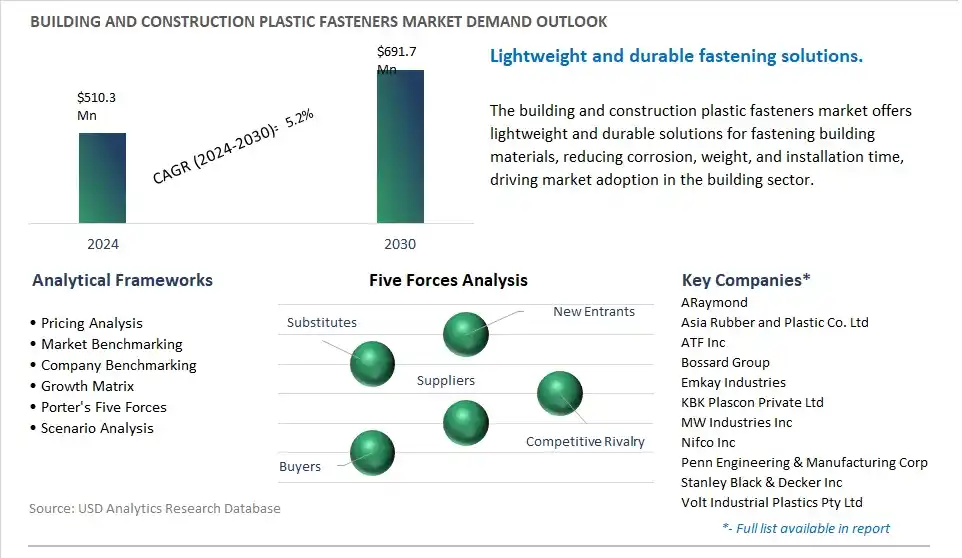

The global Building and Construction Plastic Fasteners Market is poised to register a 5.2% CAGR from $510.3 Million in 2024 to $691.7 Million in 2030.

The global Building and Construction Plastic Fasteners Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Product (Cable Ties, Rivets & Push-In Clips, Others), By Function (Bonding, Cable Management), By Distribution Channel (Direct, Third Party), By End-User (Commercial, Industrial, Residential).

An Introduction to Global Building and Construction Plastic Fasteners Market in 2024

The market for building and construction plastic fasteners is enhancing durability and efficiency in construction by providing lightweight, corrosion-resistant, and cost-effective fastening solutions for various building applications. Key trends shaping the future of this industry include advancements in plastic fastener materials, such as nylon, polypropylene, and PVC, which offer superior strength, chemical resistance, and weatherability compared to traditional metal fasteners. Additionally, developments in fastener designs, including screws, nails, anchors, and clips, cater to specific building materials and installation requirements, such as wood, drywall, concrete, and insulation. Moreover, the adoption of automated fastening tools, such as pneumatic nail guns and electric screwdrivers, enhances productivity, precision, and ergonomic comfort for construction workers, reducing installation time and labor costs. As builders, contractors, and engineers seek lightweight, durable, and corrosion-resistant fastening solutions to streamline construction processes and ensure long-term structural integrity, the demand for innovative building and construction plastic fasteners is expected to grow, driving further research, development, and market adoption in this vital segment of the construction materials industry.

Building and Construction Plastic Fasteners Market Competitive Landscape

The market report analyses the leading companies in the industry including ARaymond, Asia Rubber and Plastic Co. Ltd, ATF Inc, Bossard Group, Emkay Industries, KBK Plascon Private Ltd, MW Industries Inc, Nifco Inc, Penn Engineering & Manufacturing Corp, Stanley Black & Decker Inc, Volt Industrial Plastics Pty Ltd.

Building and Construction Plastic Fasteners Market Dynamics

Building And Construction Plastic Fasteners Market Trend: Shift Towards Lightweight and Durable Materials

A prominent trend in the market for building and construction plastic fasteners is the shift towards lightweight and durable materials. With increasing emphasis on sustainability and efficiency in construction projects, builders and contractors are seeking alternatives to traditional metal fasteners that offer comparable strength and reliability but with reduced weight and environmental impact. Plastic fasteners, such as nylon screws, anchors, and clips, are gaining popularity due to their lightweight nature, resistance to corrosion, and ease of installation. Additionally, advancements in plastic manufacturing technologies have led to the development of high-performance engineered plastics that offer superior strength and durability, making them suitable for a wide range of construction applications. As the construction industry continues to prioritize lightweight and durable materials, the demand for plastic fasteners is expected to rise, driving market growth and innovation in fastener design and materials.

Building And Construction Plastic Fasteners Market Driver: Growth in Modular Construction and Prefabrication

A key driver behind the demand for building and construction plastic fasteners is the growth in modular construction and prefabrication. As construction projects become increasingly complex and timelines become more stringent, there is a growing trend towards off-site manufacturing and assembly of building components. Modular construction and prefabrication methods rely on fasteners to join components together quickly and securely, making fastener selection a critical consideration in project planning and execution. Plastic fasteners offer advantages such as ease of handling, compatibility with a variety of materials, and resistance to rust and corrosion, making them well-suited for modular construction applications. Additionally, plastic fasteners can help reduce overall construction costs by streamlining assembly processes and minimizing labor requirements. As modular construction methods gain traction globally, the demand for building and construction plastic fasteners is expected to increase, driving market expansion and adoption of fastener solutions optimized for off-site construction techniques.

Building And Construction Plastic Fasteners Market Opportunity: Development of Eco-Friendly and Recyclable Fastener Solutions

An emerging opportunity in the market for building and construction plastic fasteners lies in the development of eco-friendly and recyclable fastener solutions. With growing concerns about plastic waste and environmental sustainability, there is a demand for fasteners that are manufactured from recycled materials or are recyclable at the end of their lifecycle. Manufacturers aim to capitalize on this opportunity by investing in research and development of fastener materials that are biodegradable, compostable, or made from renewable resources. Additionally, there is an opportunity to develop closed-loop recycling programs that enable customers to return used fasteners for repurposing or recycling into new products. By offering eco-friendly fastener solutions, manufacturers can meet the sustainability requirements of construction projects, differentiate their products in the market, and appeal to environmentally conscious customers. Embracing eco-friendly practices and materials can drive market growth and competitiveness in the building and construction plastic fasteners industry, contributing to a more sustainable built environment.

Building and Construction Plastic Fasteners Market Ecosystem

The building and construction plastic fasteners market relies on diverse key stages, with the supply of raw materials including polymers and additives from chemical companies including BASF, Dow, and LyondellBasell. These materials undergo manufacturing processes including injection molding and extrusion by established manufacturers including Hilti and Fischer, along with specialty producers focusing on specific applications including cable ties for electrical work. In construction, plastic fasteners are selected and used for various applications, requiring expertise in fastener types, sizes, and installation techniques, involving construction companies and skilled tradespeople.

Hilti and Fischer are prominent players in the building and construction plastic fasteners market, driving key stages including manufacturing, distribution, and sales. These companies, along with chemical giants including BASF, Dow, and LyondellBasell, contribute significantly to the supply chain by providing raw materials and finished products, ensuring the availability and quality of plastic fasteners for diverse construction applications worldwide.

Building and Construction Plastic Fasteners Market Share Analysis: Cable Ties held the dominant revenue share in 2024

In the Building and Construction Plastic Fasteners Market, the largest segment is cable ties, and its dominance can be attributed to diverse key factors. Cable ties are versatile fastening solutions widely used in construction applications for securing cables, wires, and other materials. Their simple yet effective design allows for quick and easy installation, making them essential components in electrical, plumbing, HVAC, and telecommunications systems. Cable ties offer strong and reliable fastening, ensuring secure bundling and organization of cables in both residential and commercial construction projects. Additionally, the increasing adoption of smart building technologies and the expansion of telecommunication networks drive the demand for cable ties in the construction industry. In addition, advancements in material technology have led to the development of cable ties with enhanced durability, weather resistance, and fire-retardant properties, further solidifying their position as the largest segment in the Building and Construction Plastic Fasteners Market. Overall, cable ties emerge as the largest segment due to their widespread use, reliability, and adaptability to various construction applications, making them indispensable components in modern building projects.

Building and Construction Plastic Fasteners Market Share Analysis: Cable Management is the fastest growing market segment over the forecast period to 2030

In the Building and Construction Plastic Fasteners Market, the fastest-growing segment is cable management, driven by diverse significant factors. Cable management fasteners play a crucial role in organizing and securing cables, wires, and conduits in construction projects, ensuring efficient and safe installation of electrical, data, and communication systems. With the increasing complexity and integration of technology in modern buildings, there is a growing demand for effective cable management solutions to maintain order, prevent cable damage, and comply with safety regulations. In addition, the rise of smart buildings, home automation, and IoT (Internet of Things) applications necessitates the installation of extensive cable networks, driving the need for innovative and adaptable cable management fasteners. Additionally, advancements in material technology have led to the development of cable management fasteners with enhanced features such as flexibility, durability, and fire resistance, further fueling their adoption in the construction industry. Further, the growing focus on energy efficiency and sustainability in building design requires efficient cable management systems to optimize the installation of renewable energy systems, lighting controls, and building automation systems, contributing to the rapid growth of the cable management segment in the Building and Construction Plastic Fasteners Market. Overall, cable management is the fastest-growing segment due to its essential role in modern construction projects and the increasing demand for efficient, safe, and adaptable solutions for managing complex cable networks.

Building and Construction Plastic Fasteners Market Share Analysis: Third Party is the fastest growing market segment over the forecast period to 2030

In the Building and Construction Plastic Fasteners Market, the fastest-growing segment is third-party distribution channels, driven by diverse significant factors. Third-party distribution channels, including wholesalers, distributors, and retailers, are experiencing rapid growth due to the increasing complexity and diversification of product offerings in the plastic fasteners market. These channels offer a wide range of plastic fasteners sourced from multiple manufacturers, providing customers with access to a comprehensive selection of products to meet their specific construction needs. In addition, third-party distributors often offer value-added services such as inventory management, technical support, and timely delivery, enhancing convenience and efficiency for construction professionals and contractors. Additionally, the expanding network of third-party distribution channels enables manufacturers to reach new markets, penetrate niche segments, and capitalize on emerging trends in the building and construction industry. Further, the growing preference for outsourcing distribution activities allows manufacturers to focus on core competencies such as product innovation and quality control, driving the reliance on third-party distribution channels for expanding market reach and driving sales growth in the Building and Construction Plastic Fasteners Market. Overall, the third-party distribution segment is experiencing fast growth due to its ability to provide a diverse range of products, value-added services, and market expansion opportunities for manufacturers in the plastic fasteners market.

Building and Construction Plastic Fasteners Market Report Scope-

By Product

Cable Ties

Rivets & Push-In Clips

Others

By Function

Bonding

Cable Management

By Distribution Channel

Direct

Third Party

By End-User

Commercial

Industrial

Residential

Building and Construction Plastic Fasteners Market Companies Profiled

ARaymond

Asia Rubber and Plastic Co. Ltd

ATF Inc

Bossard Group

Emkay Industries

KBK Plascon Private Ltd

MW Industries Inc

Nifco Inc

Penn Engineering & Manufacturing Corp

Stanley Black & Decker Inc

Volt Industrial Plastics Pty Ltd

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Building and Construction Plastic Fasteners Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Building and Construction Plastic Fasteners Market Size Outlook, $ Million, 2021 to 2030

3.2 Building and Construction Plastic Fasteners Market Outlook by Type, $ Million, 2021 to 2030

3.3 Building and Construction Plastic Fasteners Market Outlook by Product, $ Million, 2021 to 2030

3.4 Building and Construction Plastic Fasteners Market Outlook by Application, $ Million, 2021 to 2030

3.5 Building and Construction Plastic Fasteners Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Building and Construction Plastic Fasteners Industry

4.2 Key Market Trends in Building and Construction Plastic Fasteners Industry

4.3 Potential Opportunities in Building and Construction Plastic Fasteners Industry

4.4 Key Challenges in Building and Construction Plastic Fasteners Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Building and Construction Plastic Fasteners Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Building and Construction Plastic Fasteners Market Outlook by Segments

7.1 Building and Construction Plastic Fasteners Market Outlook by Segments, $ Million, 2021- 2030

By Product

Cable Ties

Rivets & Push-In Clips

Others

By Function

Bonding

Cable Management

By Distribution Channel

Direct

Third Party

By End-User

Commercial

Industrial

Residential

8 North America Building and Construction Plastic Fasteners Market Analysis and Outlook To 2030

8.1 Introduction to North America Building and Construction Plastic Fasteners Markets in 2024

8.2 North America Building and Construction Plastic Fasteners Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Building and Construction Plastic Fasteners Market size Outlook by Segments, 2021-2030

By Product

Cable Ties

Rivets & Push-In Clips

Others

By Function

Bonding

Cable Management

By Distribution Channel

Direct

Third Party

By End-User

Commercial

Industrial

Residential

9 Europe Building and Construction Plastic Fasteners Market Analysis and Outlook To 2030

9.1 Introduction to Europe Building and Construction Plastic Fasteners Markets in 2024

9.2 Europe Building and Construction Plastic Fasteners Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Building and Construction Plastic Fasteners Market Size Outlook by Segments, 2021-2030

By Product

Cable Ties

Rivets & Push-In Clips

Others

By Function

Bonding

Cable Management

By Distribution Channel

Direct

Third Party

By End-User

Commercial

Industrial

Residential

10 Asia Pacific Building and Construction Plastic Fasteners Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Building and Construction Plastic Fasteners Markets in 2024

10.2 Asia Pacific Building and Construction Plastic Fasteners Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Building and Construction Plastic Fasteners Market size Outlook by Segments, 2021-2030

By Product

Cable Ties

Rivets & Push-In Clips

Others

By Function

Bonding

Cable Management

By Distribution Channel

Direct

Third Party

By End-User

Commercial

Industrial

Residential

11 South America Building and Construction Plastic Fasteners Market Analysis and Outlook To 2030

11.1 Introduction to South America Building and Construction Plastic Fasteners Markets in 2024

11.2 South America Building and Construction Plastic Fasteners Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Building and Construction Plastic Fasteners Market size Outlook by Segments, 2021-2030

By Product

Cable Ties

Rivets & Push-In Clips

Others

By Function

Bonding

Cable Management

By Distribution Channel

Direct

Third Party

By End-User

Commercial

Industrial

Residential

12 Middle East and Africa Building and Construction Plastic Fasteners Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Building and Construction Plastic Fasteners Markets in 2024

12.2 Middle East and Africa Building and Construction Plastic Fasteners Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Building and Construction Plastic Fasteners Market size Outlook by Segments, 2021-2030

By Product

Cable Ties

Rivets & Push-In Clips

Others

By Function

Bonding

Cable Management

By Distribution Channel

Direct

Third Party

By End-User

Commercial

Industrial

Residential

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

ARaymond

Asia Rubber and Plastic Co. Ltd

ATF Inc

Bossard Group

Emkay Industries

KBK Plascon Private Ltd

MW Industries Inc

Nifco Inc

Penn Engineering & Manufacturing Corp

Stanley Black & Decker Inc

Volt Industrial Plastics Pty Ltd

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Product

Cable Ties

Rivets & Push-In Clips

Others

By Function

Bonding

Cable Management

By Distribution Channel

Direct

Third Party

By End-User

Commercial

Industrial

Residential

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)