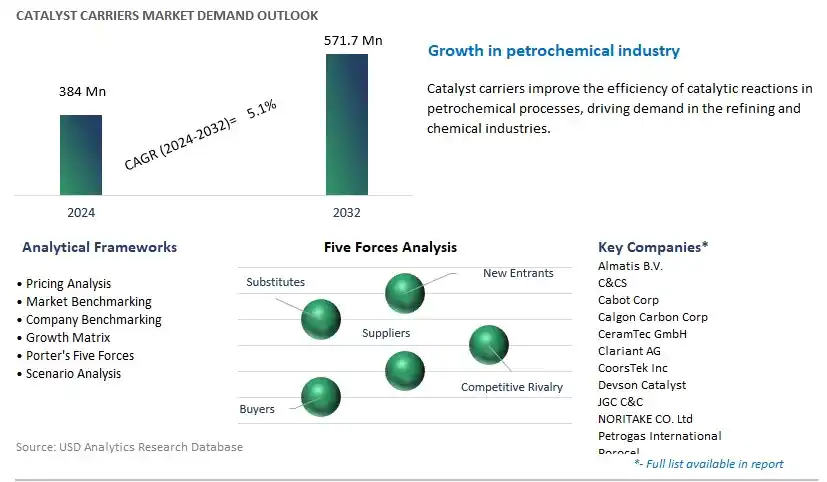

Global Catalyst Carriers Market Size is valued at $384 Million in 2024 and is forecast to register a growth rate (CAGR) of 5.1% to reach $571.7 Million by 2032.

The global Catalyst Carriers Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Product (Ceramics, Activated Carbon, Zeolites, Others), By Material (Alumina, Titania, Zirconia, Silicone Carbide, Silica, Others), By Surface Area (Low, Intermediate, High), By Composition (Spheres, Porous, Rings, Extrudate, Pellets, Powder, Honeycomb, Others), By End-User (Oil & Gas, Chemical Manufacturing, Automotive, Petrochemicals, Pharmaceuticals, Agrochemicals, Others).

An Introduction to Catalyst Carriers Market in 2024

Catalyst carriers are porous materials used to support and distribute catalysts in chemical reactions, facilitating the conversion of reactants into desired products. These carriers provide a high surface area and mechanical stability for catalyst particles, allowing for efficient contact between reactants and active sites. The market for catalyst carriers is driven by the demand for catalysts in various industries, including petrochemicals, refining, chemicals manufacturing, environmental remediation, and automotive emissions control. Catalyst carriers can be made from a variety of materials such as ceramics, metals, zeolites, and activated carbon, each offering specific properties suited to different catalytic applications. Further, advancements in carrier materials, pore structure design, and surface modification are driving innovation and market growth within the catalyst carrier industry. As industries strive to optimize chemical processes, reduce energy consumption, and minimize environmental impact, catalyst carriers play a crucial role in enhancing catalytic efficiency, selectivity, and sustainability.

Catalyst Carriers Market Competitive Landscape

The market report analyses the leading companies in the industry including Almatis B.V., C&CS, Cabot Corp, Calgon Carbon Corp, CeramTec GmbH, Clariant AG, CoorsTek Inc, Devson Catalyst, JGC C&C, NORITAKE CO. Ltd, Petrogas International, Porocel, Saint Gobain Group, Sasol Ltd, SINOCATA, Ultramet, and others.

Catalyst Carriers Market Dynamics

Market Trend: Shift Towards Sustainable and High-Performance Catalyst Carrier Materials

The market for catalyst carriers is experiencing a significant trend towards the adoption of sustainable and high-performance materials. With increasing regulatory pressure to reduce environmental impact and improve process efficiency, catalyst manufacturers are seeking innovative carrier materials that offer enhanced catalytic activity, stability, and recyclability. There's a growing preference for eco-friendly alternatives such as zeolites, alumina, silica, and carbon-based materials over traditional catalyst supports like clay and silica gel. This trend reflects a broader industry shift towards sustainability and green chemistry principles, driving the demand for catalyst carriers that enable cleaner and more efficient chemical processes while minimizing waste generation and energy consumption.

Market Driver: Expansion of Petrochemical and Chemical Manufacturing Industries

A primary driver propelling the demand for catalyst carriers is the expansion of petrochemical and chemical manufacturing industries globally. As economies continue to industrialize and demand for chemicals, fuels, and polymers rises, there's a corresponding need for catalysts that can facilitate complex chemical reactions efficiently and cost-effectively. Catalyst carriers play a crucial role in providing a stable and active surface for catalytic species, enabling the production of key industrial chemicals, fuels, and intermediates. Moreover, advancements in refining and petrochemical technologies, coupled with growing investments in infrastructure development, are driving the adoption of catalyst carriers in diverse applications such as hydroprocessing, catalytic cracking, and polymerization.

Market Opportunity: Customization and Tailoring of Catalyst Carrier Properties

An attractive opportunity within the catalyst carriers market lies in the customization and tailoring of carrier properties to meet specific application requirements. As industries demand catalysts with optimized activity, selectivity, and stability for diverse chemical processes, there's a growing need for carrier materials that can be engineered and modified to enhance performance. Manufacturers can capitalize on this opportunity by offering customized catalyst carriers with tailored pore structures, surface chemistries, and thermal stability profiles to meet the unique needs of different catalytic applications. Additionally, providing value-added services such as catalyst formulation optimization, technical support, and catalyst regeneration solutions can further differentiate offerings and strengthen relationships with customers in highly specialized industries such as refining, petrochemicals, and specialty chemicals.

Catalyst Carriers Market Share Analysis: Ceramics segment generated the highest revenue in 2024

In the realm of catalyst carriers, Ceramics is the largest segment, wielding substantial influence and driving significant market growth. In particular, ceramics offer unparalleled versatility and durability, making them indispensable in a wide array of industrial applications, including petrochemicals, chemicals, and environmental remediation. Their high surface area, thermal stability, and chemical inertness make ceramics an ideal substrate for catalyst deposition, ensuring optimal catalytic activity and longevity. Moreover, the increasing demand for clean energy solutions and environmental sustainability has propelled the adoption of ceramic-based catalyst carriers in emission control systems and renewable energy production processes. Additionally, ongoing advancements in ceramic manufacturing technologies have led to the development of tailored compositions and structures, further enhancing their performance and applicability across diverse industries. With its unmatched properties and widespread applications, the Ceramics segment continues to spearhead the catalyst carriers market, poised for sustained growth and innovation in the foreseeable future.

Catalyst Carriers Market Share Analysis: Silicon Carbide is poised to register the fastest CAGR over the forecast period

Among the diverse materials in the catalyst carriers market, Silicon Carbide is the fastest-growing segment. Silicon Carbide's surge in demand can be attributed to its exceptional properties, including high thermal conductivity, chemical inertness, and mechanical strength, making it an ideal substrate for catalyst immobilization in high-temperature processes such as petrochemical refining and automotive emissions control. Additionally, the growing emphasis on energy efficiency and environmental sustainability has spurred the adoption of Silicon Carbide-based catalyst carriers in catalytic converters and other emission reduction technologies. Furthermore, advancements in manufacturing techniques have led to the development of tailored Silicon Carbide formulations with enhanced pore structures and surface properties, further amplifying their effectiveness in catalytic applications. With its remarkable combination of performance, versatility, and environmental benefits, Silicon Carbide is poised to continue its rapid ascent in the catalyst carriers market, captivating industries and driving innovation in catalysis technology.

Catalyst Carriers Market Share Analysis: Intermediate Surface Area segment generated the highest revenue in 2024

Within the Catalyst Carriers Market, the Intermediate Surface Area segment is the largest and most influential category. The large revenue share can be attributed to the versatile nature of intermediate surface area catalyst carriers, which strike a balance between the specific surface area and pore size distribution. Catalyst carriers with intermediate surface areas offer optimal accessibility for reactants while maintaining adequate mechanical strength, making them well-suited for a wide range of catalytic applications across industries such as petroleum refining, chemical synthesis, and environmental remediation. Moreover, the demand for intermediate surface area catalyst carriers is bolstered by their ability to accommodate a diverse array of catalytic formulations, enhancing flexibility and performance in various catalytic processes. Additionally, as industries continue to prioritize efficiency, sustainability, and cost-effectiveness in catalytic operations, the versatility and reliability of intermediate surface area catalyst carriers position them as indispensable components in catalysis technology, driving their sustained dominance in the market.

Catalyst Carriers Market Share Analysis: Porous is poised to register the fastest CAGR over the forecast period

Among the various compositions in the Catalyst Carriers Market, the Porous segment is the fastest-growing category. Porous catalyst carriers offer a unique combination of high surface area, uniform pore distribution, and excellent mass transfer properties, making them highly desirable for a wide range of catalytic applications. Their porous structure facilitates efficient diffusion of reactants and products, leading to enhanced catalytic performance and process efficiency. Moreover, porous catalyst carriers exhibit versatility in accommodating different types of active catalytic materials, allowing for tailored designs to meet specific application requirements. The increasing demand for cleaner energy production, stringent environmental regulations, and the growing emphasis on sustainable manufacturing processes further propel the adoption of porous catalyst carriers in industries such as petrochemicals, chemicals, and environmental remediation. With their unmatched properties and versatility, porous catalyst carriers are poised to continue their rapid expansion, driving innovation and advancements in catalysis technology.

Catalyst Carriers Market

By Product

Ceramics

Activated Carbon

Zeolites

Others

By Material

Alumina

Titania

Zirconia

Silicone Carbide

Silica

Others

By Surface Area

Low

Intermediate

High

By Composition

Spheres

Porous

Rings

Extrudate

Pellets

Powder

Honeycomb

Others

By End-User

Oil & Gas

Chemical Manufacturing

Automotive

Petrochemicals

Pharmaceuticals

Agrochemicals

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Catalyst Carriers Companies Profiled in the Study

Almatis B.V.

C&CS

Cabot Corp

Calgon Carbon Corp

CeramTec GmbH

Clariant AG

CoorsTek Inc

Devson Catalyst

JGC C&C

NORITAKE CO. Ltd

Petrogas International

Porocel

Saint Gobain Group

Sasol Ltd

SINOCATA

Ultramet

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Catalyst Carriers Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Catalyst Carriers Market Size Outlook, $ Million, 2021 to 2032

3.2 Catalyst Carriers Market Outlook by Type, $ Million, 2021 to 2032

3.3 Catalyst Carriers Market Outlook by Product, $ Million, 2021 to 2032

3.4 Catalyst Carriers Market Outlook by Application, $ Million, 2021 to 2032

3.5 Catalyst Carriers Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Catalyst Carriers Industry

4.2 Key Market Trends in Catalyst Carriers Industry

4.3 Potential Opportunities in Catalyst Carriers Industry

4.4 Key Challenges in Catalyst Carriers Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Catalyst Carriers Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Catalyst Carriers Market Outlook by Segments

7.1 Catalyst Carriers Market Outlook by Segments, $ Million, 2021- 2032

By Product

Ceramics

Activated Carbon

Zeolites

Others

By Material

Alumina

Titania

Zirconia

Silicone Carbide

Silica

Others

By Surface Area

Low

Intermediate

High

By Composition

Spheres

Porous

Rings

Extrudate

Pellets

Powder

Honeycomb

Others

By End-User

Oil & Gas

Chemical Manufacturing

Automotive

Petrochemicals

Pharmaceuticals

Agrochemicals

Others

8 North America Catalyst Carriers Market Analysis and Outlook To 2032

8.1 Introduction to North America Catalyst Carriers Markets in 2024

8.2 North America Catalyst Carriers Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Catalyst Carriers Market size Outlook by Segments, 2021-2032

By Product

Ceramics

Activated Carbon

Zeolites

Others

By Material

Alumina

Titania

Zirconia

Silicone Carbide

Silica

Others

By Surface Area

Low

Intermediate

High

By Composition

Spheres

Porous

Rings

Extrudate

Pellets

Powder

Honeycomb

Others

By End-User

Oil & Gas

Chemical Manufacturing

Automotive

Petrochemicals

Pharmaceuticals

Agrochemicals

Others

9 Europe Catalyst Carriers Market Analysis and Outlook To 2032

9.1 Introduction to Europe Catalyst Carriers Markets in 2024

9.2 Europe Catalyst Carriers Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Catalyst Carriers Market Size Outlook by Segments, 2021-2032

By Product

Ceramics

Activated Carbon

Zeolites

Others

By Material

Alumina

Titania

Zirconia

Silicone Carbide

Silica

Others

By Surface Area

Low

Intermediate

High

By Composition

Spheres

Porous

Rings

Extrudate

Pellets

Powder

Honeycomb

Others

By End-User

Oil & Gas

Chemical Manufacturing

Automotive

Petrochemicals

Pharmaceuticals

Agrochemicals

Others

10 Asia Pacific Catalyst Carriers Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Catalyst Carriers Markets in 2024

10.2 Asia Pacific Catalyst Carriers Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Catalyst Carriers Market size Outlook by Segments, 2021-2032

By Product

Ceramics

Activated Carbon

Zeolites

Others

By Material

Alumina

Titania

Zirconia

Silicone Carbide

Silica

Others

By Surface Area

Low

Intermediate

High

By Composition

Spheres

Porous

Rings

Extrudate

Pellets

Powder

Honeycomb

Others

By End-User

Oil & Gas

Chemical Manufacturing

Automotive

Petrochemicals

Pharmaceuticals

Agrochemicals

Others

11 South America Catalyst Carriers Market Analysis and Outlook To 2032

11.1 Introduction to South America Catalyst Carriers Markets in 2024

11.2 South America Catalyst Carriers Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Catalyst Carriers Market size Outlook by Segments, 2021-2032

By Product

Ceramics

Activated Carbon

Zeolites

Others

By Material

Alumina

Titania

Zirconia

Silicone Carbide

Silica

Others

By Surface Area

Low

Intermediate

High

By Composition

Spheres

Porous

Rings

Extrudate

Pellets

Powder

Honeycomb

Others

By End-User

Oil & Gas

Chemical Manufacturing

Automotive

Petrochemicals

Pharmaceuticals

Agrochemicals

Others

12 Middle East and Africa Catalyst Carriers Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Catalyst Carriers Markets in 2024

12.2 Middle East and Africa Catalyst Carriers Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Catalyst Carriers Market size Outlook by Segments, 2021-2032

By Product

Ceramics

Activated Carbon

Zeolites

Others

By Material

Alumina

Titania

Zirconia

Silicone Carbide

Silica

Others

By Surface Area

Low

Intermediate

High

By Composition

Spheres

Porous

Rings

Extrudate

Pellets

Powder

Honeycomb

Others

By End-User

Oil & Gas

Chemical Manufacturing

Automotive

Petrochemicals

Pharmaceuticals

Agrochemicals

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Almatis B.V.

C&CS

Cabot Corp

Calgon Carbon Corp

CeramTec GmbH

Clariant AG

CoorsTek Inc

Devson Catalyst

JGC C&C

NORITAKE CO. Ltd

Petrogas International

Porocel

Saint Gobain Group

Sasol Ltd

SINOCATA

Ultramet

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Product

Ceramics

Activated Carbon

Zeolites

Others

By Material

Alumina

Titania

Zirconia

Silicone Carbide

Silica

Others

By Surface Area

Low

Intermediate

High

By Composition

Spheres

Porous

Rings

Extrudate

Pellets

Powder

Honeycomb

Others

By End-User

Oil & Gas

Chemical Manufacturing

Automotive

Petrochemicals

Pharmaceuticals

Agrochemicals

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)