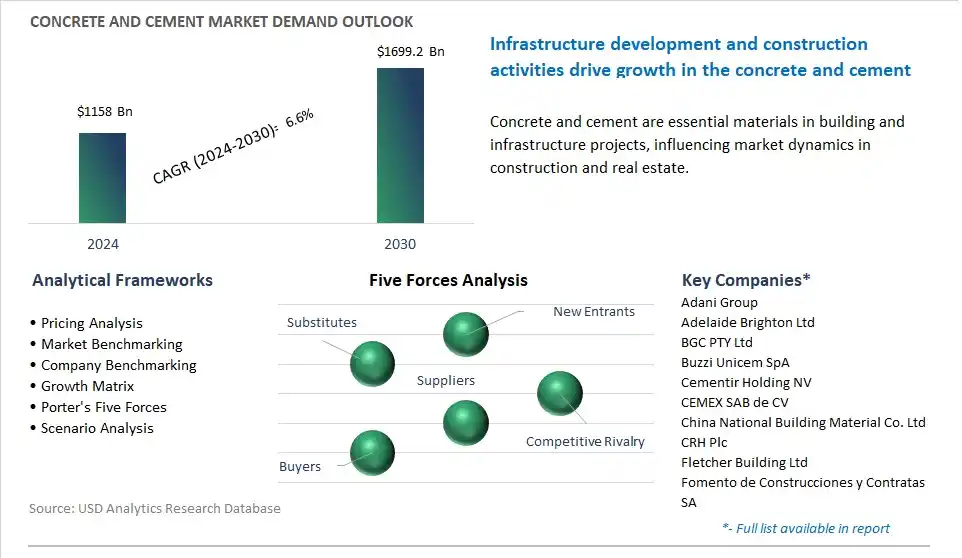

The global Concrete and Cement Market is poised to register a 6.6% CAGR from $1158 Billion in 2024 to $1699.2 Billion in 2030.

The global Concrete and Cement Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Product (Rapid Hardening Cement, Low Heat Cement, White Cement, Hydrophobic Cement, Others), By End-User (Transport, Residential, Commercial).

An Introduction to Global Concrete and Cement Market in 2024

The concrete and cement market is witnessing growth driven by infrastructure development, urbanization, and construction activities worldwide. Key trends shaping the future of the industry include innovations in cement production processes, sustainable concrete formulations, and advanced construction techniques to meet growing demand while reducing environmental impact. Advanced concrete and cement solutions offer properties such as high strength, durability, and sustainability, making them suitable for a wide range of applications in residential, commercial, and infrastructure projects. Moreover, the integration of supplementary cementitious materials (SCMs), such as fly ash, slag, and silica fume, enhances concrete performance, reduces carbon footprint, and promotes circular economy principles by utilizing industrial by-products. Additionally, the growing emphasis on green building certifications, energy efficiency, and resilient infrastructure drives market demand for eco-friendly concrete and cement solutions that contribute to sustainable development goals. As governments, developers, and construction companies invest in modernizing infrastructure, improving building performance, and addressing climate change challenges, the concrete and cement market is poised for continued growth and innovation as a fundamental component of global construction and infrastructure development.

Concrete and Cement Market Competitive Landscape

The market report analyses the leading companies in the industry including Adani Group, Adelaide Brighton Ltd, BGC PTY Ltd, Buzzi Unicem SpA, Cementir Holding NV, CEMEX SAB de CV, China National Building Material Co. Ltd, CRH Plc, Fletcher Building Ltd, Fomento de Construcciones y Contratas SA, HeidelbergCement AG, Holcim Ltd, JK Cement Ltd, Mitsubishi Cement Corp, Nippon Steel Cement Co Ltd.

Concrete and Cement Market Dynamics

Concrete and Cement Market Trend: Emphasis on Sustainable Construction Practices

The most prominent trend in the concrete and cement market is the increasing emphasis on sustainable construction practices, driven by environmental regulations, climate change concerns, and corporate sustainability initiatives. Concrete and cement production are significant contributors to carbon emissions and environmental degradation due to the energy-intensive manufacturing process and the release of CO2 during cement production. As governments and industries prioritize sustainability goals, there's a growing adoption of alternative cementitious materials, such as fly ash, slag, and recycled aggregates, to reduce the carbon footprint of concrete construction. Additionally, innovations in concrete mix designs, such as high-performance concrete and self-healing concrete, aim to improve durability, reduce maintenance needs, and prolong the service life of structures, aligning with sustainable development objectives and driving market growth in eco-friendly concrete and cement products.

Concrete and Cement Market Driver: Infrastructure Development and Urbanization

A key driver in the concrete and cement market is infrastructure development and urbanization, fueled by rapid urban population growth, urbanization, and the need to upgrade and expand transportation, water, and energy infrastructure in emerging economies. Concrete is the most widely used construction material globally, offering durability, versatility, and cost-effectiveness for building roads, bridges, dams, and buildings. As cities expand and modernize, there's a corresponding increase in demand for concrete and cement products to support urban infrastructure projects, accommodate population growth, and improve quality of life. This driver motivates governments, developers, and construction companies to invest in large-scale infrastructure projects, driving demand for concrete and cement materials and driving market growth in the construction sector.

Concrete and Cement Market Opportunity: Adoption of Carbon Capture and Utilization (CCU) Technologies

The concrete and cement market presents a potential opportunity for the adoption of carbon capture and utilization (CCU) technologies to reduce greenhouse gas emissions from cement production and mitigate climate change. Cement manufacturing is a major source of CO2 emissions, accounting for approximately 8% of global CO2 emissions, primarily from the calcination process and the use of fossil fuels for energy. By implementing CCU technologies, such as carbon capture and storage (CCS) or carbon utilization in concrete production, cement manufacturers can capture CO2 emissions from cement plants and convert them into valuable products, such as aggregates, fillers, or mineralized carbonates, for use in concrete production. Additionally, incorporating supplementary cementitious materials with low carbon footprints, such as calcined clays or limestone, can further reduce the environmental impact of concrete and cement production. By embracing CCU technologies and sustainable manufacturing practices, cement companies can enhance their environmental credentials, comply with regulatory requirements, and create new revenue streams, driving growth and innovation in the concrete and cement market.

Concrete and Cement Market Share Analysis: Rapid Hardening Cement segment generated the highest revenue in the industry

Rapid Hardening Cement is the fastest-growing segment in the Concrete and Cement Market. Its accelerated setting and hardening properties make it highly desirable in construction projects where time is of the essence. This type of cement gains strength faster than ordinary Portland cement, enabling quicker project completion and reducing construction timelines significantly. Industries such as infrastructure, residential, and commercial construction, where rapid turnaround times are critical, are increasingly turning to rapid hardening cement to expedite their projects. Additionally, its versatility allows it to be used in various applications, including repair works and precast concrete manufacturing, further driving its demand. As urbanization accelerates and infrastructure projects multiply, the need for rapid hardening cement is expected to continue its upward trajectory, positioning it as a key player in the Concrete and Cement Market.

Concrete and Cement Market Share Analysis: Commercial Sector Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The commercial sector is the fastest-growing segment in the Concrete and Cement Market. This growth is propelled by the burgeoning demand for commercial spaces driven by rapid urbanization and economic development worldwide. With the expansion of industries, retail spaces, office complexes, and entertainment hubs, there's a continuous need for robust infrastructure, of which concrete and cement are foundational components. In addition, commercial projects often involve large-scale constructions that require substantial quantities of concrete, further fueling the demand. The commercial sector's resilience and adaptability to market dynamics, coupled with the increasing trend of sustainable construction practices, ensure a sustained growth trajectory for concrete and cement in this segment. As businesses continue to flourish and urban landscapes evolve, the commercial sector remains a pivotal driver of growth in the Concrete and Cement Market.

Concrete and Cement Market Report Segmentation

By Product

Rapid Hardening Cement

Low Heat Cement

White Cement

Hydrophobic Cement

Others

By End-User

Transport

Residential

Commercial

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Concrete and Cement Companies Profiled in the Market Study

Adani Group

Adelaide Brighton Ltd

BGC PTY Ltd

Buzzi Unicem SpA

Cementir Holding NV

CEMEX SAB de CV

China National Building Material Co. Ltd

CRH Plc

Fletcher Building Ltd

Fomento de Construcciones y Contratas SA

HeidelbergCement AG

Holcim Ltd

JK Cement Ltd

Mitsubishi Cement Corp

Nippon Steel Cement Co Ltd

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Concrete and Cement Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Concrete and Cement Market Size Outlook, $ Million, 2021 to 2030

3.2 Concrete and Cement Market Outlook by Type, $ Million, 2021 to 2030

3.3 Concrete and Cement Market Outlook by Product, $ Million, 2021 to 2030

3.4 Concrete and Cement Market Outlook by Application, $ Million, 2021 to 2030

3.5 Concrete and Cement Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Concrete and Cement Industry

4.2 Key Market Trends in Concrete and Cement Industry

4.3 Potential Opportunities in Concrete and Cement Industry

4.4 Key Challenges in Concrete and Cement Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Concrete and Cement Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Concrete and Cement Market Outlook by Segments

7.1 Concrete and Cement Market Outlook by Segments, $ Million, 2021- 2030

By Product

Rapid Hardening Cement

Low Heat Cement

White Cement

Hydrophobic Cement

Others

By End-User

Transport

Residential

Commercial

8 North America Concrete and Cement Market Analysis and Outlook To 2030

8.1 Introduction to North America Concrete and Cement Markets in 2024

8.2 North America Concrete and Cement Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Concrete and Cement Market size Outlook by Segments, 2021-2030

By Product

Rapid Hardening Cement

Low Heat Cement

White Cement

Hydrophobic Cement

Others

By End-User

Transport

Residential

Commercial

9 Europe Concrete and Cement Market Analysis and Outlook To 2030

9.1 Introduction to Europe Concrete and Cement Markets in 2024

9.2 Europe Concrete and Cement Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Concrete and Cement Market Size Outlook by Segments, 2021-2030

By Product

Rapid Hardening Cement

Low Heat Cement

White Cement

Hydrophobic Cement

Others

By End-User

Transport

Residential

Commercial

10 Asia Pacific Concrete and Cement Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Concrete and Cement Markets in 2024

10.2 Asia Pacific Concrete and Cement Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Concrete and Cement Market size Outlook by Segments, 2021-2030

By Product

Rapid Hardening Cement

Low Heat Cement

White Cement

Hydrophobic Cement

Others

By End-User

Transport

Residential

Commercial

11 South America Concrete and Cement Market Analysis and Outlook To 2030

11.1 Introduction to South America Concrete and Cement Markets in 2024

11.2 South America Concrete and Cement Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Concrete and Cement Market size Outlook by Segments, 2021-2030

By Product

Rapid Hardening Cement

Low Heat Cement

White Cement

Hydrophobic Cement

Others

By End-User

Transport

Residential

Commercial

12 Middle East and Africa Concrete and Cement Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Concrete and Cement Markets in 2024

12.2 Middle East and Africa Concrete and Cement Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Concrete and Cement Market size Outlook by Segments, 2021-2030

By Product

Rapid Hardening Cement

Low Heat Cement

White Cement

Hydrophobic Cement

Others

By End-User

Transport

Residential

Commercial

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Adani Group

Adelaide Brighton Ltd

BGC PTY Ltd

Buzzi Unicem SpA

Cementir Holding NV

CEMEX SAB de CV

China National Building Material Co. Ltd

CRH Plc

Fletcher Building Ltd

Fomento de Construcciones y Contratas SA

HeidelbergCement AG

Holcim Ltd

JK Cement Ltd

Mitsubishi Cement Corp

Nippon Steel Cement Co Ltd

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Product

Rapid Hardening Cement

Low Heat Cement

White Cement

Hydrophobic Cement

Others

By End-User

Transport

Residential

Commercial

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)