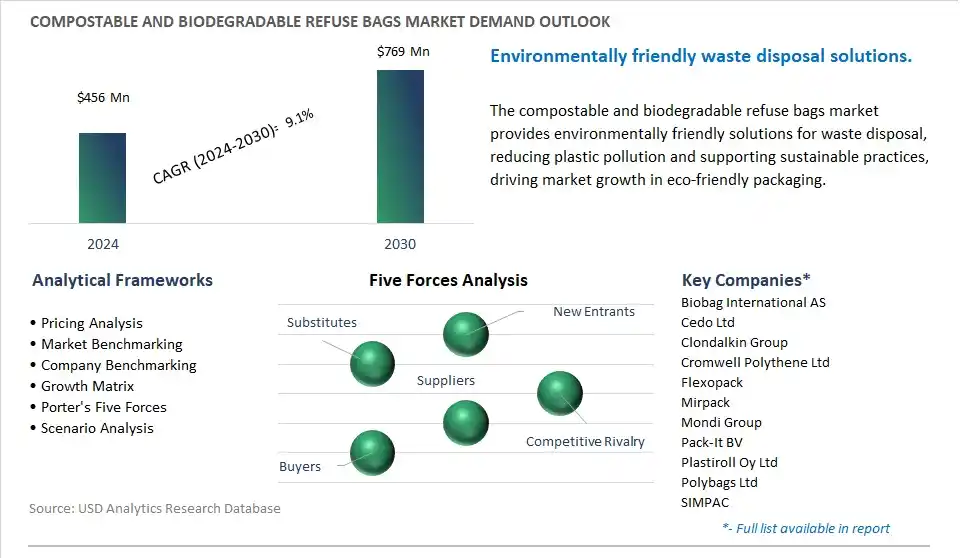

The global Compostable and Biodegradable Refuse Bags Market is poised to register a 9.1% CAGR from $456 Million in 2024 to $769 Million in 2030.

The global Compostable and Biodegradable Refuse Bags Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Capacity (7 to 20 Gallons, 20 to 30 Gallons, 30 to 40 Gallons, 40 to 55 Gallons, Above 55 Gallons), By Product (Biodegradable, Compostable), By Material (Polylactic Acid (PLA), Polyhydroxyalkanoate (PHA), PBS, PBAT, Starch Blends, Cellophane, Paper), By Thickness (0 to 0.7 Mil, 7 to 0.9 Mil, 0.9 to 1.5 Mil, Above 1.5 Mil), By End-User (Retail and Consumer, Industrial, Institutional).

An Introduction to Global Compostable and Biodegradable Refuse Bags Market in 2024

The market for compostable and biodegradable refuse bags is addressing environmental concerns in waste management by offering sustainable alternatives to traditional plastic bags for household, commercial, and municipal waste collection. Compostable and biodegradable refuse bags are made from renewable materials such as plant-based polymers or biodegradable plastics, which break down into natural compounds under composting or microbial degradation conditions. Key trends include advancements in material formulations, processing technologies, and certification standards to ensure product performance, biodegradability, and compatibility with composting facilities and anaerobic digestion systems. Additionally, developments in bag design, closure mechanisms, and barrier properties enhance functionality and user experience while minimizing environmental impact. Moreover, the integration of circular economy principles, such as closed-loop recycling and organic waste diversion, promotes resource efficiency and waste reduction throughout the product lifecycle. As governments, businesses, and consumers increasingly prioritize sustainable waste management solutions, the demand for compostable and biodegradable refuse bags is expected to grow, driving further innovation and market adoption in this critical sector of environmentally friendly packaging.

Compostable and Biodegradable Refuse Bags Market Competitive Landscape

The market report analyses the leading companies in the industry including Biobag International AS, Cedo Ltd, Clondalkin Group, Cromwell Polythene Ltd, Flexopack, Mirpack, Mondi Group, Pack-It BV, Plastiroll Oy Ltd, Polybags Ltd, SIMPAC, TERDEX GmbH, The Biodegradable Bag Company Ltd, The Compost Bag Company NV/SA, Vegware Ltd, VICTOR Güthoff & Partner GmbH, Virosac Srl.

Compostable and Biodegradable Refuse Bags Market Dynamics

Compostable and Biodegradable Refuse Bags Market Trend: Growing Consumer Preference for Sustainable Packaging Solutions

A prominent trend in the market for compostable and biodegradable refuse bags is the growing consumer preference for sustainable packaging solutions. With increasing environmental awareness and concerns over plastic pollution, consumers are seeking eco-friendly alternatives to traditional plastic bags for waste disposal. Compostable and biodegradable refuse bags, made from renewable resources such as plant-based materials or biodegradable polymers, are gaining popularity as they offer a more environmentally responsible option for managing household waste. This is driven by shifting consumer attitudes towards sustainability, eco-conscious purchasing behavior, and regulatory initiatives promoting the use of biodegradable packaging materials, leading to a higher demand for compostable and biodegradable refuse bags in the retail and consumer markets.

Compostable and Biodegradable Refuse Bags Market Driver: Regulatory Push Towards Plastic Waste Reduction

A significant driver fueling the demand for compostable and biodegradable refuse bags is the regulatory push towards plastic waste reduction. Governments and regulatory bodies worldwide are implementing policies, bans, and regulations aimed at curbing single-use plastic consumption and promoting the use of biodegradable and compostable alternatives. Measures such as plastic bag bans, extended producer responsibility (EPR) schemes, and waste management regulations incentivize the adoption of compostable and biodegradable refuse bags as sustainable alternatives to conventional plastic bags. This driver is further supported by corporate sustainability initiatives, voluntary commitments by retailers and manufacturers to reduce plastic waste, and growing public awareness of the environmental impacts of plastic pollution, driving the adoption of compostable and biodegradable refuse bags as part of efforts to address plastic waste and promote circular economy principles.

Compostable and Biodegradable Refuse Bags Market Opportunity: Expansion into Commercial and Industrial Waste Management

An opportunity within the market for compostable and biodegradable refuse bags lies in expansion into commercial and industrial waste management sectors. While consumer demand for sustainable packaging solutions drives the retail market for refuse bags, there is potential for growth in commercial and industrial applications such as restaurants, hotels, hospitals, and office buildings. These sectors generate large volumes of waste that require effective and environmentally responsible disposal solutions. By targeting commercial and industrial customers with tailored product offerings, bulk packaging options, and value-added services such as waste management consulting and sustainability certification, manufacturers of compostable and biodegradable refuse bags can tap into a lucrative market segment and capitalize on the growing demand for sustainable waste management solutions. Additionally, partnerships with waste management companies, facility managers, and corporate sustainability programs present opportunities to expand market reach and increase adoption of compostable and biodegradable refuse bags in commercial and industrial waste streams.

Compostable and Biodegradable Refuse Bags Market Ecosystem

The Market Ecosystem for compostable and biodegradable refuse bags begins with raw material acquisition, where biopolymer suppliers including NatureWorks LLC and BASF provide bio-based polymers including PLA and PHA. Optional suppliers offer materials including cellulose or paper for specific biodegradable bags. Bag manufacturing involves companies including BioBag International and BPI Group, which convert biopolymers into film and fabricate bags to meet design specifications.

Sustainable packaging distributors connect manufacturers with retailers and waste management companies, while retailers including supermarkets and online stores cater to environmentally conscious consumers. Optional stages include composting facilities for certified compostable bags and biodegradation processes depending on the material used.

Compostable and Biodegradable Refuse Bags Market Share Analysis: 7 to 20 Gallons held the dominant revenue share in 2024

The largest segment in the Compostable and Biodegradable Refuse Bags Market is the "7 to 20 Gallons" segment. This dominance is driven by smaller capacity refuse bags in the 7 to 20 gallons range are commonly used in households, offices, and small businesses for everyday waste disposal needs. These bags are suitable for collecting kitchen waste, paper, plastics, and other recyclables, making them essential items in waste management and recycling programs. Additionally, the compact size of 7 to 20-gallon refuse bags makes them convenient for storage, handling, and transportation, particularly in urban environments with limited space. In addition, there is a growing trend toward sustainability and eco-conscious consumer behavior, leading to increased demand for compostable and biodegradable refuse bags as alternatives to traditional plastic bags. Smaller capacity refuse bags are often preferred by environmentally conscious consumers due to their reduced environmental impact and compatibility with home composting systems. Further, regulatory initiatives and bans on single-use plastics in many regions worldwide further drive the adoption of compostable and biodegradable refuse bags in smaller sizes. As a result, the "7 to 20 Gallons" segment is the largest segment in the Compostable and Biodegradable Refuse Bags Market, driven by widespread usage, convenience, sustainability considerations, and regulatory trends favoring smaller capacity bags.

Compostable and Biodegradable Refuse Bags Market Share Analysis: Compostable is the fastest growing market segment over the forecast period to 2030

The fastest-growing segment in the Compostable and Biodegradable Refuse Bags Market is the "Compostable" segment. This trend is driven by there is a growing awareness and concern about plastic pollution and its environmental impact, leading to increased demand for sustainable alternatives to traditional plastic bags. Compostable refuse bags offer a viable solution to this problem, as they are made from renewable and biodegradable materials such as plant-based polymers (e.g., PLA) or bio-based plastics derived from agricultural waste or by-products. These materials break down into natural components such as water, carbon dioxide, and organic matter when subjected to composting processes, minimizing environmental harm and reducing reliance on fossil fuels. Additionally, compostable refuse bags are suitable for use in organic waste collection programs and home composting systems, where they can be disposed of along with food scraps, yard waste, and other compostable materials. Further, regulatory initiatives and consumer preferences favoring sustainable packaging solutions drive the adoption of compostable refuse bags by retailers, municipalities, and consumers. In addition, advancements in compostable packaging technologies and manufacturing processes have led to improvements in product performance, durability, and cost-effectiveness, making compostable refuse bags more competitive with traditional plastic bags in terms of functionality and affordability. As a result, the "Compostable" segment is the fastest-growing segment in the Compostable and Biodegradable Refuse Bags Market, propelled by sustainability concerns, regulatory drivers, and technological advancements in compostable packaging solutions.

Compostable and Biodegradable Refuse Bags Market Share Analysis: Polylactic Acid (PLA) is the fastest growing market segment over the forecast period to 2030

The fastest-growing segment in the Compostable and Biodegradable Refuse Bags Market is the "Polylactic Acid (PLA)" segment. This trend is driven by PLA is one of the most widely used biodegradable polymers derived from renewable resources such as corn starch or sugarcane. As consumers and businesses increasingly prioritize sustainability and environmental responsibility, there is a growing demand for packaging materials that offer a viable alternative to traditional plastics derived from fossil fuels. PLA stands out as an attractive option due to its biodegradability, compostability, and relatively low environmental impact compared to conventional plastics. Additionally, PLA exhibits good mechanical properties, including strength, flexibility, and clarity, making it suitable for a wide range of packaging applications, including refuse bags. Further, advancements in PLA production technology and manufacturing processes have led to improvements in material performance, cost-effectiveness, and scalability, driving increased adoption and market growth. In addition, regulatory initiatives and consumer preferences favoring biodegradable and compostable packaging solutions further accelerate the demand for PLA-based refuse bags. As a result, the "Polylactic Acid (PLA)" segment is the fastest-growing segment in the Compostable and Biodegradable Refuse Bags Market, propelled by sustainability concerns, regulatory drivers, technological advancements, and the versatility of PLA as a biopolymer.

Compostable and Biodegradable Refuse Bags Market Report Scope-

By Capacity

7 to 20 Gallons

20 to 30 Gallons

30 to 40 Gallons

40 to 55 Gallons

Above 55 Gallons

By Product

Biodegradable

Compostable

By Material

Polylactic Acid (PLA)

Polyhydroxyalkanoate (PHA)

PBS

PBAT

Starch Blends

Cellophane

Paper

By Thickness

0 to 0.7 Mil

7 to 0.9 Mil

0.9 to 1.5 Mil

Above 1.5 Mil

By End-User

Retail and Consumer

Industrial

Institutional

Compostable and Biodegradable Refuse Bags Market Companies Profiled

Biobag International AS

Cedo Ltd

Clondalkin Group

Cromwell Polythene Ltd

Flexopack

Mirpack

Mondi Group

Pack-It BV

Plastiroll Oy Ltd

Polybags Ltd

SIMPAC

TERDEX GmbH

The Biodegradable Bag Company Ltd

The Compost Bag Company NV/SA

Vegware Ltd

VICTOR Güthoff & Partner GmbH

Virosac Srl

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Compostable and Biodegradable Refuse Bags Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Compostable and Biodegradable Refuse Bags Market Size Outlook, $ Million, 2021 to 2030

3.2 Compostable and Biodegradable Refuse Bags Market Outlook by Type, $ Million, 2021 to 2030

3.3 Compostable and Biodegradable Refuse Bags Market Outlook by Product, $ Million, 2021 to 2030

3.4 Compostable and Biodegradable Refuse Bags Market Outlook by Application, $ Million, 2021 to 2030

3.5 Compostable and Biodegradable Refuse Bags Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Compostable and Biodegradable Refuse Bags Industry

4.2 Key Market Trends in Compostable and Biodegradable Refuse Bags Industry

4.3 Potential Opportunities in Compostable and Biodegradable Refuse Bags Industry

4.4 Key Challenges in Compostable and Biodegradable Refuse Bags Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Compostable and Biodegradable Refuse Bags Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Compostable and Biodegradable Refuse Bags Market Outlook by Segments

7.1 Compostable and Biodegradable Refuse Bags Market Outlook by Segments, $ Million, 2021- 2030

By Capacity

7 to 20 Gallons

20 to 30 Gallons

30 to 40 Gallons

40 to 55 Gallons

Above 55 Gallons

By Product

Biodegradable

Compostable

By Material

Polylactic Acid (PLA)

Polyhydroxyalkanoate (PHA)

PBS

PBAT

Starch Blends

Cellophane

Paper

By Thickness

0 to 0.7 Mil

7 to 0.9 Mil

0.9 to 1.5 Mil

Above 1.5 Mil

By End-User

Retail and Consumer

Industrial

Institutional

8 North America Compostable and Biodegradable Refuse Bags Market Analysis and Outlook To 2030

8.1 Introduction to North America Compostable and Biodegradable Refuse Bags Markets in 2024

8.2 North America Compostable and Biodegradable Refuse Bags Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Compostable and Biodegradable Refuse Bags Market size Outlook by Segments, 2021-2030

By Capacity

7 to 20 Gallons

20 to 30 Gallons

30 to 40 Gallons

40 to 55 Gallons

Above 55 Gallons

By Product

Biodegradable

Compostable

By Material

Polylactic Acid (PLA)

Polyhydroxyalkanoate (PHA)

PBS

PBAT

Starch Blends

Cellophane

Paper

By Thickness

0 to 0.7 Mil

7 to 0.9 Mil

0.9 to 1.5 Mil

Above 1.5 Mil

By End-User

Retail and Consumer

Industrial

Institutional

9 Europe Compostable and Biodegradable Refuse Bags Market Analysis and Outlook To 2030

9.1 Introduction to Europe Compostable and Biodegradable Refuse Bags Markets in 2024

9.2 Europe Compostable and Biodegradable Refuse Bags Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Compostable and Biodegradable Refuse Bags Market Size Outlook by Segments, 2021-2030

By Capacity

7 to 20 Gallons

20 to 30 Gallons

30 to 40 Gallons

40 to 55 Gallons

Above 55 Gallons

By Product

Biodegradable

Compostable

By Material

Polylactic Acid (PLA)

Polyhydroxyalkanoate (PHA)

PBS

PBAT

Starch Blends

Cellophane

Paper

By Thickness

0 to 0.7 Mil

7 to 0.9 Mil

0.9 to 1.5 Mil

Above 1.5 Mil

By End-User

Retail and Consumer

Industrial

Institutional

10 Asia Pacific Compostable and Biodegradable Refuse Bags Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Compostable and Biodegradable Refuse Bags Markets in 2024

10.2 Asia Pacific Compostable and Biodegradable Refuse Bags Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Compostable and Biodegradable Refuse Bags Market size Outlook by Segments, 2021-2030

By Capacity

7 to 20 Gallons

20 to 30 Gallons

30 to 40 Gallons

40 to 55 Gallons

Above 55 Gallons

By Product

Biodegradable

Compostable

By Material

Polylactic Acid (PLA)

Polyhydroxyalkanoate (PHA)

PBS

PBAT

Starch Blends

Cellophane

Paper

By Thickness

0 to 0.7 Mil

7 to 0.9 Mil

0.9 to 1.5 Mil

Above 1.5 Mil

By End-User

Retail and Consumer

Industrial

Institutional

11 South America Compostable and Biodegradable Refuse Bags Market Analysis and Outlook To 2030

11.1 Introduction to South America Compostable and Biodegradable Refuse Bags Markets in 2024

11.2 South America Compostable and Biodegradable Refuse Bags Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Compostable and Biodegradable Refuse Bags Market size Outlook by Segments, 2021-2030

By Capacity

7 to 20 Gallons

20 to 30 Gallons

30 to 40 Gallons

40 to 55 Gallons

Above 55 Gallons

By Product

Biodegradable

Compostable

By Material

Polylactic Acid (PLA)

Polyhydroxyalkanoate (PHA)

PBS

PBAT

Starch Blends

Cellophane

Paper

By Thickness

0 to 0.7 Mil

7 to 0.9 Mil

0.9 to 1.5 Mil

Above 1.5 Mil

By End-User

Retail and Consumer

Industrial

Institutional

12 Middle East and Africa Compostable and Biodegradable Refuse Bags Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Compostable and Biodegradable Refuse Bags Markets in 2024

12.2 Middle East and Africa Compostable and Biodegradable Refuse Bags Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Compostable and Biodegradable Refuse Bags Market size Outlook by Segments, 2021-2030

By Capacity

7 to 20 Gallons

20 to 30 Gallons

30 to 40 Gallons

40 to 55 Gallons

Above 55 Gallons

By Product

Biodegradable

Compostable

By Material

Polylactic Acid (PLA)

Polyhydroxyalkanoate (PHA)

PBS

PBAT

Starch Blends

Cellophane

Paper

By Thickness

0 to 0.7 Mil

7 to 0.9 Mil

0.9 to 1.5 Mil

Above 1.5 Mil

By End-User

Retail and Consumer

Industrial

Institutional

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Biobag International AS

Cedo Ltd

Clondalkin Group

Cromwell Polythene Ltd

Flexopack

Mirpack

Mondi Group

Pack-It BV

Plastiroll Oy Ltd

Polybags Ltd

SIMPAC

TERDEX GmbH

The Biodegradable Bag Company Ltd

The Compost Bag Company NV/SA

Vegware Ltd

VICTOR Güthoff & Partner GmbH

Virosac Srl

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Capacity

7 to 20 Gallons

20 to 30 Gallons

30 to 40 Gallons

40 to 55 Gallons

Above 55 Gallons

By Product

Biodegradable

Compostable

By Material

Polylactic Acid (PLA)

Polyhydroxyalkanoate (PHA)

PBS

PBAT

Starch Blends

Cellophane

Paper

By Thickness

0 to 0.7 Mil

7 to 0.9 Mil

0.9 to 1.5 Mil

Above 1.5 Mil

By End-User

Retail and Consumer

Industrial

Institutional

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)