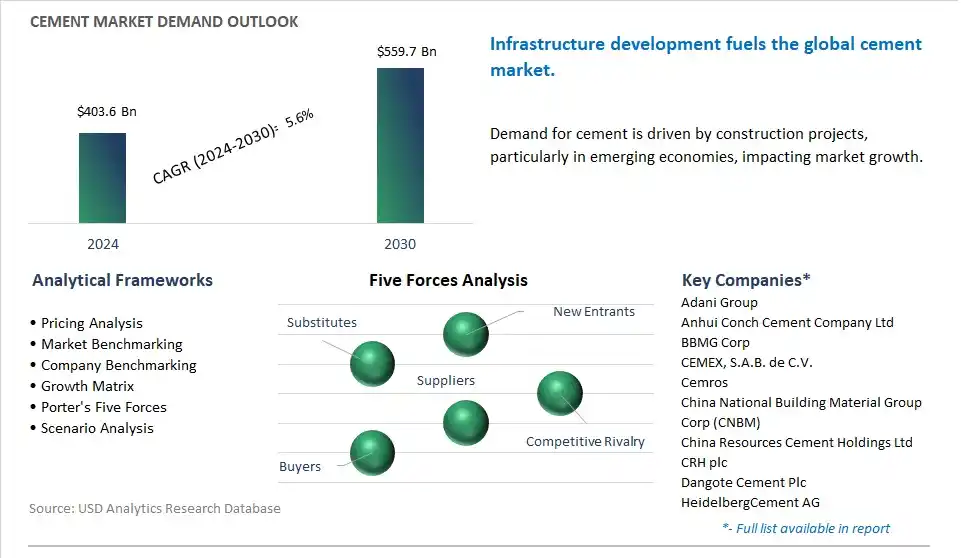

The global Cement Market is poised to register a 5.6% CAGR from $403.6 Billion in 2024 to $559.7 Billion in 2030.

The global Cement Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By End-User (Commercial, Industrial, Infrastructure, Residential), By Product (Blended Cement, Fiber Cement, Ordinary Portland Cement, White Cement, Others).

An Introduction to Global Cement Market in 2024

The cement market is witnessing significant growth driven by urbanization, infrastructure development, and construction activities worldwide. Key trends shaping the future of the industry include the increasing demand for sustainable and low-carbon cement products, driven by environmental regulations, climate change concerns, and corporate sustainability initiatives. As governments and industries prioritize carbon reduction and energy efficiency, there's a growing need for eco-friendly cement formulations such as fly ash, slag, and limestone blended cements, as well as alternative binders like geopolymers and calcium aluminate cements. Moreover, the expanding applications of cement in infrastructure projects such as roads, bridges, and airports, as well as residential and commercial construction, are driving market growth, particularly in emerging economies experiencing rapid urbanization and industrialization. Additionally, the integration of digital technologies such as Building Information Modeling (BIM), Internet of Things (IoT), and automation is revolutionizing cement manufacturing processes, optimizing resource utilization, and enhancing productivity and quality control. Furthermore, advancements in cement chemistry, production techniques, and waste utilization are improving product performance, durability, and sustainability, while regulatory compliance and quality standards ensure product reliability and safety for construction applications.

Cement Market Competitive Landscape

The market report analyses the leading companies in the industry including Adani Group, Anhui Conch Cement Company Ltd, BBMG Corp, CEMEX, S.A.B. de C.V., Cemros, China National Building Material Group Corp (CNBM), China Resources Cement Holdings Ltd, CRH plc, Dangote Cement Plc, HeidelbergCement AG, Holcim Ltd, SIG Combibloc Group AG, Taiwan Cement Corp, UltraTech Cement Ltd, Votorantim Cimentos S.A..

Cement Market Dynamics

Cement Market Trend: Shift Towards Sustainable and Green Cement

A prominent trend in the cement market is the shift towards sustainable and green cement production. With increasing environmental concerns and regulations aimed at reducing carbon emissions, there is a growing demand for cement products that have lower environmental impact. Green cement, also known as eco-friendly or sustainable cement, is produced using alternative raw materials, such as fly ash, slag, and calcined clay, and innovative manufacturing processes that result in reduced carbon dioxide emissions. This trend is driven by the construction industry's commitment to sustainability, as well as government initiatives promoting environmentally friendly building materials. As a result, manufacturers are investing in research and development to develop green cement formulations and technologies, contributing to the growth of sustainable construction practices globally.

Cement Market Driver: Infrastructure Development and Urbanization

A primary driver fueling the cement market is infrastructure development and urbanization. Cement is a fundamental building material used in the construction of infrastructure projects such as roads, bridges, dams, airports, and buildings. With rapid urbanization and population growth in emerging economies, there is a continuous demand for new infrastructure and housing developments to support growing urban populations. Moreover, government initiatives aimed at improving transportation networks, upgrading utilities, and enhancing living standards further drive the demand for cement. The construction of mega-projects such as high-speed railways, smart cities, and sustainable urban developments also contributes to the steady growth of the cement market globally.

Cement Market Opportunity: Adoption of Advanced Technologies

An opportunity within the cement market lies in the adoption of advanced technologies to enhance production efficiency, reduce costs, and improve product quality. Technologies such as automation, artificial intelligence, and digitalization offer opportunities to optimize cement manufacturing processes, streamline operations, and minimize environmental impact. Automation systems can help monitor and control production parameters in real-time, leading to increased efficiency and consistency in cement manufacturing. Additionally, innovations such as carbon capture and utilization (CCU) technologies enable cement plants to capture carbon dioxide emissions and convert them into valuable products, contributing to sustainability goals. By investing in advanced technologies and implementing best practices, cement manufacturers can enhance competitiveness, meet evolving customer demands, and capitalize on opportunities for growth in the global cement market.

Cement Market Share Analysis: Infrastructure segment generated the highest revenue in the industry

Among the delineated segments based on end-users, the Infrastructure segment is the largest in the Cement Market, propelled by diverse pivotal factors. Infrastructure projects, including roads, bridges, dams, airports, and other public works, require substantial quantities of cement for construction and maintenance. The robust demand from government-funded infrastructure initiatives, driven by urbanization, population growth, and economic development, contributes significantly to the dominance of this segment. In addition, cement's indispensable role in providing durable and long-lasting structures makes it a fundamental component in infrastructure development projects, ensuring the stability and longevity of critical infrastructure assets. Additionally, the increasing trend towards sustainable and resilient infrastructure further amplifies the demand for high-quality cement with enhanced performance characteristics. As governments worldwide prioritize infrastructure investments to address aging infrastructure, accommodate population growth, and stimulate economic growth, the Infrastructure segment continues to drive substantial demand for cement, solidifying its position as the largest segment in the Cement Market.

Cement Market Share Analysis: Blended Cement Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

Among the delineated segments based on product type, Blended Cement is the fastest-growing segment in the Cement Market, driven by diverse key factors. Blended cement, which comprises a combination of Portland cement and supplementary cementitious materials such as fly ash, slag, silica fume, or limestone, offers diverse advantages over conventional cement types. The blended cement possesses improved durability, strength, and resistance to cracking and shrinkage, making it particularly suitable for infrastructure projects and high-performance concrete applications. Additionally, blended cement contributes to reduced carbon emissions and energy consumption compared to Ordinary Portland Cement (OPC), aligning with sustainability objectives and environmental regulations. The growing emphasis on sustainable construction practices and green building certifications further accelerates the adoption of blended cement in construction projects worldwide. In addition, government policies promoting the use of supplementary cementitious materials and incentivizing sustainable construction practices propel market growth for blended cement. As stakeholders across the construction industry increasingly prioritize performance, sustainability, and cost-efficiency, the demand for blended cement continues to surge, positioning it as the fastest-growing segment in the Cement Market.

Cement Market Report Segmentation

By End-User

Commercial

Industrial

Infrastructure

Residential

By Product

Blended Cement

Fiber Cement

Ordinary Portland Cement

White Cement

Others

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Cement Companies Profiled in the Market Study

Adani Group

Anhui Conch Cement Company Ltd

BBMG Corp

CEMEX, S.A.B. de C.V.

Cemros

China National Building Material Group Corp (CNBM)

China Resources Cement Holdings Ltd

CRH plc

Dangote Cement Plc

HeidelbergCement AG

Holcim Ltd

SIG Combibloc Group AG

Taiwan Cement Corp

UltraTech Cement Ltd

Votorantim Cimentos S.A.

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Cement Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Cement Market Size Outlook, $ Million, 2021 to 2030

3.2 Cement Market Outlook by Type, $ Million, 2021 to 2030

3.3 Cement Market Outlook by Product, $ Million, 2021 to 2030

3.4 Cement Market Outlook by Application, $ Million, 2021 to 2030

3.5 Cement Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Cement Industry

4.2 Key Market Trends in Cement Industry

4.3 Potential Opportunities in Cement Industry

4.4 Key Challenges in Cement Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Cement Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Cement Market Outlook by Segments

7.1 Cement Market Outlook by Segments, $ Million, 2021- 2030

By End-User

Commercial

Industrial

Infrastructure

Residential

By Product

Blended Cement

Fiber Cement

Ordinary Portland Cement

White Cement

Others

8 North America Cement Market Analysis and Outlook To 2030

8.1 Introduction to North America Cement Markets in 2024

8.2 North America Cement Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Cement Market size Outlook by Segments, 2021-2030

By End-User

Commercial

Industrial

Infrastructure

Residential

By Product

Blended Cement

Fiber Cement

Ordinary Portland Cement

White Cement

Others

9 Europe Cement Market Analysis and Outlook To 2030

9.1 Introduction to Europe Cement Markets in 2024

9.2 Europe Cement Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Cement Market Size Outlook by Segments, 2021-2030

By End-User

Commercial

Industrial

Infrastructure

Residential

By Product

Blended Cement

Fiber Cement

Ordinary Portland Cement

White Cement

Others

10 Asia Pacific Cement Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Cement Markets in 2024

10.2 Asia Pacific Cement Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Cement Market size Outlook by Segments, 2021-2030

By End-User

Commercial

Industrial

Infrastructure

Residential

By Product

Blended Cement

Fiber Cement

Ordinary Portland Cement

White Cement

Others

11 South America Cement Market Analysis and Outlook To 2030

11.1 Introduction to South America Cement Markets in 2024

11.2 South America Cement Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Cement Market size Outlook by Segments, 2021-2030

By End-User

Commercial

Industrial

Infrastructure

Residential

By Product

Blended Cement

Fiber Cement

Ordinary Portland Cement

White Cement

Others

12 Middle East and Africa Cement Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Cement Markets in 2024

12.2 Middle East and Africa Cement Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Cement Market size Outlook by Segments, 2021-2030

By End-User

Commercial

Industrial

Infrastructure

Residential

By Product

Blended Cement

Fiber Cement

Ordinary Portland Cement

White Cement

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Adani Group

Anhui Conch Cement Company Ltd

BBMG Corp

CEMEX, S.A.B. de C.V.

Cemros

China National Building Material Group Corp (CNBM)

China Resources Cement Holdings Ltd

CRH plc

Dangote Cement Plc

HeidelbergCement AG

Holcim Ltd

SIG Combibloc Group AG

Taiwan Cement Corp

UltraTech Cement Ltd

Votorantim Cimentos S.A.

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By End-User

Commercial

Industrial

Infrastructure

Residential

By Product

Blended Cement

Fiber Cement

Ordinary Portland Cement

White Cement

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)