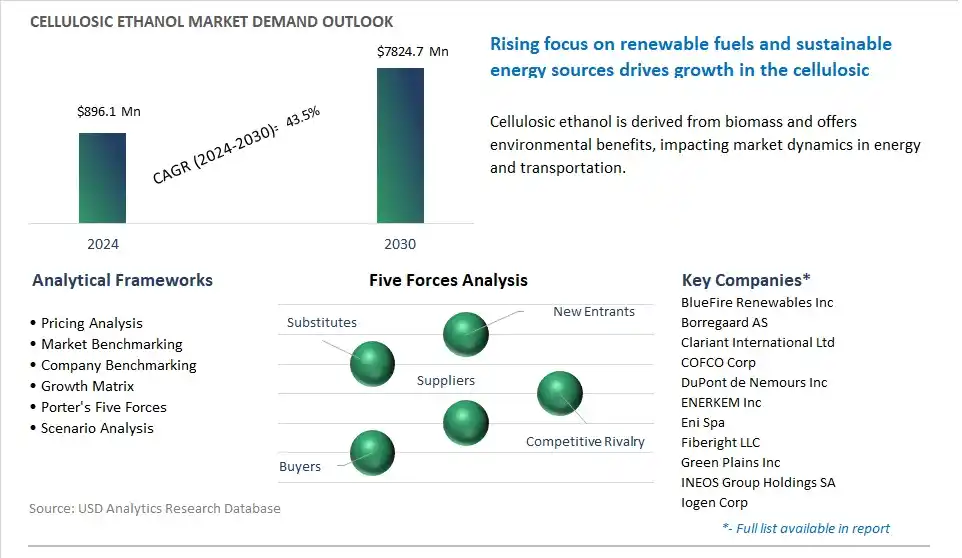

The global Cellulosic Ethanol Market is poised to register a 43.5% CAGR from $896.1 Million in 2024 to $7824.7 Million in 2030.

The global Cellulosic Ethanol Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Feedstock (Energy Crops, Agricultural residues, Organic MSW, Forest residues), By Application (Detergent, Gasoline).

An Introduction to Global Cellulosic Ethanol Market in 2024

The cellulosic ethanol market is experiencing growth driven by the increasing demand for renewable and sustainable biofuels as alternatives to fossil fuels in the transportation sector. Key trends shaping the future of the industry include innovations in cellulosic ethanol production technologies, biomass feedstock utilization, and process efficiency improvements to enhance production yields, reduce costs, and mitigate environmental impact. Advanced cellulosic ethanol processes utilize non-food biomass sources such as agricultural residues, forest residues, and dedicated energy crops, providing a sustainable and environmentally friendly feedstock for biofuel production. Moreover, the integration of advanced pretreatment methods, enzymatic hydrolysis, and fermentation technologies enables efficient conversion of cellulosic biomass into ethanol, overcoming the challenges associated with lignocellulosic feedstocks' recalcitrance. Additionally, the growing emphasis on greenhouse gas emissions reduction, energy security, and rural development drives market demand for cellulosic ethanol as a low-carbon transportation fuel with economic and environmental benefits. As governments, automotive manufacturers, and consumers prioritize renewable energy sources and carbon-neutral transportation solutions, the cellulosic ethanol market is poised for continued growth and innovation as a key contributor to the transition towards a sustainable bioeconomy.

Cellulosic Ethanol Market Competitive Landscape

The market report analyses the leading companies in the industry including BlueFire Renewables Inc, Borregaard AS, Clariant International Ltd, COFCO Corp, DuPont de Nemours Inc, ENERKEM Inc, Eni Spa, Fiberight LLC, Green Plains Inc, INEOS Group Holdings SA, Iogen Corp, Novozymes AS, Orsted AS, POET LLC, Praj Industries Ltd.

Cellulosic Ethanol Market Dynamics

Cellulosic Ethanol Market Trend: Shift towards Renewable Energy Sources

The most prominent trend in the cellulosic ethanol market is the global shift towards renewable energy sources, driven by concerns over climate change, energy security, and sustainable development. Cellulosic ethanol, derived from non-food biomass sources such as agricultural residues, forest residues, and municipal solid waste, offers a promising alternative to conventional ethanol produced from food crops such as corn or sugarcane. As governments, industries, and consumers seek to reduce greenhouse gas emissions, dependence on fossil fuels, and environmental impact, there's a growing emphasis on the production and use of cellulosic ethanol as a low-carbon transportation fuel. This trend is fueled by regulatory mandates, renewable fuel standards, and incentives promoting the adoption of biofuels, driving market growth and investment in cellulosic ethanol production technologies and infrastructure.

Cellulosic Ethanol Market Driver: Regulatory Support and Renewable Fuel Standards

A key driver in the cellulosic ethanol market is the regulatory support and renewable fuel standards implemented by governments worldwide to promote the use of biofuels and reduce reliance on fossil fuels. Regulatory initiatives such as the Renewable Fuel Standard (RFS) in the United States, the Renewable Energy Directive (RED) in the European Union, and similar mandates in other regions set targets for the blending of renewable fuels, including cellulosic ethanol, into transportation fuels. These mandates create a favorable policy environment for investment in cellulosic ethanol production facilities, research and development initiatives, and market deployment efforts. Additionally, incentives such as tax credits, grants, and loan guarantees further drive investment and innovation in cellulosic ethanol technologies, positioning it as a key driver of market growth and adoption in the renewable energy sector.

Cellulosic Ethanol Market Opportunity: Expansion into Advanced Biofuels and Chemicals

The cellulosic ethanol market presents a significant opportunity for expansion into advanced biofuels and biochemicals beyond traditional ethanol production, driven by advancements in biomass conversion technologies and biorefinery processes. Cellulosic ethanol production involves the enzymatic or chemical conversion of lignocellulosic biomass into sugars, which are then fermented into ethanol. However, beyond ethanol, the same biomass feedstocks can be used to produce a range of advanced biofuels such as renewable diesel, biobutanol, and jet fuels, as well as biochemicals such as organic acids, solvents, and platform chemicals. By leveraging integrated biorefinery concepts, co-production strategies, and process optimization techniques, manufacturers can diversify their product portfolio, maximize resource utilization, and capture additional value from cellulosic biomass, creating new revenue streams and market opportunities in the emerging bioeconomy.

Cellulosic Ethanol Market Share Analysis: Agricultural residues feedstock segment generated the highest revenue in the industry

The largest segment in the Cellulosic Ethanol Market is the Agricultural residues feedstock segment. This dominance can be attributed to diverse factors. The agricultural residues, such as corn stover, wheat straw, rice husks, and sugarcane bagasse, are abundant and readily available feedstocks for cellulosic ethanol production. These residues are generated in large quantities as by-products of agricultural activities such as harvesting, processing, and milling, making them a sustainable and cost-effective source of biomass for ethanol production. Additionally, agricultural residues offer diverse advantages as feedstocks for cellulosic ethanol production, including their high cellulose and hemicellulose content, which can be converted into fermentable sugars through enzymatic hydrolysis. In addition, the use of agricultural residues as feedstocks for cellulosic ethanol production helps to mitigate agricultural waste disposal issues, reduce greenhouse gas emissions, and promote rural economic development by providing additional revenue streams for farmers and agricultural communities. Further, advancements in biomass pretreatment, enzymatic hydrolysis, and fermentation technologies have improved the efficiency and economics of converting agricultural residues into cellulosic ethanol, further driving their dominance in the Cellulosic Ethanol Market. As industries continue to seek sustainable alternatives to fossil fuels and governments implement policies to promote biofuel production and reduce carbon emissions, the Agricultural residues feedstock segment is expected to maintain its dominance in the Cellulosic Ethanol Market.

Cellulosic Ethanol Market Share Analysis: Cellulosic Ethanol Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

Among the options provided, the fastest-growing segment in the Cellulosic Ethanol Market is the Gasoline application segment. This growth can be attributed to diverse factors. The there is a global push towards reducing greenhouse gas emissions and mitigating climate change, driving the adoption of renewable fuels as alternatives to traditional fossil fuels. Cellulosic ethanol, produced from non-food biomass sources such as agricultural residues, forest residues, and energy crops, is considered a low-carbon or carbon-neutral fuel due to its ability to sequester carbon during feedstock growth and production. Additionally, cellulosic ethanol offers diverse environmental benefits compared to gasoline, including lower emissions of greenhouse gases, particulate matter, and toxic air pollutants. In addition, cellulosic ethanol can be blended with gasoline in various proportions to create ethanol-gasoline blends such as E10 (10% ethanol, 90% gasoline) and E85 (85% ethanol, 15% gasoline), which can be used as drop-in replacements for gasoline in conventional vehicles or flex-fuel vehicles. Further, advancements in cellulosic ethanol production technology, including biomass pretreatment, enzymatic hydrolysis, and fermentation, have improved the efficiency, scalability, and cost-effectiveness of ethanol production from cellulosic feedstocks, further driving its adoption as a gasoline substitute. As governments implement renewable fuel mandates, incentivize biofuel production, and invest in bioenergy infrastructure, the Gasoline application segment is expected to experience rapid growth in the Cellulosic Ethanol Market.

Cellulosic Ethanol Market Report Segmentation

By Feedstock

Energy Crops

Agricultural residues

Organic MSW

Forest residues

By Application

Detergent

Gasoline

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Cellulosic Ethanol Companies Profiled in the Market Study

BlueFire Renewables Inc

Borregaard AS

Clariant International Ltd

COFCO Corp

DuPont de Nemours Inc

ENERKEM Inc

Eni Spa

Fiberight LLC

Green Plains Inc

INEOS Group Holdings SA

Iogen Corp

Novozymes AS

Orsted AS

POET LLC

Praj Industries Ltd

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Cellulosic Ethanol Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Cellulosic Ethanol Market Size Outlook, $ Million, 2021 to 2030

3.2 Cellulosic Ethanol Market Outlook by Type, $ Million, 2021 to 2030

3.3 Cellulosic Ethanol Market Outlook by Product, $ Million, 2021 to 2030

3.4 Cellulosic Ethanol Market Outlook by Application, $ Million, 2021 to 2030

3.5 Cellulosic Ethanol Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Cellulosic Ethanol Industry

4.2 Key Market Trends in Cellulosic Ethanol Industry

4.3 Potential Opportunities in Cellulosic Ethanol Industry

4.4 Key Challenges in Cellulosic Ethanol Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Cellulosic Ethanol Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Cellulosic Ethanol Market Outlook by Segments

7.1 Cellulosic Ethanol Market Outlook by Segments, $ Million, 2021- 2030

By Feedstock

Energy Crops

Agricultural residues

Organic MSW

Forest residues

By Application

Detergent

Gasoline

8 North America Cellulosic Ethanol Market Analysis and Outlook To 2030

8.1 Introduction to North America Cellulosic Ethanol Markets in 2024

8.2 North America Cellulosic Ethanol Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Cellulosic Ethanol Market size Outlook by Segments, 2021-2030

By Feedstock

Energy Crops

Agricultural residues

Organic MSW

Forest residues

By Application

Detergent

Gasoline

9 Europe Cellulosic Ethanol Market Analysis and Outlook To 2030

9.1 Introduction to Europe Cellulosic Ethanol Markets in 2024

9.2 Europe Cellulosic Ethanol Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Cellulosic Ethanol Market Size Outlook by Segments, 2021-2030

By Feedstock

Energy Crops

Agricultural residues

Organic MSW

Forest residues

By Application

Detergent

Gasoline

10 Asia Pacific Cellulosic Ethanol Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Cellulosic Ethanol Markets in 2024

10.2 Asia Pacific Cellulosic Ethanol Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Cellulosic Ethanol Market size Outlook by Segments, 2021-2030

By Feedstock

Energy Crops

Agricultural residues

Organic MSW

Forest residues

By Application

Detergent

Gasoline

11 South America Cellulosic Ethanol Market Analysis and Outlook To 2030

11.1 Introduction to South America Cellulosic Ethanol Markets in 2024

11.2 South America Cellulosic Ethanol Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Cellulosic Ethanol Market size Outlook by Segments, 2021-2030

By Feedstock

Energy Crops

Agricultural residues

Organic MSW

Forest residues

By Application

Detergent

Gasoline

12 Middle East and Africa Cellulosic Ethanol Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Cellulosic Ethanol Markets in 2024

12.2 Middle East and Africa Cellulosic Ethanol Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Cellulosic Ethanol Market size Outlook by Segments, 2021-2030

By Feedstock

Energy Crops

Agricultural residues

Organic MSW

Forest residues

By Application

Detergent

Gasoline

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

BlueFire Renewables Inc

Borregaard AS

Clariant International Ltd

COFCO Corp

DuPont de Nemours Inc

ENERKEM Inc

Eni Spa

Fiberight LLC

Green Plains Inc

INEOS Group Holdings SA

Iogen Corp

Novozymes AS

Orsted AS

POET LLC

Praj Industries Ltd

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Feedstock

Energy Crops

Agricultural residues

Organic MSW

Forest residues

By Application

Detergent

Gasoline

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)