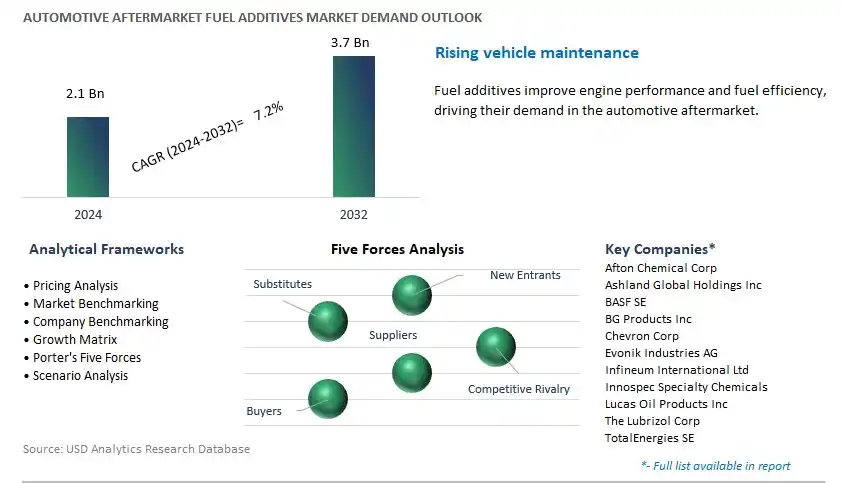

Global Automotive Aftermarket Fuel Additives Market Size is valued at $2.1 Billion in 2024 and is forecast to register a growth rate (CAGR) of 7.2% to reach $3.7 Billion by 2032.

The global Automotive Aftermarket Fuel Additives Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Application (Gasoline, Diesel), By Distribution Channel (Big Stores, 4S Stores, Unauthorized Centers, Gas Stations), By Supply Mode (Third Party, OEM).

An Introduction to Automotive Aftermarket Fuel Additives Market in 2024

Automotive aftermarket fuel additives are chemical formulations designed to enhance the performance, efficiency, and longevity of internal combustion engines by improving fuel quality and combustion characteristics. These additives are typically added to gasoline or diesel fuel to address common issues such as engine deposits, corrosion, lubrication, and emissions. The market for automotive aftermarket fuel additives is driven by the increasing demand for solutions to optimize engine performance, reduce emissions, and prolong engine life. Fuel additives can improve fuel stability, prevent corrosion in fuel systems, clean fuel injectors, and enhance combustion efficiency, leading to smoother operation, reduced fuel consumption, and lower emissions. Additionally, fuel additives are used to address specific issues such as ethanol corrosion protection, water removal, and cold weather operability. Further, advancements in additive chemistry, including multi-functional formulations and nano-additives, are driving innovation and growth within the market. As vehicle owners seek ways to improve fuel economy, reduce maintenance costs, and meet regulatory requirements, automotive aftermarket fuel additives offer a convenient and cost-effective solution for optimizing engine performance and fuel efficiency.

Automotive Aftermarket Fuel Additives Market Competitive Landscape

The market report analyses the leading companies in the industry including Afton Chemical Corp, Ashland Global Holdings Inc, BASF SE, BG Products Inc, Chevron Corp, Evonik Industries AG, Infineum International Ltd, Innospec Specialty Chemicals, Lucas Oil Products Inc, The Lubrizol Corp, TotalEnergies SE, and others.

Automotive Aftermarket Fuel Additives Market Dynamics

Market Trend: Increasing Focus on Fuel Efficiency and Emissions Reduction

A significant market trend for Automotive Aftermarket Fuel Additives is the increasing focus on fuel efficiency and emissions reduction driven by stringent environmental regulations, rising fuel prices, and consumer demand for cleaner and more efficient vehicles. As governments worldwide implement stricter emission standards to combat air pollution and climate change, there is a growing need for automotive aftermarket fuel additives that optimize engine performance, improve fuel economy, and reduce harmful emissions. Automotive aftermarket fuel additives, including octane boosters, cetane improvers, fuel stabilizers, and fuel system cleaners, offer motorists a cost-effective solution to enhance vehicle performance, prolong engine life, and lower fuel consumption. This trend reflects a broader industry shift towards sustainable transportation solutions, driving the adoption of aftermarket fuel additives as a proactive measure to reduce vehicle emissions and mitigate environmental impact.

Market Driver: Increasing Vehicle Fleet Age and Maintenance Awareness

A significant market driver for Automotive Aftermarket Fuel Additives is the increasing vehicle fleet age and growing awareness of the importance of vehicle maintenance among consumers. As vehicles age, engine performance may degrade due to carbon buildup, fuel system deposits, and wear and tear, leading to decreased fuel efficiency, increased emissions, and reduced overall reliability. Automotive aftermarket fuel additives offer motorists a convenient and cost-effective way to address common fuel-related issues, such as fuel system fouling, injector clogging, and fuel quality deterioration, without the need for costly engine repairs or component replacements. The rising awareness of the benefits of regular maintenance and preventive care drives the demand for aftermarket fuel additives as part of a comprehensive vehicle maintenance regimen, supporting market growth in the automotive aftermarket segment.

Market Opportunity: Innovation in Advanced Fuel Additive Formulations

An attractive opportunity in the Automotive Aftermarket Fuel Additives market lies in innovation in advanced fuel additive formulations tailored to address specific engine types, fuel compositions, and performance requirements. Manufacturers can capitalize on the opportunity to develop next-generation fuel additives that offer superior cleaning, lubricating, and performance-enhancing properties, enabling motorists to maximize fuel efficiency, engine power, and emissions control. Opportunities exist to develop multifunctional additives that target multiple fuel-related issues simultaneously, such as improving combustion efficiency, reducing friction and wear, and minimizing harmful emissions. Additionally, there is an opportunity to innovate in the area of alternative fuels and alternative propulsion systems, such as electric vehicles and hybrid vehicles, by developing specialized additives that optimize performance and compatibility with emerging fuel technologies. By investing in research and development, collaborating with automotive OEMs and fuel suppliers, and leveraging advanced testing and validation methods, companies can differentiate themselves in the market, meet evolving customer needs, and capitalize on opportunities for growth and innovation in the automotive aftermarket fuel additives industry.

Automotive Aftermarket Fuel Additives Market Share Analysis: Gasoline generated the highest revenue in 2024

Within the Automotive Aftermarket Fuel Additives Market, the Gasoline segment is the largest segment. Gasoline-powered vehicles constitute a significant portion of the global automotive fleet, particularly in regions with well-established transportation infrastructures. As such, there is a substantial demand for aftermarket fuel additives designed specifically for gasoline engines. These additives are formulated to address various performance issues, including engine deposits, fuel system cleanliness, octane enhancement, and emissions reduction. Additionally, gasoline additives often contain detergents, dispersants, and corrosion inhibitors to maintain engine efficiency and prolong component life. With consumers increasingly seeking ways to optimize vehicle performance, improve fuel economy, and reduce emissions, the demand for gasoline aftermarket fuel additives continues to grow. Moreover, stringent environmental regulations and evolving engine technologies further drive the need for innovative additives tailored to gasoline-powered vehicles. As a result, the Gasoline segment maintains its position as the largest within the Automotive Aftermarket Fuel Additives Market.

Automotive Aftermarket Fuel Additives Market Share Analysis: Gas Stations is poised to register the fastest CAGR over the forecast period

Among the options provided, the Gas Stations segment is experiencing rapid growth within the Automotive Aftermarket Fuel Additives Market. Gas stations serve as convenient points of access for consumers seeking automotive aftermarket fuel additives. With the increasing complexity of modern engines and the demand for improved fuel efficiency and performance, drivers are turning to fuel additives as a cost-effective solution to address various fuel-related issues. Gas stations capitalize on this trend by stocking a diverse range of aftermarket fuel additives, providing consumers with easy access to these products during routine refuelling stops. Additionally, gas stations often promote and recommend fuel additives through signage, promotional materials, and direct interaction with customers, further driving sales. Moreover, the proliferation of gas stations, especially in urban and suburban areas, ensures widespread availability of aftermarket fuel additives, contributing to the segment's rapid growth. As consumers prioritize vehicle maintenance and performance optimization, the Gas Stations segment continues to expand, solidifying its position as the fastest-growing distribution channel in the Automotive Aftermarket Fuel Additives Market.

Automotive Aftermarket Fuel Additives Market Share Analysis: Third Party generated the highest revenue in 2024

Within the Automotive Aftermarket Fuel Additives Market, the Third-Party segment is the largest segment. Third-party suppliers of aftermarket fuel additives offer a wide range of products tailored to meet the specific needs and preferences of consumers. These suppliers often specialize in developing innovative formulations designed to address various fuel-related issues, including engine deposits, fuel system cleanliness, lubrication enhancement, and emissions reduction. Moreover, third-party suppliers typically have extensive distribution networks and marketing strategies that enable them to reach a broader customer base, including independent auto repair shops, online retailers, and automotive supply stores. Additionally, third-party suppliers often offer competitive pricing and personalized customer service, further attracting consumers seeking high-quality aftermarket fuel additives. As consumers increasingly prioritize vehicle maintenance and performance optimization, the Third-Party segment continues to expand, solidifying its position as the largest within the Automotive Aftermarket Fuel Additives Market.

Automotive Aftermarket Fuel Additives Market

By Application

Gasoline

Diesel

By Distribution Channel

Big Stores

4S Stores

Unauthorized Centers

Gas Stations

By Supply Mode

Third Party

OEMCountries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Automotive Aftermarket Fuel Additives Companies Profiled in the Study

Afton Chemical Corp

Ashland Global Holdings Inc

BASF SE

BG Products Inc

Chevron Corp

Evonik Industries AG

Infineum International Ltd

Innospec Specialty Chemicals

Lucas Oil Products Inc

The Lubrizol Corp

TotalEnergies SE

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Automotive Aftermarket Fuel Additives Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Automotive Aftermarket Fuel Additives Market Size Outlook, $ Million, 2021 to 2032

3.2 Automotive Aftermarket Fuel Additives Market Outlook by Type, $ Million, 2021 to 2032

3.3 Automotive Aftermarket Fuel Additives Market Outlook by Product, $ Million, 2021 to 2032

3.4 Automotive Aftermarket Fuel Additives Market Outlook by Application, $ Million, 2021 to 2032

3.5 Automotive Aftermarket Fuel Additives Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Automotive Aftermarket Fuel Additives Industry

4.2 Key Market Trends in Automotive Aftermarket Fuel Additives Industry

4.3 Potential Opportunities in Automotive Aftermarket Fuel Additives Industry

4.4 Key Challenges in Automotive Aftermarket Fuel Additives Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Automotive Aftermarket Fuel Additives Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Automotive Aftermarket Fuel Additives Market Outlook by Segments

7.1 Automotive Aftermarket Fuel Additives Market Outlook by Segments, $ Million, 2021- 2032

By Application

Gasoline

Diesel

By Distribution Channel

Big Stores

4S Stores

Unauthorized Centers

Gas Stations

By Supply Mode

Third Party

OEM

8 North America Automotive Aftermarket Fuel Additives Market Analysis and Outlook To 2032

8.1 Introduction to North America Automotive Aftermarket Fuel Additives Markets in 2024

8.2 North America Automotive Aftermarket Fuel Additives Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Automotive Aftermarket Fuel Additives Market size Outlook by Segments, 2021-2032

By Application

Gasoline

Diesel

By Distribution Channel

Big Stores

4S Stores

Unauthorized Centers

Gas Stations

By Supply Mode

Third Party

OEM

9 Europe Automotive Aftermarket Fuel Additives Market Analysis and Outlook To 2032

9.1 Introduction to Europe Automotive Aftermarket Fuel Additives Markets in 2024

9.2 Europe Automotive Aftermarket Fuel Additives Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Automotive Aftermarket Fuel Additives Market Size Outlook by Segments, 2021-2032

By Application

Gasoline

Diesel

By Distribution Channel

Big Stores

4S Stores

Unauthorized Centers

Gas Stations

By Supply Mode

Third Party

OEM

10 Asia Pacific Automotive Aftermarket Fuel Additives Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Automotive Aftermarket Fuel Additives Markets in 2024

10.2 Asia Pacific Automotive Aftermarket Fuel Additives Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Automotive Aftermarket Fuel Additives Market size Outlook by Segments, 2021-2032

By Application

Gasoline

Diesel

By Distribution Channel

Big Stores

4S Stores

Unauthorized Centers

Gas Stations

By Supply Mode

Third Party

OEM

11 South America Automotive Aftermarket Fuel Additives Market Analysis and Outlook To 2032

11.1 Introduction to South America Automotive Aftermarket Fuel Additives Markets in 2024

11.2 South America Automotive Aftermarket Fuel Additives Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Automotive Aftermarket Fuel Additives Market size Outlook by Segments, 2021-2032

By Application

Gasoline

Diesel

By Distribution Channel

Big Stores

4S Stores

Unauthorized Centers

Gas Stations

By Supply Mode

Third Party

OEM

12 Middle East and Africa Automotive Aftermarket Fuel Additives Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Automotive Aftermarket Fuel Additives Markets in 2024

12.2 Middle East and Africa Automotive Aftermarket Fuel Additives Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Automotive Aftermarket Fuel Additives Market size Outlook by Segments, 2021-2032

By Application

Gasoline

Diesel

By Distribution Channel

Big Stores

4S Stores

Unauthorized Centers

Gas Stations

By Supply Mode

Third Party

OEM

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Afton Chemical Corp

Ashland Global Holdings Inc

BASF SE

BG Products Inc

Chevron Corp

Evonik Industries AG

Infineum International Ltd

Innospec Specialty Chemicals

Lucas Oil Products Inc

The Lubrizol Corp

TotalEnergies SE

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Application

Gasoline

Diesel

By Distribution Channel

Big Stores

4S Stores

Unauthorized Centers

Gas Stations

By Supply Mode

Third Party

OEM

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)