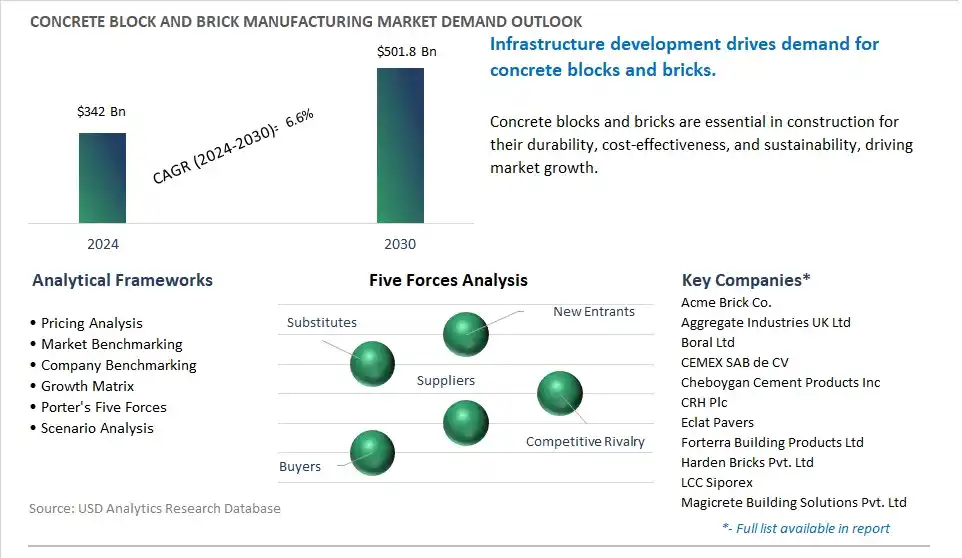

The global Concrete Block and Brick Manufacturing Market is poised to register a 6.6% CAGR from $342 Billion in 2024 to $501.8 Billion in 2030.

The global Concrete Block and Brick Manufacturing Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (Block, Brick), By End-User (Residential Sector, Non-Residential Sector), By Application (Structural, Non-Structural).

An Introduction to Global Concrete Block and Brick Manufacturing Market in 2024

The market for concrete block and brick manufacturing is experiencing growth, driven by increasing construction activities, urbanization, and infrastructure development worldwide. Key trends shaping the future of the industry include advancements in manufacturing processes, materials technology, and sustainable construction practices to meet the evolving needs of builders, architects, and contractors for durable, cost-effective, and environmentally friendly building materials. Manufacturers are focusing on developing concrete blocks and bricks with improved strength, thermal insulation, and aesthetic appeal while reducing carbon footprint and environmental impact throughout the production lifecycle. Additionally, there is a growing emphasis on innovative building techniques such as insulated concrete forms (ICFs), modular construction, and precast concrete elements, driving the adoption of concrete blocks and bricks in residential, commercial, and industrial construction projects. Moreover, advancements in automation, robotics, and digital manufacturing are driving innovation in concrete block and brick production, enabling higher productivity, quality control, and customization of products to meet specific project requirements and design specifications. Furthermore, collaborations between concrete manufacturers, research institutions, and construction industry stakeholders are shaping the development of sustainable building materials, standardized testing methods, and best practices that promote the use of concrete blocks and bricks in green building projects, urban renewal initiatives, and affordable housing programs worldwide. Overall, the future of concrete block and brick manufacturing lies in continuous innovation, collaboration, and sustainability initiatives to address emerging market needs, technological challenges, and environmental concerns while meeting the growing demand for durable and resilient building materials in a rapidly urbanizing world.

Concrete Block and Brick Manufacturing Market Competitive Landscape

The market report analyses the leading companies in the industry including Acme Brick Co., Aggregate Industries UK Ltd, Boral Ltd, CEMEX SAB de CV, Cheboygan Cement Products Inc, CRH Plc, Eclat Pavers, Forterra Building Products Ltd, Harden Bricks Pvt. Ltd, LCC Siporex, Magicrete Building Solutions Pvt. Ltd, Midwest Block & Brick, Mona Precast Anglesey Ltd, R.W. Sidley Inc, RCP Block & Brick Inc, Thomas Armstrong Concrete Blocks Ltd, UltraTech Cement Ltd, Wienerberger AG, William D. Lewis Aberdare Ltd, Xella International GmbH.

Concrete Block and Brick Manufacturing Market Dynamics

Concrete Block and Brick Manufacturing Market Trend: Adoption of Sustainable and Eco-Friendly Practices

In the Concrete Block and Brick Manufacturing market, a prominent trend is the adoption of sustainable and eco-friendly practices. With increasing awareness of environmental issues and regulations aimed at reducing carbon emissions, there's a growing emphasis on sustainable manufacturing processes and materials in the construction industry. This trend is driven by factors such as green building certifications, government incentives for sustainable construction, and consumer demand for environmentally responsible products. As manufacturers strive to minimize environmental impact and meet regulatory requirements, there's a rising market demand for concrete blocks and bricks made from recycled materials, optimized production techniques, and energy-efficient manufacturing processes, driving innovation and adoption in the concrete block and brick manufacturing market.

Concrete Block and Brick Manufacturing Market Driver: Growth in Construction and Infrastructure Development

A significant driver in the Concrete Block and Brick Manufacturing market is the growth in construction and infrastructure development. With rapid urbanization, population growth, and economic expansion, there's a robust demand for building materials to support residential, commercial, and infrastructure projects worldwide. This driver is fueled by factors such as government investments in infrastructure, urban renewal projects, and the need for affordable housing and public amenities. As construction activity continues to expand globally, there's a corresponding market demand for concrete blocks and bricks for use in various applications such as walls, pavements, and landscaping, driving growth and investment in the concrete block and brick manufacturing industry.

Concrete Block and Brick Manufacturing Market Opportunity: Integration of Advanced Manufacturing Technologies

A promising opportunity within the Concrete Block and Brick Manufacturing market lies in the integration of advanced manufacturing technologies. Opportunities exist in adopting technologies such as automation, robotics, and digitalization to improve production efficiency, product quality, and customization capabilities. Advanced manufacturing technologies enable manufacturers to optimize raw material usage, reduce waste, and enhance product consistency while meeting evolving market demands for customization and rapid delivery. By investing in the adoption of advanced manufacturing technologies, manufacturers can streamline operations, reduce costs, and gain a competitive edge in the concrete block and brick manufacturing industry while also meeting sustainability goals and addressing market trends.

Concrete Block and Brick Manufacturing Market Share Analysis: Block segment generated the highest revenue in 2024

The largest segment in the Concrete Block and Brick Manufacturing Market is the Block segment. This dominance is. concrete blocks are widely used in various construction applications due to their versatility, durability, and cost-effectiveness. Concrete blocks are primarily used in load-bearing walls, retaining walls, partition walls, foundations, and other structural elements in residential, commercial, industrial, and infrastructure projects. Additionally, concrete blocks offer excellent compressive strength, fire resistance, thermal insulation, and sound insulation properties, making them suitable for building durable and energy-efficient structures. Further, concrete blocks can be manufactured in different sizes, shapes, and configurations to meet specific design requirements and construction standards, providing architects, engineers, and builders with flexibility and customization options. Furthermore, concrete blocks are manufactured using readily available raw materials such as cement, aggregates, water, and admixtures, making them cost-effective compared to alternative building materials such as bricks. Additionally, advancements in concrete block manufacturing technology, such as automated production processes, improved mix designs, and quality control measures, have enhanced product consistency, uniformity, and strength, further reinforcing the dominance of the Block segment in the Concrete Block and Brick Manufacturing Market. Furthermore, the widespread adoption of concrete blocks in large-scale construction projects, such as residential housing developments, commercial buildings, roads, bridges, and infrastructure projects, drives the demand for concrete block manufacturing globally. Additionally, concrete blocks offer environmental benefits such as energy efficiency, recyclability, and low embodied carbon compared to alternative building materials, aligning with sustainability initiatives and green building standards in the construction industry. Therefore, the Block segment remains the largest in the Concrete Block and Brick Manufacturing Market due to its widespread use, durability, cost-effectiveness, versatility, technological advancements, and alignment with sustainability trends in the construction industry.

Concrete Block and Brick Manufacturing Market Share Analysis: Non-Residential Sector segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The fastest-growing segment in the Concrete Block and Brick Manufacturing Market is the Non-Residential Sector. The non-residential sector includes commercial, industrial, institutional, and infrastructure projects such as office buildings, retail complexes, warehouses, manufacturing facilities, schools, hospitals, airports, roads, bridges, and other public works projects. These projects require a significant volume of concrete blocks and bricks for various structural and non-structural applications, including walls, partitions, facades, landscaping, paving, and hardscaping. Additionally, the non-residential sector is characterized by large-scale construction projects with substantial demand for building materials, including concrete blocks and bricks. Further, economic growth, urbanization, population growth, and infrastructure development drive investment in non-residential construction projects, creating opportunities for concrete block and brick manufacturers to supply materials for these projects. Furthermore, advancements in construction technology, design trends, and building codes have increased the demand for specialized concrete blocks and bricks tailored to the requirements of non-residential applications. For example, high-strength concrete blocks, insulated concrete blocks, architectural concrete blocks, and permeable pavers are increasingly used in non-residential projects to meet performance, sustainability, and aesthetic criteria. Additionally, the non-residential sector is less cyclical and more resilient to economic downturns compared to the residential sector, providing stability and growth opportunities for concrete block and brick manufacturers. Furthermore, government infrastructure spending, public-private partnerships, and initiatives such as smart cities, green building programs, and sustainable development projects further drive demand for concrete blocks and bricks in the non-residential sector. Additionally, the emphasis on sustainable construction practices, energy efficiency, and environmental stewardship in non-residential projects creates opportunities for innovative concrete block and brick products that offer enhanced performance and contribute to green building certifications. Therefore, the Non-Residential Sector presents significant growth opportunities in the Concrete Block and Brick Manufacturing Market, driven by the demand for building materials in large-scale construction projects, infrastructure development, technological advancements, design trends, and sustainability initiatives in the non-residential construction sector.

Concrete Block and Brick Manufacturing Market Share Analysis: Non-Structural application segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The fastest-growing segment in the Concrete Block and Brick Manufacturing Market is the Non-Structural application segment. non-structural applications encompass a wide range of uses for concrete blocks and bricks beyond load-bearing or structural purposes. These applications include landscaping, paving, decorative elements, partitions, facades, cladding, retaining walls, sound barriers, and fire walls, among others. The versatility of concrete blocks and bricks allows them to be utilized in various non-structural applications, providing architects, builders, and designers with flexibility in design and functionality. Additionally, non-structural concrete blocks and bricks are often used for aesthetic purposes, enhancing the visual appeal and architectural character of buildings and outdoor spaces. For example, decorative concrete blocks with textured surfaces, patterns, colors, and finishes can create unique design features and focal points in residential, commercial, and public projects. Further, non-structural concrete blocks and bricks are commonly employed in landscaping and hardscaping projects to build garden walls, planter boxes, pathways, patios, and outdoor seating areas. These applications contribute to the growing demand for concrete blocks and bricks in the residential, commercial, and institutional sectors, particularly in urban and suburban environments where outdoor living spaces and green spaces are valued. Furthermore, advancements in concrete block and brick manufacturing technology have expanded the range of available products for non-structural applications, including lightweight blocks, interlocking blocks, permeable pavers, and eco-friendly blocks made from recycled materials. These innovative products address emerging trends such as sustainability, durability, and ease of installation, driving their adoption in landscaping and hardscaping projects. Additionally, the growing focus on sustainability and environmental stewardship in construction practices encourages the use of locally sourced and recyclable building materials, further boosting the demand for non-structural concrete blocks and bricks. Further, non-structural applications offer opportunities for customization, personalization, and differentiation in architectural design, allowing builders and developers to create distinctive and memorable spaces that meet the needs and preferences of end-users. Therefore, the Non-Structural application segment presents significant growth opportunities in the Concrete Block and Brick Manufacturing Market, driven by the versatility, aesthetics, functionality, innovation, and sustainability of concrete blocks and bricks in landscaping, hardscaping, and decorative applications.

Concrete Block and Brick Manufacturing Market Report Segmentation

By Type

Block

Brick

By End-User

Residential Sector

Non-Residential Sector

By Application

Structural

Non-Structural

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Concrete Block and Brick Manufacturing Companies Profiled in the Market Study

Acme Brick Co.

Aggregate Industries UK Ltd

Boral Ltd

CEMEX SAB de CV

Cheboygan Cement Products Inc

CRH Plc

Eclat Pavers

Forterra Building Products Ltd

Harden Bricks Pvt. Ltd

LCC Siporex

Magicrete Building Solutions Pvt. Ltd

Midwest Block & Brick

Mona Precast Anglesey Ltd

R.W. Sidley Inc

RCP Block & Brick Inc

Thomas Armstrong Concrete Blocks Ltd

UltraTech Cement Ltd

Wienerberger AG

William D. Lewis Aberdare Ltd

Xella International GmbH

*- List Not Exhaustive