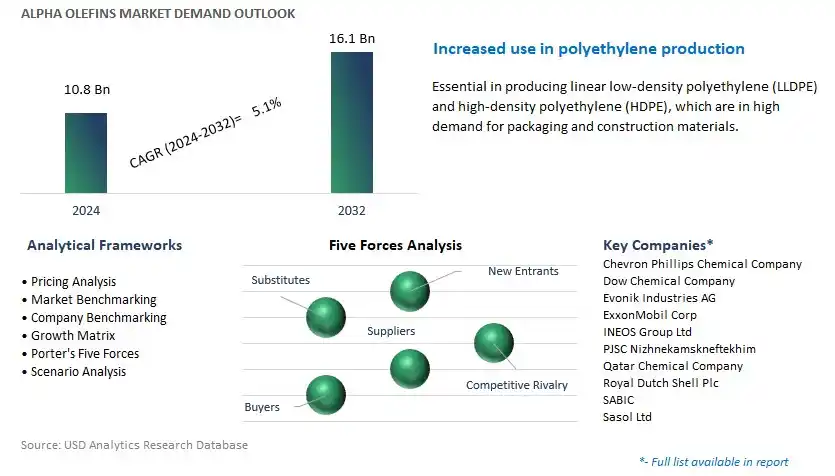

Global Alpha Olefins Market Size is valued at $10.8 Billion in 2024 and is forecast to register a growth rate (CAGR) of 5.1% to reach $16.1 Billion by 2032.

The global Alpha Olefins Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (1-Hexene, 1-Octene, 1-Butene, Others), By Application (Polyolefins comonomer, Surfactants and intermediates, Lubricants, Fine chemicals, Plasticizer, Oil field chemicals, Others).

An Introduction to Alpha Olefins Market in 2024

Alpha olefins are a group of linear, unbranched hydrocarbons with a terminal double bond, typically derived from ethylene through ethylene oligomerization or Fischer-Tropsch synthesis. These olefins serve as essential building blocks for the production of a wide range of chemicals and polymers. The market for alpha olefins is driven by their versatility and reactivity, which allow for the synthesis of various high-value products, including polyethylene, plasticizers, lubricants, and detergents. Alpha olefins exhibit excellent chemical and thermal stability, making them valuable intermediates in the manufacturing of specialty chemicals such as surfactants, detergents, and lubricant additives. Further, advancements in olefin production technologies, such as metathesis and catalytic oligomerization, are expanding the range of alpha olefin derivatives and driving innovation within the market. As industries seek sustainable and cost-effective solutions, alpha olefins play a crucial role in enabling the development of environmentally friendly materials and chemicals.

Alpha Olefins Market Competitive Landscape

The market report analyses the leading companies in the industry including Chevron Phillips Chemical Company, Dow Chemical Company, Evonik Industries AG, ExxonMobil Corp, INEOS Group Ltd, PJSC Nizhnekamskneftekhim, Qatar Chemical Company, Royal Dutch Shell Plc, SABIC, Sasol Ltd, and others.

Alpha Olefins Market Dynamics

Market Trend: Increasing Demand for Polyethylene and Polyalphaolefins

A significant market trend for Alpha Olefins is the increasing demand for polyethylene and polyalphaolefins (PAO), driven by their versatile applications in various industries such as packaging, automotive, construction, and lubricants. Alpha olefins serve as key raw materials in the production of linear low-density polyethylene (LLDPE), high-density polyethylene (HDPE), and PAO, which are used in manufacturing plastics, synthetic lubricants, adhesives, and other specialty chemicals. With the growing global population, urbanization, and industrialization, there is a rising need for polymers and lubricants that offer properties such as strength, flexibility, chemical resistance, and thermal stability. This trend reflects a broader industry shift towards the use of alpha olefins as feedstocks for high-performance materials that meet the evolving needs of modern applications and end-users.

Market Driver: Expansion of Petrochemical and Chemical Industries

A significant market driver for Alpha Olefins is the expansion of petrochemical and chemical industries worldwide, where alpha olefins are essential building blocks for the synthesis of various downstream products. With increasing demand for plastics, synthetic rubbers, surfactants, and detergents, there is a growing need for alpha olefins as intermediates in chemical manufacturing processes. Alpha olefins are produced through ethylene oligomerization or Fischer-Tropsch synthesis, primarily from petroleum-based feedstocks such as ethylene or natural gas liquids (NGLs). The growth in petrochemical and chemical industries, driven by economic development, infrastructure projects, and consumer demand, stimulates the demand for alpha olefins and supports market expansion in the alpha olefins industry.

Market Opportunity: Development of Bio-Based Alpha Olefins

An attractive opportunity in the Alpha Olefins market lies in the development of bio-based alpha olefins derived from renewable feedstocks such as plant oils, biomass, or waste materials. With increasing environmental awareness, sustainability goals, and regulatory pressures to reduce carbon emissions and reliance on fossil fuels, there is a growing interest in bio-based alternatives to petroleum-derived alpha olefins. Bio-based alpha olefins offer advantages such as reduced environmental impact, lower greenhouse gas emissions, and potential cost competitiveness compared to traditional petrochemicals. By investing in research and development, partnering with biotechnology firms, and leveraging innovative production technologies such as fermentation or enzymatic processes, alpha olefins manufacturers can capitalize on the demand for sustainable solutions, expand their product portfolio, and gain a competitive edge in the bio-based alpha olefins market.

Alpha Olefins Market Share Analysis: 1-Hexene is poised to register the fastest CAGR over the forecast period

1-Hexene is the largest and fastest-growing segment in the Alpha Olefins market. The large revenue share is attributed to its extensive application in the production of polyethylene, particularly high-density polyethylene (HDPE) and linear low-density polyethylene (LLDPE). These materials are essential in manufacturing a wide range of products, including plastic films, pipes, and containers, which are in high demand across various industries such as packaging, automotive, and construction. The robust growth of these industries, driven by urbanization and increasing consumer goods consumption, significantly boosts the demand for 1-Hexene. Furthermore, advancements in polymerization technologies and the development of more efficient and sustainable production methods for alpha olefins enhance the supply capabilities and cost-effectiveness of 1-Hexene, supporting its leading position in the market. As manufacturers continue to innovate and expand their production capacities, 1-Hexene remains a critical component in meeting the rising global demand for advanced polyethylene products.

Alpha Olefins Market Share Analysis: Polyolefins Comonomer is poised to register the fastest CAGR over the forecast period

The polyolefins comonomer segment is the fastest-growing segment in the Alpha Olefins market. This rapid growth is primarily driven by the escalating demand for high-performance polyethylene products, such as high-density polyethylene (HDPE) and linear low-density polyethylene (LLDPE), which are integral in the production of durable plastic goods. Polyolefins comonomers like 1-Hexene and 1-Octene are essential in enhancing the properties of these polyolefins, providing improved strength, flexibility, and resistance to environmental stress. The increasing use of HDPE and LLDPE in packaging, automotive parts, construction materials, and consumer goods amplifies the demand for alpha olefins as comonomers. Additionally, the shift towards sustainable and lightweight packaging solutions further propels the market, as industries seek materials that are both cost-effective and environmentally friendly. The continuous advancements in polymerization technologies and the expansion of polyolefin production capacities globally also contribute significantly to the growth of this segment, ensuring a steady supply to meet the burgeoning demand. Consequently, the polyolefins comonomer segment stands out as a pivotal driver of growth within the Alpha Olefins market.

Alpha Olefins Market

By Type

1-Hexene

1-Octene

1-Butene

Others

By Application

Polyolefins comonomer

Surfactants and intermediates

Lubricants

Fine chemicals

Plasticizer

Oil field chemicals

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Alpha Olefins Companies Profiled in the Study

Chevron Phillips Chemical Company

Dow Chemical Company

Evonik Industries AG

ExxonMobil Corp

INEOS Group Ltd

PJSC Nizhnekamskneftekhim

Qatar Chemical Company

Royal Dutch Shell Plc

SABIC

Sasol Ltd

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Alpha Olefins Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Alpha Olefins Market Size Outlook, $ Million, 2021 to 2032

3.2 Alpha Olefins Market Outlook by Type, $ Million, 2021 to 2032

3.3 Alpha Olefins Market Outlook by Product, $ Million, 2021 to 2032

3.4 Alpha Olefins Market Outlook by Application, $ Million, 2021 to 2032

3.5 Alpha Olefins Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Alpha Olefins Industry

4.2 Key Market Trends in Alpha Olefins Industry

4.3 Potential Opportunities in Alpha Olefins Industry

4.4 Key Challenges in Alpha Olefins Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Alpha Olefins Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Alpha Olefins Market Outlook by Segments

7.1 Alpha Olefins Market Outlook by Segments, $ Million, 2021- 2032

By Type

1-Hexene

1-Octene

1-Butene

Others

By Application

Polyolefins comonomer

Surfactants and intermediates

Lubricants

Fine chemicals

Plasticizer

Oil field chemicals

Others

8 North America Alpha Olefins Market Analysis and Outlook To 2032

8.1 Introduction to North America Alpha Olefins Markets in 2024

8.2 North America Alpha Olefins Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Alpha Olefins Market size Outlook by Segments, 2021-2032

By Type

1-Hexene

1-Octene

1-Butene

Others

By Application

Polyolefins comonomer

Surfactants and intermediates

Lubricants

Fine chemicals

Plasticizer

Oil field chemicals

Others

9 Europe Alpha Olefins Market Analysis and Outlook To 2032

9.1 Introduction to Europe Alpha Olefins Markets in 2024

9.2 Europe Alpha Olefins Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Alpha Olefins Market Size Outlook by Segments, 2021-2032

By Type

1-Hexene

1-Octene

1-Butene

Others

By Application

Polyolefins comonomer

Surfactants and intermediates

Lubricants

Fine chemicals

Plasticizer

Oil field chemicals

Others

10 Asia Pacific Alpha Olefins Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Alpha Olefins Markets in 2024

10.2 Asia Pacific Alpha Olefins Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Alpha Olefins Market size Outlook by Segments, 2021-2032

By Type

1-Hexene

1-Octene

1-Butene

Others

By Application

Polyolefins comonomer

Surfactants and intermediates

Lubricants

Fine chemicals

Plasticizer

Oil field chemicals

Others

11 South America Alpha Olefins Market Analysis and Outlook To 2032

11.1 Introduction to South America Alpha Olefins Markets in 2024

11.2 South America Alpha Olefins Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Alpha Olefins Market size Outlook by Segments, 2021-2032

By Type

1-Hexene

1-Octene

1-Butene

Others

By Application

Polyolefins comonomer

Surfactants and intermediates

Lubricants

Fine chemicals

Plasticizer

Oil field chemicals

Others

12 Middle East and Africa Alpha Olefins Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Alpha Olefins Markets in 2024

12.2 Middle East and Africa Alpha Olefins Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Alpha Olefins Market size Outlook by Segments, 2021-2032

By Type

1-Hexene

1-Octene

1-Butene

Others

By Application

Polyolefins comonomer

Surfactants and intermediates

Lubricants

Fine chemicals

Plasticizer

Oil field chemicals

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Chevron Phillips Chemical Company

Dow Chemical Company

Evonik Industries AG

ExxonMobil Corp

INEOS Group Ltd

PJSC Nizhnekamskneftekhim

Qatar Chemical Company

Royal Dutch Shell Plc

SABIC

Sasol Ltd

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

1-Hexene

1-Octene

1-Butene

Others

By Application

Polyolefins comonomer

Surfactants and intermediates

Lubricants

Fine chemicals

Plasticizer

Oil field chemicals

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)