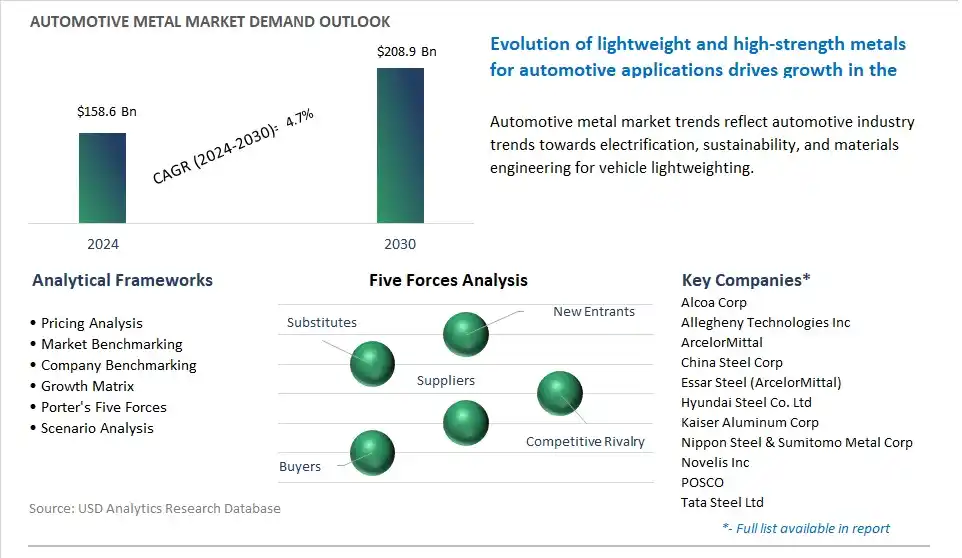

The global Automotive Metal Market is poised to register a 4.7% CAGR from $158.6 Billion in 2024 to $208.9 Billion in 2030.

The global Automotive Metal Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Product (Aluminum, Steel, Magnesium, Others), By Application (Body Structure, Power Train, Suspension, Others), By Vehicle (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles).

An Introduction to Global Automotive Metal Market in 2024

The market for automotive metals is experiencing growth driven by the increasing demand for lightweight, high-strength materials to improve vehicle fuel efficiency, performance, and safety. Key trends shaping the future of the industry include innovations in metal alloys, forming processes, and joining technologies to meet the requirements for reducing vehicle weight, enhancing structural integrity, and enabling design flexibility. Advanced automotive metals offer benefits such as high tensile strength, crashworthiness, corrosion resistance, and recyclability, making them essential for manufacturing body panels, chassis components, and powertrain parts in modern vehicles. Moreover, the integration of advanced manufacturing techniques, such as hot stamping, hydroforming, and laser welding, enables automakers to produce complex parts with superior strength-to-weight ratios and dimensional accuracy, contributing to overall vehicle performance and durability. Additionally, the growing emphasis on electric mobility, autonomous driving, and sustainability drives market demand for automotive metals that support lightweighting, energy efficiency, and emission reductions while meeting stringent safety and regulatory standards. As automotive manufacturers transition to electric and autonomous vehicles and adopt advanced materials and manufacturing processes, the automotive metals market is poised for continued growth and innovation as a critical enabler of next-generation automotive technologies and solutions.

Automotive Metal Market Competitive Landscape

The market report analyses the leading companies in the industry including Alcoa Corp, Allegheny Technologies Inc, ArcelorMittal, China Steel Corp, Essar Steel (ArcelorMittal), Hyundai Steel Co. Ltd, Kaiser Aluminum Corp, Nippon Steel & Sumitomo Metal Corp, Novelis Inc, POSCO, Tata Steel Ltd, thyssenkrupp AG, United States Steel Corp, voestalpine AG.

Automotive Metal Market Dynamics

Automotive Metal Market Trend: Increasing Demand for Lightweight Materials

A prominent trend in the automotive metal market is the increasing demand for lightweight materials in vehicle manufacturing. With the automotive industry shifting towards electric vehicles (EVs) and stricter fuel efficiency standards, there is a growing emphasis on reducing vehicle weight to improve fuel economy and extend driving range. Lightweight metals such as aluminum, magnesium, and advanced high-strength steel (AHSS) are gaining traction as preferred materials for automotive components such as body panels, chassis structures, and powertrain components. This trend is driven by consumer preferences for fuel-efficient vehicles, regulatory requirements for emissions reduction, and technological advancements in materials science and manufacturing processes, shaping the future of the automotive metal market towards greater adoption of lightweight solutions.

Automotive Metal Market Driver: Innovation in Automotive Design and Manufacturing

The primary driver behind the growth of the automotive metal market is innovation in automotive design and manufacturing. With the rise of electric and autonomous vehicles, there is a need for innovative materials and manufacturing techniques that can meet the performance, safety, and sustainability requirements of next-generation vehicles. Automotive manufacturers are investing in lightweight metals, advanced alloys, and novel fabrication methods to improve vehicle efficiency, performance, and structural integrity. Moreover, advancements in metal forming, joining, and assembly technologies enable the production of complex and lightweight automotive components with improved strength-to-weight ratios, driving market growth and investment in automotive metal solutions.

Automotive Metal Market Opportunity: Expansion into Electric Vehicle (EV) Components

An opportunity for market growth within the automotive metal sector lies in the expansion into electric vehicle (EV) components and systems. As the automotive industry transitions towards electrification, there is a growing demand for lightweight metals and advanced materials for EV battery enclosures, chassis structures, thermal management systems, and power electronics. Lightweight metals offer advantages such as high energy efficiency, fast charging capabilities, and improved vehicle dynamics for electric vehicles. By focusing on developing specialized alloys, fabrication techniques, and component designs tailored to the unique requirements of electric vehicles, automotive metal manufacturers can capitalize on the growing EV market, secure partnerships with EV manufacturers, and diversify their product portfolios to meet evolving industry needs. Additionally, collaboration with EV battery manufacturers, research institutions, and government agencies enables automotive metal suppliers to stay at the forefront of innovation and drive market growth in the rapidly evolving electric mobility sector.

Automotive Metal Market Share Analysis: Steel segment generated the highest revenue in the industry

The steel segment is the largest segment in the Automotive Metal Market for diverse compelling reasons. The steel has been a traditional and dominant material used in automotive manufacturing for decades due to its excellent combination of strength, formability, durability, and cost-effectiveness. Steel provides structural integrity to vehicles and offers superior crashworthiness and occupant protection, meeting stringent safety standards and regulatory requirements in the automotive industry. Additionally, advancements in steel manufacturing technologies, such as advanced high-strength steels (AHSS) and ultra-high-strength steels (UHSS), have enabled the development of lightweight yet strong steel grades that help reduce vehicle weight without compromising safety or performance. In addition, steel remains the material of choice for critical automotive components such as chassis, body panels, frames, and structural reinforcements due to its versatility and compatibility with various manufacturing processes, including stamping, welding, and forming. Further, the widespread availability of steel, established supply chains, and cost-effective production processes contribute to its dominance in the automotive industry. As automakers continue to prioritize lightweighting initiatives, fuel efficiency, and sustainability, steel retains its position as the largest segment in the Automotive Metal Market.

Automotive Metal Market Share Analysis: Power Train Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The Power Train segment is the fastest-growing segment in the Automotive Metal Market for diverse compelling reasons. The the power train system plays a critical role in vehicle performance, efficiency, and drivability, encompassing components such as engines, transmissions, drivelines, and axles. These components require materials with high strength, durability, and thermal conductivity to withstand the stresses and operating conditions encountered during vehicle operation. Additionally, advancements in automotive power train technology, including the development of electric and hybrid power trains, have increased the demand for lightweight yet durable materials to improve energy efficiency and range. Metals such as aluminum and magnesium are increasingly used in power train components to reduce weight and enhance performance. In addition, the shift towards electrification and the adoption of lightweight materials in power train systems contribute to the growth of the Power Train segment in the Automotive Metal Market. Further, stringent emissions regulations and fuel economy standards drive the automotive industry's focus on power train efficiency and optimization, further boosting the demand for advanced metal alloys in power train applications. As automakers continue to innovate and invest in power train technologies to meet regulatory requirements and consumer preferences for performance and sustainability, the Power Train segment is expected to experience rapid growth, positioning it as the fastest-growing segment in the Automotive Metal Market.

Automotive Metal Market Share Analysis: Passenger Cars Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The Passenger Cars segment is the fastest-growing segment in the Automotive Metal Market for diverse compelling reasons. The the passenger car segment represents the largest share of the automotive market in terms of production and sales volume globally. As consumer preferences shift towards smaller, more fuel-efficient vehicles with advanced features and technology, automakers are increasingly focusing on lightweighting initiatives to improve fuel economy and reduce emissions. Additionally, the growing demand for electric and hybrid vehicles further accelerates the adoption of lightweight materials in passenger cars to enhance range and performance. Metals such as aluminum, high-strength steel, and advanced alloys are increasingly used in passenger car manufacturing to reduce weight while maintaining structural integrity and safety. In addition, the automotive industry's emphasis on design flexibility, crashworthiness, and recyclability drives the use of advanced metal alloys in passenger car construction. Further, the introduction of stringent emissions regulations and fuel economy standards worldwide encourages automakers to invest in lightweight materials and innovative manufacturing processes to meet regulatory requirements. As passenger car manufacturers continue to prioritize lightweighting strategies and adopt advanced metal technologies to improve vehicle performance and sustainability, the Passenger Cars segment is expected to experience rapid growth, positioning it as the fastest-growing segment in the Automotive Metal Market.

Automotive Metal Market Report Segmentation

By Product

Aluminum

Steel

Magnesium

Others

By Application

Body Structure

Power Train

Suspension

Others

By Vehicle

Passenger Cars

Light Commercial Vehicles

Heavy Commercial Vehicles

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Automotive Metal Companies Profiled in the Market Study

Alcoa Corp

Allegheny Technologies Inc

ArcelorMittal

China Steel Corp

Essar Steel (ArcelorMittal)

Hyundai Steel Co. Ltd

Kaiser Aluminum Corp

Nippon Steel & Sumitomo Metal Corp

Novelis Inc

POSCO

Tata Steel Ltd

thyssenkrupp AG

United States Steel Corp

voestalpine AG

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Automotive Metal Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Automotive Metal Market Size Outlook, $ Million, 2021 to 2030

3.2 Automotive Metal Market Outlook by Type, $ Million, 2021 to 2030

3.3 Automotive Metal Market Outlook by Product, $ Million, 2021 to 2030

3.4 Automotive Metal Market Outlook by Application, $ Million, 2021 to 2030

3.5 Automotive Metal Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Automotive Metal Industry

4.2 Key Market Trends in Automotive Metal Industry

4.3 Potential Opportunities in Automotive Metal Industry

4.4 Key Challenges in Automotive Metal Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Automotive Metal Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Automotive Metal Market Outlook by Segments

7.1 Automotive Metal Market Outlook by Segments, $ Million, 2021- 2030

By Product

Aluminum

Steel

Magnesium

Others

By Application

Body Structure

Power Train

Suspension

Others

By Vehicle

Passenger Cars

Light Commercial Vehicles

Heavy Commercial Vehicles

8 North America Automotive Metal Market Analysis and Outlook To 2030

8.1 Introduction to North America Automotive Metal Markets in 2024

8.2 North America Automotive Metal Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Automotive Metal Market size Outlook by Segments, 2021-2030

By Product

Aluminum

Steel

Magnesium

Others

By Application

Body Structure

Power Train

Suspension

Others

By Vehicle

Passenger Cars

Light Commercial Vehicles

Heavy Commercial Vehicles

9 Europe Automotive Metal Market Analysis and Outlook To 2030

9.1 Introduction to Europe Automotive Metal Markets in 2024

9.2 Europe Automotive Metal Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Automotive Metal Market Size Outlook by Segments, 2021-2030

By Product

Aluminum

Steel

Magnesium

Others

By Application

Body Structure

Power Train

Suspension

Others

By Vehicle

Passenger Cars

Light Commercial Vehicles

Heavy Commercial Vehicles

10 Asia Pacific Automotive Metal Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Automotive Metal Markets in 2024

10.2 Asia Pacific Automotive Metal Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Automotive Metal Market size Outlook by Segments, 2021-2030

By Product

Aluminum

Steel

Magnesium

Others

By Application

Body Structure

Power Train

Suspension

Others

By Vehicle

Passenger Cars

Light Commercial Vehicles

Heavy Commercial Vehicles

11 South America Automotive Metal Market Analysis and Outlook To 2030

11.1 Introduction to South America Automotive Metal Markets in 2024

11.2 South America Automotive Metal Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Automotive Metal Market size Outlook by Segments, 2021-2030

By Product

Aluminum

Steel

Magnesium

Others

By Application

Body Structure

Power Train

Suspension

Others

By Vehicle

Passenger Cars

Light Commercial Vehicles

Heavy Commercial Vehicles

12 Middle East and Africa Automotive Metal Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Automotive Metal Markets in 2024

12.2 Middle East and Africa Automotive Metal Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Automotive Metal Market size Outlook by Segments, 2021-2030

By Product

Aluminum

Steel

Magnesium

Others

By Application

Body Structure

Power Train

Suspension

Others

By Vehicle

Passenger Cars

Light Commercial Vehicles

Heavy Commercial Vehicles

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Alcoa Corp

Allegheny Technologies Inc

ArcelorMittal

China Steel Corp

Essar Steel (ArcelorMittal)

Hyundai Steel Co. Ltd

Kaiser Aluminum Corp

Nippon Steel & Sumitomo Metal Corp

Novelis Inc

POSCO

Tata Steel Ltd

thyssenkrupp AG

United States Steel Corp

voestalpine AG

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Product

Aluminum

Steel

Magnesium

Others

By Application

Body Structure

Power Train

Suspension

Others

By Vehicle

Passenger Cars

Light Commercial Vehicles

Heavy Commercial Vehicles

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)