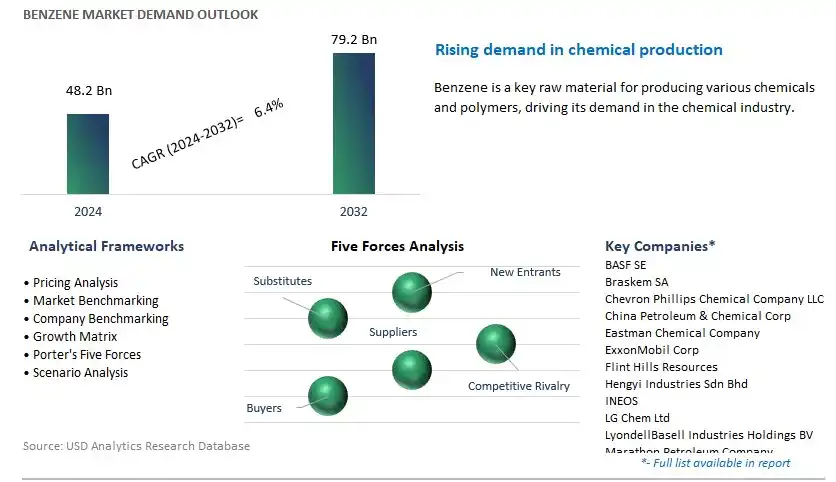

Global Benzene Market Size is valued at $48.2 Billion in 2024 and is forecast to register a growth rate (CAGR) of 6.4% to reach $79.2 Billion by 2032.

The global Benzene Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Derivative (Ethyl Benzene, Alkyl Benzene, Cumene, Cyclohexane, Nitro Benzene, Others), By Production Process (Catalytic reforming, Steam cracking, Others).

An Introduction to Benzene Market in 2024

Benzene is a colorless, flammable liquid aromatic hydrocarbon derived from petroleum refining and chemical synthesis processes. It is a fundamental building block in the production of various chemicals, including plastics, resins, synthetic fibers, rubber, and pharmaceuticals. The market for benzene is driven by its importance as a precursor in numerous industrial processes and applications. Benzene is primarily used in the manufacturing of styrene, which is then polymerized to produce polystyrene, a widely used plastic material. Additionally, benzene is a key raw material in the production of other chemicals such as phenol, cyclohexane, and nitrobenzene, which are used in the manufacture of pharmaceuticals, explosives, and pesticides. Further, benzene serves as a solvent in various industrial processes and as a component in gasoline to improve octane ratings. However, benzene is also known to be toxic and carcinogenic, leading to regulatory restrictions and efforts to reduce emissions and exposure in industrial and environmental settings. As industries seek alternatives and safer handling practices, benzene s to be a critical component in the production of essential chemicals and materials for modern society.

Benzene Market Competitive Landscape

The market report analyses the leading companies in the industry including BASF SE, Braskem SA, Chevron Phillips Chemical Company LLC, China Petroleum & Chemical Corp, Eastman Chemical Company, ExxonMobil Corp, Flint Hills Resources, Hengyi Industries Sdn Bhd, INEOS, LG Chem Ltd, LyondellBasell Industries Holdings BV, Marathon Petroleum Company, Maruzen Petrochemical, Mitsubishi Chemical Corp, Reliance Industries Ltd, SABIC, Shell PLC, SIBUR, and others.

Benzene Market Dynamics

Market Trend: Shift Towards Sustainable and Green Chemistry Practices

A significant market trend for Benzene is the shift towards sustainable and green chemistry practices driven by environmental regulations, corporate sustainability goals, and consumer demand for safer and eco-friendly products. Benzene, a key petrochemical used in the production of various industrial chemicals, plastics, and synthetic materials, has historically been associated with environmental and health concerns due to its toxicity and carcinogenicity. As a result, there is a growing emphasis on reducing benzene emissions, minimizing exposure risks, and exploring alternative production methods that prioritize safety, efficiency, and environmental sustainability. This trend reflects a broader industry movement towards greener manufacturing processes, renewable feedstocks, and circular economy principles, influencing the market dynamics and driving innovation in benzene production and utilization.

Market Driver: Demand from Petrochemical and Polymer Industries

A significant market driver for Benzene is the demand from petrochemical and polymer industries for raw materials used in the production of plastics, resins, synthetic fibers, and rubber products. Benzene serves as a vital feedstock in the synthesis of styrene, ethylbenzene, cumene, and other intermediates that are essential building blocks for a wide range of downstream applications in manufacturing sectors such as automotive, construction, packaging, and consumer goods. With increasing global demand for polymers and specialty chemicals, there is a steady demand for benzene as a primary raw material to support production capacity expansions, new product developments, and market growth in petrochemical value chains. The continued growth of end-use industries, coupled with technological advancements in benzene production and processing, drives the demand for benzene and sustains its position as a key commodity in the chemical industry.

Market Opportunity: Exploration of Sustainable Benzene Production Technologies

An attractive opportunity in the Benzene market lies in the exploration of sustainable production technologies that minimize environmental impact, improve resource efficiency, and reduce greenhouse gas emissions. While conventional benzene production processes such as catalytic reforming and steam cracking are well-established, there is potential for innovation in alternative routes such as biomass conversion, carbon capture and utilization (CCU), and renewable energy integration. Opportunities exist to develop novel catalysts, reactor designs, and process optimizations that enable the production of benzene from renewable feedstocks, carbon-neutral sources, or waste streams, offering a more sustainable and socially responsible approach to benzene manufacturing. By investing in research and development, collaborating with academia, government agencies, and industry partners, and leveraging advancements in green chemistry and process engineering, companies can capitalize on opportunities to reduce environmental footprint, enhance competitiveness, and meet evolving regulatory requirements in the global benzene market.

Benzene Market Share Analysis: Alkyl Benzene is poised to register the fastest CAGR over the forecast period

Alkyl benzene is the fastest-growing segment in the benzene market due to its extensive applications in the production of linear alkyl benzene (LAB), a key ingredient in the manufacturing of detergents. The increasing demand for household and industrial detergents, particularly in emerging economies with growing populations and rising standards of living, is driving the expansion of the alkyl benzene segment. Additionally, the versatility of alkyl benzene in other industries such as paints and coatings, lubricants, and pharmaceuticals contributes to its rapid growth. Furthermore, technological advancements in production processes, coupled with the implementation of stringent environmental regulations promoting the use of eco-friendly detergents, are propelling the demand for alkyl benzene derivatives. With its significant market share and promising growth prospects driven by the booming detergent industry and diversified applications, alkyl benzene stands as the largest segment within the benzene market.

Benzene Market Share Analysis: Steam Cracking is poised to register the fastest CAGR over the forecast period

Steam cracking is the fastest-growing segment in the benzene market, driven by its crucial role in the petrochemical industry for producing a wide range of valuable chemical products. Steam cracking involves thermal decomposition of hydrocarbons under high temperatures, leading to the formation of benzene along with other key intermediates like ethylene, propylene, and butadiene. The increasing demand for these downstream petrochemicals, particularly in sectors such as plastics, synthetic rubbers, and resins, is fuelling the expansion of steam cracking processes. Moreover, advancements in steam cracking technology, such as the development of more efficient catalysts and optimized operating conditions, are enhancing the yields and quality of benzene and its derivatives. Additionally, the flexibility of steam cracking units to utilize various feedstocks, including natural gas liquids and naphtha, further contributes to its rapid growth. With its pivotal role in supplying benzene and other essential petrochemicals for a multitude of industries and ongoing innovations driving efficiency and productivity, steam cracking stands as the fastest-growing segment within the benzene market.

Benzene Market

By Derivative

Ethyl Benzene

Alkyl Benzene

Cumene

Cyclohexane

Nitro Benzene

Others

By Production Process

Catalytic reforming

Steam cracking

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Benzene Companies Profiled in the Study

BASF SE

Braskem SA

Chevron Phillips Chemical Company LLC

China Petroleum & Chemical Corp

Eastman Chemical Company

ExxonMobil Corp

Flint Hills Resources

Hengyi Industries Sdn Bhd

INEOS

LG Chem Ltd

LyondellBasell Industries Holdings BV

Marathon Petroleum Company

Maruzen Petrochemical

Mitsubishi Chemical Corp

Reliance Industries Ltd

SABIC

Shell PLC

SIBUR

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Benzene Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Benzene Market Size Outlook, $ Million, 2021 to 2032

3.2 Benzene Market Outlook by Type, $ Million, 2021 to 2032

3.3 Benzene Market Outlook by Product, $ Million, 2021 to 2032

3.4 Benzene Market Outlook by Application, $ Million, 2021 to 2032

3.5 Benzene Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Benzene Industry

4.2 Key Market Trends in Benzene Industry

4.3 Potential Opportunities in Benzene Industry

4.4 Key Challenges in Benzene Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Benzene Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Benzene Market Outlook by Segments

7.1 Benzene Market Outlook by Segments, $ Million, 2021- 2032

By Derivative

Ethyl Benzene

Alkyl Benzene

Cumene

Cyclohexane

Nitro Benzene

Others

By Production Process

Catalytic reforming

Steam cracking

Others

8 North America Benzene Market Analysis and Outlook To 2032

8.1 Introduction to North America Benzene Markets in 2024

8.2 North America Benzene Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Benzene Market size Outlook by Segments, 2021-2032

By Derivative

Ethyl Benzene

Alkyl Benzene

Cumene

Cyclohexane

Nitro Benzene

Others

By Production Process

Catalytic reforming

Steam cracking

Others

9 Europe Benzene Market Analysis and Outlook To 2032

9.1 Introduction to Europe Benzene Markets in 2024

9.2 Europe Benzene Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Benzene Market Size Outlook by Segments, 2021-2032

By Derivative

Ethyl Benzene

Alkyl Benzene

Cumene

Cyclohexane

Nitro Benzene

Others

By Production Process

Catalytic reforming

Steam cracking

Others

10 Asia Pacific Benzene Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Benzene Markets in 2024

10.2 Asia Pacific Benzene Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Benzene Market size Outlook by Segments, 2021-2032

By Derivative

Ethyl Benzene

Alkyl Benzene

Cumene

Cyclohexane

Nitro Benzene

Others

By Production Process

Catalytic reforming

Steam cracking

Others

11 South America Benzene Market Analysis and Outlook To 2032

11.1 Introduction to South America Benzene Markets in 2024

11.2 South America Benzene Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Benzene Market size Outlook by Segments, 2021-2032

By Derivative

Ethyl Benzene

Alkyl Benzene

Cumene

Cyclohexane

Nitro Benzene

Others

By Production Process

Catalytic reforming

Steam cracking

Others

12 Middle East and Africa Benzene Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Benzene Markets in 2024

12.2 Middle East and Africa Benzene Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Benzene Market size Outlook by Segments, 2021-2032

By Derivative

Ethyl Benzene

Alkyl Benzene

Cumene

Cyclohexane

Nitro Benzene

Others

By Production Process

Catalytic reforming

Steam cracking

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

BASF SE

Braskem SA

Chevron Phillips Chemical Company LLC

China Petroleum & Chemical Corp

Eastman Chemical Company

ExxonMobil Corp

Flint Hills Resources

Hengyi Industries Sdn Bhd

INEOS

LG Chem Ltd

LyondellBasell Industries Holdings BV

Marathon Petroleum Company

Maruzen Petrochemical

Mitsubishi Chemical Corp

Reliance Industries Ltd

SABIC

Shell PLC

SIBUR

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Derivative

Ethyl Benzene

Alkyl Benzene

Cumene

Cyclohexane

Nitro Benzene

Others

By Production Process

Catalytic reforming

Steam cracking

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)