to reach $9.3 Billion by 2032.

The global Aerospace Foams Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Material (PU Foams, PE Foams, Melamine Foams, Metal Foams, PMI/Polyimide Foams, Others), By End-User (Commercial Aircraft, Military Aircraft, General Aviation, Others), By Application (Aircraft Seats, Aircraft Floor Carpets, Flight Deck Pads, Cabin Walls and Ceilings, Overhead Stow Bins, Others).

An Introduction to Aerospace Foams Market in 2024

Aerospace foams are lightweight, cellular materials used in aerospace applications for insulation, cushioning, and structural reinforcement. These foams offer properties such as low density, high strength-to-weight ratios, and thermal insulation, making them essential for space exploration, aircraft interiors, and impact protection systems. The market for aerospace foams is driven by the need for lightweight, durable, and thermally stable materials that can withstand the extreme conditions of aerospace environments. Aerospace foams are used in applications such as thermal insulation for cryogenic fuel tanks, acoustic insulation for aircraft cabins, and impact absorption for spacecraft reentry vehicles. Additionally, advancements in foam manufacturing techniques, including microcellular foaming and nanocomposite formulations, are enhancing foam properties such as fire resistance, conductivity, and mechanical strength. As aerospace missions become more ambitious and diverse, the demand for specialized foams tailored to specific performance requirements is expected to grow, driving innovation and investment in foam technology.

Aerospace Foams Market Competitive Landscape

The market report analyses the leading companies in the industry including Armacell, BASF SE, Boyd Corp, DuPont de Nemours Inc, ERG Aerospace Corp, Evonik Industries AG, General Plastics Manufacturing Company, NCFI Polyurethanes, Recticel NV/SA, Rogers Corp, SABIC, Solvay S.A., UFP Technologies Inc, Zotefoams Plc, and others.

Aerospace Foams Market Dynamics

Market Trend: Growing Demand for Lightweight and Energy-Efficient Materials

A significant market trend for Aerospace Foams is the growing demand for lightweight and energy-efficient materials in aerospace applications, driven by the need to improve fuel efficiency, reduce emissions, and enhance performance of aircraft and spacecraft. Aerospace foams, with their low density, thermal insulation properties, and shock absorption capabilities, are increasingly utilized in interior and exterior applications such as seating, insulation, vibration damping, and structural reinforcement. As airlines, aerospace manufacturers, and space agencies seek to meet sustainability goals, comply with stringent regulations, and optimize operational costs, there is a rising preference for foams that offer weight savings, thermal management, and acoustic insulation, while maintaining durability and safety standards. This trend reflects a broader industry focus on lightweighting and material innovation in aerospace manufacturing to address environmental concerns, operational challenges, and market competitiveness.

Market Driver: Innovation in Material Science and Manufacturing Technologies

A significant market driver for Aerospace Foams is innovation in material science, polymer chemistry, and manufacturing technologies, enabling the development of foams with enhanced properties, performance, and cost-effectiveness for aerospace applications. With continuous research and development efforts, manufacturers are able to engineer foams that offer improved strength-to-weight ratio, flame retardancy, thermal stability, and resistance to chemical degradation, meeting the rigorous requirements of aerospace industry standards and regulatory certifications. Additionally, advancements in manufacturing processes such as injection molding, foam extrusion, and additive manufacturing enable the production of complex foam structures with precise geometries, reduced weight, and optimized performance. The demand for aerospace foams is further driven by technological advancements in additive manufacturing, allowing for the customization and optimization of foam properties to meet specific aerospace requirements, thereby fueling market growth and innovation in the aerospace foam industry.

Market Opportunity: Expansion into Space Exploration and Satellite Applications

An attractive opportunity in the Aerospace Foams market lies in expanding into space exploration and satellite applications, where foams play a critical role in providing thermal insulation, structural support, and protection against extreme environments. In space exploration missions, foams are utilized for thermal insulation in spacecraft components, habitat modules, and space suits, ensuring temperature stability and crew comfort in outer space. Additionally, foams are used in satellite payloads and components for vibration damping, shock absorption, and structural reinforcement, safeguarding sensitive equipment and electronics from mechanical stress and launch-induced vibrations. With the increasing commercialization of space and the growing demand for small satellites, constellations, and space tourism, there is a significant opportunity for foam manufacturers to provide innovative solutions that meet the unique challenges and requirements of space exploration and satellite applications. By leveraging their expertise in foam technology and collaborating with aerospace agencies and satellite manufacturers, foam suppliers can capitalize on this opportunity to expand their market presence and drive growth in the aerospace foam industry.

Aerospace Foams Market Share Analysis: PU Foams Segment generated the highest revenue in 2024

In the Aerospace Foams market segmented by material, the PU (Polyurethane) Foams segment is the largest category. The large revenue share is primarily due to the widespread use and versatile properties of polyurethane foams in aerospace applications. PU foams offer a combination of lightweight construction, excellent thermal insulation, cushioning, sound absorption, and vibration damping properties, making them suitable for various aerospace interior and insulation applications. These foams are extensively utilized in aircraft seating, cabin interiors, galleys, overhead storage bins, and thermal insulation panels to enhance passenger comfort, safety, and energy efficiency. Additionally, PU foams can be easily molded, shaped, and fabricated to meet specific design requirements, offering flexibility in aerospace interior design and manufacturing processes. Moreover, advancements in PU foam technology, such as the development of flame-retardant and low-smoke formulations, further contribute to their widespread adoption in aircraft interiors. Furthermore, PU foams are cost-effective and readily available, making them a preferred choice for aerospace manufacturers seeking lightweight and durable foam solutions. As the aerospace industry continues to prioritize passenger comfort, safety, and fuel efficiency, the PU Foams segment maintains its leading position in the Aerospace Foams market.

Aerospace Foams Market Share Analysis: Commercial Aircraft segment is poised to register the fastest CAGR over the forecast period

Within the Aerospace Foams market segmented by end-user, the Commercial Aircraft segment is the fastest-growing category. The market growth is driven by increasing demand for aerospace foams in commercial aviation applications. With the steady growth of air travel and rising passenger volumes globally, there is a corresponding increase in the production and modernization of commercial aircraft fleets. Aerospace foams play a crucial role in enhancing passenger comfort, safety, and operational efficiency within commercial aircraft cabins and interiors. These foams are utilized in seating, cabin linings, overhead bins, galleys, and lavatories to provide cushioning, noise reduction, thermal insulation, and fire resistance properties. Moreover, as airlines strive to differentiate their services and improve passenger experience, there is a growing emphasis on cabin amenities and comfort features, driving the demand for high-quality foams in commercial aircraft interiors. Additionally, advancements in foam technology, such as the development of lightweight, durable, and eco-friendly formulations, further contribute to the growth of the Commercial Aircraft segment in the Aerospace Foams market. Furthermore, as regulatory standards and aircraft certification requirements continue to evolve, aerospace foams that meet stringent safety and performance criteria are increasingly in demand for commercial aviation applications. As the commercial aviation sector continues to expand and modernize its fleets to meet growing passenger demand, the Commercial Aircraft segment is poised for sustained rapid growth in the Aerospace Foams market.

Aerospace Foams Market Share Analysis: Aircraft Seats Application Segment generated the highest revenue in 2024

In the Aerospace Foams market segmented by application, the Aircraft Seats segment is the largest category. The large revenue share is primarily due to the significant demand for foam materials in manufacturing comfortable and durable seating solutions for aircraft passengers. Aircraft seats require foam padding to provide cushioning, support, and comfort during flights, making foam materials an essential component of seat construction. Foam materials used in aircraft seats offer properties such as resilience, shock absorption, and fire resistance to ensure passenger safety and comfort throughout the duration of the flight. Additionally, foam materials are utilized in various components of aircraft seats, including seat cushions, backrests, armrests, and headrests, further driving the demand for foam materials in the Aircraft Seats segment. Moreover, as airlines focus on enhancing passenger experience and satisfaction, there is a growing trend towards the adoption of ergonomically designed seats with advanced foam padding technologies to improve comfort and reduce fatigue during long-haul flights. Furthermore, advancements in foam manufacturing processes and materials technology have led to the development of lightweight, durable, and environmentally friendly foam solutions for aircraft seating applications, further bolstering the dominance of the Aircraft Seats segment in the Aerospace Foams market. As the global air travel market continues to grow and airlines invest in fleet expansion and modernization, the demand for foam materials in aircraft seating applications is expected to remain robust, sustaining the leadership of the Aircraft Seats segment in the Aerospace Foams market.

Aerospace Foams Market

By Material

PU Foams

PE Foams

Melamine Foams

Metal Foams

PMI/Polyimide Foams

Others

By End-User

Commercial Aircraft

Military Aircraft

General Aviation

Others

By Application

Aircraft Seats

Aircraft Floor Carpets

Flight Deck Pads

Cabin Walls and Ceilings

Overhead Stow Bins

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Aerospace Foams Companies Profiled in the Study

Armacell

BASF SE

Boyd Corp

DuPont de Nemours Inc

ERG Aerospace Corp

Evonik Industries AG

General Plastics Manufacturing Company

NCFI Polyurethanes

Recticel NV/SA

Rogers Corp

SABIC

Solvay S.A.

UFP Technologies Inc

Zotefoams Plc

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Aerospace Foams Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Aerospace Foams Market Size Outlook, $ Million, 2021 to 2032

3.2 Aerospace Foams Market Outlook by Type, $ Million, 2021 to 2032

3.3 Aerospace Foams Market Outlook by Product, $ Million, 2021 to 2032

3.4 Aerospace Foams Market Outlook by Application, $ Million, 2021 to 2032

3.5 Aerospace Foams Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Aerospace Foams Industry

4.2 Key Market Trends in Aerospace Foams Industry

4.3 Potential Opportunities in Aerospace Foams Industry

4.4 Key Challenges in Aerospace Foams Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Aerospace Foams Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Aerospace Foams Market Outlook by Segments

7.1 Aerospace Foams Market Outlook by Segments, $ Million, 2021- 2032

By Material

PU Foams

PE Foams

Melamine Foams

Metal Foams

PMI/Polyimide Foams

Others

By End-User

Commercial Aircraft

Military Aircraft

General Aviation

Others

By Application

Aircraft Seats

Aircraft Floor Carpets

Flight Deck Pads

Cabin Walls and Ceilings

Overhead Stow Bins

Others

8 North America Aerospace Foams Market Analysis and Outlook To 2032

8.1 Introduction to North America Aerospace Foams Markets in 2024

8.2 North America Aerospace Foams Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Aerospace Foams Market size Outlook by Segments, 2021-2032

By Material

PU Foams

PE Foams

Melamine Foams

Metal Foams

PMI/Polyimide Foams

Others

By End-User

Commercial Aircraft

Military Aircraft

General Aviation

Others

By Application

Aircraft Seats

Aircraft Floor Carpets

Flight Deck Pads

Cabin Walls and Ceilings

Overhead Stow Bins

Others

9 Europe Aerospace Foams Market Analysis and Outlook To 2032

9.1 Introduction to Europe Aerospace Foams Markets in 2024

9.2 Europe Aerospace Foams Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Aerospace Foams Market Size Outlook by Segments, 2021-2032

By Material

PU Foams

PE Foams

Melamine Foams

Metal Foams

PMI/Polyimide Foams

Others

By End-User

Commercial Aircraft

Military Aircraft

General Aviation

Others

By Application

Aircraft Seats

Aircraft Floor Carpets

Flight Deck Pads

Cabin Walls and Ceilings

Overhead Stow Bins

Others

10 Asia Pacific Aerospace Foams Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Aerospace Foams Markets in 2024

10.2 Asia Pacific Aerospace Foams Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Aerospace Foams Market size Outlook by Segments, 2021-2032

By Material

PU Foams

PE Foams

Melamine Foams

Metal Foams

PMI/Polyimide Foams

Others

By End-User

Commercial Aircraft

Military Aircraft

General Aviation

Others

By Application

Aircraft Seats

Aircraft Floor Carpets

Flight Deck Pads

Cabin Walls and Ceilings

Overhead Stow Bins

Others

11 South America Aerospace Foams Market Analysis and Outlook To 2032

11.1 Introduction to South America Aerospace Foams Markets in 2024

11.2 South America Aerospace Foams Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Aerospace Foams Market size Outlook by Segments, 2021-2032

By Material

PU Foams

PE Foams

Melamine Foams

Metal Foams

PMI/Polyimide Foams

Others

By End-User

Commercial Aircraft

Military Aircraft

General Aviation

Others

By Application

Aircraft Seats

Aircraft Floor Carpets

Flight Deck Pads

Cabin Walls and Ceilings

Overhead Stow Bins

Others

12 Middle East and Africa Aerospace Foams Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Aerospace Foams Markets in 2024

12.2 Middle East and Africa Aerospace Foams Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Aerospace Foams Market size Outlook by Segments, 2021-2032

By Material

PU Foams

PE Foams

Melamine Foams

Metal Foams

PMI/Polyimide Foams

Others

By End-User

Commercial Aircraft

Military Aircraft

General Aviation

Others

By Application

Aircraft Seats

Aircraft Floor Carpets

Flight Deck Pads

Cabin Walls and Ceilings

Overhead Stow Bins

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Armacell

BASF SE

Boyd Corp

DuPont de Nemours Inc

ERG Aerospace Corp

Evonik Industries AG

General Plastics Manufacturing Company

NCFI Polyurethanes

Recticel NV/SA

Rogers Corp

SABIC

Solvay S.A.

UFP Technologies Inc

Zotefoams Plc

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Material

PU Foams

PE Foams

Melamine Foams

Metal Foams

PMI/Polyimide Foams

Others

By End-User

Commercial Aircraft

Military Aircraft

General Aviation

Others

By Application

Aircraft Seats

Aircraft Floor Carpets

Flight Deck Pads

Cabin Walls and Ceilings

Overhead Stow Bins

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)