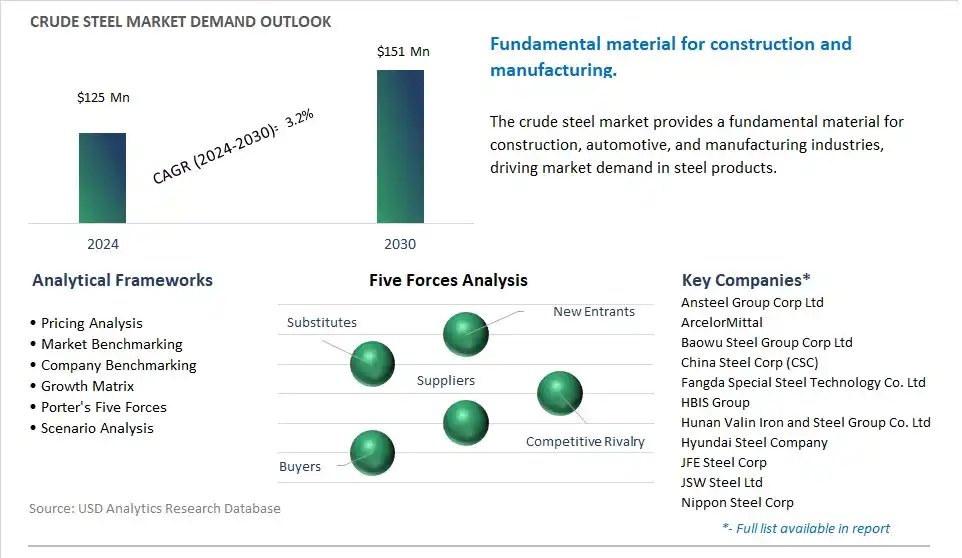

The global Crude Steel Market is poised to register a 3.2% CAGR from $125 Million in 2024 to $151 Million in 2030.

The global Crude Steel Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Composition (Killed Steel, Semi-Killed Steel), By Manufacturing Process (Basic Oxygen Furnace (BOF), Electric Arc Furnace (EAF)), By End-User (Building and Construction, Transportation, Tools and Machinery, Energy, Consumer Goods, Others).

An Introduction to Global Crude Steel Market in 2024

The future of the crude steel market is influenced by trends such as urbanization, infrastructure development, and technological advancements driving innovation in steel production, processing, and applications. Crude steel, the primary product of integrated steel mills, is a critical raw material for various industries including construction, automotive, machinery, and energy. Key trends shaping this market include the adoption of advanced manufacturing processes such as electric arc furnaces and direct reduced iron technology to improve energy efficiency, reduce emissions, and enhance productivity, the development of high-strength and lightweight steel alloys for automotive and transportation applications, and the integration of digital technologies such as artificial intelligence and automation for optimized production and quality control. As global demand for steel continues to grow, driven by urbanization, infrastructure renewal, and industrialization, the steel industry is expected to innovate and evolve to meet the challenges of sustainability, resource efficiency, and technological progress, driving market growth and shaping the future of steel production and applications.

Crude Steel Market Competitive Landscape

The market report analyses the leading companies in the industry including Ansteel Group Corp Ltd, ArcelorMittal, Baowu Steel Group Corp Ltd, China Steel Corp (CSC), Fangda Special Steel Technology Co. Ltd, HBIS Group, Hunan Valin Iron and Steel Group Co. Ltd, Hyundai Steel Company, JFE Steel Corp, JSW Steel Ltd, Nippon Steel Corp, Novolipetsk Steel (NLMK), Nucor Corp, POSCO (Pohang Iron and Steel Company), Rizhao Steel Holding Group Co. Ltd, Shagang Group Inc, Steel Authority of India Ltd (SAIL), Tata Steel Ltd, Techint Group, United States Steel Corp.

Crude Steel Market Dynamics

Crude Steel Market Trend: Increasing Demand for Sustainable Steel Production

One prominent market trend in the crude steel industry is the increasing demand for sustainable steel production methods. With growing concerns about climate change and environmental sustainability, there is a global push towards reducing carbon emissions and minimizing the environmental impact of industrial processes. Accordingly, steel producers are increasingly adopting technologies and practices aimed at improving energy efficiency, reducing greenhouse gas emissions, and utilizing recycled materials in steel production. The trend towards sustainable steelmaking methods, such as electric arc furnaces (EAFs) powered by renewable energy sources and the use of scrap steel as feedstock, is reshaping the crude steel market landscape and driving investments in greener steel production facilities.

Crude Steel Market Driver: Growth in Construction and Infrastructure Development

A key driver in the crude steel market is the growth in construction and infrastructure development worldwide. Steel is a fundamental material used in construction projects, infrastructure development, and manufacturing activities across various sectors, including buildings, bridges, roads, railways, automotive, and machinery. Rapid urbanization, population growth, and economic development in emerging markets are fueling demand for steel-intensive infrastructure projects such as skyscrapers, airports, highways, and power plants. Additionally, government initiatives aimed at stimulating economic growth through infrastructure investments, such as China's Belt and Road Initiative and infrastructure plans in India and Southeast Asia, are driving the demand for crude steel globally.

Crude Steel Market Opportunity: Adoption of Advanced Technologies for Steel Production

One potential opportunity in the crude steel market lies in the adoption of advanced technologies for steel production. As steelmakers face pressure to improve efficiency, reduce costs, and meet sustainability targets, there is an opportunity to invest in innovative technologies that optimize the steelmaking process. Advanced technologies such as direct reduced iron (DRI) plants, continuous casting, and next-generation blast furnaces offer opportunities to enhance productivity, reduce energy consumption, and lower carbon emissions in crude steel production. Additionally, digitalization, automation, and artificial intelligence (AI) technologies can optimize operations, improve process control, and enable predictive maintenance in steel manufacturing facilities. By embracing advanced technologies, steel producers can enhance their competitiveness, mitigate environmental impact, and capitalize on opportunities for growth in the dynamic global steel market.

Crude Steel Market Ecosystem

The crude steel Market Ecosystem encompasses a series of interconnected stages, with Raw Material Acquisition. Iron Ore Miners including Rio Tinto Group and Vale S.A. extract iron ore, while Coal Miners including Peabody Energy Corporation supply coal for metallurgical purposes. Flux Suppliers provide materials including limestone for steelmaking. Transportation and Logistics companies including Maersk handle the movement of raw materials to steel mills. Steelmaking involves Integrated Steel Producers including ArcelorMittal SA and Mini-Mills including Nucor Corporation, utilizing various processes to produce crude steel. Processing and Upgrading stages involve Semi-Finished Steel Producers, which further process crude steel into semi-finished products.

Following production, Distribution and Sales channels come into play, with Steel Trading Companies including Glencore plc sourcing and trading crude steel for downstream manufacturers. Large steel producers typically engage in Direct Sales, serving major customers in industries including automotive, construction, and machinery. Further, End-Use Applications see crude steel transformed into various finished products, including construction materials, automotive components, machinery, shipbuilding materials, and consumer durables, demonstrating its versatility across multiple sectors.

Crude Steel Market Share Analysis: Killed Steel held the dominant revenue share in 2024

Among the segments of the Crude Steel Market, "Killed Steel" is the largest segment. Killed steel is produced by adding deoxidizing agents during the steelmaking process to remove oxygen from the molten steel, thereby reducing the risk of gas porosity and improving the steel's overall quality and consistency. This process results in a more uniform composition and better mechanical properties compared to semi-killed steel. Killed steel finds extensive use in various industries, including automotive, construction, infrastructure, and machinery manufacturing, where stringent quality standards and reliability are paramount. Its superior properties make it suitable for critical applications requiring high strength, toughness, and weldability. In addition, advancements in steelmaking technologies and the growing demand for high-quality steel products in infrastructure development and industrial manufacturing further drive the dominance of killed steel in the Crude Steel Market.

Crude Steel Market Share Analysis: Electric Arc Furnace (EAF) is the fastest growing market segment over the forecast period to 2030

In the Crude Steel Market, the Electric Arc Furnace (EAF) segment is experiencing rapid growth due to diverse key factors. Firstly, EAF steelmaking offers significant advantages in terms of flexibility, efficiency, and sustainability compared to traditional Basic Oxygen Furnace (BOF) steelmaking. EAF technology utilizes scrap steel as its primary raw material, allowing for the recycling of steel scrap and reducing the reliance on virgin iron ore and coke, which are associated with higher energy consumption and environmental impact. This aligns with the growing emphasis on sustainability and circular economy principles in the steel industry. In addition, EAF steelmaking is inherently more adaptable to market demand fluctuations and can quickly adjust production volumes and product specifications to meet changing customer needs. Additionally, advancements in EAF technology, including the use of advanced electrodes, process controls, and automation, have improved energy efficiency, productivity, and product quality, further driving the adoption of EAF steelmaking globally. Overall, the combination of environmental benefits, operational flexibility, and technological advancements positions the Electric Arc Furnace (EAF) segment as the fastest-growing in the Crude Steel Market.

Crude Steel Market Share Analysis: Transportation is the fastest growing market segment over the forecast period to 2030

In the Crude Steel Market, the Transportation segment is experiencing rapid growth due to diverse key factors. Firstly, the transportation industry, encompassing automotive, rail, and maritime sectors, is witnessing robust growth driven by increasing urbanization, population growth, and economic development worldwide. This growth translates into rising demand for steel-intensive transportation infrastructure, vehicles, and equipment. Steel remains the material of choice in transportation due to its exceptional strength-to-weight ratio, durability, and cost-effectiveness, making it essential for vehicle bodies, chassis, structural components, and infrastructure such as bridges, railways, and ports. Additionally, advancements in automotive engineering, including the development of electric and autonomous vehicles, require innovative steel solutions to meet stringent safety, performance, and sustainability standards. In addition, government initiatives aimed at improving transportation infrastructure, reducing emissions, and promoting sustainable mobility further stimulate demand for steel in the transportation sector. Overall, the combination of growing transportation needs, technological advancements, and infrastructure investments positions the Transportation segment as the fastest-growing in the Crude Steel Market.

Crude Steel Market Report Scope-

By Composition

Killed Steel

Semi-Killed Steel

By Manufacturing Process

Basic Oxygen Furnace (BOF)

Electric Arc Furnace (EAF)

By End-User

Building and Construction

Transportation

Tools and Machinery

Energy

Consumer Goods

Others

Crude Steel Market Companies Profiled

Ansteel Group Corp Ltd

ArcelorMittal

Baowu Steel Group Corp Ltd

China Steel Corp (CSC)

Fangda Special Steel Technology Co. Ltd

HBIS Group

Hunan Valin Iron and Steel Group Co. Ltd

Hyundai Steel Company

JFE Steel Corp

JSW Steel Ltd

Nippon Steel Corp

Novolipetsk Steel (NLMK)

Nucor Corp

POSCO (Pohang Iron and Steel Company)

Rizhao Steel Holding Group Co. Ltd

Shagang Group Inc

Steel Authority of India Ltd (SAIL)

Tata Steel Ltd

Techint Group

United States Steel Corp

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Crude Steel Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Crude Steel Market Size Outlook, $ Million, 2021 to 2030

3.2 Crude Steel Market Outlook by Type, $ Million, 2021 to 2030

3.3 Crude Steel Market Outlook by Product, $ Million, 2021 to 2030

3.4 Crude Steel Market Outlook by Application, $ Million, 2021 to 2030

3.5 Crude Steel Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Crude Steel Industry

4.2 Key Market Trends in Crude Steel Industry

4.3 Potential Opportunities in Crude Steel Industry

4.4 Key Challenges in Crude Steel Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Crude Steel Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Crude Steel Market Outlook by Segments

7.1 Crude Steel Market Outlook by Segments, $ Million, 2021- 2030

By Composition

Killed Steel

Semi-Killed Steel

By Manufacturing Process

Basic Oxygen Furnace (BOF)

Electric Arc Furnace (EAF)

By End-User

Building and Construction

Transportation

Tools and Machinery

Energy

Consumer Goods

Others

8 North America Crude Steel Market Analysis and Outlook To 2030

8.1 Introduction to North America Crude Steel Markets in 2024

8.2 North America Crude Steel Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Crude Steel Market size Outlook by Segments, 2021-2030

By Composition

Killed Steel

Semi-Killed Steel

By Manufacturing Process

Basic Oxygen Furnace (BOF)

Electric Arc Furnace (EAF)

By End-User

Building and Construction

Transportation

Tools and Machinery

Energy

Consumer Goods

Others

9 Europe Crude Steel Market Analysis and Outlook To 2030

9.1 Introduction to Europe Crude Steel Markets in 2024

9.2 Europe Crude Steel Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Crude Steel Market Size Outlook by Segments, 2021-2030

By Composition

Killed Steel

Semi-Killed Steel

By Manufacturing Process

Basic Oxygen Furnace (BOF)

Electric Arc Furnace (EAF)

By End-User

Building and Construction

Transportation

Tools and Machinery

Energy

Consumer Goods

Others

10 Asia Pacific Crude Steel Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Crude Steel Markets in 2024

10.2 Asia Pacific Crude Steel Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Crude Steel Market size Outlook by Segments, 2021-2030

By Composition

Killed Steel

Semi-Killed Steel

By Manufacturing Process

Basic Oxygen Furnace (BOF)

Electric Arc Furnace (EAF)

By End-User

Building and Construction

Transportation

Tools and Machinery

Energy

Consumer Goods

Others

11 South America Crude Steel Market Analysis and Outlook To 2030

11.1 Introduction to South America Crude Steel Markets in 2024

11.2 South America Crude Steel Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Crude Steel Market size Outlook by Segments, 2021-2030

By Composition

Killed Steel

Semi-Killed Steel

By Manufacturing Process

Basic Oxygen Furnace (BOF)

Electric Arc Furnace (EAF)

By End-User

Building and Construction

Transportation

Tools and Machinery

Energy

Consumer Goods

Others

12 Middle East and Africa Crude Steel Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Crude Steel Markets in 2024

12.2 Middle East and Africa Crude Steel Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Crude Steel Market size Outlook by Segments, 2021-2030

By Composition

Killed Steel

Semi-Killed Steel

By Manufacturing Process

Basic Oxygen Furnace (BOF)

Electric Arc Furnace (EAF)

By End-User

Building and Construction

Transportation

Tools and Machinery

Energy

Consumer Goods

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Ansteel Group Corp Ltd

ArcelorMittal

Baowu Steel Group Corp Ltd

China Steel Corp (CSC)

Fangda Special Steel Technology Co. Ltd

HBIS Group

Hunan Valin Iron and Steel Group Co. Ltd

Hyundai Steel Company

JFE Steel Corp

JSW Steel Ltd

Nippon Steel Corp

Novolipetsk Steel (NLMK)

Nucor Corp

POSCO (Pohang Iron and Steel Company)

Rizhao Steel Holding Group Co. Ltd

Shagang Group Inc

Steel Authority of India Ltd (SAIL)

Tata Steel Ltd

Techint Group

United States Steel Corp

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Composition

Killed Steel

Semi-Killed Steel

By Manufacturing Process

Basic Oxygen Furnace (BOF)

Electric Arc Furnace (EAF)

By End-User

Building and Construction

Transportation

Tools and Machinery

Energy

Consumer Goods

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)