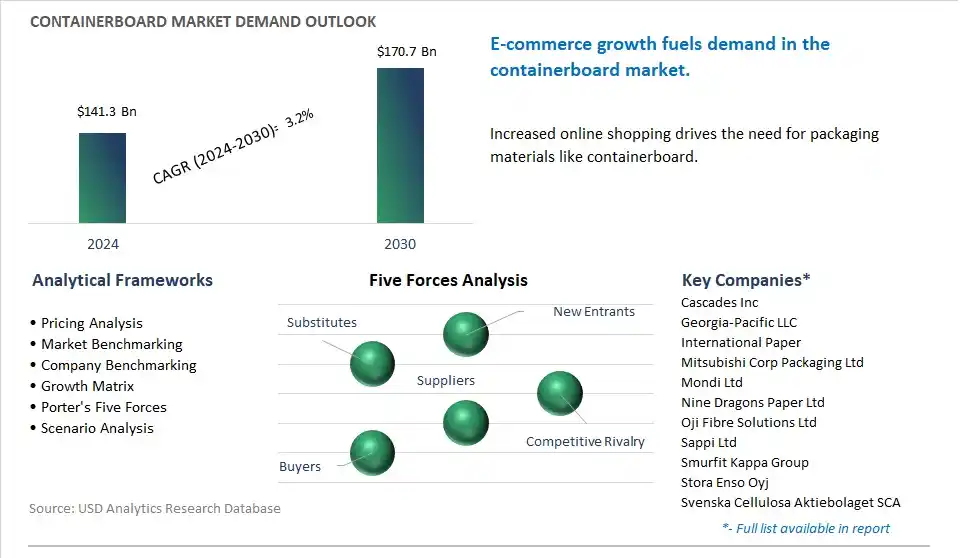

The global Containerboard Market is poised to register a 3.2% CAGR from $141.3 Billion in 2024 to $170.7 Billion in 2030.

The global Containerboard Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Material (Virgin Fibers, Recycled Fibers, Virgin + Recycled Fibers), By Type (Kraftliners, Testliners, Flutings, Others), By End-User (Food and Beverage, Consumer Goods, Industrial, Others).

An Introduction to Global Containerboard Market in 2024

The containerboard market is experiencing significant growth driven by the increasing demand for sustainable packaging solutions, e-commerce expansion, and shifting consumer preferences towards eco-friendly products. Key trends shaping the future of the industry include the rising adoption of lightweight and recyclable containerboard materials, innovative packaging designs, and digital printing technologies for brand differentiation and supply chain optimization. As companies strive to reduce environmental footprint and meet regulatory requirements, there's a growing need for containerboard solutions that offer strength, durability, and cost-efficiency while minimizing waste and carbon emissions. Moreover, advancements in containerboard manufacturing processes, such as energy-efficient production methods and alternative fiber sourcing, are driving market expansion. Additionally, the integration of smart packaging technologies, such as RFID tracking and sensor-enabled packaging, is enhancing supply chain visibility and product traceability, driving innovation and market growth in the containerboard industry.

Containerboard Market Competitive Landscape

The market report analyses the leading companies in the industry including Cascades Inc, Georgia-Pacific LLC, International Paper, Mitsubishi Corp Packaging Ltd, Mondi Ltd, Nine Dragons Paper Ltd, Oji Fibre Solutions Ltd, Sappi Ltd, Smurfit Kappa Group, Stora Enso Oyj, Svenska Cellulosa Aktiebolaget SCA, Westrock Company.

Containerboard Market Dynamics

Containerboard Market Trend: Increasing Demand for Sustainable Packaging Solutions

One prominent trend in the containerboard market is the increasing demand for sustainable packaging solutions. With growing environmental concerns and regulatory pressures, there is a rising preference for packaging materials that are recyclable, biodegradable, and sourced from renewable materials. Containerboard, made primarily from recycled paper fibers and virgin wood pulp, aligns with sustainability goals by offering a renewable and recyclable alternative to single-use plastics and non-biodegradable packaging materials. Additionally, containerboard's versatility and strength make it suitable for a wide range of packaging applications, including corrugated boxes, cartons, and packaging inserts, further driving its adoption as a sustainable packaging solution. This trend is driven by consumer preferences for eco-friendly products, corporate sustainability initiatives, and regulatory mandates promoting recycling and waste reduction, shaping the containerboard market towards more environmentally conscious options.

Containerboard Market Driver: Growth in E-commerce and Online Retail

A primary driver shaping the containerboard market is the growth in e-commerce and online retail activities. With the rise of digital commerce platforms and changing consumer shopping habits, there is a significant increase in the demand for shipping and delivery packaging to transport goods purchased online. Containerboard, as the primary material used in corrugated packaging, plays a vital role in fulfilling this demand by providing durable and protective packaging solutions for shipping and logistics purposes. Additionally, the trend towards omnichannel retailing and direct-to-consumer distribution models further drives the need for efficient and sustainable packaging solutions that can withstand the rigors of transportation while protecting products from damage. The expansion of e-commerce activities drives market demand for containerboard as a preferred packaging material, stimulating growth and investment in the containerboard industry.

Containerboard Market Opportunity: Innovation in Lightweight and High-Performance Grades

An opportunity within the containerboard market lies in innovation focused on lightweight and high-performance grades of containerboard. As businesses seek to optimize packaging efficiency, reduce shipping costs, and improve supply chain sustainability, there is a demand for containerboard grades that offer enhanced strength-to-weight ratios, improved printability, and superior moisture resistance. Lightweight containerboard grades allow for the production of thinner and lighter packaging materials without compromising performance, enabling cost savings and environmental benefits through reduced material usage and transportation emissions. Additionally, high-performance grades with advanced coatings or barrier properties provide added protection against moisture, grease, and punctures, expanding the range of applications for containerboard packaging in industries such as food and beverage, pharmaceuticals, and electronics. By investing in research and development to innovate lightweight and high-performance containerboard grades and collaborating with packaging converters and end-users to validate and implement these solutions, manufacturers can capitalize on opportunities to meet evolving customer needs, drive market differentiation, and create value in the containerboard industry.

Containerboard Market Share Analysis: Recycled Fibers segment generated the highest revenue in the industry

The recycled fibers segment is the largest segment in the Containerboard Market due to diverse key factors. The there is a growing global emphasis on sustainability and environmental responsibility, driving the demand for recycled packaging materials. Recycled fibers are derived from recovered paper and cardboard products, reducing the need for virgin wood pulp and minimizing the environmental impact of paper production. Additionally, recycled fibers offer comparable performance characteristics to virgin fibers in terms of strength, durability, and printability, making them suitable for a wide range of packaging applications, including corrugated boxes, cartons, and packaging inserts. In addition, the recycling process for paper and cardboard products consumes less energy and water compared to the production of virgin fibers, resulting in lower carbon emissions and resource consumption. Further, the availability of recycled fibers is increasing as recycling infrastructure improves and recycling rates continue to rise globally. This abundance of recycled fiber feedstock makes it a cost-effective and sustainable choice for manufacturers in the containerboard industry. Over the forecast period, the dominance of the recycled fibers segment in the Containerboard Market is attributed to its environmental benefits, performance characteristics, cost-effectiveness, and availability, making it the preferred choice for a majority of containerboard manufacturers and end-users.

Containerboard Market Share Analysis: Flutings Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The flutings segment is the fastest-growing segment in the Containerboard Market due to diverse compelling reasons. The the growing e-commerce industry and the shift towards online shopping have led to an increased demand for corrugated packaging materials, including flutings. Flutings are the corrugated medium sandwiched between two linerboards to form corrugated board, which is widely used in the production of shipping boxes, cartons, and packaging materials for e-commerce shipments. With the rise of e-commerce platforms and the surge in parcel deliveries, there is a corresponding increase in the consumption of corrugated packaging to protect goods during transit and ensure their safe delivery to consumers. Additionally, flutings offer excellent cushioning and impact resistance properties, providing adequate protection for a wide range of products, from fragile items to heavy goods. In addition, advancements in manufacturing technology have led to the development of high-performance flutings with improved strength, printability, and moisture resistance, further driving their adoption in the packaging industry. Further, the sustainability credentials of flutings, especially those made from recycled fibers, align with the growing environmental awareness among consumers and regulatory pressures for sustainable packaging solutions. Over the forecast period, the rapid growth of the flutings segment in the Containerboard Market is driven by the expanding e-commerce sector, the need for protective and sustainable packaging solutions, and advancements in fluting technology that enhance performance and versatility.

Containerboard Market Share Analysis: Food and Beverage Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The food and beverage segment is the fastest-growing segment in the Containerboard Market due to diverse compelling factors. The the food and beverage industry is experiencing rapid growth driven by changing consumer preferences, urbanization, and the rise of online grocery shopping. As the demand for packaged food and beverages increases, so does the need for reliable and sustainable packaging solutions. Containerboard is widely used in the packaging of various food and beverage products, including dry goods, fresh produce, beverages, and processed foods. Additionally, the stringent regulatory requirements for food safety and hygiene necessitate the use of high-quality packaging materials that ensure product integrity and prevent contamination. Containerboard offers excellent protection against moisture, grease, and other environmental factors, maintaining the freshness and quality of food and beverage products throughout the supply chain. In addition, the food and beverage industry is embracing sustainability initiatives, driving the adoption of eco-friendly packaging materials such as containerboard made from recycled fibers. Consumers are increasingly concerned about the environmental impact of packaging waste, leading to a preference for recyclable and biodegradable packaging options. Containerboard meets these sustainability criteria, making it a preferred choice for food and beverage manufacturers seeking to reduce their carbon footprint and meet consumer expectations for eco-friendly packaging. Further, the COVID-19 pandemic has accelerated the shift towards packaged food and beverages, as consumers prioritize safety and convenience, further driving the demand for containerboard packaging solutions in the food and beverage sector. Over the forecast period, the rapid growth of the food and beverage segment in the Containerboard Market is driven by the increasing demand for packaged food and beverages, stringent regulatory requirements, sustainability initiatives, and changing consumer preferences for safe and eco-friendly packaging options.

Containerboard Market Report Segmentation

By Material

Virgin Fibers

Recycled Fibers

Virgin + Recycled Fibers

By Type

Kraftliners

Testliners

Flutings

Others

By End-User

Food and Beverage

Consumer Goods

Industrial

Others

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Containerboard Companies Profiled in the Market Study

Cascades Inc

Georgia-Pacific LLC

International Paper

Mitsubishi Corp Packaging Ltd

Mondi Ltd

Nine Dragons Paper Ltd

Oji Fibre Solutions Ltd

Sappi Ltd

Smurfit Kappa Group

Stora Enso Oyj

Svenska Cellulosa Aktiebolaget SCA

Westrock Company

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Containerboard Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Containerboard Market Size Outlook, $ Million, 2021 to 2030

3.2 Containerboard Market Outlook by Type, $ Million, 2021 to 2030

3.3 Containerboard Market Outlook by Product, $ Million, 2021 to 2030

3.4 Containerboard Market Outlook by Application, $ Million, 2021 to 2030

3.5 Containerboard Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Containerboard Industry

4.2 Key Market Trends in Containerboard Industry

4.3 Potential Opportunities in Containerboard Industry

4.4 Key Challenges in Containerboard Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Containerboard Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Containerboard Market Outlook by Segments

7.1 Containerboard Market Outlook by Segments, $ Million, 2021- 2030

By Material

Virgin Fibers

Recycled Fibers

Virgin + Recycled Fibers

By Type

Kraftliners

Testliners

Flutings

Others

By End-User

Food and Beverage

Consumer Goods

Industrial

Others

8 North America Containerboard Market Analysis and Outlook To 2030

8.1 Introduction to North America Containerboard Markets in 2024

8.2 North America Containerboard Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Containerboard Market size Outlook by Segments, 2021-2030

By Material

Virgin Fibers

Recycled Fibers

Virgin + Recycled Fibers

By Type

Kraftliners

Testliners

Flutings

Others

By End-User

Food and Beverage

Consumer Goods

Industrial

Others

9 Europe Containerboard Market Analysis and Outlook To 2030

9.1 Introduction to Europe Containerboard Markets in 2024

9.2 Europe Containerboard Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Containerboard Market Size Outlook by Segments, 2021-2030

By Material

Virgin Fibers

Recycled Fibers

Virgin + Recycled Fibers

By Type

Kraftliners

Testliners

Flutings

Others

By End-User

Food and Beverage

Consumer Goods

Industrial

Others

10 Asia Pacific Containerboard Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Containerboard Markets in 2024

10.2 Asia Pacific Containerboard Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Containerboard Market size Outlook by Segments, 2021-2030

By Material

Virgin Fibers

Recycled Fibers

Virgin + Recycled Fibers

By Type

Kraftliners

Testliners

Flutings

Others

By End-User

Food and Beverage

Consumer Goods

Industrial

Others

11 South America Containerboard Market Analysis and Outlook To 2030

11.1 Introduction to South America Containerboard Markets in 2024

11.2 South America Containerboard Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Containerboard Market size Outlook by Segments, 2021-2030

By Material

Virgin Fibers

Recycled Fibers

Virgin + Recycled Fibers

By Type

Kraftliners

Testliners

Flutings

Others

By End-User

Food and Beverage

Consumer Goods

Industrial

Others

12 Middle East and Africa Containerboard Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Containerboard Markets in 2024

12.2 Middle East and Africa Containerboard Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Containerboard Market size Outlook by Segments, 2021-2030

By Material

Virgin Fibers

Recycled Fibers

Virgin + Recycled Fibers

By Type

Kraftliners

Testliners

Flutings

Others

By End-User

Food and Beverage

Consumer Goods

Industrial

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Cascades Inc

Georgia-Pacific LLC

International Paper

Mitsubishi Corp Packaging Ltd

Mondi Ltd

Nine Dragons Paper Ltd

Oji Fibre Solutions Ltd

Sappi Ltd

Smurfit Kappa Group

Stora Enso Oyj

Svenska Cellulosa Aktiebolaget SCA

Westrock Company

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Material

Virgin Fibers

Recycled Fibers

Virgin + Recycled Fibers

By Type

Kraftliners

Testliners

Flutings

Others

By End-User

Food and Beverage

Consumer Goods

Industrial

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)