The Autotransfusion Systems Market study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments- By Product (Devices, Consumables), By Application (Cardiac Surgeries, Orthopedic Surgeries, Organ Transplantation, Others), By End-User (Hospitals, Ambulatory Surgical Centers, Others).

Autotransfusion systems represent a valuable technology in the management of blood loss during surgical procedures, allowing patients to receive their own blood (autologous blood) instead of donor blood transfusions. In 2024, autotransfusion systems encompass a variety of devices and techniques, including cell salvage systems and intraoperative blood salvage (IBS) devices, designed to collect, process, and reinfuse shed blood back into the patient during surgery. These systems utilize centrifugation or filtration methods to remove contaminants and debris from the salvaged blood, ensuring its safety and compatibility for reinfusion. Autotransfusion offers several advantages over allogeneic blood transfusions, including reduced risk of transfusion reactions, infections, and immunological complications. With advancements in device technology, blood processing techniques, and safety features, autotransfusion systems continue to evolve, offering surgeons and anesthesiologists effective strategies for managing intraoperative blood loss and minimizing the need for allogeneic blood transfusions, ultimately improving patient outcomes and reducing healthcare costs.

One prominent trend in the autotransfusion systems market is the shift towards minimally invasive surgery. As minimally invasive surgical techniques continue to gain popularity across various medical specialties, there is a growing demand for autotransfusion systems that support these procedures. Autotransfusion systems enable the collection, processing, and reinfusion of a patient's own blood during surgery, reducing the need for allogeneic blood transfusions and minimizing the risk of transfusion-related complications. This trend reflects the increasing preference among surgeons and patients for minimally invasive approaches that offer faster recovery times, reduced postoperative pain, and improved clinical outcomes, driving the adoption of autotransfusion systems in modern surgical practice.

A significant driver in the autotransfusion systems market is the concerns over blood transfusion risks and blood supply shortages. Allogeneic blood transfusions carry inherent risks such as transfusion reactions, infections, and immune sensitization, prompting healthcare providers to seek alternative strategies to minimize reliance on donor blood products. Autotransfusion systems offer a safe and effective solution by enabling the utilization of the patient's own blood, thereby reducing the exposure to allogeneic blood and associated risks. Additionally, concerns over blood supply shortages, particularly during emergencies or in regions with limited access to blood banks, drive the adoption of autotransfusion systems as a sustainable and cost-effective approach to blood management in healthcare settings, supporting patient safety and healthcare sustainability initiatives.

An emerging opportunity in the autotransfusion systems market is the expansion into emerging markets and surgical specialties. While autotransfusion systems have traditionally been used in cardiac, orthopedic, and trauma surgery, there is potential to penetrate new geographic regions and surgical disciplines where the adoption of autotransfusion technology is still nascent. This includes applications in neurosurgery, vascular surgery, obstetrics, and gynecology, where blood conservation strategies and transfusion avoidance are increasingly recognized as priorities. By expanding into emerging markets and surgical specialties, manufacturers of autotransfusion systems can capitalize on untapped opportunities, address unmet clinical needs, and drive market growth while improving patient care and outcomes across diverse healthcare settings.

Among the segments in the Autotransfusion Systems Market, the Devices segment is experiencing the fastest growth. This growth can be attributed to several factors driving the demand for autotransfusion devices in healthcare settings. Autotransfusion devices play a crucial role in intraoperative blood salvage and reinfusion, allowing for the collection and processing of a patient's own blood lost during surgery and subsequent transfusion back to the patient. The increasing emphasis on patient blood management strategies, including minimizing allogeneic blood transfusions and reducing the risk of transfusion-related complications, drives the adoption of autotransfusion devices across various surgical specialties such as cardiac surgeries, orthopedic surgeries, and organ transplantation. Additionally, advancements in autotransfusion device technology, including improved automation, closed-system design, and enhanced safety features, contribute to the growing acceptance and utilization of these devices in hospitals and ambulatory surgical centers. Furthermore, the cost-effectiveness and potential for improved patient outcomes associated with autotransfusion procedures further stimulate demand for autotransfusion devices in surgical settings. As healthcare providers prioritize blood conservation techniques and strive to minimize the use of allogeneic blood products, the Devices segment is expected to sustain its rapid growth in the Autotransfusion Systems Market.

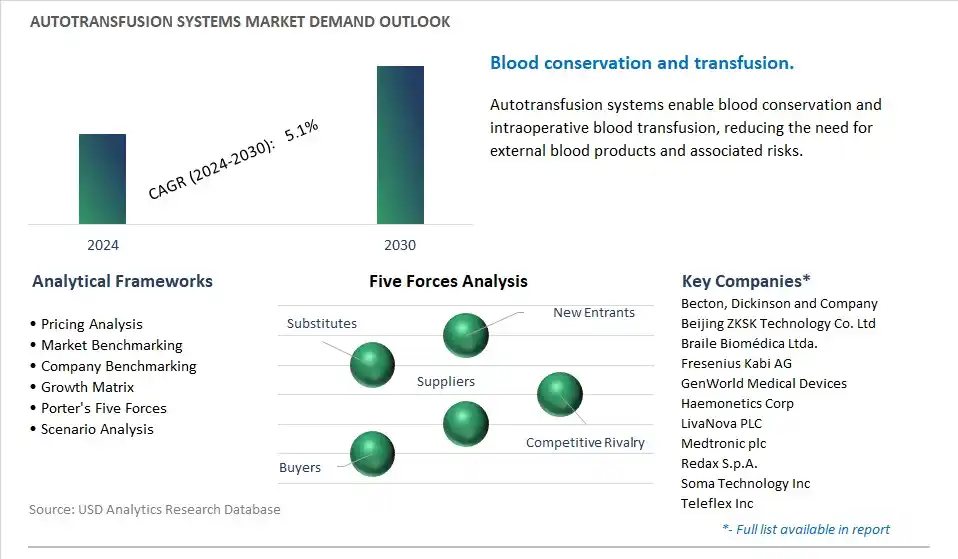

The market research study provides in-depth insights into leading companies including the SWOT analyses, product profile, financial details, and recent developments acrossBecton, Dickinson and Company, Beijing ZKSK Technology Co. Ltd, Braile Biomédica Ltda., Fresenius Kabi AG, GenWorld Medical Devices, Haemonetics Corp, LivaNova PLC, Medtronic plc, Redax S.p.A., Soma Technology Inc, Teleflex Inc, Zimmer Biomet Holdings Inc

By Product

Devices

Consumables

By Application

Cardiac Surgeries

Orthopedic Surgeries

Organ Transplantation

Others

By End-User

Hospitals

Ambulatory Surgical Centers

Others

Geographical Analysis

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Becton, Dickinson and Company

Beijing ZKSK Technology Co. Ltd

Braile Biomédica Ltda.

Fresenius Kabi AG

GenWorld Medical Devices

Haemonetics Corp

LivaNova PLC

Medtronic plc

Redax S.p.A.

Soma Technology Inc

Teleflex Inc

Zimmer Biomet Holdings Inc

• Deepen your industry insights and navigate uncertainties for strategy formulation, CAPEX, and Operational decisions

• Gain access to detailed insights on the Autotransfusion Systems Market, encompassing current market size, growth trends, and forecasts till 2030.

• Access detailed competitor analysis, enabling competitive advantage through a thorough understanding of market players, strategies, and potential differentiation opportunities

• Stay ahead of the curve with insights on technological advancements, innovations, and upcoming trends

• Identify lucrative investment avenues and expansion opportunities within the Autotransfusion Systems Market industry, guided by robust, data-backed analysis.

• Understand regional and global markets through country-wise analysis, regional market potential, regulatory nuances, and dynamics

• Execute strategies with confidence and speed through information, analytics, and insights on the industry value chain

• Corporate leaders, strategists, financial experts, shareholders, asset managers, and governmental representatives can make long-term planning scenarios and build an integrated and timely understanding of market dynamics

• Benefit from tailored solutions and expert consultation based on report insights, providing personalized strategies aligned with specific business needs.

TABLE OF CONTENTS

1 Introduction to 2024 Autotransfusion Systems Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Autotransfusion Systems Market Size Outlook, $ Million, 2021 to 2030

3.2 Autotransfusion Systems Market Outlook by Type, $ Million, 2021 to 2030

3.3 Autotransfusion Systems Market Outlook by Product, $ Million, 2021 to 2030

3.4 Autotransfusion Systems Market Outlook by Application, $ Million, 2021 to 2030

3.5 Autotransfusion Systems Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Autotransfusion Systems Industry

4.2 Key Market Trends in Autotransfusion Systems Industry

4.3 Potential Opportunities in Autotransfusion Systems Industry

4.4 Key Challenges in Autotransfusion Systems Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Autotransfusion Systems Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Autotransfusion Systems Market Outlook by Segments

7.1 Autotransfusion Systems Market Outlook by Segments, $ Million, 2021- 2030

By Product

Devices

Consumables

By Application

Cardiac Surgeries

Orthopedic Surgeries

Organ Transplantation

Others

By End-User

Hospitals

Ambulatory Surgical Centers

Others

8 North America Autotransfusion Systems Market Analysis and Outlook To 2030

8.1 Introduction to North America Autotransfusion Systems Markets in 2024

8.2 North America Autotransfusion Systems Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Autotransfusion Systems Market size Outlook by Segments, 2021-2030

By Product

Devices

Consumables

By Application

Cardiac Surgeries

Orthopedic Surgeries

Organ Transplantation

Others

By End-User

Hospitals

Ambulatory Surgical Centers

Others

9 Europe Autotransfusion Systems Market Analysis and Outlook To 2030

9.1 Introduction to Europe Autotransfusion Systems Markets in 2024

9.2 Europe Autotransfusion Systems Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Autotransfusion Systems Market Size Outlook by Segments, 2021-2030

By Product

Devices

Consumables

By Application

Cardiac Surgeries

Orthopedic Surgeries

Organ Transplantation

Others

By End-User

Hospitals

Ambulatory Surgical Centers

Others

10 Asia Pacific Autotransfusion Systems Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Autotransfusion Systems Markets in 2024

10.2 Asia Pacific Autotransfusion Systems Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Autotransfusion Systems Market size Outlook by Segments, 2021-2030

By Product

Devices

Consumables

By Application

Cardiac Surgeries

Orthopedic Surgeries

Organ Transplantation

Others

By End-User

Hospitals

Ambulatory Surgical Centers

Others

11 South America Autotransfusion Systems Market Analysis and Outlook To 2030

11.1 Introduction to South America Autotransfusion Systems Markets in 2024

11.2 South America Autotransfusion Systems Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Autotransfusion Systems Market size Outlook by Segments, 2021-2030

By Product

Devices

Consumables

By Application

Cardiac Surgeries

Orthopedic Surgeries

Organ Transplantation

Others

By End-User

Hospitals

Ambulatory Surgical Centers

Others

12 Middle East and Africa Autotransfusion Systems Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Autotransfusion Systems Markets in 2024

12.2 Middle East and Africa Autotransfusion Systems Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Autotransfusion Systems Market size Outlook by Segments, 2021-2030

By Product

Devices

Consumables

By Application

Cardiac Surgeries

Orthopedic Surgeries

Organ Transplantation

Others

By End-User

Hospitals

Ambulatory Surgical Centers

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

List of Companies

Becton, Dickinson and Company

Beijing ZKSK Technology Co. Ltd

Braile Biomédica Ltda.

Fresenius Kabi AG

GenWorld Medical Devices

Haemonetics Corp

LivaNova PLC

Medtronic plc

Redax S.p.A.

Soma Technology Inc

Teleflex Inc

Zimmer Biomet Holdings Inc

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Product

Devices

Consumables

By Application

Cardiac Surgeries

Orthopedic Surgeries

Organ Transplantation

Others

By End-User

Hospitals

Ambulatory Surgical Centers

Others

Countries Analyzed

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

The global Autotransfusion Systems Market is one of the lucrative growth markets, poised to register a 5.1% growth (CAGR) between 2024 and 2030.

Emerging Markets across Asia Pacific, Europe, and Americas present robust growth prospects.

Becton, Dickinson and Company, Beijing ZKSK Technology Co. Ltd, Braile Biomédica Ltda., Fresenius Kabi AG, GenWorld Medical Devices, Haemonetics Corp, LivaNova PLC, Medtronic plc, Redax S.p.A., Soma Technology Inc, Teleflex Inc, Zimmer Biomet Holdings Inc

Base Year- 2023; Estimated Year- 2024; Historic Period- 2018-2023; Forecast period- 2024 to 2030; Currency: USD; Volume