Market Analysis: Cloud Microservices Market Surges Ahead with Serverless, AI, and Next-Gen Container Innovations

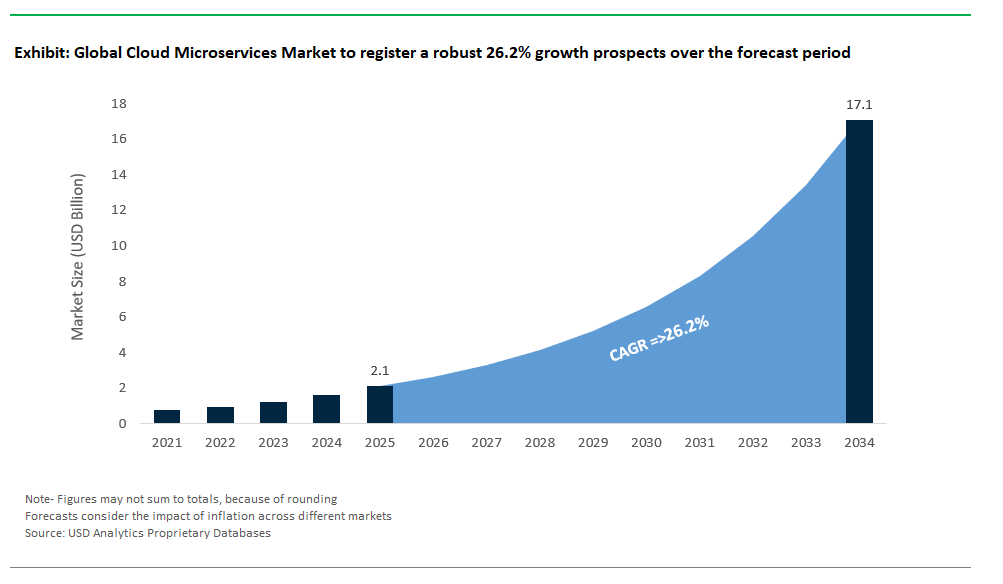

The Global Cloud Microservices Market Size is estimated at $2.1 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 26.2% to reach $17.1 Billion by 2034.

The cloud microservices market is undergoing rapid evolution as global tech giants and enterprise platforms introduce new capabilities for scalability, AI, and developer agility. In May 2025, Amazon Web Services (AWS) announced the general availability of Aurora DSQL, a groundbreaking serverless distributed SQL database with virtually unlimited scale. Tailored for event-driven and microservices architectures, Aurora DSQL offers multi-region resilience and high throughput, setting a new standard for scalable microservices deployment. Meanwhile, Google Cloud is boosting its edge in AI and machine learning by enabling NVIDIA GPU support on Cloud Run, its serverless container platform, allowing developers to run GPU-accelerated workloads as microservices a major performance leap for AI/ML-driven applications.

The leading cloud platforms are reinforcing their dominance in microservices infrastructure and serverless computing. Microsoft Azure was named a Leader in Forrester’s Q2 2025 Wave for Serverless Development Platforms, highlighting Azure’s strong scale and enterprise feature set for microservices deployment. At IBM Think 2025, IBM spotlighted a unified, composable cloud foundation for enterprise AI emphasizing how microservices architectures will be the backbone of scalable, hybrid AI environments. Snowflake signaled the convergence of data platforms and microservices by unveiling Snowpark Container Services (now in preview), empowering organizations to run containerized data-processing microservices directly within the Snowflake environment for greater flexibility and performance.

Security, developer experience, and advanced data workloads are further driving innovation in the cloud microservices market. Microsoft announced Azure Confidential Containers, a solution that enables Kubernetes-based microservices workloads to run with hardware-enforced memory encryption for end-to-end data confidentiality. In precision health, DNAnexus integrated NVIDIA NIM and CUDA-X microservices into its cloud platform to accelerate genomic research, drug discovery, and clinical analytics proving the value of microservices in vertical AI-driven use cases. Meanwhile, Red Hat’s ongoing expansion of the OpenShift Kubernetes platform continues to enhance security, scalability, and ease of management for deploying and orchestrating microservices across hybrid and multi-cloud landscapes. Collectively, these advancements underscore a dynamic, competitive, and innovation-driven future for the cloud microservices market powering digital transformation for enterprises worldwide.

Key Innovations in the Cloud Microservices Market

Trend: Real-Time Latency Optimization for Financial Transaction Processing

The Cloud Microservices market is evolving rapidly as financial institutions and high-frequency trading platforms demand real-time latency optimization to maintain a competitive edge. Ultra-low latency is now a critical performance metric in applications such as trade settlement, where milliseconds can significantly impact profitability and risk exposure. To address this, developers are implementing advanced deterministic scheduling algorithms within cloud orchestration platforms, drastically reducing processing delays. These innovations enhance transaction throughput, improving settlement speed and compliance in fast-moving financial markets.

A transformative development within this trend is the integration of microservices architecture with hardware accelerators such as Field-Programmable Gate Arrays (FPGAs). By leveraging FPGA-based acceleration alongside containerized microservices, financial platforms achieve both agility and performance, enabling dynamic scaling while maintaining deterministic execution. This convergence not only minimizes latency but also optimizes infrastructure utilization, significantly reducing total cost of ownership. For high-frequency trading environments where performance and cost-efficiency are paramount, real-time latency optimization through microservices-driven architectures is becoming a strategic imperative.

Opportunity: Safety-Critical Microservices in Automotive (ISO 26262 Compliance)

The automotive sector presents a substantial growth opportunity for cloud microservices, particularly in safety-critical systems governed by ISO 26262 standards. As vehicles transition toward higher autonomy levels, ensuring software reliability, traceability, and compliance has become a top priority. Combining AUTOSAR Adaptive platforms with microservices-based architectures is emerging as a key strategy to meet these rigorous requirements. This approach not only enables modular, upgradable software but also significantly reduces OTA (over-the-air) update failure rates a critical factor for maintaining vehicle safety and performance integrity.

The regulatory landscape is expanding to demand aerospace-level digital traceability concepts, making microservices essential for achieving Automotive Safety Integrity Level D (ASIL-D) compliance. These frameworks allow for granular tracking of software changes, ensuring accountability and functional safety throughout the vehicle lifecycle. With autonomous driving systems projected to become increasingly complex, demand for compliant microservices solutions is poised to surge, creating a multi-billion-dollar addressable market. Cloud service providers that can deliver ISO 26262-compliant microservices, coupled with robust data integrity solutions, will gain a significant competitive advantage as automotive OEMs prioritize safety and regulatory adherence in next-generation vehicles.

Competitive Landscape: Cloud Microservices Market

AWS: Dominating Cloud Microservices with Comprehensive and Scalable Offerings

Amazon Web Services (AWS) firmly holds its position as the world’s leading provider in the cloud microservices market, leveraging the broadest and deepest portfolio of microservices infrastructure and tools available today. AWS supports every stage of the microservices lifecycle from container orchestration with Amazon EKS and ECS to fully managed serverless compute with AWS Lambda and AWS Fargate, empowering organizations to scale applications without infrastructure headaches. AWS also provides a seamless developer experience through integrated DevOps tools such as AWS CodePipeline, CodeBuild, and CDK, accelerating the deployment and management of complex microservices architectures. Its advanced application integration services including Amazon SQS, SNS, EventBridge, API Gateway, and AppSync streamline asynchronous messaging and API management for cloud-native microservices. With managed databases like Amazon DynamoDB and Aurora, developers can build highly scalable, resilient, and flexible cloud applications. Recent innovations, such as deep AI/ML integration across services and enhanced serverless capabilities, ensure AWS remains at the forefront of modern application development. Ongoing investments in hybrid and multi-cloud support further solidify AWS as the top choice for enterprises seeking to modernize legacy systems, orchestrate large-scale distributed workloads, and capitalize on the agility of microservices.

Microsoft Azure: Enterprise-Ready Microservices with Deep Integration and Hybrid Cloud Strength

Microsoft Azure continues to gain market share as a premier destination for enterprise microservices, offering robust solutions that emphasize developer productivity, application resilience, and seamless integration with existing IT environments. Azure’s platform excels with Azure Kubernetes Service (AKS) for managed container orchestration, Azure Functions for serverless compute, and Azure Container Apps for flexible, event-driven architectures all tightly integrated with enterprise-grade messaging (Azure Service Bus, Event Grid, API Management) and databases (Azure Cosmos DB, Azure SQL, and more). Azure’s commitment to developer empowerment is reflected in Azure DevOps and the deep integration of Dapr, streamlining common microservices challenges such as state management, pub/sub, and service invocation. Azure also leads in observability and monitoring with Azure Monitor and Application Insights, ensuring end-to-end visibility and performance optimization for distributed microservices. Recent advancements in AI and machine learning, coupled with Azure’s strong hybrid cloud and multi-cloud capabilities, allow businesses to deploy microservices across on-premises, cloud, and edge environments without compromise. Updated architecture guidance, security enhancements, and enterprise support position Microsoft Azure as a leading platform for mission-critical microservices at scale.

Google Cloud: Kubernetes Leadership and GenAI Integration Fueling Microservices Innovation

Google Cloud Platform (GCP) is synonymous with developer-centric cloud microservices, built upon its unmatched expertise in Kubernetes and open-source cloud-native technologies. Google Kubernetes Engine (GKE) remains a benchmark for container orchestration, offering superior scalability, automated upgrades, and advanced security. For organizations pursuing serverless-first strategies, Cloud Run and Cloud Functions enable seamless deployment of event-driven, auto-scaling microservices. GCP’s robust integration and messaging capabilities such as Cloud Pub/Sub, Apigee API Management, and Anthos Service Mesh allow for powerful, secure communication between microservices, whether deployed on Google Cloud or in hybrid, multi-cloud environments. Google’s database portfolio, featuring Cloud Spanner, Firestore, and Cloud SQL, supports applications requiring global scalability and low latency. The integration of Vertex AI and GenAI tools across GCP enables the rapid development of intelligent microservices, from personalized recommendations to advanced chatbots. Google Cloud’s focus on simplifying microservices with serverless technologies, deep observability via Operations Suite, and Anthos for consistent multi-cloud management positions it as the go-to choice for organizations seeking agility, innovation, and operational excellence in the cloud microservices market.

IBM Cloud: Enterprise Microservices Transformation with Hybrid, Open Source, and AI Capabilities

IBM Cloud brings a strong enterprise pedigree to the cloud microservices market, helping organizations modernize legacy applications and accelerate their digital transformation journeys. IBM Cloud Kubernetes Service and IBM Cloud Code Engine provide managed, scalable environments for deploying containerized and serverless microservices, while IBM Cloud Functions leverages open-source Apache OpenWhisk for flexible event-driven workloads. IBM’s rich integration suite, featuring API Gateway, Event Streams (Kafka), and IBM MQ, ensures reliable and high-throughput messaging for complex microservices ecosystems. A standout strength is IBM’s hybrid cloud strategy, anchored by Red Hat OpenShift, which allows seamless deployment and management of microservices across on-premises, private, and public cloud infrastructures. IBM’s microservices builder tools, robust DevOps pipelines, and comprehensive monitoring (with Sysdig and LogDNA) ensure security and performance at every stage. The integration of watsonx AI further distinguishes IBM Cloud, enabling enterprises to build and deploy AI-powered microservices that drive automation and insight. Continuous investment in modernization, security, and industry-specific solutions makes IBM Cloud a strategic partner for enterprises navigating cloud-native transformation.

Alibaba Cloud: Cloud-Native Microservices at Scale with AI and Industry-Focused Solutions

Alibaba Cloud is a formidable force in the global cloud microservices market, particularly across Asia and emerging international markets. The platform’s Apsara-based services, such as ACK (Alibaba Cloud Kubernetes), Function Compute, and Container Compute Service, deliver powerful tools for container orchestration and serverless microservices deployment at massive scale. Alibaba Cloud’s Microservice Engine (MSE) consolidates governance, service registry, and distributed middleware, simplifying the development and management of large, enterprise-grade microservices ecosystems. With a suite of robust messaging services (ApsaraMQ, EventBridge), managed databases (ApsaraDB), and an Istio-based service mesh, Alibaba Cloud empowers organizations to build high-performance, resilient applications. The platform’s SOFAStack™ further supports financial-grade, mission-critical microservices architectures. Continuous AI innovation exemplified by Lingma (AI coding assistant), Model Studio, and industry-focused tools enables intelligent microservices and automation. Enhanced security offerings, DevOps pipelines, and comprehensive monitoring tools address the operational challenges of modern microservices. Alibaba Cloud’s focus on industry-specific solutions, security, and ongoing investment in cloud-native services make it a compelling partner for enterprises seeking to accelerate microservices adoption and digital transformation.

Market Share and Segmentation Insights: Cloud Microservices Market

By Component: Solutions Lead, Services Accelerate with Cloud-Native Shift

The cloud microservices market is led by solutions, accounting for 70.2% market share in 2025. This dominance is fueled by enterprises prioritizing scalable, containerized platforms such as Kubernetes and Docker to accelerate development cycles, enhance agility, and optimize cloud resource utilization. As organizations modernize legacy applications, microservices solutions offer unmatched flexibility and resilience in distributed environments. Meanwhile, services are the fastest-growing segment, expanding at a CAGR of 27.1%, as businesses increasingly rely on consulting, integration, and managed support to navigate the complexities of cloud-native transformation. The rise in demand for custom migration, orchestration, and DevOps expertise is pushing service providers to innovate around automation and end-to-end lifecycle management.

By End-User Industry: IT & Telecom Dominate, Retail & E-commerce Grow Fastest

Within end-user industries, IT & telecommunications hold the largest market share at 24.8% in 2025, driven by rapid cloud adoption and 5G network integration, which require microservices to manage network slicing, automation, and real-time analytics. However, retail and e-commerce is the fastest-growing industry segment, posting a robust CAGR of 28.1%. This surge is powered by the sector’s need for real-time inventory management, personalized shopping experiences, and API-driven omni-channel strategies. Healthcare is also surging, as digital transformation initiatives such as telemedicine, EHR systems, and connected devices depend on microservices for scalability and security. BFSI, media & entertainment, government, and logistics are steadily expanding their microservices adoption to support agile business models, seamless customer experiences, and faster innovation cycles.

.png)

United States: Cloud Microservices Market Trends and Enterprise Adoption

The United States stands as the dominant force in the global cloud microservices market, claiming a 43.2% revenue share in 2024 due to its robust cloud infrastructure and early enterprise adoption. By December 2024, major public cloud providers such as AWS, Microsoft Azure, and Google Cloud Platform collectively hosted more than 5.1 billion API calls daily across 2.4 million services, with 1.9 million new microservices deployments recorded in the last quarter alone. The rapid shift is most evident among large organizations 62% of Fortune 500 companies had adopted containerized microservices by 2024, up from 47% in 2022. The U.S. is at the forefront of serverless microservices as well, with over 1,100 enterprises deploying serverless functions that execute more than 9 billion function invocations each month. These patterns reduced average deployment times by 47%, dropping from 7.3 minutes to 3.9 minutes per release, demonstrating the scalability and operational efficiency that microservices architectures bring to American enterprises.

Innovation remains central to U.S. cloud microservices market growth. In 2025, Amazon Web Services launched Aurora DSQL, a serverless distributed SQL database specifically optimized for microservices and event-driven architectures, while Google Cloud introduced NVIDIA GPU support for Cloud Run, enabling powerful AI workloads in serverless container environments. Microsoft Azure retained its leadership in serverless platforms, as recognized in Forrester’s 2025 Wave report. Leading U.S. companies such as Nutanix and DNAnexus have rolled out AI/ML microservices optimized for public clouds, with strong enterprise adoption across healthcare and genomics. To address the complexity of distributed cloud-native systems, major U.S. firms like VMware, F5, and Mirantis launched advanced observability and security solutions for microservices in multi-cloud environments, further solidifying the U.S. position as the global benchmark for cloud microservices innovation and best practices.

China: Digital Sovereignty, Domestic Cloud Innovation, and Microservices Expansion

China’s cloud microservices market has experienced explosive growth, underpinned by comprehensive digital transformation policies and a strong push toward technological sovereignty. Chinese cloud giants, notably Alibaba Cloud, launched the Microservices Engine (MSE), an open-source, fully managed platform that integrates configuration management, cloud-native gateways, and microservices governance. These innovations support a rapidly maturing open-source ecosystem and are widely adopted by both private and public sectors. The Chinese government has prioritized the migration of public services to government clouds as a national strategic objective, leveraging microservices architectures to improve inter-agency collaboration and citizen engagement across multiple government layers. Tencent Cloud is also a major innovator, with its microservices-based offerings for AI, machine learning, and gaming, providing resilient and scalable infrastructure for China’s booming digital economy.

Another critical growth driver in China’s cloud microservices market is the country’s concerted effort to achieve digital self-sufficiency and data sovereignty. Domestic cloud service providers have rapidly closed the technological gap with international players by heavily investing in developing microservices frameworks that cater to the specific regulatory, security, and scalability requirements of Chinese enterprises. As a result, China has seen a rise in homegrown cloud-native platforms optimized for the local market, ensuring compliance and fostering rapid digital transformation across industries. These advancements have positioned China not only as a major consumer but also as an exporter of cloud-native microservices technology, increasingly targeting overseas expansion and supporting Chinese enterprises’ global ambitions.

India: Digital Public Infrastructure and Cloud Microservices Transformation

India’s cloud microservices market is advancing rapidly, driven by a string of government-led digital transformation programs under the "Digital India" initiative and related policies such as the National e-Governance Plan, Government Community Cloud (GCC), and GI Cloud (Meghraj). These initiatives have accelerated the adoption of modern cloud-native architectures, with microservices playing a crucial role in delivering modular, scalable, and resilient digital services for government and citizens alike. In 2025, Microsoft announced a $3 billion investment to expand Azure’s cloud and AI infrastructure in India, further strengthening the country’s foundation for deploying cloud microservices at scale. According to SalesEdge data, cloud computing accounted for ₹760,062 million 33.7% of total digital spending in FY24, reflecting robust financial commitment and broad-based adoption of cloud technologies that inherently support microservices.

India’s rapidly expanding data center industry is another catalyst, with capacity projected to grow by 678 MW over the next three years, placing India among the top global markets for digital infrastructure. The rise of open-source projects for cloud observability such as OpenTelemetry, Jaeger, and Prometheus demonstrates a growing maturity in managing complex microservices environments. The IndiaAI mission and increased focus on AI-first control planes are also driving the proliferation of cloud-native AI workloads that rely on microservices for flexibility and scale. As Indian enterprises and public sector bodies accelerate digital transformation, microservices architectures are enabling them to innovate, manage workloads efficiently, and offer seamless, modern experiences to users across the country.

Germany: Hybrid Cloud, Industry Digitization, and Microservices Leadership

Germany is a leader in Europe’s cloud microservices market, leveraging a strong industrial base and commitment to digital transformation. In 2024, 80% of public cloud decision-makers in German government organizations reported using hybrid cloud strategies, and 71% were leveraging multiple public clouds, underscoring a sophisticated approach to cloud architecture that favors flexible, microservices-friendly models. German enterprises such as SAP SE are transforming flagship offerings like S/4HANA Cloud into microservices-based platforms, enabling greater agility, scalability, and modularity in enterprise software. The rise of microservices in Germany is further supported by the country’s focus on data privacy, compliance, and interoperability key factors driving adoption in both the public and private sectors.

Siemens AG, another German giant, has accelerated investment in digitalization and IoT solutions, with its MindSphere platform and other industrial cloud applications extensively using microservices to enable real-time analytics, modular updates, and industrial automation at scale. These platforms allow manufacturers and utilities to modernize legacy systems, integrate with cutting-edge technologies, and maintain operational continuity in complex environments. Germany’s mature approach to hybrid and multi-cloud, coupled with sustained investment from global and domestic software leaders, ensures its ongoing leadership in the European cloud microservices landscape, particularly for high-value industrial and enterprise use cases.

United Kingdom: Rapid Market Growth, DevOps Maturity, and Public Sector Digitalization

The United Kingdom is witnessing robust expansion in the cloud microservices market, with industry reports forecasting a significant CAGR through 2033. This growth is fueled by the UK’s advanced DevOps and cloud-native ecosystem, where organizations are integrating agile development and continuous delivery practices to accelerate the adoption of microservices architectures. British enterprises across industries are investing in cloud-native tools and platforms to optimize application performance, scalability, and resilience key competitive differentiators in an increasingly digital economy. Cloud microservices are also enabling UK companies to deliver faster innovation, seamless updates, and enhanced customer experiences across both web and mobile channels.

Government-led digitalization is another powerful driver, as the UK government continues to modernize public services using cloud-native and microservices-based models to replace legacy systems. Announcements from the UK Government Digital Service highlight ongoing investments in scalable, secure digital platforms, underpinned by microservices for improved reliability and flexibility. As adoption grows, UK organizations are prioritizing cloud security solutions tailored to microservices environments, addressing distributed vulnerabilities and stringent regulatory requirements. This dual focus on technological maturity and digital public service delivery positions the UK as a key leader in the European cloud microservices market.

Canada: BFSI Innovation and Government Cloud Modernization

Canada’s cloud microservices market is gaining momentum, particularly in the banking, financial services, and insurance (BFSI) sector. Canadian banks and insurers are adopting cloud-native, microservices-based architectures to boost agility, accelerate product deployment, and deliver seamless digital customer experiences. The modular nature of microservices allows BFSI organizations to update applications rapidly, introduce new financial products, and maintain high availability all while meeting strict compliance standards. The growing demand for scalable and flexible IT solutions is also extending microservices adoption to telecommunications, healthcare, and other sectors seeking to modernize legacy systems.

Public sector modernization further amplifies market growth. Canadian government agencies are adopting "cloud-first" strategies, leveraging microservices to improve the efficiency and responsiveness of government services. Cloud-native applications and microservices are facilitating the digital transformation of critical public infrastructure, from health care platforms to citizen service portals. As Canadian organizations continue their digital journeys, the adoption of microservices is expected to accelerate, supporting national goals for efficiency, security, and innovation across both private and public sectors.

Australia: Enterprise Digital Transformation and Edge Computing Growth

Australia’s cloud microservices market is experiencing strong growth as enterprises invest in digital transformation to remain competitive in the global economy. Local IT consultancies such as Attained Group are specializing in cloud management and microservices, meeting the rising demand for agile, scalable, and resilient software solutions among Australian businesses. The adoption of microservices is enabling organizations to develop modular applications that can adapt quickly to changing market dynamics and regulatory requirements. As Australian companies embrace the benefits of microservices, they are also focusing on integrating advanced cloud management, DevOps practices, and automation for optimal operational efficiency.

Edge computing and IoT represent emerging growth drivers for microservices adoption in Australia. Enterprises are leveraging distributed, microservices-based platforms to support real-time analytics, device management, and secure data processing at the network edge. This trend is particularly pronounced in industries such as utilities, mining, and logistics, where low-latency performance and scalability are critical. As digital infrastructure matures and businesses demand more agile IT solutions, microservices will continue to underpin Australia’s enterprise and industrial cloud transformation strategies.

Brazil: Cloud Microservices Adoption in BFSI, E-commerce, and Infrastructure

Brazil is a regional powerhouse for cloud microservices adoption, propelled by strong economic growth and accelerated digital transformation in banking, financial services, and insurance (BFSI), as well as e-commerce. Brazilian banks and fintechs are leveraging microservices architectures to enable agile product launches, scale digital offerings, and handle high transaction volumes efficiently. The modular nature of microservices is also enabling leading e-commerce platforms in Brazil to support rapid user growth, ensure site reliability, and deliver personalized shopping experiences at scale. With Brazil being the largest cloud market in Latin America, increased investments in digital infrastructure such as new data centers and cloud platform expansion are laying the groundwork for robust microservices deployments.

The Brazilian public sector and enterprise organizations are also embracing microservices as part of larger digital modernization programs, improving the scalability, security, and cost-effectiveness of critical applications. With growing interest in hybrid and multi-cloud strategies, Brazilian companies are positioned to capitalize on the operational flexibility and competitive advantages that microservices offer. As cloud adoption continues to surge across Brazil’s BFSI, retail, healthcare, and government sectors, microservices architectures are expected to underpin much of the country’s digital innovation and modernization efforts in the years ahead.

Cloud Microservices Market Report Scope

Cloud Microservices Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.1 Billion

|

|

Market Size (2034)

|

$17.1 Billion

|

|

Market Growth Rate

|

26.2%

|

|

Segments

|

By Component (Solution, Services), By Deployment Model, Public Cloud, Hybrid Cloud, Private Cloud), By Enterprise Size (Large Enterprises, Small and Medium-Sized Enterprises (SMEs)), By End-User Industry (IT and Telecommunication, BFSI (Banking, Financial Services, and Insurance), Healthcare, Retail and E-commerce, Government, Media and Entertainment, Transportation and Logistics, Manufacturing, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amazon Web Services (AWS), Microsoft Azure, Google Cloud, IBM, Oracle Corporation, Salesforce.com Inc., Alibaba Cloud, Tencent Cloud, DigitalOcean, Tata Consultancy Services Limited, Broadcom Inc. (CA Technologies), VMware Inc. (Pivotal Software Inc.), Infosys Ltd., NGINX Inc., Syntel Inc., Idexcel Inc., RapidValue IT Services Private Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Cloud Microservices Market Segmentation

By Component

By Deployment Model

- Public Cloud

- Hybrid Cloud

- Private Cloud

By Enterprise Size

- Large Enterprises

- Small and Medium-Sized Enterprises (SMEs)

By End-User Industry

- IT and Telecommunication

- BFSI (Banking, Financial Services, and Insurance)

- Healthcare

- Retail and E-commerce

- Government

- Media and Entertainment

- Transportation and Logistics

- Manufacturing

- Other End-user Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Cloud Microservices Market

- Amazon Web Services (AWS)

- Microsoft Azure

- Google Cloud

- IBM

- Oracle Corporation

- Salesforce.com Inc.

- Alibaba Cloud

- Tencent Cloud

- DigitalOcean

- Tata Consultancy Services Limited

- Broadcom Inc. (CA Technologies)

- VMware Inc. (Pivotal Software Inc.)

- Infosys Ltd.

- NGINX Inc.

- Syntel Inc.

- Idexcel Inc.

- RapidValue IT Services Private Limited

* List Not Exhaustive

Research Coverage

This comprehensive Cloud Microservices Market report from USDAnalytics provides in-depth market sizing, CAGR, and value projections, placing recent developments such as serverless distributed SQL, AI/ML integration, and real-time cloud edge innovations at the center of industry growth. The study examines evolving market dynamics, deployment models, key technology trends, leading cloud platforms, and critical industry drivers and challenges, all structured for industry professionals.

Segmentation includes component (solution, services), deployment model (public, hybrid, private cloud), enterprise size (large, SMEs), and end-user industries (IT & telecom, BFSI, healthcare, retail, government, and others). The report profiles top companies such as AWS, Microsoft Azure, Google Cloud, IBM, Oracle, Salesforce, Alibaba Cloud, Tencent Cloud, DigitalOcean, and TCS, highlighting their strategic offerings and recent advancements.

Geographic coverage spans North America, Europe, Asia Pacific, South America, and Middle East & Africa, with detailed analysis of historic (2021–2024) and forecast (2025–2034) data. The study delivers actionable insights for decision-makers and cloud architects, emphasizing recent innovations, digital transformation drivers, regional adoption trends, and competitive landscape in the rapidly expanding cloud microservices market.

Deliverables:

- Full Market Research Report (PDF, Excel): Complete data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis.

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis.

- Recent Developments & News Tracker

- Executive Summary & Analyst Insights.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.