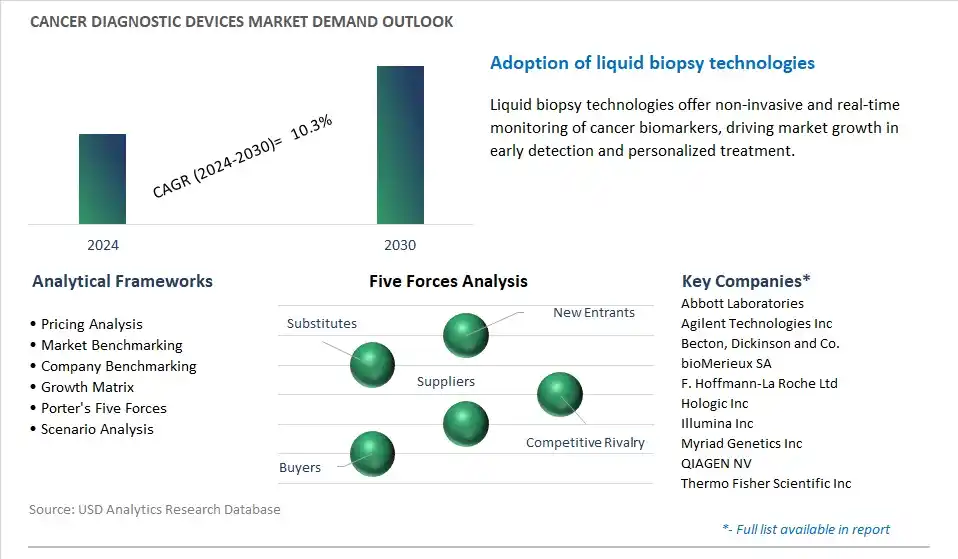

Cancer Diagnostic Devices Market is estimated to increase at a growth rate of 10.3% CAGR over the forecast period from 2024 to 2030.

The global Cancer Diagnostic Devices Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments including By Product (Molecular Diagnostics, Companion Diagnostics), By Diagnostic (Diagnostic Imaging Tests, Biopsy and Cytology Tests, Tumor Biomarkers, Others).

An Introduction to Cancer Diagnostic Devices Market in 2024

The Cancer Diagnostic Devices Market encompasses a wide range of medical devices, instruments, and technologies used in diagnosing various types of cancer. These devices include imaging modalities like computed tomography (CT), magnetic resonance imaging (MRI), positron emission tomography (PET), and biopsy tools, molecular diagnostic tests, and circulating tumor cell detection systems. In 2024, this market emphasizes early cancer detection, precision diagnostics, and advancements in imaging and molecular testing for accurate cancer diagnosis and treatment planning.

Cancer Diagnostic Devices Market Competitive Landscape

The global Cancer Diagnostic Devices Industry is highly competitive with a large number of companies focusing on niche market segments. Amidst intense competitive conditions, Cancer Diagnostic Devices Companies are investing in new product launches and strengthening distribution channels. Key companies operating in the Cancer Diagnostic Devices Industry include- Abbott Laboratories, Agilent Technologies Inc, Becton, Dickinson and Co., bioMerieux SA, F. Hoffmann-La Roche Ltd, Hologic Inc, Illumina Inc, Myriad Genetics Inc, QIAGEN NV, Thermo Fisher Scientific Inc.

Cancer Diagnostic Devices Market Trend: Advancements in Cancer Diagnostic Technologies

A significant trend in the Cancer Diagnostic Devices market is the continuous advancements in diagnostic technologies aimed at improving the accuracy, speed, and accessibility of cancer detection. Technological innovations such as next-generation sequencing (NGS), liquid biopsy, multiplexed immunohistochemistry, and artificial intelligence (AI) algorithms have revolutionized cancer diagnostics by enabling comprehensive molecular profiling, early detection of biomarkers, and non-invasive testing methods. These advancements offer healthcare providers powerful tools for diagnosing cancer at earlier stages, characterizing tumor subtypes, predicting treatment response, and monitoring disease progression. Additionally, there's a growing trend towards the development of integrated diagnostic platforms that combine multiple testing modalities to provide holistic diagnostic solutions, facilitating personalized treatment decisions and improving patient outcomes.

Cancer Diagnostic Devices Market Driver: Rising Incidence and Prevalence of Cancer Worldwide

A major driver for the Cancer Diagnostic Devices market is the rising incidence and prevalence of cancer globally, driven by aging populations, lifestyle factors, environmental exposures, and improved cancer detection and reporting. Cancer remains one of the leading causes of morbidity and mortality worldwide, with millions of new cases diagnosed each year. Early and accurate diagnosis is critical for effective cancer management and treatment, highlighting the importance of robust diagnostic technologies and infrastructure. As the burden of cancer continues to escalate, there's a growing demand for innovative diagnostic devices and assays that can reliably detect cancer at its earliest stages, facilitate precise tumor characterization, and guide personalized treatment strategies. This increasing demand for cancer diagnostic solutions drives market growth and stimulates investment in research and development aimed at advancing diagnostic capabilities and expanding access to cancer screening and testing services globally.

Cancer Diagnostic Devices Market Opportunity: Expanding Market Penetration in Emerging Economies and Underserved Regions

An opportunity for market expansion in the Cancer Diagnostic Devices market lies in increasing market penetration in emerging economies and underserved regions with high unmet needs for cancer screening and diagnostic services. Despite advances in cancer diagnostics, access to high-quality diagnostic testing remains limited in many low- and middle-income countries due to infrastructure constraints, resource limitations, and disparities in healthcare access. By focusing on expanding market reach and enhancing affordability, manufacturers of cancer diagnostic devices can tap into emerging markets and address the growing demand for cancer screening and early detection services. This includes developing cost-effective and portable diagnostic solutions suitable for resource-limited settings, establishing partnerships with local healthcare providers and governments, and investing in capacity-building initiatives to strengthen diagnostic infrastructure and healthcare delivery systems. By leveraging these opportunities, companies can contribute to reducing the global burden of cancer and improving patient outcomes worldwide.

Market Share Analysis: Molecular Diagnostics for Cancer Diagnosis is the fastest growing segment in the Cancer Diagnostic Devices industry

Among cancer diagnostic devices, the segment experiencing the fastest growth is Molecular Diagnostics. Molecular diagnostics involve the analysis of biological markers in the patient's DNA, RNA, or proteins to detect specific genetic mutations, biomarkers, or gene expressions associated with cancer. This approach offers several advantages over traditional diagnostic methods, including higher sensitivity and specificity, early detection of cancer, and personalized treatment strategies based on the patient's molecular profile. With advancements in technology and increased understanding of the molecular basis of cancer, molecular diagnostics have become increasingly important in cancer diagnosis and management. The growing demand for precision medicine and targeted therapies further drives the adoption of molecular diagnostics in oncology, making it the fastest-growing segment in the cancer diagnostic devices market.

Cancer Diagnostic Devices Market Segmentation

By Product

Molecular Diagnostics

Companion Diagnostics

By Diagnostic Type

Diagnostic Imaging Tests

Biopsy and Cytology Tests

Tumor Biomarkers

Others

Geographical Analysis

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Cancer Diagnostic Devices Companies

Abbott Laboratories

Agilent Technologies Inc

Becton, Dickinson and Co.

bioMerieux SA

F. Hoffmann-La Roche Ltd

Hologic Inc

Illumina Inc

Myriad Genetics Inc

QIAGEN NV

Thermo Fisher Scientific Inc

* List not Exhaustive

Reasons to Buy the Cancer Diagnostic Devices Market Study

• Deepen your industry insights and navigate uncertainties for strategy formulation, CAPEX, and Operational decisions

• Gain access to detailed insights on the Cancer Diagnostic Devices Market, encompassing current market size, growth trends, and forecasts till 2030.

• Access detailed competitor analysis, enabling competitive advantage through a thorough understanding of market players, strategies, and potential differentiation opportunities

• Stay ahead of the curve with insights on technological advancements, innovations, and upcoming trends

• Identify lucrative investment avenues and expansion opportunities within the Cancer Diagnostic Devices Industry, guided by robust, data-backed analysis.

• Understand regional and global markets through country-wise analysis, regional market potential, regulatory nuances, and dynamics

• Execute strategies with confidence and speed through information, analytics, and insights on the industry value chain

• Corporate leaders, strategists, financial experts, shareholders, asset managers, and governmental representatives can make long-term planning scenarios and build an integrated and timely understanding of market dynamics

• Benefit from tailored solutions and expert consultation based on report insights, providing personalized strategies aligned with specific business needs.

TABLE OF CONTENTS

1 Introduction to 2024 Cancer Diagnostic Devices Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Analyzed

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Cancer Diagnostic Devices Market Size Outlook, $ Million, 2021 to 2030

3.2 Cancer Diagnostic Devices Market Outlook by Type, $ Million, 2021 to 2030

3.3 Cancer Diagnostic Devices Market Outlook by Product, $ Million, 2021 to 2030

3.4 Cancer Diagnostic Devices Market Outlook by Application, $ Million, 2021 to 2030

3.5 Cancer Diagnostic Devices Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Cancer Diagnostic Devices Industry

4.2 Key Market Trends in Cancer Diagnostic Devices Industry

4.3 Potential Opportunities in Cancer Diagnostic Devices Industry

4.4 Key Challenges in Cancer Diagnostic Devices Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Cancer Diagnostic Devices Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Cancer Diagnostic Devices Market Outlook by Segments

7.1 Cancer Diagnostic Devices Market Outlook by Segments, $ Million, 2021- 2030

By Product

Molecular Diagnostics

Companion Diagnostics

By Diagnostic Type

Diagnostic Imaging Tests

Biopsy and Cytology Tests

Tumor Biomarkers

Others

8 North America Cancer Diagnostic Devices Market Analysis and Outlook To 2030

8.1 Introduction to North America Cancer Diagnostic Devices Markets in 2024

8.2 North America Cancer Diagnostic Devices Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Cancer Diagnostic Devices Market size Outlook by Segments, 2021-2030

By Product

Molecular Diagnostics

Companion Diagnostics

By Diagnostic Type

Diagnostic Imaging Tests

Biopsy and Cytology Tests

Tumor Biomarkers

Others

9 Europe Cancer Diagnostic Devices Market Analysis and Outlook To 2030

9.1 Introduction to Europe Cancer Diagnostic Devices Markets in 2024

9.2 Europe Cancer Diagnostic Devices Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Cancer Diagnostic Devices Market Size Outlook by Segments, 2021-2030

By Product

Molecular Diagnostics

Companion Diagnostics

By Diagnostic Type

Diagnostic Imaging Tests

Biopsy and Cytology Tests

Tumor Biomarkers

Others

10 Asia Pacific Cancer Diagnostic Devices Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Cancer Diagnostic Devices Markets in 2024

10.2 Asia Pacific Cancer Diagnostic Devices Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Cancer Diagnostic Devices Market size Outlook by Segments, 2021-2030

By Product

Molecular Diagnostics

Companion Diagnostics

By Diagnostic Type

Diagnostic Imaging Tests

Biopsy and Cytology Tests

Tumor Biomarkers

Others

11 South America Cancer Diagnostic Devices Market Analysis and Outlook To 2030

11.1 Introduction to South America Cancer Diagnostic Devices Markets in 2024

11.2 South America Cancer Diagnostic Devices Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Cancer Diagnostic Devices Market size Outlook by Segments, 2021-2030

By Product

Molecular Diagnostics

Companion Diagnostics

By Diagnostic Type

Diagnostic Imaging Tests

Biopsy and Cytology Tests

Tumor Biomarkers

Others

12 Middle East and Africa Cancer Diagnostic Devices Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Cancer Diagnostic Devices Markets in 2024

12.2 Middle East and Africa Cancer Diagnostic Devices Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Cancer Diagnostic Devices Market size Outlook by Segments, 2021-2030

By Product

Molecular Diagnostics

Companion Diagnostics

By Diagnostic Type

Diagnostic Imaging Tests

Biopsy and Cytology Tests

Tumor Biomarkers

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

List of Companies

Abbott Laboratories

Agilent Technologies Inc

Becton, Dickinson and Co.

bioMerieux SA

F. Hoffmann-La Roche Ltd

Hologic Inc

Illumina Inc

Myriad Genetics Inc

QIAGEN NV

Thermo Fisher Scientific Inc

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise