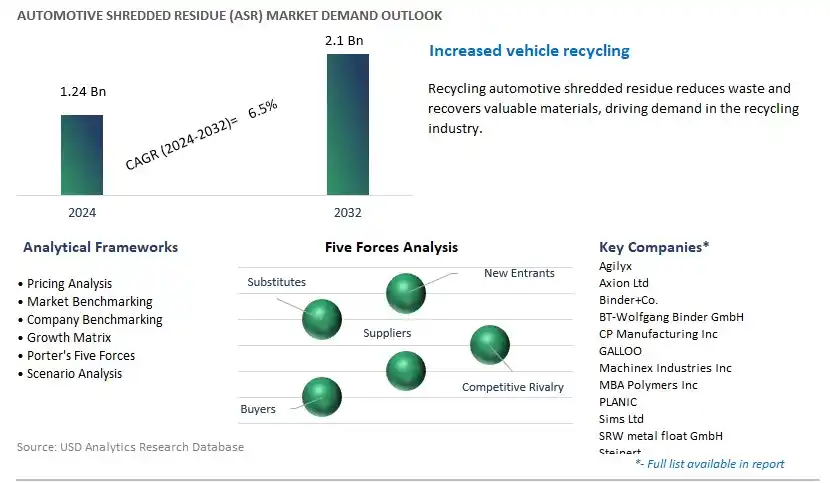

Global Automotive Shredded Residue (ASR) Market Size is valued at $1.24 Billion in 2024 and is forecast to register a growth rate (CAGR) of 6.5% to reach $2.1 Billion by 2032.

The global Automotive Shredded Residue (ASR) Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Application (Landfill, Energy recovery, Recycling), By Composition (Metals, Plastics, Rubber, Textile, Others), By Technology (Air classification, Optical sorting, Magnetic separation, Eddy current separation, Screening, Others).

An Introduction to Automotive Shredded Residue (ASR) Market in 2024

Automotive shredded residue (ASR) refers to the non-metallic waste materials generated during the recycling process of end-of-life vehicles (ELVs). ASR includes various materials such as plastics, rubber, foam, textiles, glass, and residual fluids that remain after the recovery of metals from ELVs. The market for automotive shredded residue is driven by the need to manage and recycle the non-metallic components of ELVs in an environmentally sustainable manner. ASR processing facilities use mechanical and/or chemical methods to separate and recover recyclable materials from the shredded residue, such as plastics for recycling into new products or energy recovery through incineration or pyrolysis. Additionally, efforts are made to minimize the environmental impact of ASR disposal by implementing waste management practices that prioritize recycling, resource recovery, and pollution prevention. Further, advancements in ASR recycling technologies, such as automated sorting systems and innovative separation techniques, are driving innovation and growth within the market. As automotive recycling practices evolve to meet sustainability goals and regulatory requirements, the management of automotive shredded residue plays a crucial role in minimizing waste and maximizing the recovery of valuable resources from end-of-life vehicles.

Automotive Shredded Residue (ASR) Market Competitive Landscape

The market report analyses the leading companies in the industry including Agilyx, Axion Ltd, Binder+Co., BT-Wolfgang Binder GmbH, CP Manufacturing Inc, GALLOO, Machinex Industries Inc, MBA Polymers Inc, PLANIC, Sims Ltd, SRW metal float GmbH, Steinert, Tomra Systems ASA, Wendt Corp, and others.

Automotive Shredded Residue (ASR) Market Dynamics

Market Trend: Increasing Focus on Sustainable Waste Management Practices

A significant market trend for Automotive Shredded Residue is the increasing focus on sustainable waste management practices driven by environmental regulations, corporate sustainability initiatives, and consumer awareness of environmental issues. Automotive shredded residue, which consists of materials such as plastics, rubber, foam, textiles, and metals generated from the shredding and recycling of end-of-life vehicles (ELVs), presents both challenges and opportunities for waste management stakeholders. As governments worldwide implement stricter regulations to reduce landfilling and promote recycling and resource recovery, there is a growing demand for innovative solutions to manage and process automotive shredded residue in an environmentally responsible manner. This trend reflects a broader industry shift towards circular economy principles, driving the adoption of advanced recycling technologies, waste-to-energy solutions, and sustainable materials management strategies in the automotive sector.

Market Driver: Circular Economy Initiatives and Recycling Mandates

A significant market driver for Automotive Shredded Residue is the proliferation of circular economy initiatives and recycling mandates aimed at reducing waste generation, conserving resources, and minimizing environmental impact throughout the automotive value chain. With the automotive industry facing pressure to improve sustainability performance and comply with regulatory requirements, automotive manufacturers, dismantlers, recyclers, and waste management companies are seeking innovative ways to maximize the recovery and reuse of materials from end-of-life vehicles. Automotive shredded residue, if managed effectively, can serve as a valuable resource for secondary raw materials, energy recovery, and manufacturing feedstock, contributing to the circularity and resource efficiency goals of the automotive sector. The implementation of recycling mandates, extended producer responsibility (EPR) schemes, and eco-labeling programs incentivizes stakeholders to invest in infrastructure, technology, and processes for the sustainable management of automotive shredded residue, driving market growth and development in the automotive recycling industry.

Market Opportunity: Development of Advanced Recycling and Resource Recovery Technologies

An attractive opportunity in the Automotive Shredded Residue market lies in the development of advanced recycling and resource recovery technologies that enable the efficient and sustainable processing of automotive shredded residue into valuable products and materials. Manufacturers can capitalize on the opportunity to innovate in areas such as mechanical recycling, chemical recycling, pyrolysis, gasification, and waste-to-energy conversion to extract maximum value from automotive shredded residue streams. Opportunities exist to develop processes and technologies for the separation, sorting, and purification of materials such as plastics, metals, and fibers from shredded automotive waste, enabling their reuse in manufacturing new products or energy recovery applications. By investing in research and development, collaborating with industry partners, and leveraging emerging technologies such as artificial intelligence, robotics, and automation, companies can unlock the economic and environmental potential of automotive shredded residue, create new revenue streams, and contribute to the advancement of sustainable waste management practices in the automotive sector.

Automotive Shredded Residue (ASR) Market Share Analysis: Landfill generated the highest revenue in 2024

Within the Automotive Shredded Residue (ASR) Market, the Landfill segment is the largest segment. ASR consists of various materials derived from end-of-life vehicles, including plastics, rubber, foam, textiles, and metals, which are not easily recyclable or suitable for energy recovery processes. As a result, a significant portion of ASR ends up in landfills, where it is disposed of along with other municipal solid waste. Landfilling ASR remains a common practice due to the challenges associated with separating and recycling the heterogeneous mix of materials contained within ASR. Additionally, while efforts to divert ASR from landfills through recycling and energy recovery initiatives are underway, landfilling continues to be a cost-effective and convenient disposal option for ASR in many regions. Moreover, the sheer volume of end-of-life vehicles reaching the end of their useful life contributes to the substantial amount of ASR generated, further driving its disposal in landfills. As a result, the Landfill segment maintains its position as the largest within the Automotive Shredded Residue (ASR) Market.

Automotive Shredded Residue (ASR) Market Share Analysis: Plastics is poised to register the fastest CAGR over the forecast period

Among the options provided, the Plastics segment is experiencing rapid growth within the Automotive Shredded Residue (ASR) Market. ASR contains a significant proportion of plastics derived from various components of end-of-life vehicles, including interior trim, bumpers, and dashboard panels. Plastics are non-biodegradable materials that pose environmental challenges when disposed of in landfills, leading to increased efforts to divert plastic waste from landfilling through recycling and energy recovery processes. The growing emphasis on sustainability and circular economy principles has prompted automotive manufacturers and recycling facilities to invest in technologies capable of segregating, sorting, and processing ASR plastics for recycling into new products or energy recovery. Moreover, regulatory initiatives aimed at reducing landfill waste and promoting resource conservation further drive the demand for plastic recycling solutions within the automotive sector. As a result, the Plastics segment is poised for significant growth within the Automotive Shredded Residue (ASR) Market, driven by the increasing focus on plastic waste management and environmental sustainability.

Automotive Shredded Residue (ASR) Market Share Analysis: Magnetic Separation generated the highest revenue in 2024

Within the Automotive Shredded Residue (ASR) Market, the Magnetic Separation segment is the largest segment. Magnetic separation technology is widely used in the processing of ASR to recover ferrous metals such as iron and steel, which constitute a significant portion of the shredded residue generated from end-of-life vehicles. Ferrous metals are highly magnetic and can be efficiently separated from the ASR stream using magnetic separators, which employ powerful magnets to attract and extract ferrous materials from the waste stream. Moreover, ferrous metals have high recycling value and can be recycled into new steel products, making them economically viable to recover from ASR for recycling purposes. Additionally, the prevalence of magnetic separation equipment in recycling facilities and scrap yards equipped to process ASR further contributes to the dominance of the Magnetic Separation segment within the Automotive Shredded Residue (ASR) Market. As a result, magnetic separation technology remains the preferred method for recovering ferrous metals from ASR, solidifying its position as the largest segment in the market.

Automotive Shredded Residue (ASR) Market

By Application

Landfill

Energy recovery

Recycling

By Composition

Metals

Plastics

Rubber

Textile

Others

By Technology

Air classification

Optical sorting

Magnetic separation

Eddy current separation

Screening

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Automotive Shredded Residue Companies Profiled in the Study

Agilyx

Axion Ltd

Binder+Co.

BT-Wolfgang Binder GmbH

CP Manufacturing Inc

GALLOO

Machinex Industries Inc

MBA Polymers Inc

PLANIC

Sims Ltd

SRW metal float GmbH

Steinert

Tomra Systems ASA

Wendt Corp

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Automotive Shredded Residue Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Automotive Shredded Residue Market Size Outlook, $ Million, 2021 to 2032

3.2 Automotive Shredded Residue Market Outlook by Type, $ Million, 2021 to 2032

3.3 Automotive Shredded Residue Market Outlook by Product, $ Million, 2021 to 2032

3.4 Automotive Shredded Residue Market Outlook by Application, $ Million, 2021 to 2032

3.5 Automotive Shredded Residue Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Automotive Shredded Residue Industry

4.2 Key Market Trends in Automotive Shredded Residue Industry

4.3 Potential Opportunities in Automotive Shredded Residue Industry

4.4 Key Challenges in Automotive Shredded Residue Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Automotive Shredded Residue Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Automotive Shredded Residue Market Outlook by Segments

7.1 Automotive Shredded Residue Market Outlook by Segments, $ Million, 2021- 2032

By Application

Landfill

Energy recovery

Recycling

By Composition

Metals

Plastics

Rubber

Textile

Others

By Technology

Air classification

Optical sorting

Magnetic separation

Eddy current separation

Screening

Others

8 North America Automotive Shredded Residue Market Analysis and Outlook To 2032

8.1 Introduction to North America Automotive Shredded Residue Markets in 2024

8.2 North America Automotive Shredded Residue Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Automotive Shredded Residue Market size Outlook by Segments, 2021-2032

By Application

Landfill

Energy recovery

Recycling

By Composition

Metals

Plastics

Rubber

Textile

Others

By Technology

Air classification

Optical sorting

Magnetic separation

Eddy current separation

Screening

Others

9 Europe Automotive Shredded Residue Market Analysis and Outlook To 2032

9.1 Introduction to Europe Automotive Shredded Residue Markets in 2024

9.2 Europe Automotive Shredded Residue Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Automotive Shredded Residue Market Size Outlook by Segments, 2021-2032

By Application

Landfill

Energy recovery

Recycling

By Composition

Metals

Plastics

Rubber

Textile

Others

By Technology

Air classification

Optical sorting

Magnetic separation

Eddy current separation

Screening

Others

10 Asia Pacific Automotive Shredded Residue Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Automotive Shredded Residue Markets in 2024

10.2 Asia Pacific Automotive Shredded Residue Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Automotive Shredded Residue Market size Outlook by Segments, 2021-2032

By Application

Landfill

Energy recovery

Recycling

By Composition

Metals

Plastics

Rubber

Textile

Others

By Technology

Air classification

Optical sorting

Magnetic separation

Eddy current separation

Screening

Others

11 South America Automotive Shredded Residue Market Analysis and Outlook To 2032

11.1 Introduction to South America Automotive Shredded Residue Markets in 2024

11.2 South America Automotive Shredded Residue Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Automotive Shredded Residue Market size Outlook by Segments, 2021-2032

By Application

Landfill

Energy recovery

Recycling

By Composition

Metals

Plastics

Rubber

Textile

Others

By Technology

Air classification

Optical sorting

Magnetic separation

Eddy current separation

Screening

Others

12 Middle East and Africa Automotive Shredded Residue Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Automotive Shredded Residue Markets in 2024

12.2 Middle East and Africa Automotive Shredded Residue Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Automotive Shredded Residue Market size Outlook by Segments, 2021-2032

By Application

Landfill

Energy recovery

Recycling

By Composition

Metals

Plastics

Rubber

Textile

Others

By Technology

Air classification

Optical sorting

Magnetic separation

Eddy current separation

Screening

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Agilyx

Axion Ltd

Binder+Co.

BT-Wolfgang Binder GmbH

CP Manufacturing Inc

GALLOO

Machinex Industries Inc

MBA Polymers Inc

PLANIC

Sims Ltd

SRW metal float GmbH

Steinert

Tomra Systems ASA

Wendt Corp

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Application

Landfill

Energy recovery

Recycling

By Composition

Metals

Plastics

Rubber

Textile

Others

By Technology

Air classification

Optical sorting

Magnetic separation

Eddy current separation

Screening

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)