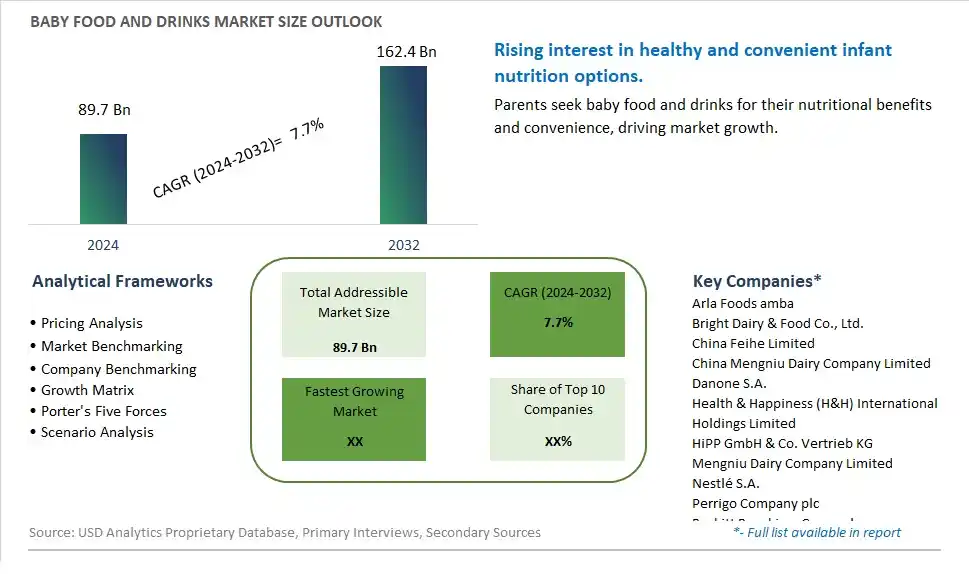

Global Baby Food and Drinks Market Size is valued at $89.7 Billion in 2024 and is forecast to register a growth rate (CAGR) of 7.7% to reach $162.4 Billion by 2032.

The global Baby Food and Drinks Market Comprehensive Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Product (Organic, Conventional), By Type (Infant Formula, Dried Baby Food, Ready to Feed Baby Food, Baby Juice, Baby Electrolyte, Others), By Distribution Channel (Drugstores/ Pharmacies, Supermarkets/ Hypermarkets, Convenience Stores, Online Channels, Others)

An Introduction to Baby Food and Drinks Market

The Baby Food and Drinks market in 2024 is thriving, driven by the rising awareness of the importance of early childhood nutrition and the increasing demand for convenient and healthy feeding options. The market encompasses a wide range of products, including purees, cereals, snacks, and beverages, designed to meet the nutritional needs of infants and toddlers. The market is supported by the growing trend towards organic and clean-label baby foods, as well as the demand for functional and fortified products that support growth and development. Innovations in product formulation, packaging, and preservation are enhancing the quality, safety, and convenience of baby food and drinks. The market is also benefiting from strong support from healthcare professionals and increasing consumer willingness to invest in premium and high-quality baby nutrition products.

Baby Food and Drinks Competitive Landscape

The market report analyses the leading companies in the industry including Arla Foods amba, Bright Dairy & Food Co., Ltd., China Feihe Limited, China Mengniu Dairy Company Limited, Danone S.A., Health & Happiness (H&H) International Holdings Limited, HiPP GmbH & Co. Vertrieb KG, Mengniu Dairy Company Limited, Nestlé S.A., Perrigo Company plc, Reckitt Benckiser Group plc, Royal FrieslandCampina N.V., The Kraft Heinz Company, Töpfer GmbH, and Others.

Baby Food and Drinks Market Dynamics

Baby Food and Drinks Market Trend: Increasing Demand for Organic and Clean Label Products

The most prominent market trend for Baby Food and Drinks is the increasing demand for organic and clean label products among parents. As parents prioritize the health and well-being of their infants, there's a growing preference for baby food and drinks made with organic ingredients, free from artificial additives, preservatives, and genetically modified organisms (GMOs). This trend reflects a broader shift towards natural and transparent food choices, emphasizing the importance of purity, nutritional quality, and safety in infant nutrition.

Baby Food and Drinks Market Driver: Health and Nutrition Awareness Among Parents

A key market driver for Baby Food and Drinks is the heightened awareness of health and nutrition among parents. With access to information about the impact of diet on children's growth, development, and long-term health, parents are more informed and proactive in selecting nutritious and balanced food options for their babies. The drive to provide optimal nutrition, support immune health, and prevent allergies and sensitivities fuels the demand for baby food and drinks formulated with carefully selected ingredients that meet stringent quality and safety standards.

Baby Food and Drinks Market Opportunity: Expansion in Functional and Developmental Nutrition

A potential opportunity within the Baby Food and Drinks market lies in the expansion of functional and developmental nutrition offerings. Collaborating with pediatricians, nutrition experts, and food scientists can lead to the development of innovative baby food and drink formulations that target specific health benefits such as brain development, immune support, digestive health, and allergy prevention. Additionally, exploring new product formats, packaging designs, and flavor varieties tailored to different age groups and developmental stages can enhance product appeal, meet evolving consumer preferences, and drive growth in the competitive baby nutrition segment.

Baby Food and Drinks Market Share Analysis: Conventional segment generated the highest revenue share in the industry

The largest segment in the Baby Food and Drinks Market is the Conventional product category. Conventional baby food and drinks refer to products that are produced using traditional methods and may include ingredients that are not certified organic. This segment dominates the market due to several key factors. Firstly, conventional baby food and drinks are often more widely available and accessible compared to organic counterparts, making them the preferred choice for many parents, especially those looking for convenient and cost-effective options. The affordability of conventional baby food and drinks also plays a significant role in driving their popularity, as they are priced lower than organic products, catering to a broader consumer base with varying budget constraints. Additionally, conventional baby food and drinks may undergo more extensive testing and regulatory scrutiny, providing parents with a sense of assurance regarding safety and quality standards. While organic baby food and drinks appeal to a growing segment of health-conscious consumers seeking natural and pesticide-free options, the widespread acceptance and familiarity of conventional products continue to make them the dominant force in the market. As a result, the Conventional product category maintains its position as the largest segment in the Baby Food and Drinks Market, with a strong presence across various retail channels and geographic regions.

Baby Food and Drinks Market Share Analysis: Baby Electrolyte is the fastest growing segment over the forecast period to 2032

The fastest-growing segment in the Baby Food and Drinks Market is Baby Electrolyte. Baby electrolytes are specialized drinks formulated to replenish essential minerals and fluids in infants and young children, especially during periods of illness or dehydration. This segment is experiencing rapid growth due to several factors. Firstly, increased awareness among parents about the importance of hydration and electrolyte balance in babies has led to a higher demand for products that cater specifically to these needs. As more parents become proactive about their children's health and well-being, they are seeking out products like baby electrolytes that offer targeted benefits. Further, advancements in formulation and packaging technology have made baby electrolytes more convenient and appealing to consumers. Many products in this segment now come in ready-to-drink formats with improved flavors and textures, making them easier to administer to infants and toddlers. Additionally, the rising incidence of infant illnesses such as diarrhea and vomiting, coupled with changing weather patterns leading to higher instances of dehydration, has further fueled the demand for baby electrolytes. Manufacturers are also focusing on introducing natural and organic variants within this segment, capitalizing on the trend towards healthier and cleaner-label products. As a result, Baby Electrolyte stands out as the fastest-growing segment in the Baby Food and Drinks Market, poised for significant expansion and innovation in the coming years.

Baby Food and Drinks Market Share Analysis: Supermarkets/Hypermarkets segment generated the highest revenue share in the industry

The largest segment in the Baby Food and Drinks Market based on distribution channels is Supermarkets/Hypermarkets. This segment comprises retail outlets that offer a wide range of baby food and drink products, catering to the diverse needs of parents and caregivers. Supermarkets and hypermarkets have emerged as key players in the baby food and drinks market due to their extensive reach, convenient shopping experience, and diverse product offerings. They provide a one-stop destination for parents to purchase various types of baby food, including infant formula, baby cereals, purees, snacks, and beverages. The fast growth of this segment is attributed to several factors. Firstly, the convenience and accessibility of supermarkets/hypermarkets attract a large customer base, including busy parents looking for convenient shopping solutions. Further, these retail channels often offer competitive pricing, promotions, and discounts on baby food products, making them more attractive to budget-conscious consumers. Additionally, supermarkets/hypermarkets invest in marketing and promotion activities, highlighting the nutritional benefits and safety standards of the baby food and drink products they carry, further driving sales. As parents prioritize convenience, affordability, and quality when purchasing baby food and drinks, supermarkets/hypermarkets continue to dominate the distribution landscape and are expected to sustain their growth trajectory in the coming years.

Baby Food and Drinks Market Segmentation

By Product

Organic

Conventional

By Type

Infant Formula

Dried Baby Food

Ready to Feed Baby Food

Baby Juice

Baby Electrolyte

Others

By Distribution Channel

Drugstores/ Pharmacies

Supermarkets/ Hypermarkets

Convenience Stores

Online Channels

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Baby Food and Drinks Companies Profiled in the Study

Arla Foods amba

Bright Dairy & Food Co., Ltd.

China Feihe Limited

China Mengniu Dairy Company Limited

Danone S.A.

Health & Happiness (H&H) International Holdings Limited

HiPP GmbH & Co. Vertrieb KG

Mengniu Dairy Company Limited

Nestlé S.A.

Perrigo Company plc

Reckitt Benckiser Group plc

Royal FrieslandCampina N.V.

The Kraft Heinz Company

Töpfer GmbH

*- List Not Exhaustive

Chapter 1. TABLE OF CONTENTS

Chapter 2. Introduction to Baby Food and Drinks Market

2.1. Market Overview

2.2. Key Statistics and Report Highlights

2.3. Scope of the Comprehensive Study

2.3.1. Market Definition

2.3.2 Countries and Regions Covered

2.3.3 Research Objective

2.3.4 Units, Currency, and Conversions

2.3.5 Industry Value Chain

2.4. Key Market Segments

2.5. Key Companies

2.6. Study Period

Chapter 3. Strategic Analysis Review

3.1. Baby Food and Drinks Pricing Analysis and Forecast

3.2. Porter’s Five Forces

3.3. Market Ecosystem

3.4. SWOT Analysis

3.5. Regulatory Scenario

3.3. Effects of Inflation, Russia-Ukraine War, moderating economic growth, and other macroeconomic factors

Chapter 4. Competitive Landscape

4.1. Market Share Analysis

4.1.1. Global Baby Food and Drinks Market Share by Company, 2023

4.1.2. Product Offerings of Leading Baby Food and Drinks Companies

4.2. Market Entropy

4.2.1. New Product Launches in the Industry

4.2.2. Mergers, Acquisitions, Joint ventures, and Partnerships

4.3. Key Strategies and Best Practices

Chapter 5. Global Market Projections: Best, Reference, and Low Case Scenarios

5.1. Growth Analysis- Case Scenario Definitions

5.2. Low Growth Case Scenario Forecasts

5.3. Reference Growth Case Scenario Forecasts

5.4. High Growth Case Scenario Forecasts

Chapter 6. Market Dynamics

6.1. Baby Food and Drinks Market Drivers

6.2. Baby Food and Drinks Market Challenges

6.6. Baby Food and Drinks Market Opportunities

6.4. Baby Food and Drinks Market Trends

Chapter 7. Global Baby Food and Drinks Market Outlook Trends

7.1. Global Baby Food and Drinks Revenue (USD Million) and CAGR (%) by Type (2021-2032)

7.2. Global Baby Food and Drinks Revenue (USD Million) and CAGR (%) by Application (2021-2032)

7.3. Global Baby Food and Drinks Revenue (USD Million) and CAGR (%) by Product (2021-2032)

By Product

Organic

Conventional

By Type

Infant Formula

Dried Baby Food

Ready to Feed Baby Food

Baby Juice

Baby Electrolyte

Others

By Distribution Channel

Drugstores/ Pharmacies

Supermarkets/ Hypermarkets

Convenience Stores

Online Channels

Others

Chapter 8. Global Baby Food and Drinks Regional Analysis and Outlook

8.1. Global Baby Food and Drinks Revenue (USD Million) By Regions (2021- 2032)

8.2. North America Baby Food and Drinks Revenue (USD Million) by Country (2021-2032)

8.2.1. United States Baby Food and Drinks Regional Analysis and Outlook

8.2.2. Canada Baby Food and Drinks Regional Analysis and Outlook

8.2.3. Mexico Baby Food and Drinks Regional Analysis and Outlook

8.3. Europe Baby Food and Drinks Revenue (USD Million), by Country (2021-2032)

8.3.1. Germany Baby Food and Drinks Regional Analysis and Outlook

8.3.2. France Baby Food and Drinks Regional Analysis and Outlook

8.3.3. United Kingdom Baby Food and Drinks Regional Analysis and Outlook

8.3.4. Spain Baby Food and Drinks Regional Analysis and Outlook

8.3.5. Italy Baby Food and Drinks Regional Analysis and Outlook

8.3.6. Russia Baby Food and Drinks Regional Analysis and Outlook

8.3.7. Rest of Europe Baby Food and Drinks Regional Analysis and Outlook

8.4. Asia Pacific Baby Food and Drinks Revenue (USD Million) by Country (2021-2032)

8.4.1. China Baby Food and Drinks Regional Analysis and Outlook

8.4.2. Japan Baby Food and Drinks Regional Analysis and Outlook

8.4.3. India Baby Food and Drinks Regional Analysis and Outlook

8.4.4. South Korea Baby Food and Drinks Regional Analysis and Outlook

8.4.5. Australia Baby Food and Drinks Regional Analysis and Outlook

8.4.6. South East Asia Baby Food and Drinks Regional Analysis and Outlook

8.4.7. Rest of Asia Pacific Baby Food and Drinks Regional Analysis and Outlook

8.5. South America Baby Food and Drinks Revenue (USD Million), by Country (2021-2032)

8.5.1. Brazil Baby Food and Drinks Regional Analysis and Outlook

8.5.2. Argentina Baby Food and Drinks Regional Analysis and Outlook

8.5.3. Rest of South America Baby Food and Drinks Regional Analysis and Outlook

8.6. Middle East and Africa Baby Food and Drinks Revenue (USD Million) by Country (2021-2032)

8.6.1. Middle East Baby Food and Drinks Regional Analysis and Outlook

8.6.2. Africa Baby Food and Drinks Regional Analysis and Outlook

Chapter 9. North America Baby Food and Drinks Analysis and Outlook

9.1. North America Baby Food and Drinks Revenue (USD Million) by Segments (2021-2032)

9.1.1. North America Baby Food and Drinks Revenue (USD Million) by Type (2021-2032)

9.1.2. North America Baby Food and Drinks Revenue (USD Million) by Application (2021-2032)

9.1.3. North America Baby Food and Drinks Revenue (USD Million) by Product (2021-2032)

By Product

Organic

Conventional

By Type

Infant Formula

Dried Baby Food

Ready to Feed Baby Food

Baby Juice

Baby Electrolyte

Others

By Distribution Channel

Drugstores/ Pharmacies

Supermarkets/ Hypermarkets

Convenience Stores

Online Channels

Others

Chapter 10. Europe Baby Food and Drinks Analysis and Outlook

10.1. Europe Baby Food and Drinks Revenue (USD Million), by Segments (USD Million) (2021-2032)

10.1.1. Europe Baby Food and Drinks Revenue (USD Million) by Type (2021-2032)

10.1.2. Europe Baby Food and Drinks Revenue (USD Million) by Application (2021-2032)

10.1.3. Europe Baby Food and Drinks Revenue (USD Million) by Product (2021-2032)

By Product

Organic

Conventional

By Type

Infant Formula

Dried Baby Food

Ready to Feed Baby Food

Baby Juice

Baby Electrolyte

Others

By Distribution Channel

Drugstores/ Pharmacies

Supermarkets/ Hypermarkets

Convenience Stores

Online Channels

Others

Chapter 11. Asia Pacific Baby Food and Drinks Analysis and Outlook

11.1. Asia Pacific Baby Food and Drinks Revenue (USD Million), and Revenue (USD Million) by Segments (2021-2032)

11.1.1. Asia Pacific Baby Food and Drinks Revenue (USD Million) by Type (2021-2032)

11.1.2. Asia Pacific Baby Food and Drinks Revenue (USD Million) by Application (2021-2032)

11.1.3. Asia Pacific Baby Food and Drinks Revenue (USD Million) by Product (2021-2032)

By Product

Organic

Conventional

By Type

Infant Formula

Dried Baby Food

Ready to Feed Baby Food

Baby Juice

Baby Electrolyte

Others

By Distribution Channel

Drugstores/ Pharmacies

Supermarkets/ Hypermarkets

Convenience Stores

Online Channels

Others

Chapter 12. South America Baby Food and Drinks Analysis and Outlook

12.1. South America Baby Food and Drinks Revenue (USD Million), by Segments (2021-2032)

12.1.1. South America Baby Food and Drinks Revenue (USD Million) by Type (2021-2032)

12.1.2. South America Baby Food and Drinks Revenue (USD Million) by Application (2021-2032)

12.1.3. South America Baby Food and Drinks Revenue (USD Million) by Product (2021-2032)

By Product

Organic

Conventional

By Type

Infant Formula

Dried Baby Food

Ready to Feed Baby Food

Baby Juice

Baby Electrolyte

Others

By Distribution Channel

Drugstores/ Pharmacies

Supermarkets/ Hypermarkets

Convenience Stores

Online Channels

Others

Chapter 13. Middle East and Africa Baby Food and Drinks Analysis and Outlook

13.1. Middle East and Africa Baby Food and Drinks Revenue (USD Million), by Segments (2021-2032)

13.1.1. Middle East and Africa Baby Food and Drinks Revenue (USD Million) by Type (2021-2032)

13.1.2. Middle East and Africa Baby Food and Drinks Revenue (USD Million) by Application (2021-2032)

13.1.3. Middle East and Africa Baby Food and Drinks Revenue (USD Million) by Product (2021-2032)

By Product

Organic

Conventional

By Type

Infant Formula

Dried Baby Food

Ready to Feed Baby Food

Baby Juice

Baby Electrolyte

Others

By Distribution Channel

Drugstores/ Pharmacies

Supermarkets/ Hypermarkets

Convenience Stores

Online Channels

Others

Chapter 14. Baby Food and Drinks Company Profiles

14.1 Business Overview

14.2 Product Profiles

14.3 SWOT Profiles

14.5 Recent Developments

14.6 Financial Profile

List of Companies

Arla Foods amba

Bright Dairy & Food Co., Ltd.

China Feihe Limited

China Mengniu Dairy Company Limited

Danone S.A.

Health & Happiness (H&H) International Holdings Limited

HiPP GmbH & Co. Vertrieb KG

Mengniu Dairy Company Limited

Nestlé S.A.

Perrigo Company plc

Reckitt Benckiser Group plc

Royal FrieslandCampina N.V.

The Kraft Heinz Company

Töpfer GmbH

15. Methodology and Data Sources

15.1 Customization Offerings

15.2 Subscription Services

15.3 Related Reports

15.4 Publisher Expertise

LIST OF TABLES

Table 1 Market Segmentation Analysis

Table 2 Global Baby Food and Drinks Market Share of Leading Companies, 2023

Table 3 Product Offerings of Leading Companies

Table 4 Low Growth Scenario Forecasts

Table 5 Reference Case Growth Scenario

Table 6 High Growth Case Scenario

Table 7 Global Baby Food and Drinks Revenue (USD Million) And CAGR (%) By Type (2021-2032)

Table 8 Global Baby Food and Drinks Revenue (USD Million) And CAGR (%) By Application (2021-2032)

Table 9 Global Baby Food and Drinks Revenue (USD Million) And CAGR (%) By Product (2021-2032)

Table 10 Global Baby Food and Drinks Market Revenue (USD Million) By Regions (2021-2032)

Table 11 Global Baby Food and Drinks Market Share (%) By Regions (2021-2032)

Table 12 North America Baby Food and Drinks Revenue (USD Million) By Country (2021-2032)

Table 13 Europe Baby Food and Drinks Revenue (USD Million) By Country (2021-2032)

Table 14 Asia Pacific Baby Food and Drinks Revenue (USD Million) By Country (2021-2032)

Table 15 South America Baby Food and Drinks Revenue (USD Million) By Country (2021-2032)

Table 16 Middle East and Africa Baby Food and Drinks Revenue (USD Million) By Region (2021-2032)

Table 17 North America Baby Food and Drinks Revenue (USD Million) By Type (2021-2032)

Table 18 North America Baby Food and Drinks Revenue (USD Million) By Application (2021-2032)

Table 19 North America Baby Food and Drinks Revenue (USD Million) By Product (2021-2032)

Table 20 Europe Baby Food and Drinks Revenue (USD Million) By Type (2021-2032)

Table 21 Europe Baby Food and Drinks Revenue (USD Million) By Application (2021-2032)

Table 22 Europe Baby Food and Drinks Revenue (USD Million) By Product (2021-2032)

Table 23 Asia Pacific Baby Food and Drinks Revenue (USD Million) By Type (2021-2032)

Table 24 Asia Pacific Baby Food and Drinks Revenue (USD Million) By Application (2021-2032)

Table 25 Asia Pacific Baby Food and Drinks Revenue (USD Million) By Product (2021-2032)

Table 26 South America Baby Food and Drinks Revenue (USD Million) By Type (2021-2032)

Table 27 South America Baby Food and Drinks Revenue (USD Million) By Application (2021-2032)

Table 28 South America Baby Food and Drinks Revenue (USD Million) By Product (2021-2032)

Table 29 Middle East and Africa Baby Food and Drinks Revenue (USD Million) By Type (2021-2032)

Table 30 Middle East and Africa Baby Food and Drinks Revenue (USD Million) By Application (2021-2032)

Table 31 Middle East and Africa Baby Food and Drinks Revenue (USD Million) By Product (2021-2032)

LIST OF FIGURES

Figure 1. Market Scope

Figure 2. Pricing Forecasts Per Unit, 2023- 2032

Figure 3. Porter’s Five Forces

Figure 4. Global Baby Food and Drinks Market Revenue (USD Million) By Regions (2021-2032)

Figure 5. Global Baby Food and Drinks Market Share (%) By Regions (2023)

Figure 6. North America Baby Food and Drinks Revenue (USD Million) By Country (2021-2032)

Figure 7. United States Baby Food and Drinks Revenue (USD Million) By Country (2021-2032)

Figure 8. Canada Baby Food and Drinks Revenue (USD Million) By Country (2021-2032)

Figure 9. Mexico Baby Food and Drinks Revenue (USD Million) By Country (2021-2032)

Figure 10. Europe Baby Food and Drinks Revenue (USD Million) By Country (2021-2032)

Figure 11. Germany Baby Food and Drinks Revenue (USD Million) By Country (2021-2032)

Figure 12. France Baby Food and Drinks Revenue (USD Million) By Country (2021-2032)

Figure 13. United Kingdom Baby Food and Drinks Revenue (USD Million) By Country (2021-2032)

Figure 14. Spain Baby Food and Drinks Revenue (USD Million) By Country (2021-2032)

Figure 15. Italy Baby Food and Drinks Revenue (USD Million) By Country (2021-2032)

Figure 16. Russia Baby Food and Drinks Revenue (USD Million) By Country (2021-2032)

Figure 17. Rest of Europe Baby Food and Drinks Revenue (USD Million) By Country (2021-2032)

Figure 11. Asia Pacific Baby Food and Drinks Revenue (USD Million) By Country (2021-2032)

Figure 12. China Baby Food and Drinks Revenue (USD Million) By Country (2021-2032)

Figure 13. Japan Baby Food and Drinks Revenue (USD Million) By Country (2021-2032)

Figure 14. India Baby Food and Drinks Revenue (USD Million) By Country (2021-2032)

Figure 15. South Korea Baby Food and Drinks Revenue (USD Million) By Country (2021-2032)

Figure 16. Australia Baby Food and Drinks Revenue (USD Million) By Country (2021-2032)

Figure 17. South East Asia Baby Food and Drinks Revenue (USD Million) By Country (2021-2032)

Figure 18. South America Baby Food and Drinks Revenue (USD Million) By Country (2021-2032)

Figure 19. Brazil Baby Food and Drinks Revenue (USD Million) By Country (2021-2032)

Figure 20. Argentina Baby Food and Drinks Revenue (USD Million) By Country (2021-2032)

Figure 21. Rest of Asia Pacific Baby Food and Drinks Revenue (USD Million) By Country (2021-2032)

Figure 22. Middle East and Africa Baby Food and Drinks Revenue (USD Million) By Region (2021-2032)

Figure 23. Saudi Arabia Baby Food and Drinks Revenue (USD Million) By Region (2021-2032)

Figure 24. The UAE Baby Food and Drinks Revenue (USD Million) By Region (2021-2032)

Figure 25. Rest of Middle East Baby Food and Drinks Revenue (USD Million) By Region (2021-2032)

Figure 26. South Africa Baby Food and Drinks Revenue (USD Million) By Region (2021-2032)

Figure 27. Africa Baby Food and Drinks Revenue (USD Million) By Region (2021-2032)

Figure 28. North America Baby Food and Drinks Revenue (USD Million) By Type (2021-2032)

Figure 29. North America Baby Food and Drinks Revenue (USD Million) By Application (2021-2032)

Figure 30. North America Baby Food and Drinks Revenue (USD Million) By Product (2021-2032)

Figure 31. Europe Baby Food and Drinks Revenue (USD Million) By Type (2021-2032)

Figure 32. Europe Baby Food and Drinks Revenue (USD Million) By Application (2021-2032)

Figure 33. Europe Baby Food and Drinks Revenue (USD Million) By Product (2021-2032)

Figure 34. Asia Pacific Baby Food and Drinks Revenue (USD Million) By Type (2021-2032)

Figure 35. Asia Pacific Baby Food and Drinks Revenue (USD Million) By Application (2021-2032)

Figure 36. Asia Pacific Baby Food and Drinks Revenue (USD Million) By Product (2021-2032)

Figure 37. South America Baby Food and Drinks Revenue (USD Million) By Type (2021-2032)

Figure 38. South America Baby Food and Drinks Revenue (USD Million) By Application (2021-2032)

Figure 39. South America Baby Food and Drinks Revenue (USD Million) By Product (2021-2032)

Figure 40. Middle East and Africa Baby Food and Drinks Revenue (USD Million) By Type (2021-2032)

Figure 41. Middle East and Africa Baby Food and Drinks Revenue (USD Million) By Application (2021-2032)

Figure 42. Middle East and Africa Baby Food and Drinks Revenue (USD Million) By Product (2021-2032)

By Product

Organic

Conventional

By Type

Infant Formula

Dried Baby Food

Ready to Feed Baby Food

Baby Juice

Baby Electrolyte

Others

By Distribution Channel

Drugstores/ Pharmacies

Supermarkets/ Hypermarkets

Convenience Stores

Online Channels

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)