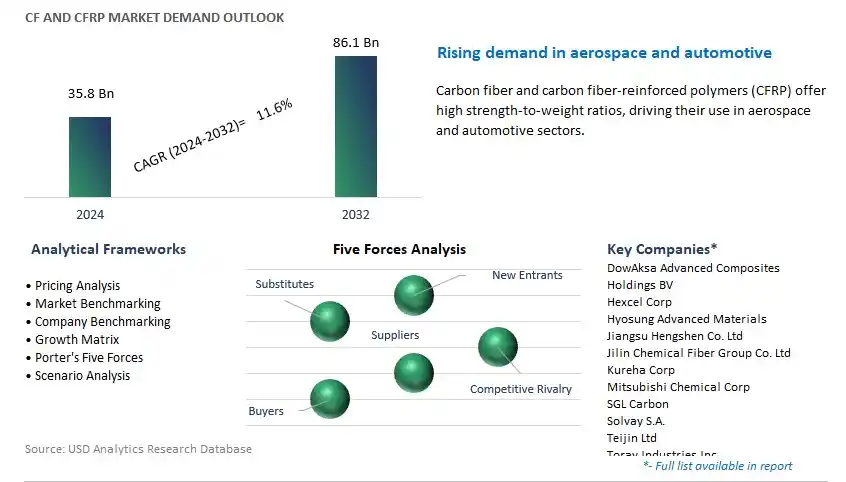

Global CF and CFRP Market Size is valued at $35.8 Billion in 2024 and is forecast to register a growth rate (CAGR) of 11.6% to reach $86.1 Billion by 2032.

The global CF and CFRP Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Precursor (PAN, Pitch, Rayon), By Source (Virgin CF, Recycled CF), By Resin (Thermosetting CFRP, Thermoplastic CFRP), By Manufacturing Process (Lay-up, Compression Molding, Resin Transfer Molding, Filament Winding, Pultrusion, Injection Molding, Others), By End-User (Aerospace & Defense, Wind Energy, Automotive, Sporting Goods, Pipes & Tanks, Marine, Medical, Electrical & Electronics, Others).

An Introduction to CF and CFRP Market in 2024

CF (Carbon Fiber) and CFRP (Carbon Fiber Reinforced Polymer) are composite materials consisting of carbon fibers embedded in a polymer matrix, typically epoxy resin. These materials offer exceptional strength, stiffness, and lightweight properties, making them ideal for high-performance applications in industries such as aerospace, automotive, sports and leisure, and construction. The market for CF and CFRP is driven by the demand for lightweight and durable materials that can replace traditional metals and alloys while offering superior mechanical properties. CF and CFRP are used in aircraft structures, automotive components, sporting equipment, wind turbine blades, and architectural structures, among other applications. They offer advantages such as high specific strength-to-weight ratio, corrosion resistance, fatigue resistance, and design flexibility. Further, advancements in carbon fiber manufacturing processes, resin formulations, and composite design optimization are driving innovation and market growth within the CF and CFRP industry. As industries to prioritize fuel efficiency, sustainability, and performance, CF and CFRP remain key materials in enabling lightweight and innovative solutions for various engineering challenges.

CF and CFRP Market Competitive Landscape

The market report analyses the leading companies in the industry including DowAksa Advanced Composites Holdings BV, Hexcel Corp, Hyosung Advanced Materials, Jiangsu Hengshen Co. Ltd, Jilin Chemical Fiber Group Co. Ltd, Kureha Corp, Mitsubishi Chemical Corp, SGL Carbon, Solvay S.A., Teijin Ltd, Toray Industries Inc, Zhongfu Shenying Carbon Co. Ltd, and others.

CF and CFRP Market Dynamics

Market Trend: Increasing Adoption in Lightweighting Solutions Across Industries

The market for carbon fiber (CF) and carbon fiber-reinforced polymers (CFRP) is witnessing a prominent trend towards increasing adoption in lightweighting solutions across industries. As industries seek to improve fuel efficiency, reduce emissions, and enhance performance, there is a growing demand for materials that offer high strength-to-weight ratios. CF and CFRP, known for their exceptional strength, stiffness, and lightweight properties, are increasingly being used in applications such as automotive components, aerospace structures, sporting goods, and wind turbine blades. This trend is driven by the need to meet regulatory requirements, achieve sustainability goals, and enhance product competitiveness in a rapidly evolving market landscape.

Market Driver: Technological Advancements in Manufacturing Processes

The market for CF and CFRP is being driven by technological advancements in manufacturing processes. Innovations such as automated layup, resin infusion, and additive manufacturing have revolutionized the production of carbon fiber composites, enabling faster production cycles, improved quality control, and cost-effective scalability. These advancements have made CF and CFRP more accessible to a wider range of industries, driving adoption across various applications. Additionally, advancements in material formulations and surface treatments have further enhanced the performance and versatility of CF and CFRP, making them increasingly attractive for lightweighting solutions. This driver is fueled by ongoing research and development efforts aimed at optimizing manufacturing processes, reducing production costs, and expanding the application potential of CF and CFRP in emerging markets.

Market Opportunity: Expansion into Infrastructure and Construction Applications

An opportunity for market expansion in the CF and CFRP industry lies in penetrating infrastructure and construction applications. While CF and CFRP are predominantly used in industries such as aerospace, automotive, and sports, there is a growing opportunity to leverage their unique properties in infrastructure projects and construction applications. CF and CFRP offer advantages such as high strength, corrosion resistance, and durability, making them ideal for reinforcing concrete structures, bridges, and building components. By targeting the infrastructure and construction sectors, manufacturers can tap into a vast market opportunity driven by urbanization, infrastructure development, and the need for sustainable building materials. This presents an opportunity to diversify product offerings, expand market reach, and drive innovation in CF and CFRP applications for infrastructure and construction projects worldwide.

CF & CFRP Market Share Analysis: PAN (Polyacrylonitrile) segment generated the highest revenue in 2024

In the CF & CFRP (Carbon Fiber and Carbon Fiber Reinforced Polymer) Market, PAN (Polyacrylonitrile) is the largest and most influential precursor segment. PAN-based carbon fibers offer superior mechanical properties, including high tensile strength, stiffness, and lightweight characteristics, making them highly sought after in various industries such as aerospace, automotive, and wind energy. PAN-based carbon fibers are widely used in the production of carbon fiber reinforced polymers (CFRP), which find applications in aircraft components, automotive parts, sporting goods, and structural materials. Moreover, PAN-based carbon fibers exhibit excellent thermal and chemical resistance, further expanding their utility across a diverse range of applications. The extensive research and development efforts aimed at enhancing PAN precursor materials and carbon fiber production processes continue to drive the dominance of PAN in the CF & CFRP Market. With its unmatched properties and versatility, PAN remains at the forefront, shaping the landscape of carbon fiber and CFRP solutions in various industries.

CF & CFRP Market Share Analysis: Recycled CF (Carbon Fiber) is poised to register the fastest CAGR over the forecast period

Among the segments in the CF & CFRP (Carbon Fiber and Carbon Fiber Reinforced Polymer) Market, Recycled CF (Carbon Fiber) is the fastest-growing segment. The increasing focus on sustainability, resource efficiency, and circular economy principles has propelled the adoption of recycled carbon fiber materials in various industries. Recycled CF offers a cost-effective and environmentally friendly alternative to virgin carbon fiber, as it utilizes reclaimed carbon fiber waste from manufacturing processes or end-of-life products. Moreover, advancements in recycling technologies have improved the quality and performance of recycled carbon fiber materials, making them suitable for a wide range of applications, including automotive components, consumer electronics, and sporting goods. Additionally, the growing demand for lightweight, high-performance materials and the implementation of stringent environmental regulations further drive the growth of recycled carbon fiber in the CF & CFRP Market. With its potential to reduce carbon emissions, minimize waste, and lower production costs, recycled carbon fiber is poised to continue its rapid ascent, reshaping the landscape of carbon fiber and CFRP solutions in various industries.

CF & CFRP Market Share Analysis: Thermosetting CFRP segment generated the highest revenue in 2024

Within the CF & CFRP (Carbon Fiber and Carbon Fiber Reinforced Polymer) Market, Thermosetting CFRP is the largest and most influential segment. Thermosetting CFRP offers exceptional mechanical properties, including high strength, stiffness, and chemical resistance, making it highly sought after in various industries such as aerospace, automotive, and construction. Thermosetting resins, such as epoxy, polyester, and vinyl ester, are commonly used in the production of CFRP due to their ability to cure into a rigid, durable matrix when exposed to heat. Moreover, thermosetting CFRP materials exhibit excellent dimensional stability and fatigue resistance, further enhancing their suitability for demanding applications. Additionally, the extensive research and development efforts focused on improving thermosetting resin formulations and manufacturing processes continue to drive the dominance of thermosetting CFRP in the market. With its unmatched properties and versatility, thermosetting CFRP remains at the forefront, shaping the landscape of carbon fiber and CFRP solutions in various industries.

CF & CFRP Market Share Analysis: Filament Winding is poised to register the fastest CAGR over the forecast period

Among the various manufacturing processes in the CF & CFRP (Carbon Fiber and Carbon Fiber Reinforced Polymer) Market, Filament Winding is the fastest-growing segment. Filament winding offers unique advantages such as high production efficiency, cost-effectiveness, and the ability to produce complex shapes with excellent fiber orientation and consistency. This process involves winding continuous carbon fiber filaments around a mandrel or mold in a predetermined pattern, followed by the impregnation with resin to form the final CFRP component. The automated nature of filament winding allows for precise control over fiber placement and resin content, resulting in CFRP products with superior mechanical properties and performance characteristics. Moreover, the growing demand for lightweight, high-strength materials in industries such as aerospace, automotive, and sporting goods further drives the adoption of filament winding technology. Additionally, advancements in filament winding equipment and materials continue to enhance production efficiency and product quality, contributing to the rapid growth of this segment in the CF & CFRP Market. With its versatility, efficiency, and ability to meet the evolving demands of various industries, filament winding technology is poised to continue its remarkable ascent, shaping the future of carbon fiber and CFRP solutions in manufacturing processes.

CF and CFRP Market

By Precursor

PAN

Pitch

Rayon

By Source

Virgin CF

Recycled CF

By Resin

Thermosetting CFRP

Thermoplastic CFRP

By Manufacturing Process

Lay-up

Compression Molding

Resin Transfer Molding

Filament Winding

Pultrusion

Injection Molding

Others

By End-User

Aerospace & Defense

Wind Energy

Automotive

Sporting Goods

Pipes & Tanks

Marine

Medical

Electrical & Electronics

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

CF and CFRP Companies Profiled in the Study

DowAksa Advanced Composites Holdings BV

Hexcel Corp

Hyosung Advanced Materials

Jiangsu Hengshen Co. Ltd

Jilin Chemical Fiber Group Co. Ltd

Kureha Corp

Mitsubishi Chemical Corp

SGL Carbon

Solvay S.A.

Teijin Ltd

Toray Industries Inc

Zhongfu Shenying Carbon Co. Ltd

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 CF and CFRP Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global CF and CFRP Market Size Outlook, $ Million, 2021 to 2032

3.2 CF and CFRP Market Outlook by Type, $ Million, 2021 to 2032

3.3 CF and CFRP Market Outlook by Product, $ Million, 2021 to 2032

3.4 CF and CFRP Market Outlook by Application, $ Million, 2021 to 2032

3.5 CF and CFRP Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of CF and CFRP Industry

4.2 Key Market Trends in CF and CFRP Industry

4.3 Potential Opportunities in CF and CFRP Industry

4.4 Key Challenges in CF and CFRP Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global CF and CFRP Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global CF and CFRP Market Outlook by Segments

7.1 CF and CFRP Market Outlook by Segments, $ Million, 2021- 2032

By Precursor

PAN

Pitch

Rayon

By Source

Virgin CF

Recycled CF

By Resin

Thermosetting CFRP

Thermoplastic CFRP

By Manufacturing Process

Lay-up

Compression Molding

Resin Transfer Molding

Filament Winding

Pultrusion

Injection Molding

Others

By End-User

Aerospace & Defense

Wind Energy

Automotive

Sporting Goods

Pipes & Tanks

Marine

Medical

Electrical & Electronics

Others

8 North America CF and CFRP Market Analysis and Outlook To 2032

8.1 Introduction to North America CF and CFRP Markets in 2024

8.2 North America CF and CFRP Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America CF and CFRP Market size Outlook by Segments, 2021-2032

By Precursor

PAN

Pitch

Rayon

By Source

Virgin CF

Recycled CF

By Resin

Thermosetting CFRP

Thermoplastic CFRP

By Manufacturing Process

Lay-up

Compression Molding

Resin Transfer Molding

Filament Winding

Pultrusion

Injection Molding

Others

By End-User

Aerospace & Defense

Wind Energy

Automotive

Sporting Goods

Pipes & Tanks

Marine

Medical

Electrical & Electronics

Others

9 Europe CF and CFRP Market Analysis and Outlook To 2032

9.1 Introduction to Europe CF and CFRP Markets in 2024

9.2 Europe CF and CFRP Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe CF and CFRP Market Size Outlook by Segments, 2021-2032

By Precursor

PAN

Pitch

Rayon

By Source

Virgin CF

Recycled CF

By Resin

Thermosetting CFRP

Thermoplastic CFRP

By Manufacturing Process

Lay-up

Compression Molding

Resin Transfer Molding

Filament Winding

Pultrusion

Injection Molding

Others

By End-User

Aerospace & Defense

Wind Energy

Automotive

Sporting Goods

Pipes & Tanks

Marine

Medical

Electrical & Electronics

Others

10 Asia Pacific CF and CFRP Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific CF and CFRP Markets in 2024

10.2 Asia Pacific CF and CFRP Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific CF and CFRP Market size Outlook by Segments, 2021-2032

By Precursor

PAN

Pitch

Rayon

By Source

Virgin CF

Recycled CF

By Resin

Thermosetting CFRP

Thermoplastic CFRP

By Manufacturing Process

Lay-up

Compression Molding

Resin Transfer Molding

Filament Winding

Pultrusion

Injection Molding

Others

By End-User

Aerospace & Defense

Wind Energy

Automotive

Sporting Goods

Pipes & Tanks

Marine

Medical

Electrical & Electronics

Others

11 South America CF and CFRP Market Analysis and Outlook To 2032

11.1 Introduction to South America CF and CFRP Markets in 2024

11.2 South America CF and CFRP Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America CF and CFRP Market size Outlook by Segments, 2021-2032

By Precursor

PAN

Pitch

Rayon

By Source

Virgin CF

Recycled CF

By Resin

Thermosetting CFRP

Thermoplastic CFRP

By Manufacturing Process

Lay-up

Compression Molding

Resin Transfer Molding

Filament Winding

Pultrusion

Injection Molding

Others

By End-User

Aerospace & Defense

Wind Energy

Automotive

Sporting Goods

Pipes & Tanks

Marine

Medical

Electrical & Electronics

Others

12 Middle East and Africa CF and CFRP Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa CF and CFRP Markets in 2024

12.2 Middle East and Africa CF and CFRP Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa CF and CFRP Market size Outlook by Segments, 2021-2032

By Precursor

PAN

Pitch

Rayon

By Source

Virgin CF

Recycled CF

By Resin

Thermosetting CFRP

Thermoplastic CFRP

By Manufacturing Process

Lay-up

Compression Molding

Resin Transfer Molding

Filament Winding

Pultrusion

Injection Molding

Others

By End-User

Aerospace & Defense

Wind Energy

Automotive

Sporting Goods

Pipes & Tanks

Marine

Medical

Electrical & Electronics

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

DowAksa Advanced Composites Holdings BV

Hexcel Corp

Hyosung Advanced Materials

Jiangsu Hengshen Co. Ltd

Jilin Chemical Fiber Group Co. Ltd

Kureha Corp

Mitsubishi Chemical Corp

SGL Carbon

Solvay S.A.

Teijin Ltd

Toray Industries Inc

Zhongfu Shenying Carbon Co. Ltd

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Precursor

PAN

Pitch

Rayon

By Source

Virgin CF

Recycled CF

By Resin

Thermosetting CFRP

Thermoplastic CFRP

By Manufacturing Process

Lay-up

Compression Molding

Resin Transfer Molding

Filament Winding

Pultrusion

Injection Molding

Others

By End-User

Aerospace & Defense

Wind Energy

Automotive

Sporting Goods

Pipes & Tanks

Marine

Medical

Electrical & Electronics

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)