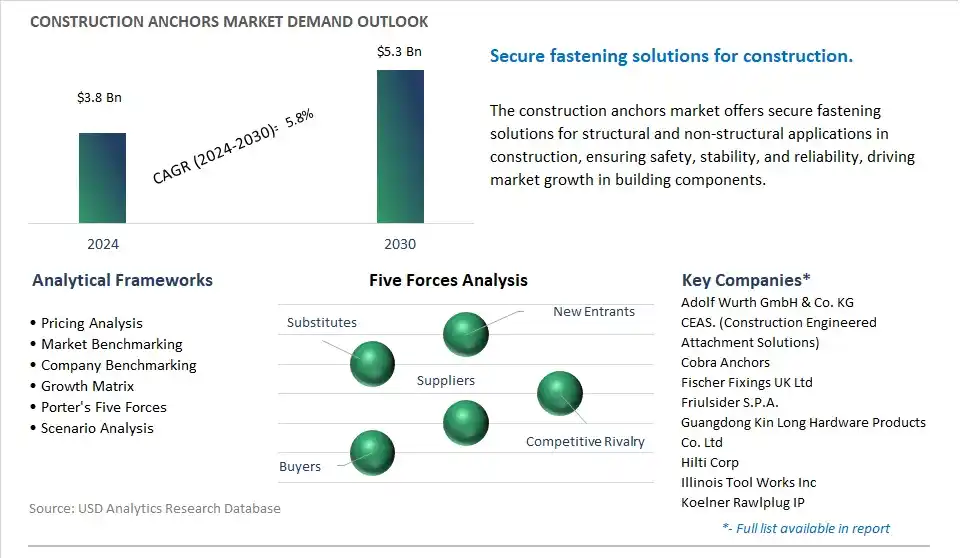

The global Construction Anchors Market is poised to register a 5.8% CAGR from $3.8 Billion in 2024 to $5.3 Billion in 2030.

The global Construction Anchors Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Product (Hangers, Mechanical), By Material (Stainless Steel, Carbon Steel, Others), By End-User (Residential, Commercial, Industrial, Infrastructural).

An Introduction to Global Construction Anchors Market in 2024

In the construction anchors market, the future is characterized by the demand for high-performance, code-compliant anchoring solutions that ensure structural integrity and safety in diverse construction applications. Anchors are essential for securing structural elements, equipment, and fixtures to concrete, masonry, steel, and other substrates, providing load transfer and resistance to forces such as wind, seismic activity, and gravity. Key trends shaping this industry include innovations in anchor design to enhance strength, reliability, and ease of installation, the development of corrosion-resistant materials for long-term durability, and the adoption of digital tools for precise design, simulation, and monitoring of anchor systems. As construction practices evolve to meet the challenges of urbanization, sustainability, and resilience, the demand for advanced anchoring solutions tailored to specific project requirements will continue to drive innovation and market growth.

Construction Anchors Market Competitive Landscape

The market report analyses the leading companies in the industry including Adolf Wurth GmbH & Co. KG, CEAS. (Construction Engineered Attachment Solutions), Cobra Anchors, Fischer Fixings UK Ltd, Friulsider S.P.A., Guangdong Kin Long Hardware Products Co. Ltd, Hilti Corp, Illinois Tool Works Inc, Koelner Rawlplug IP, Mechanical Plastics Corp, MKT Fastening LLC, SFS Group Fastening Technology Ltd, Sika AG, Stanley Black & Decker Inc- DEWALT.

Construction Anchors Market Dynamics

Construction Anchors Market Trend: Increasing Emphasis on Infrastructure Development

One prominent market trend in the construction anchors industry is the increasing emphasis on infrastructure development globally. With growing urbanization and population expansion, there is a rising demand for robust infrastructure to support economic growth and societal needs. The trend is driving significant investments in construction projects such as highways, bridges, airports, and commercial buildings, consequently boosting the demand for construction anchors. These anchors play a crucial role in securing structures and ensuring their stability, making them indispensable components in the construction industry's pursuit of durable and reliable infrastructure solutions.

Construction Anchors Market Driver: Stringent Building Regulations and Safety Standards

A key driver in the construction anchors market is the enforcement of stringent building regulations and safety standards worldwide. Governments and regulatory bodies are imposing strict requirements to enhance structural integrity, prevent accidents, and mitigate risks associated with building failures. Construction anchors are vital components in adhering to these regulations, as they provide the necessary reinforcement and stability to construction structures. As safety concerns continue to drive regulatory measures, the demand for high-quality, compliant construction anchors is expected to escalate, compelling manufacturers to innovate and offer solutions that meet or exceed industry standards.

Construction Anchors Market Opportunity: Expansion in Renewable Energy Infrastructure

One potential opportunity in the construction anchors market lies in the expansion of renewable energy infrastructure projects. With the global shift towards sustainable energy sources such as wind and solar power, there is a growing need for robust anchoring systems to support renewable energy installations. Wind turbines, solar panel arrays, and other renewable energy structures require secure anchoring solutions to withstand harsh environmental conditions and ensure long-term reliability. By providing specialized anchors tailored to the unique requirements of renewable energy projects, manufacturers can tap into this burgeoning market segment and contribute to the growth of sustainable energy initiatives worldwide.

Construction Anchors Market Ecosystem

In the Construction Anchors market, the Market Ecosystem begins with Raw Material Acquisition, where Steel Producers including ArcelorMittal supply various grades of steel required for anchor manufacturing. Optional Processing stages involve Steel Service Centers including Ryerson Holding Corporation, which can tailor steel coils or sheets to specific anchor requirements. The subsequent Anchor Manufacturing phase is led by Construction Anchor Manufacturers including Hilti Corporation, which designs and produces anchors using processes including forging or casting.

Distribution and Sales are facilitated by Construction Supply Distributors including Ferguson plc, connecting manufacturers with construction companies and hardware stores. Alternatively, large anchor manufacturers opt for Direct Sales, especially for major projects or specialized anchor types. Further, Installation is handled by Construction Contractors or Specialist Installers, ensuring anchors are correctly placed according to manufacturer guidelines and building codes.

Construction Anchors Market Share Analysis: Mechanical held the dominant revenue share in 2024

The largest segment in the Construction Anchors Market is the "Mechanical" anchors segment. This dominance is driven by mechanical anchors are widely used in construction projects due to their versatility, reliability, and ease of installation. Mechanical anchors, such as wedge anchors, sleeve anchors, and expansion anchors, provide robust and secure fastening solutions for a variety of substrates, including concrete, masonry, brick, and stone. Additionally, mechanical anchors offer high load-bearing capacities and excellent pull-out resistance, making them suitable for anchoring heavy loads and structural elements in both residential and commercial construction applications. In addition, mechanical anchors are available in a wide range of sizes, materials, and configurations to meet the diverse needs of construction projects, providing flexibility and adaptability in anchor selection and installation. Further, advancements in anchor design and manufacturing technologies have led to the development of innovative mechanical anchors with enhanced performance characteristics, such as improved corrosion resistance, seismic resistance, and ease of use, further driving their widespread adoption in the construction industry. As a result, the "Mechanical" anchors segment is the largest segment in the Construction Anchors Market due to its versatility, reliability, and widespread use in construction applications requiring secure and durable anchoring solutions.

Construction Anchors Market Share Analysis: Stainless Steel is the fastest growing market segment over the forecast period to 2030

The fastest-growing segment in the Construction Anchors Market is the "Stainless Steel" segment. This trend is driven by stainless steel anchors offer superior corrosion resistance compared to carbon steel anchors, making them suitable for use in a wide range of construction applications, including outdoor and marine environments where exposure to moisture, humidity, and corrosive elements is prevalent. Additionally, stainless steel anchors provide long-term durability and reliability, reducing the need for maintenance and replacement over time, which is particularly advantageous in infrastructure projects and coastal regions. In addition, the increasing emphasis on sustainability and lifecycle cost considerations drives the demand for durable and long-lasting construction materials, favoring the adoption of stainless steel anchors over carbon steel alternatives. Further, advancements in stainless steel manufacturing technologies have led to the development of high-strength and low-maintenance stainless steel alloys tailored for specific construction applications, further enhancing their appeal and market acceptance. As a result, the "Stainless Steel" segment is the fastest-growing segment in the Construction Anchors Market, propelled by its superior corrosion resistance, durability, and suitability for a wide range of construction projects requiring reliable anchoring solutions in challenging environments.

Construction Anchors Market Share Analysis: Infrastructural is the fastest growing market segment over the forecast period to 2030

The fastest-growing segment in the Construction Anchors Market is the "Infrastructural" segment. This trend is driven by infrastructure projects, including bridges, tunnels, highways, dams, and airports, require robust and reliable anchoring solutions to ensure structural integrity, safety, and longevity. As governments and private sectors invest in infrastructure development and maintenance projects worldwide, there is a growing demand for high-performance construction anchors that can withstand dynamic loads, environmental factors, and harsh conditions associated with infrastructure applications. Additionally, infrastructure projects often involve challenging site conditions, such as seismic zones, coastal areas, and high-traffic environments, necessitating the use of specialized anchoring systems engineered to meet stringent performance requirements and regulatory standards. In addition, the increasing focus on resilient and sustainable infrastructure solutions drives the adoption of advanced anchoring technologies and materials that offer durability, corrosion resistance, and long-term performance in infrastructure applications. Further, the growing complexity and scale of infrastructure projects require innovative anchoring solutions that can accommodate large-scale construction requirements, tight project schedules, and budget constraints, further driving the demand for construction anchors in the infrastructural segment. As a result, the "Infrastructural" segment is the fastest-growing segment in the Construction Anchors Market, propelled by the increasing investments in infrastructure development, the need for reliable anchoring solutions in challenging environments, and the emphasis on resilient and sustainable infrastructure solutions worldwide.

Construction Anchors Market Report Scope-

By Product

Hangers

Mechanical

-Cast-In Anchors

-Post-Installed Anchors

-Chemical

-Nail-In

-Wall

-Others

By Material

Stainless Steel

Carbon Steel

Others

By End-User

Residential

Commercial

Industrial

Infrastructural

Construction Anchors Market Companies Profiled

Adolf Wurth GmbH & Co. KG

CEAS. (Construction Engineered Attachment Solutions)

Cobra Anchors

Fischer Fixings UK Ltd

Friulsider S.P.A.

Guangdong Kin Long Hardware Products Co. Ltd

Hilti Corp

Illinois Tool Works Inc

Koelner Rawlplug IP

Mechanical Plastics Corp

MKT Fastening LLC

SFS Group Fastening Technology Ltd

Sika AG

Stanley Black & Decker Inc- DEWALT

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Construction Anchors Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Construction Anchors Market Size Outlook, $ Million, 2021 to 2030

3.2 Construction Anchors Market Outlook by Type, $ Million, 2021 to 2030

3.3 Construction Anchors Market Outlook by Product, $ Million, 2021 to 2030

3.4 Construction Anchors Market Outlook by Application, $ Million, 2021 to 2030

3.5 Construction Anchors Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Construction Anchors Industry

4.2 Key Market Trends in Construction Anchors Industry

4.3 Potential Opportunities in Construction Anchors Industry

4.4 Key Challenges in Construction Anchors Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Construction Anchors Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Construction Anchors Market Outlook by Segments

7.1 Construction Anchors Market Outlook by Segments, $ Million, 2021- 2030

By Product

Hangers

Mechanical

-Cast-In Anchors

-Post-Installed Anchors

-Chemical

-Nail-In

-Wall

-Others

By Material

Stainless Steel

Carbon Steel

Others

By End-User

Residential

Commercial

Industrial

Infrastructural

8 North America Construction Anchors Market Analysis and Outlook To 2030

8.1 Introduction to North America Construction Anchors Markets in 2024

8.2 North America Construction Anchors Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Construction Anchors Market size Outlook by Segments, 2021-2030

By Product

Hangers

Mechanical

-Cast-In Anchors

-Post-Installed Anchors

-Chemical

-Nail-In

-Wall

-Others

By Material

Stainless Steel

Carbon Steel

Others

By End-User

Residential

Commercial

Industrial

Infrastructural

9 Europe Construction Anchors Market Analysis and Outlook To 2030

9.1 Introduction to Europe Construction Anchors Markets in 2024

9.2 Europe Construction Anchors Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Construction Anchors Market Size Outlook by Segments, 2021-2030

By Product

Hangers

Mechanical

-Cast-In Anchors

-Post-Installed Anchors

-Chemical

-Nail-In

-Wall

-Others

By Material

Stainless Steel

Carbon Steel

Others

By End-User

Residential

Commercial

Industrial

Infrastructural

10 Asia Pacific Construction Anchors Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Construction Anchors Markets in 2024

10.2 Asia Pacific Construction Anchors Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Construction Anchors Market size Outlook by Segments, 2021-2030

By Product

Hangers

Mechanical

-Cast-In Anchors

-Post-Installed Anchors

-Chemical

-Nail-In

-Wall

-Others

By Material

Stainless Steel

Carbon Steel

Others

By End-User

Residential

Commercial

Industrial

Infrastructural

11 South America Construction Anchors Market Analysis and Outlook To 2030

11.1 Introduction to South America Construction Anchors Markets in 2024

11.2 South America Construction Anchors Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Construction Anchors Market size Outlook by Segments, 2021-2030

By Product

Hangers

Mechanical

-Cast-In Anchors

-Post-Installed Anchors

-Chemical

-Nail-In

-Wall

-Others

By Material

Stainless Steel

Carbon Steel

Others

By End-User

Residential

Commercial

Industrial

Infrastructural

12 Middle East and Africa Construction Anchors Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Construction Anchors Markets in 2024

12.2 Middle East and Africa Construction Anchors Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Construction Anchors Market size Outlook by Segments, 2021-2030

By Product

Hangers

Mechanical

-Cast-In Anchors

-Post-Installed Anchors

-Chemical

-Nail-In

-Wall

-Others

By Material

Stainless Steel

Carbon Steel

Others

By End-User

Residential

Commercial

Industrial

Infrastructural

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Adolf Wurth GmbH & Co. KG

CEAS. (Construction Engineered Attachment Solutions)

Cobra Anchors

Fischer Fixings UK Ltd

Friulsider S.P.A.

Guangdong Kin Long Hardware Products Co. Ltd

Hilti Corp

Illinois Tool Works Inc

Koelner Rawlplug IP

Mechanical Plastics Corp

MKT Fastening LLC

SFS Group Fastening Technology Ltd

Sika AG

Stanley Black & Decker Inc- DEWALT

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Product

Hangers

Mechanical

-Cast-In Anchors

-Post-Installed Anchors

-Chemical

-Nail-In

-Wall

-Others

By Material

Stainless Steel

Carbon Steel

Others

By End-User

Residential

Commercial

Industrial

Infrastructural

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)