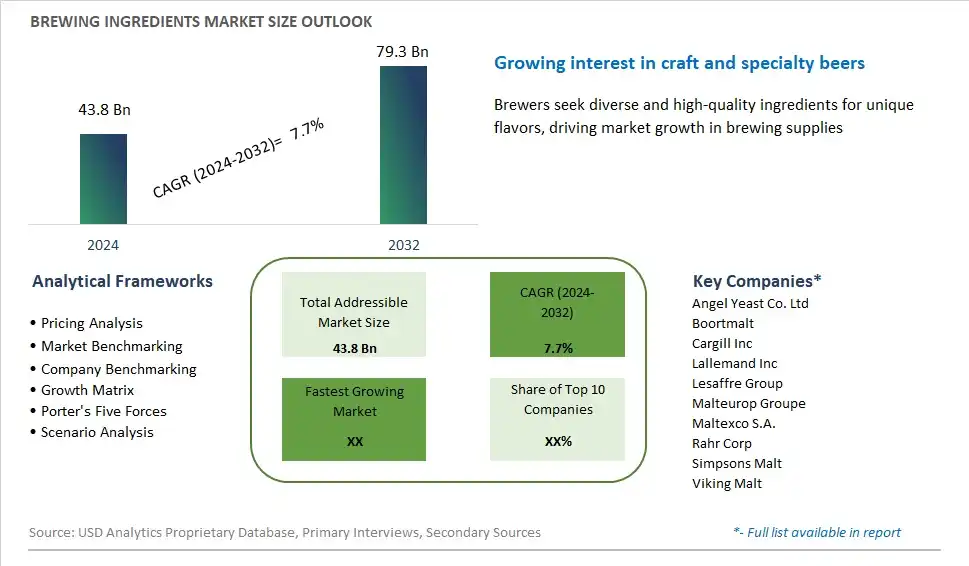

Global Brewing Ingredients Market Size is valued at $43.8 Billion in 2024 and is forecast to register a growth rate (CAGR) of 7.7% to reach $79.3 Billion by 2032.

The global Brewing Ingredients Market Comprehensive Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Source (Malt extract, Adjuncts/Grains, Hops, Beer yeast, Beer additives), By Brewery Size (Macro Brewery, Craft Brewery), By Form (Dry, Liquid)

An Introduction to Brewing Ingredients Market

Brewing ingredients are essential components used in the production of beer, cider, and other fermented beverages, contributing to flavor, aroma, and fermentation in 2024. These ingredients include malted grains, hops, yeast, and adjuncts such as fruits, spices, and herbs, which are carefully selected and combined to create unique and distinctive beverage profiles. With a growing craft beer movement and consumer demand for innovative flavors and styles, brewing ingredients play a critical role in driving creativity and differentiation in the market. From traditional barley-based beers to experimental sour ales and fruit-infused ciders, brewers are experimenting with a wide range of ingredients and techniques to push the boundaries of taste and sensory experiences. As consumer preferences evolve and global brewing trends continue to evolve, the market for brewing ingredients is expected to expand, driven by demand for high-quality, locally sourced, and sustainably produced ingredients that enhance the flavor, aroma, and authenticity of craft beverages.

Brewing Ingredients Competitive Landscape

The market report analyses the leading companies in the industry including Angel Yeast Co. Ltd, Boortmalt, Cargill Inc, Lallemand Inc, Lesaffre Group, Malteurop Groupe, Maltexco S.A., Rahr Corp, Simpsons Malt, Viking Malt, and Others.

Brewing Ingredients Market Dynamics

Brewing Ingredients Market Trend: Craft Beer Revolution and Demand for Unique Flavors

One prominent trend in the brewing ingredients market is the craft beer revolution and the growing demand for unique flavors and innovative brewing techniques. As consumers increasingly seek authenticity, variety, and artisanal experiences in their beer choices, craft breweries are flourishing, driving experimentation with different brewing ingredients and styles. This trend is fueled by factors such as changing consumer preferences, the rise of beer tourism, and the craft beer movement's emphasis on quality, creativity, and locality. Brewers are exploring a wide range of brewing ingredients, including hops, malt, yeast, and specialty adjuncts, to create distinctive and memorable brews that cater to diverse tastes and preferences. Additionally, there's a growing interest in novel ingredients such as exotic hops varieties, ancient grains, botanicals, and spices, as brewers seek to differentiate their offerings and appeal to adventurous consumers seeking new taste experiences. The craft beer revolution is reshaping the brewing ingredients market, driving demand for premium, high-quality ingredients that enable brewers to push the boundaries of traditional beer styles and create innovative, flavor-forward brews.

Market Driver: Expansion of the Craft Beer Industry and Microbreweries

A key driver propelling the growth of the brewing ingredients market is the expansion of the craft beer industry and the proliferation of microbreweries worldwide. Craft breweries, characterized by their small-scale production, independent ownership, and focus on quality and innovation, have experienced remarkable growth and popularity in recent years, reshaping the beer landscape and driving demand for brewing ingredients. This driver is fueled by factors such as changing consumer preferences towards locally produced, artisanal products, the craft beer movement's cultural and social appeal, and regulatory support for small-scale breweries and entrepreneurship. As the number of craft breweries continues to rise, so does the demand for brewing ingredients such as specialty malts, aromatic hops, and unique yeast strains that enable brewers to create distinct and memorable beers. Additionally, the growth of microbreweries fosters a culture of experimentation and collaboration, driving innovation in brewing techniques, ingredient sourcing, and flavor profiles, further fueling demand for diverse and high-quality brewing ingredients. As the craft beer industry continues to expand and diversify, the demand for brewing ingredients is expected to grow, presenting opportunities for ingredient suppliers and manufacturers to cater to the unique needs and preferences of craft brewers.

Market Opportunity: Innovation in Sustainable and Functional Ingredients

An opportunity within the brewing ingredients market lies in innovation in sustainable and functional ingredients that address environmental concerns and consumer demand for health-conscious and purposeful products. With increasing awareness of sustainability issues, climate change, and environmental impact, there's a growing emphasis on sustainability throughout the food and beverage industry, including the brewing sector. Brewers are seeking ingredients that are not only high-quality and flavorful but also environmentally friendly, ethically sourced, and socially responsible. This presents an opportunity for ingredient suppliers to develop sustainable alternatives to conventional brewing ingredients, such as organic malts, eco-friendly hops varieties, and water-saving yeast strains. Additionally, there's potential for innovation in functional ingredients that offer health benefits beyond basic nutrition, such as probiotic yeast strains, antioxidant-rich grains, and gluten-free alternatives, catering to the growing demand for healthier beer options and addressing dietary restrictions and preferences. By focusing on sustainability, health, and innovation, ingredient suppliers can differentiate their offerings, enhance their value proposition, and capitalize on the growing market opportunity in the brewing ingredients segment.

Brewing Ingredients Market Share Analysis: Adjuncts/Grains held the dominant market share in 2024

In the Brewing Ingredients Market segmented by source, the largest segment is adjuncts/grains, owing to pivotal factors shaping the brewing industry. Adjuncts and grains, such as barley, corn, rice, wheat, and oats, serve as the primary sources of fermentable sugars and starches crucial for the production of beer. As brewing techniques evolve and consumer preferences diversify, the use of adjuncts and grains has become integral to creating a wide array of beer styles, from light lagers to rich stouts. Further, adjuncts and grains offer brewers flexibility in recipe formulation, enabling them to achieve desired flavor profiles, mouthfeel, and alcohol content while optimizing cost efficiency. Additionally, the growing craft beer movement and experimentation with novel ingredients have fueled the demand for specialty grains and adjuncts, further driving the dominance of this segment in the Brewing Ingredients Market. Furthermore, advancements in malting and processing technologies have enhanced the availability and quality of adjuncts and grains, contributing to their widespread adoption by brewers worldwide. As a result, the adjuncts/grains segment stands as the largest in the Brewing Ingredients Market, poised for continued growth as the brewing industry continues to innovate and diversify to meet evolving consumer tastes and preferences.

Brewing Ingredients Market Share Analysis: Craft Brewery market is poised to register the fastest growth rae over the forecast period to 2032

In the Brewing Ingredients Market segmented by brewery size, the craft brewery segment is the fastest-growing, driven by several transformative factors shaping the brewing industry landscape. Craft breweries, characterized by their focus on innovation, quality, and unique flavor profiles, have experienced exponential growth and consumer demand in recent years. The robust growth outlook is driven by changing consumer preferences for locally produced, artisanal beers that offer authenticity and a sense of community. Craft breweries often experiment with a diverse range of brewing ingredients, including specialty malts, hops, and yeast strains, to create distinctive and creative beer styles that appeal to discerning consumers seeking new taste experiences. Further, the craft beer movement has gained momentum globally, fueled by factors such as the rise of beer tourism, the proliferation of craft beer festivals and events, and the increasing availability of craft beer in retail outlets and hospitality venues. Additionally, the craft brewery segment benefits from its agility and adaptability, allowing for rapid innovation and responsiveness to evolving consumer trends, compared to larger macro breweries. As a result, the craft brewery segment stands as the fastest-growing in the Brewing Ingredients Market, poised for continued expansion as craft beer enthusiasts drive demand for unique and flavorful brews brewed with high-quality ingredients.

Brewing Ingredients Market Share Analysis: Dry held the dominant market share in 2024

In the Brewing Ingredients Market segmented by form, the dry segment is the largest, driven by several pivotal factors that shape brewing operations. Dry brewing ingredients, including dry malt extract, dry hops, and dry yeast, offer brewers numerous advantages over their liquid counterparts. Firstly, dry ingredients have an extended shelf life and improved stability, making them easier to store and transport, thus reducing logistical complexities and costs. Additionally, dry ingredients are more concentrated, allowing brewers to achieve consistent flavor profiles and desired brewing characteristics with smaller quantities, enhancing efficiency and cost-effectiveness. Furthermore, dry ingredients are easier to handle and dose, minimizing the risk of contamination and ensuring accurate measurements during the brewing process. Further, advancements in drying technologies have led to the production of high-quality dry ingredients with enhanced flavor retention and solubility, further driving their popularity among brewers. As a result, the dry segment stands as the largest in the Brewing Ingredients Market, poised for sustained growth as brewers continue to prioritize convenience, quality, and efficiency in their brewing operations.

Brewing Ingredients Market Segmentation

By Source

Malt extract

Adjuncts/Grains

Hops

Beer yeast

Beer additives

By Brewery Size

Macro Brewery

Craft Brewery

By Form

Dry

Liquid

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Brewing Ingredients Companies Profiled in the Study

Angel Yeast Co. Ltd

Boortmalt

Cargill Inc

Lallemand Inc

Lesaffre Group

Malteurop Groupe

Maltexco S.A.

Rahr Corp

Simpsons Malt

Viking Malt

*- List Not Exhaustive

Chapter 1. TABLE OF CONTENTS

Chapter 2. Introduction to Brewing Ingredients Market

2.1. Market Overview

2.2. Key Statistics and Report Highlights

2.3. Scope of the Comprehensive Study

2.3.1. Market Definition

2.3.2 Countries and Regions Covered

2.3.3 Research Objective

2.3.4 Units, Currency, and Conversions

2.3.5 Industry Value Chain

2.4. Key Market Segments

2.5. Key Companies

2.6. Study Period

Chapter 3. Strategic Analysis Review

3.1. Brewing Ingredients Pricing Analysis and Forecast

3.2. Porter’s Five Forces

3.3. Market Ecosystem

3.4. SWOT Analysis

3.5. Regulatory Scenario

3.3. Effects of Inflation, Russia-Ukraine War, moderating economic growth, and other macroeconomic factors

Chapter 4. Competitive Landscape

4.1. Market Share Analysis

4.1.1. Global Brewing Ingredients Market Share by Company, 2023

4.1.2. Product Offerings of Leading Brewing Ingredients Companies

4.2. Market Entropy

4.2.1. New Product Launches in the Industry

4.2.2. Mergers, Acquisitions, Joint ventures, and Partnerships

4.3. Key Strategies and Best Practices

Chapter 5. Global Market Projections: Best, Reference, and Low Case Scenarios

5.1. Growth Analysis- Case Scenario Definitions

5.2. Low Growth Case Scenario Forecasts

5.3. Reference Growth Case Scenario Forecasts

5.4. High Growth Case Scenario Forecasts

Chapter 6. Market Dynamics

6.1. Brewing Ingredients Market Drivers

6.2. Brewing Ingredients Market Challenges

6.6. Brewing Ingredients Market Opportunities

6.4. Brewing Ingredients Market Trends

Chapter 7. Global Brewing Ingredients Market Outlook Trends

7.1. Global Brewing Ingredients Revenue (USD Million) and CAGR (%) by Type (2021-2032)

7.2. Global Brewing Ingredients Revenue (USD Million) and CAGR (%) by Application (2021-2032)

7.3. Global Brewing Ingredients Revenue (USD Million) and CAGR (%) by Product (2021-2032)

By Source

Malt extract

Adjuncts/Grains

Hops

Beer yeast

Beer additives

By Brewery Size

Macro Brewery

Craft Brewery

By Form

Dry

Liquid

Chapter 8. Global Brewing Ingredients Regional Analysis and Outlook

8.1. Global Brewing Ingredients Revenue (USD Million) By Regions (2021- 2032)

8.2. North America Brewing Ingredients Revenue (USD Million) by Country (2021-2032)

8.2.1. United States Brewing Ingredients Regional Analysis and Outlook

8.2.2. Canada Brewing Ingredients Regional Analysis and Outlook

8.2.3. Mexico Brewing Ingredients Regional Analysis and Outlook

8.3. Europe Brewing Ingredients Revenue (USD Million), by Country (2021-2032)

8.3.1. Germany Brewing Ingredients Regional Analysis and Outlook

8.3.2. France Brewing Ingredients Regional Analysis and Outlook

8.3.3. United Kingdom Brewing Ingredients Regional Analysis and Outlook

8.3.4. Spain Brewing Ingredients Regional Analysis and Outlook

8.3.5. Italy Brewing Ingredients Regional Analysis and Outlook

8.3.6. Russia Brewing Ingredients Regional Analysis and Outlook

8.3.7. Rest of Europe Brewing Ingredients Regional Analysis and Outlook

8.4. Asia Pacific Brewing Ingredients Revenue (USD Million) by Country (2021-2032)

8.4.1. China Brewing Ingredients Regional Analysis and Outlook

8.4.2. Japan Brewing Ingredients Regional Analysis and Outlook

8.4.3. India Brewing Ingredients Regional Analysis and Outlook

8.4.4. South Korea Brewing Ingredients Regional Analysis and Outlook

8.4.5. Australia Brewing Ingredients Regional Analysis and Outlook

8.4.6. South East Asia Brewing Ingredients Regional Analysis and Outlook

8.4.7. Rest of Asia Pacific Brewing Ingredients Regional Analysis and Outlook

8.5. South America Brewing Ingredients Revenue (USD Million), by Country (2021-2032)

8.5.1. Brazil Brewing Ingredients Regional Analysis and Outlook

8.5.2. Argentina Brewing Ingredients Regional Analysis and Outlook

8.5.3. Rest of South America Brewing Ingredients Regional Analysis and Outlook

8.6. Middle East and Africa Brewing Ingredients Revenue (USD Million) by Country (2021-2032)

8.6.1. Middle East Brewing Ingredients Regional Analysis and Outlook

8.6.2. Africa Brewing Ingredients Regional Analysis and Outlook

Chapter 9. North America Brewing Ingredients Analysis and Outlook

9.1. North America Brewing Ingredients Revenue (USD Million) by Segments (2021-2032)

9.1.1. North America Brewing Ingredients Revenue (USD Million) by Type (2021-2032)

9.1.2. North America Brewing Ingredients Revenue (USD Million) by Application (2021-2032)

9.1.3. North America Brewing Ingredients Revenue (USD Million) by Product (2021-2032)

By Source

Malt extract

Adjuncts/Grains

Hops

Beer yeast

Beer additives

By Brewery Size

Macro Brewery

Craft Brewery

By Form

Dry

Liquid

Chapter 10. Europe Brewing Ingredients Analysis and Outlook

10.1. Europe Brewing Ingredients Revenue (USD Million), by Segments (USD Million) (2021-2032)

10.1.1. Europe Brewing Ingredients Revenue (USD Million) by Type (2021-2032)

10.1.2. Europe Brewing Ingredients Revenue (USD Million) by Application (2021-2032)

10.1.3. Europe Brewing Ingredients Revenue (USD Million) by Product (2021-2032)

By Source

Malt extract

Adjuncts/Grains

Hops

Beer yeast

Beer additives

By Brewery Size

Macro Brewery

Craft Brewery

By Form

Dry

Liquid

Chapter 11. Asia Pacific Brewing Ingredients Analysis and Outlook

11.1. Asia Pacific Brewing Ingredients Revenue (USD Million), and Revenue (USD Million) by Segments (2021-2032)

11.1.1. Asia Pacific Brewing Ingredients Revenue (USD Million) by Type (2021-2032)

11.1.2. Asia Pacific Brewing Ingredients Revenue (USD Million) by Application (2021-2032)

11.1.3. Asia Pacific Brewing Ingredients Revenue (USD Million) by Product (2021-2032)

By Source

Malt extract

Adjuncts/Grains

Hops

Beer yeast

Beer additives

By Brewery Size

Macro Brewery

Craft Brewery

By Form

Dry

Liquid

Chapter 12. South America Brewing Ingredients Analysis and Outlook

12.1. South America Brewing Ingredients Revenue (USD Million), by Segments (2021-2032)

12.1.1. South America Brewing Ingredients Revenue (USD Million) by Type (2021-2032)

12.1.2. South America Brewing Ingredients Revenue (USD Million) by Application (2021-2032)

12.1.3. South America Brewing Ingredients Revenue (USD Million) by Product (2021-2032)

By Source

Malt extract

Adjuncts/Grains

Hops

Beer yeast

Beer additives

By Brewery Size

Macro Brewery

Craft Brewery

By Form

Dry

Liquid

Chapter 13. Middle East and Africa Brewing Ingredients Analysis and Outlook

13.1. Middle East and Africa Brewing Ingredients Revenue (USD Million), by Segments (2021-2032)

13.1.1. Middle East and Africa Brewing Ingredients Revenue (USD Million) by Type (2021-2032)

13.1.2. Middle East and Africa Brewing Ingredients Revenue (USD Million) by Application (2021-2032)

13.1.3. Middle East and Africa Brewing Ingredients Revenue (USD Million) by Product (2021-2032)

By Source

Malt extract

Adjuncts/Grains

Hops

Beer yeast

Beer additives

By Brewery Size

Macro Brewery

Craft Brewery

By Form

Dry

Liquid

Chapter 14. Brewing Ingredients Company Profiles

14.1 Business Overview

14.2 Product Profiles

14.3 SWOT Profiles

14.5 Recent Developments

14.6 Financial Profile

List of Companies

Angel Yeast Co. Ltd

Boortmalt

Cargill Inc

Lallemand Inc

Lesaffre Group

Malteurop Groupe

Maltexco S.A.

Rahr Corp

Simpsons Malt

Viking Malt

15. Methodology and Data Sources

15.1 Customization Offerings

15.2 Subscription Services

15.3 Related Reports

15.4 Publisher Expertise

LIST OF TABLES

Table 1 Market Segmentation Analysis

Table 2 Global Brewing Ingredients Market Share of Leading Companies, 2023

Table 3 Product Offerings of Leading Companies

Table 4 Low Growth Scenario Forecasts

Table 5 Reference Case Growth Scenario

Table 6 High Growth Case Scenario

Table 7 Global Brewing Ingredients Revenue (USD Million) And CAGR (%) By Type (2021-2032)

Table 8 Global Brewing Ingredients Revenue (USD Million) And CAGR (%) By Application (2021-2032)

Table 9 Global Brewing Ingredients Revenue (USD Million) And CAGR (%) By Product (2021-2032)

Table 10 Global Brewing Ingredients Market Revenue (USD Million) By Regions (2021-2032)

Table 11 Global Brewing Ingredients Market Share (%) By Regions (2021-2032)

Table 12 North America Brewing Ingredients Revenue (USD Million) By Country (2021-2032)

Table 13 Europe Brewing Ingredients Revenue (USD Million) By Country (2021-2032)

Table 14 Asia Pacific Brewing Ingredients Revenue (USD Million) By Country (2021-2032)

Table 15 South America Brewing Ingredients Revenue (USD Million) By Country (2021-2032)

Table 16 Middle East and Africa Brewing Ingredients Revenue (USD Million) By Region (2021-2032)

Table 17 North America Brewing Ingredients Revenue (USD Million) By Type (2021-2032)

Table 18 North America Brewing Ingredients Revenue (USD Million) By Application (2021-2032)

Table 19 North America Brewing Ingredients Revenue (USD Million) By Product (2021-2032)

Table 20 Europe Brewing Ingredients Revenue (USD Million) By Type (2021-2032)

Table 21 Europe Brewing Ingredients Revenue (USD Million) By Application (2021-2032)

Table 22 Europe Brewing Ingredients Revenue (USD Million) By Product (2021-2032)

Table 23 Asia Pacific Brewing Ingredients Revenue (USD Million) By Type (2021-2032)

Table 24 Asia Pacific Brewing Ingredients Revenue (USD Million) By Application (2021-2032)

Table 25 Asia Pacific Brewing Ingredients Revenue (USD Million) By Product (2021-2032)

Table 26 South America Brewing Ingredients Revenue (USD Million) By Type (2021-2032)

Table 27 South America Brewing Ingredients Revenue (USD Million) By Application (2021-2032)

Table 28 South America Brewing Ingredients Revenue (USD Million) By Product (2021-2032)

Table 29 Middle East and Africa Brewing Ingredients Revenue (USD Million) By Type (2021-2032)

Table 30 Middle East and Africa Brewing Ingredients Revenue (USD Million) By Application (2021-2032)

Table 31 Middle East and Africa Brewing Ingredients Revenue (USD Million) By Product (2021-2032)

LIST OF FIGURES

Figure 1. Market Scope

Figure 2. Pricing Forecasts Per Unit, 2023- 2032

Figure 3. Porter’s Five Forces

Figure 4. Global Brewing Ingredients Market Revenue (USD Million) By Regions (2021-2032)

Figure 5. Global Brewing Ingredients Market Share (%) By Regions (2023)

Figure 6. North America Brewing Ingredients Revenue (USD Million) By Country (2021-2032)

Figure 7. United States Brewing Ingredients Revenue (USD Million) By Country (2021-2032)

Figure 8. Canada Brewing Ingredients Revenue (USD Million) By Country (2021-2032)

Figure 9. Mexico Brewing Ingredients Revenue (USD Million) By Country (2021-2032)

Figure 10. Europe Brewing Ingredients Revenue (USD Million) By Country (2021-2032)

Figure 11. Germany Brewing Ingredients Revenue (USD Million) By Country (2021-2032)

Figure 12. France Brewing Ingredients Revenue (USD Million) By Country (2021-2032)

Figure 13. United Kingdom Brewing Ingredients Revenue (USD Million) By Country (2021-2032)

Figure 14. Spain Brewing Ingredients Revenue (USD Million) By Country (2021-2032)

Figure 15. Italy Brewing Ingredients Revenue (USD Million) By Country (2021-2032)

Figure 16. Russia Brewing Ingredients Revenue (USD Million) By Country (2021-2032)

Figure 17. Rest of Europe Brewing Ingredients Revenue (USD Million) By Country (2021-2032)

Figure 11. Asia Pacific Brewing Ingredients Revenue (USD Million) By Country (2021-2032)

Figure 12. China Brewing Ingredients Revenue (USD Million) By Country (2021-2032)

Figure 13. Japan Brewing Ingredients Revenue (USD Million) By Country (2021-2032)

Figure 14. India Brewing Ingredients Revenue (USD Million) By Country (2021-2032)

Figure 15. South Korea Brewing Ingredients Revenue (USD Million) By Country (2021-2032)

Figure 16. Australia Brewing Ingredients Revenue (USD Million) By Country (2021-2032)

Figure 17. South East Asia Brewing Ingredients Revenue (USD Million) By Country (2021-2032)

Figure 18. South America Brewing Ingredients Revenue (USD Million) By Country (2021-2032)

Figure 19. Brazil Brewing Ingredients Revenue (USD Million) By Country (2021-2032)

Figure 20. Argentina Brewing Ingredients Revenue (USD Million) By Country (2021-2032)

Figure 21. Rest of Asia Pacific Brewing Ingredients Revenue (USD Million) By Country (2021-2032)

Figure 22. Middle East and Africa Brewing Ingredients Revenue (USD Million) By Region (2021-2032)

Figure 23. Saudi Arabia Brewing Ingredients Revenue (USD Million) By Region (2021-2032)

Figure 24. The UAE Brewing Ingredients Revenue (USD Million) By Region (2021-2032)

Figure 25. Rest of Middle East Brewing Ingredients Revenue (USD Million) By Region (2021-2032)

Figure 26. South Africa Brewing Ingredients Revenue (USD Million) By Region (2021-2032)

Figure 27. Africa Brewing Ingredients Revenue (USD Million) By Region (2021-2032)

Figure 28. North America Brewing Ingredients Revenue (USD Million) By Type (2021-2032)

Figure 29. North America Brewing Ingredients Revenue (USD Million) By Application (2021-2032)

Figure 30. North America Brewing Ingredients Revenue (USD Million) By Product (2021-2032)

Figure 31. Europe Brewing Ingredients Revenue (USD Million) By Type (2021-2032)

Figure 32. Europe Brewing Ingredients Revenue (USD Million) By Application (2021-2032)

Figure 33. Europe Brewing Ingredients Revenue (USD Million) By Product (2021-2032)

Figure 34. Asia Pacific Brewing Ingredients Revenue (USD Million) By Type (2021-2032)

Figure 35. Asia Pacific Brewing Ingredients Revenue (USD Million) By Application (2021-2032)

Figure 36. Asia Pacific Brewing Ingredients Revenue (USD Million) By Product (2021-2032)

Figure 37. South America Brewing Ingredients Revenue (USD Million) By Type (2021-2032)

Figure 38. South America Brewing Ingredients Revenue (USD Million) By Application (2021-2032)

Figure 39. South America Brewing Ingredients Revenue (USD Million) By Product (2021-2032)

Figure 40. Middle East and Africa Brewing Ingredients Revenue (USD Million) By Type (2021-2032)

Figure 41. Middle East and Africa Brewing Ingredients Revenue (USD Million) By Application (2021-2032)

Figure 42. Middle East and Africa Brewing Ingredients Revenue (USD Million) By Product (2021-2032)

By Source

Malt extract

Adjuncts/Grains

Hops

Beer yeast

Beer additives

By Brewery Size

Macro Brewery

Craft Brewery

By Form

Dry

Liquid

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)