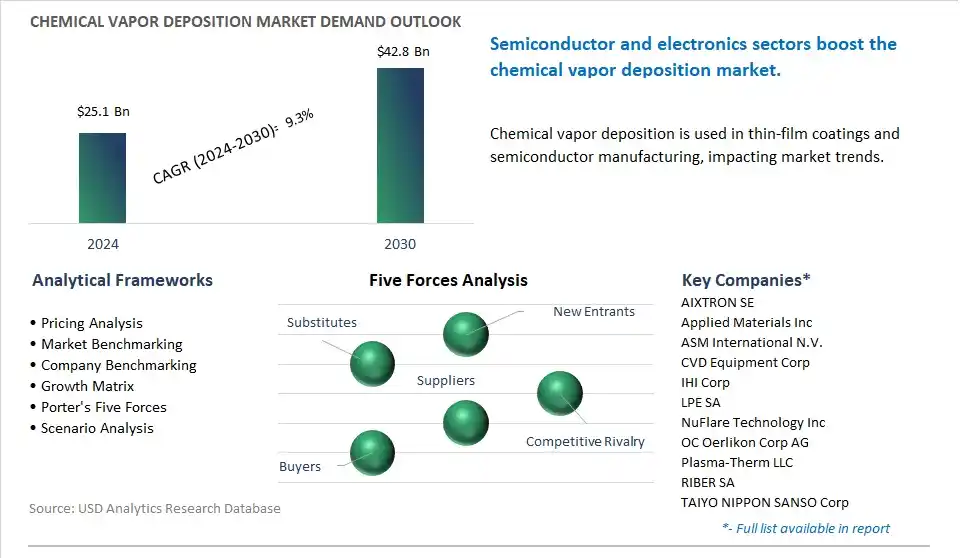

The global Chemical Vapor Deposition Market is poised to register a 9.3% CAGR from $25.1 Billion in 2024 to $42.8 Billion in 2030.

The global Chemical Vapor Deposition Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Category (CVD Equipment, CVD Materials, CVD Services), By Application (Microelectronics, Data Storage, Solar Products, Cutting Tools, Medical Equipment, Other).

An Introduction to Global Chemical Vapor Deposition Market in 2024

The chemical vapor deposition (CVD) market is witnessing steady growth driven by its applications in semiconductor manufacturing, coatings, and surface modification. Key trends shaping the future of the industry include the increasing demand for CVD equipment and materials that offer high deposition rates, uniformity, and precision in thin film deposition processes. As industries such as electronics, automotive, and aerospace seek to enhance product performance, durability, and functionality, there's a growing need for advanced CVD technologies capable of depositing thin films with tailored properties such as conductivity, optical transparency, and thermal stability. Moreover, advancements in CVD process control, substrate compatibility, and precursor materials are enabling the deposition of complex and multifunctional coatings on diverse substrates, driving market expansion. Additionally, the integration of novel CVD techniques such as atomic layer deposition (ALD) and plasma-enhanced chemical vapor deposition (PECVD) is enabling the fabrication of nanoscale structures, coatings, and devices with precise control over thickness, composition, and morphology. Furthermore, the development of CVD equipment with enhanced automation, scalability, and cost-effectiveness is enabling the widespread adoption of CVD technology in research, development, and production applications across various industries.

Chemical Vapor Deposition Market Competitive Landscape

The market report analyses the leading companies in the industry including AIXTRON SE, Applied Materials Inc, ASM International N.V., CVD Equipment Corp, IHI Corp, LPE SA, NuFlare Technology Inc, OC Oerlikon Corp AG, Plasma-Therm LLC, RIBER SA, TAIYO NIPPON SANSO Corp, Tokyo Electron Ltd, ULVAC Inc, Veeco Instruments Inc, voestalpine AG.

Chemical Vapor Deposition Market Dynamics

Chemical Vapor Deposition Market Trend: Growing Demand for Advanced Materials in Semiconductor and Electronics Industries

A prominent trend in the chemical vapor deposition (CVD) market is the increasing demand for advanced materials used in semiconductor and electronics manufacturing. As technology continues to advance, there is a rising need for thin films and coatings with specific properties such as high conductivity, thermal stability, and optical transparency. This trend is fueled by the rapid expansion of industries such as consumer electronics, automotive electronics, and renewable energy, driving the adoption of CVD techniques for depositing precise and uniform layers of materials onto substrates. Additionally, emerging applications in areas like nanotechnology and biomedicine are further driving the demand for CVD processes, highlighting a growing market opportunity for innovative deposition solutions.

Chemical Vapor Deposition Market Driver: Technological Advancements and R&D Investments

The primary driver shaping the CVD market is ongoing technological advancements and substantial investments in research and development (R&D). With a constant emphasis on enhancing material properties, deposition processes, and equipment capabilities, manufacturers are pushing the boundaries of CVD technology to meet the evolving needs of various industries. Investments in R&D lead to the development of novel precursors, deposition techniques, and equipment designs, enabling improved film quality, higher deposition rates, and greater control over material characteristics. Moreover, collaborations between academia, government agencies, and industry players drive innovation and foster the commercialization of cutting-edge CVD solutions, driving market growth and competitiveness.

Chemical Vapor Deposition Market Opportunity: Expansion into Emerging Applications and Industries

A significant opportunity within the CVD market lies in expanding into emerging applications and industries beyond traditional semiconductor and electronics sectors. As advancements in material science and manufacturing technologies continue, new opportunities are emerging in areas such as energy storage, aerospace, healthcare, and automotive. For instance, CVD is increasingly being utilized for depositing coatings on battery electrodes, manufacturing lightweight composites for aerospace components, and producing biomedical implants with tailored surface properties. By diversifying their product offerings and targeting these emerging sectors, CVD manufacturers can capitalize on growing demand and establish themselves as key players in a broader range of industries, driving revenue growth and market expansion.

Chemical Vapor Deposition Market Share Analysis: CVD Equipment segment generated the highest revenue in the industry

Among the delineated segments based on category, CVD Equipment is the largest segment in the Chemical Vapor Deposition (CVD) Market, driven by diverse pivotal factors. CVD equipment refers to the specialized machinery, systems, and tools used in the chemical vapor deposition process to deposit thin films or coatings onto substrates with precision and control. The dominance of the CVD Equipment segment is driven by CVD equipment represents the foundational technology and infrastructure required for performing chemical vapor deposition processes across various industries and applications, including semiconductor manufacturing, aerospace, automotive, optics, and electronics. As such, the demand for CVD equipment is closely tied to the broader adoption of CVD technology in these industries for applications such as thin film deposition, surface modification, and materials synthesis. Additionally, advancements in CVD equipment design, automation, and process control capabilities enhance productivity, reliability, and scalability, making them indispensable assets for research, development, and production activities. In addition, the growing demand for advanced materials with tailored properties, such as high conductivity, optical transparency, and thermal stability, drives investments in CVD equipment for the deposition of functional coatings and thin films on diverse substrates. Further, the proliferation of emerging technologies and applications, such as nanotechnology, microelectronics, and renewable energy, expands the scope of CVD equipment usage, driving market growth. As industries continue to innovate and seek advanced materials and surface engineering solutions, the CVD Equipment segment maintains its dominance in the Chemical Vapor Deposition Market, reflecting its pivotal role in enabling technological advancements and product innovation across diverse sectors.

Chemical Vapor Deposition Market Share Analysis: Solar Products Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

Among the delineated segments based on application, Solar Products emerge as the fastest-growing segment in the Chemical Vapor Deposition (CVD) Market, driven by diverse compelling factors. The rapid growth of the Solar Products segment can be attributed to diverse key trends and developments in the solar energy industry. The the increasing global focus on renewable energy sources, coupled with advancements in photovoltaic (PV) technology, drives the demand for high-efficiency solar cells and modules. Chemical vapor deposition plays a critical role in the fabrication of thin-film solar cells, such as cadmium telluride (CdTe) and copper indium gallium selenide (CIGS), which offer advantages in terms of flexibility, light weight, and manufacturing scalability compared to traditional crystalline silicon solar cells. Additionally, CVD processes enable the deposition of thin-film coatings, such as anti-reflective coatings and passivation layers, which enhance the performance and durability of solar panels, leading to increased energy conversion efficiency and longevity. In addition, the declining costs of solar energy technologies and government incentives for renewable energy adoption further stimulate investments in solar power generation, driving the demand for CVD equipment and materials in solar product manufacturing. Further, technological advancements and innovation in CVD processes, equipment, and materials contribute to the continuous improvement of solar cell efficiency, cost-effectiveness, and sustainability, fostering market growth. As the world transitions towards a clean energy future and solar energy becomes increasingly competitive with conventional energy sources, the Solar Products segment experiences rapid growth in the Chemical Vapor Deposition Market, reflecting its pivotal role in advancing solar technology and expanding renewable energy deployment worldwide.

Chemical Vapor Deposition Market Report Segmentation

By Category

CVD Equipment

CVD Materials

CVD Services

By Application

Microelectronics

Data Storage

Solar Products

Cutting Tools

Medical Equipment

Other

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Chemical Vapor Deposition Companies Profiled in the Market Study

AIXTRON SE

Applied Materials Inc

ASM International N.V.

CVD Equipment Corp

IHI Corp

LPE SA

NuFlare Technology Inc

OC Oerlikon Corp AG

Plasma-Therm LLC

RIBER SA

TAIYO NIPPON SANSO Corp

Tokyo Electron Ltd

ULVAC Inc

Veeco Instruments Inc

voestalpine AG

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Chemical Vapor Deposition Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Chemical Vapor Deposition Market Size Outlook, $ Million, 2021 to 2030

3.2 Chemical Vapor Deposition Market Outlook by Type, $ Million, 2021 to 2030

3.3 Chemical Vapor Deposition Market Outlook by Product, $ Million, 2021 to 2030

3.4 Chemical Vapor Deposition Market Outlook by Application, $ Million, 2021 to 2030

3.5 Chemical Vapor Deposition Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Chemical Vapor Deposition Industry

4.2 Key Market Trends in Chemical Vapor Deposition Industry

4.3 Potential Opportunities in Chemical Vapor Deposition Industry

4.4 Key Challenges in Chemical Vapor Deposition Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Chemical Vapor Deposition Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Chemical Vapor Deposition Market Outlook by Segments

7.1 Chemical Vapor Deposition Market Outlook by Segments, $ Million, 2021- 2030

By Category

CVD Equipment

CVD Materials

CVD Services

By Application

Microelectronics

Data Storage

Solar Products

Cutting Tools

Medical Equipment

Other

8 North America Chemical Vapor Deposition Market Analysis and Outlook To 2030

8.1 Introduction to North America Chemical Vapor Deposition Markets in 2024

8.2 North America Chemical Vapor Deposition Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Chemical Vapor Deposition Market size Outlook by Segments, 2021-2030

By Category

CVD Equipment

CVD Materials

CVD Services

By Application

Microelectronics

Data Storage

Solar Products

Cutting Tools

Medical Equipment

Other

9 Europe Chemical Vapor Deposition Market Analysis and Outlook To 2030

9.1 Introduction to Europe Chemical Vapor Deposition Markets in 2024

9.2 Europe Chemical Vapor Deposition Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Chemical Vapor Deposition Market Size Outlook by Segments, 2021-2030

By Category

CVD Equipment

CVD Materials

CVD Services

By Application

Microelectronics

Data Storage

Solar Products

Cutting Tools

Medical Equipment

Other

10 Asia Pacific Chemical Vapor Deposition Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Chemical Vapor Deposition Markets in 2024

10.2 Asia Pacific Chemical Vapor Deposition Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Chemical Vapor Deposition Market size Outlook by Segments, 2021-2030

By Category

CVD Equipment

CVD Materials

CVD Services

By Application

Microelectronics

Data Storage

Solar Products

Cutting Tools

Medical Equipment

Other

11 South America Chemical Vapor Deposition Market Analysis and Outlook To 2030

11.1 Introduction to South America Chemical Vapor Deposition Markets in 2024

11.2 South America Chemical Vapor Deposition Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Chemical Vapor Deposition Market size Outlook by Segments, 2021-2030

By Category

CVD Equipment

CVD Materials

CVD Services

By Application

Microelectronics

Data Storage

Solar Products

Cutting Tools

Medical Equipment

Other

12 Middle East and Africa Chemical Vapor Deposition Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Chemical Vapor Deposition Markets in 2024

12.2 Middle East and Africa Chemical Vapor Deposition Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Chemical Vapor Deposition Market size Outlook by Segments, 2021-2030

By Category

CVD Equipment

CVD Materials

CVD Services

By Application

Microelectronics

Data Storage

Solar Products

Cutting Tools

Medical Equipment

Other

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

AIXTRON SE

Applied Materials Inc

ASM International N.V.

CVD Equipment Corp

IHI Corp

LPE SA

NuFlare Technology Inc

OC Oerlikon Corp AG

Plasma-Therm LLC

RIBER SA

TAIYO NIPPON SANSO Corp

Tokyo Electron Ltd

ULVAC Inc

Veeco Instruments Inc

voestalpine AG

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Category

CVD Equipment

CVD Materials

CVD Services

By Application

Microelectronics

Data Storage

Solar Products

Cutting Tools

Medical Equipment

Other

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)