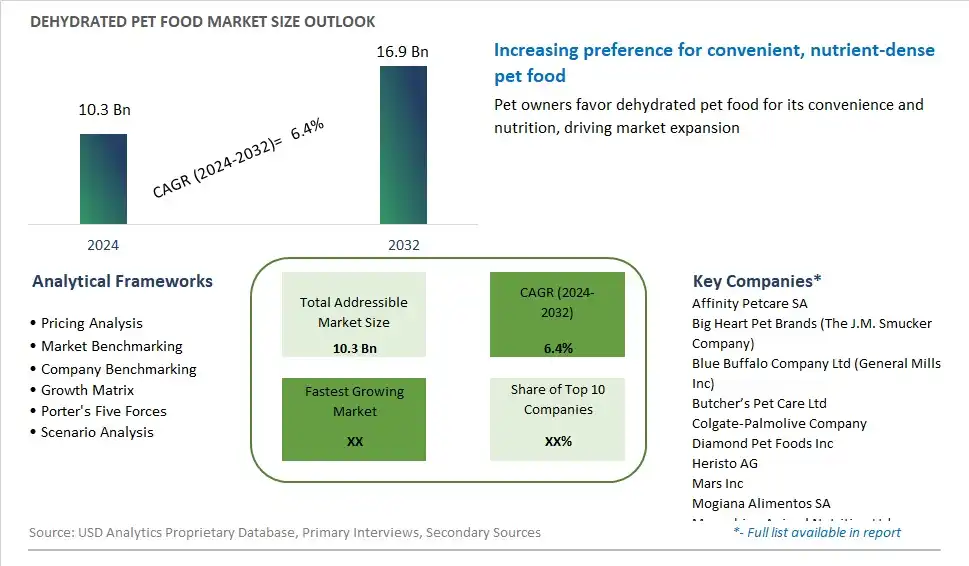

Global Dehydrated Pet Food Market Size is valued at $10.3 Billion in 2024 and is forecast to register a growth rate (CAGR) of 6.4% to reach $16.9 Billion by 2032.

The global Dehydrated Pet Food Market Comprehensive Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Nature (Natural, Conventional), By Pet (Cat, Dog, Birds), By Application (Pet Shops, Veterinary Clinics, Online, Others)

An Introduction to Dehydrated Pet Food Market

Dehydrated pet food is a type of pet food made from fresh ingredients that have been gently dehydrated to remove moisture while retaining nutrients and flavor in 2024. This process involves slowly drying raw ingredients such as meat, fruits, vegetables, and grains at low temperatures to preserve their natural goodness without the need for artificial preservatives or additives. Dehydrated pet food offers several benefits over traditional kibble, including higher nutritional value, enhanced digestibility, and improved palatability. It is also convenient to store, transport, and serve, as it requires less space and has a longer shelf life compared to fresh or frozen pet food. With the increasing emphasis on pet health and wellness, the demand for dehydrated pet food is growing. Pet owners are seeking natural, minimally processed diets for their furry companions, driving manufacturers to develop premium dehydrated pet food formulations that cater to specific dietary needs and preferences while ensuring the safety and quality of pet nutrition.

Dehydrated Pet Food Competitive Landscape

The market report analyses the leading companies in the industry including Affinity Petcare SA, Big Heart Pet Brands (The J.M. Smucker Company), Blue Buffalo Company Ltd (General Mills Inc), Butcher’s Pet Care Ltd, Colgate-Palmolive Company, Diamond Pet Foods Inc, Heristo AG, Mars Inc, Mogiana Alimentos SA, Moonshine Animal Nutrition Ltd, Nestlé Purina PetCare Company, Nisshin Pet Food Inc, Ramical SA, Total Alimentos SA, Unicharm Corp, and Others.

Dehydrated Pet Food Market Dynamics

Dehydrated Pet Food Market Trend: Growing Preference for Natural and Nutritious Pet Food Options

A significant trend in the dehydrated pet food market is the increasing preference among pet owners for natural and nutritious food options for their furry companions. As pet owners become more health-conscious and seek to provide their pets with diets that mirror their own dietary choices, there is a growing demand for pet foods made with high-quality, whole food ingredients. Dehydrated pet food offers a convenient and minimally processed option that retains the nutritional integrity of ingredients while providing pets with essential vitamins, minerals, and protein sources. This trend is driven by a desire to improve pet health and well-being, address food sensitivities and allergies, and promote longevity and vitality in companion animals. As consumers prioritize natural and holistic approaches to pet care, the demand for dehydrated pet food is expected to continue to rise, driving market growth and innovation in the pet food industry.

Market Driver: Pet Humanization and Premiumization Trends

A key driver of the dehydrated pet food market is the trend towards pet humanization and premiumization, whereby pets are increasingly viewed as members of the family and afforded the same level of care and attention as their human counterparts. Pet owners are willing to invest in higher-quality and more premium pet food options that offer health benefits, superior ingredients, and enhanced palatability. Dehydrated pet food appeals to this demographic of pet owners seeking natural, gourmet, and artisanal food options for their pets, reflecting their own preferences for high-quality, minimally processed foods. Additionally, as pet owners become more informed about pet nutrition and seek alternatives to traditional kibble and canned pet foods, the demand for dehydrated pet food as a premium and functional pet food option is expected to grow. The trend towards pet humanization and premiumization presents a significant opportunity for manufacturers to capitalize on the growing demand for premium pet food products and cater to the evolving needs and preferences of pet owners.

Market Opportunity: Expansion into Specialty and Functional Pet Food Segments

An opportunity for the dehydrated pet food market lies in expanding into specialty and functional pet food segments to meet the diverse needs and preferences of pet owners. By developing dehydrated pet food formulations tailored to specific dietary requirements, life stages, and health conditions, manufacturers can address niche markets and differentiate their products in a crowded marketplace. For example, offering dehydrated pet food options for pets with food sensitivities, weight management needs, or specific health issues such as joint health or skin and coat conditions can appeal to pet owners seeking specialized nutrition solutions for their pets. Furthermore, incorporating functional ingredients such as probiotics, antioxidants, and omega-3 fatty acids into dehydrated pet food formulations can enhance the nutritional profile and health benefits of the products, appealing to pet owners looking to support their pets' overall health and vitality. By expanding into specialty and functional pet food segments, the dehydrated pet food market can capture new market share, foster brand loyalty, and drive innovation in the pet food industry.

Dehydrated Pet Food Market Share Analysis: Natural Dehydrated Pet Food Market held the dominant market share in 2024

Within the segmentation of the Dehydrated Pet Food Market by Nature, the Natural Dehydrated Pet Food segment is the largest, propelled by several key factors driving its rapid growth. Natural dehydrated pet food offers pet owners a reassuring alternative to conventional options, free from artificial flavors, colors, and preservatives. With a growing emphasis on pet health and wellness, consumers increasingly seek out natural pet food formulations that mimic the nutritional benefits of a species-appropriate diet. Natural dehydrated pet food often contains high-quality ingredients such as real meat, fruits, and vegetables, providing essential nutrients and promoting overall well-being in pets. Additionally, the convenience and longer shelf life of dehydrated pet food appeal to pet owners looking for practical and cost-effective feeding solutions. As pet owners become more discerning about the ingredients in their pets' food and prioritize their furry companions' health, the natural dehydrated pet food market continues to expand, solidifying its position as a dominant force in the pet food industry.

Dehydrated Pet Food Market Share Analysis: Dehydrated Dog Food Market held the dominant market share in 2024

Among the segmentation of the Dehydrated Pet Food Market by Pet, the Dehydrated Dog Food segment stands out as the fastest-growing, driven by several key factors contributing to its exponential expansion. As dogs are one of the most popular and beloved pets globally, the demand for high-quality, nutritious food options for them continues to rise. Dehydrated dog food offers pet owners a convenient and nutritionally dense alternative to traditional kibble or canned food, with many formulations boasting natural ingredients and minimal processing. Additionally, the shift towards humanization of pets has led to increased scrutiny over the quality and safety of pet food, prompting pet owners to seek out premium options that prioritize their dogs' health and well-being. Dehydrated dog food often contains a higher percentage of real meat, fruits, and vegetables, providing essential nutrients and supporting optimal canine health. Furthermore, the ease of preparation and storage of dehydrated dog food appeals to busy pet owners looking for hassle-free feeding solutions. As the pet food industry continues to evolve and consumers become more educated about pet nutrition, the dehydrated dog food market is poised for sustained growth, driven by the increasing demand for premium, natural pet food options tailored to canine companions.

Dehydrated Pet Food Market Share Analysis: Dehydrated Pet Food Market in Pet Shops held the dominant market share in 2024

Within the segmentation of the Dehydrated Pet Food Market by Application, the Pet Shops segment is the largest, driven by several factors that contribute to its dominance in the market. Pet shops serve as convenient one-stop destinations for pet owners to purchase a variety of pet products, including food, toys, and accessories. These establishments often carry a diverse selection of dehydrated pet food brands and formulations, catering to the nutritional needs and preferences of different pets. Further, pet shop staff are typically knowledgeable about pet nutrition and can provide personalized recommendations to pet owners, further enhancing the shopping experience. Additionally, the physical presence of pet shops allows for tactile inspection of product packaging and ingredients, instilling trust and confidence in pet owners regarding the quality and safety of the food they purchase for their furry companions. As pet ownership continues to rise globally, pet shops remain essential retail channels for pet owners seeking convenient access to premium dehydrated pet food options, solidifying their position as the largest segment in the Dehydrated Pet Food Market by Application.

Dehydrated Pet Food Market Segmentation

By Nature

Natural

Conventional

By Pet

Cat

Dog

Birds

By Application

Pet Shops

Veterinary Clinics

Online

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Dehydrated Pet Food Companies Profiled in the Study

Affinity Petcare SA

Big Heart Pet Brands (The J.M. Smucker Company)

Blue Buffalo Company Ltd (General Mills Inc)

Butcher’s Pet Care Ltd

Colgate-Palmolive Company

Diamond Pet Foods Inc

Heristo AG

Mars Inc

Mogiana Alimentos SA

Moonshine Animal Nutrition Ltd

Nestlé Purina PetCare Company

Nisshin Pet Food Inc

Ramical SA

Total Alimentos SA

Unicharm Corp

*- List Not Exhaustive

Chapter 1. TABLE OF CONTENTS

Chapter 2. Introduction to Dehydrated Pet Food Market

2.1. Market Overview

2.2. Key Statistics and Report Highlights

2.3. Scope of the Comprehensive Study

2.3.1. Market Definition

2.3.2 Countries and Regions Covered

2.3.3 Research Objective

2.3.4 Units, Currency, and Conversions

2.3.5 Industry Value Chain

2.4. Key Market Segments

2.5. Key Companies

2.6. Study Period

Chapter 3. Strategic Analysis Review

3.1. Dehydrated Pet Food Pricing Analysis and Forecast

3.2. Porter’s Five Forces

3.3. Market Ecosystem

3.4. SWOT Analysis

3.5. Regulatory Scenario

3.3. Effects of Inflation, Russia-Ukraine War, moderating economic growth, and other macroeconomic factors

Chapter 4. Competitive Landscape

4.1. Market Share Analysis

4.1.1. Global Dehydrated Pet Food Market Share by Company, 2023

4.1.2. Product Offerings of Leading Dehydrated Pet Food Companies

4.2. Market Entropy

4.2.1. New Product Launches in the Industry

4.2.2. Mergers, Acquisitions, Joint ventures, and Partnerships

4.3. Key Strategies and Best Practices

Chapter 5. Global Market Projections: Best, Reference, and Low Case Scenarios

5.1. Growth Analysis- Case Scenario Definitions

5.2. Low Growth Case Scenario Forecasts

5.3. Reference Growth Case Scenario Forecasts

5.4. High Growth Case Scenario Forecasts

Chapter 6. Market Dynamics

6.1. Dehydrated Pet Food Market Drivers

6.2. Dehydrated Pet Food Market Challenges

6.6. Dehydrated Pet Food Market Opportunities

6.4. Dehydrated Pet Food Market Trends

Chapter 7. Global Dehydrated Pet Food Market Outlook Trends

7.1. Global Dehydrated Pet Food Revenue (USD Million) and CAGR (%) by Type (2021-2032)

7.2. Global Dehydrated Pet Food Revenue (USD Million) and CAGR (%) by Application (2021-2032)

7.3. Global Dehydrated Pet Food Revenue (USD Million) and CAGR (%) by Product (2021-2032)

By Nature

Natural

Conventional

By Pet

Cat

Dog

Birds

By Application

Pet Shops

Veterinary Clinics

Online

Others

Chapter 8. Global Dehydrated Pet Food Regional Analysis and Outlook

8.1. Global Dehydrated Pet Food Revenue (USD Million) By Regions (2021- 2032)

8.2. North America Dehydrated Pet Food Revenue (USD Million) by Country (2021-2032)

8.2.1. United States Dehydrated Pet Food Regional Analysis and Outlook

8.2.2. Canada Dehydrated Pet Food Regional Analysis and Outlook

8.2.3. Mexico Dehydrated Pet Food Regional Analysis and Outlook

8.3. Europe Dehydrated Pet Food Revenue (USD Million), by Country (2021-2032)

8.3.1. Germany Dehydrated Pet Food Regional Analysis and Outlook

8.3.2. France Dehydrated Pet Food Regional Analysis and Outlook

8.3.3. United Kingdom Dehydrated Pet Food Regional Analysis and Outlook

8.3.4. Spain Dehydrated Pet Food Regional Analysis and Outlook

8.3.5. Italy Dehydrated Pet Food Regional Analysis and Outlook

8.3.6. Russia Dehydrated Pet Food Regional Analysis and Outlook

8.3.7. Rest of Europe Dehydrated Pet Food Regional Analysis and Outlook

8.4. Asia Pacific Dehydrated Pet Food Revenue (USD Million) by Country (2021-2032)

8.4.1. China Dehydrated Pet Food Regional Analysis and Outlook

8.4.2. Japan Dehydrated Pet Food Regional Analysis and Outlook

8.4.3. India Dehydrated Pet Food Regional Analysis and Outlook

8.4.4. South Korea Dehydrated Pet Food Regional Analysis and Outlook

8.4.5. Australia Dehydrated Pet Food Regional Analysis and Outlook

8.4.6. South East Asia Dehydrated Pet Food Regional Analysis and Outlook

8.4.7. Rest of Asia Pacific Dehydrated Pet Food Regional Analysis and Outlook

8.5. South America Dehydrated Pet Food Revenue (USD Million), by Country (2021-2032)

8.5.1. Brazil Dehydrated Pet Food Regional Analysis and Outlook

8.5.2. Argentina Dehydrated Pet Food Regional Analysis and Outlook

8.5.3. Rest of South America Dehydrated Pet Food Regional Analysis and Outlook

8.6. Middle East and Africa Dehydrated Pet Food Revenue (USD Million) by Country (2021-2032)

8.6.1. Middle East Dehydrated Pet Food Regional Analysis and Outlook

8.6.2. Africa Dehydrated Pet Food Regional Analysis and Outlook

Chapter 9. North America Dehydrated Pet Food Analysis and Outlook

9.1. North America Dehydrated Pet Food Revenue (USD Million) by Segments (2021-2032)

9.1.1. North America Dehydrated Pet Food Revenue (USD Million) by Type (2021-2032)

9.1.2. North America Dehydrated Pet Food Revenue (USD Million) by Application (2021-2032)

9.1.3. North America Dehydrated Pet Food Revenue (USD Million) by Product (2021-2032)

By Nature

Natural

Conventional

By Pet

Cat

Dog

Birds

By Application

Pet Shops

Veterinary Clinics

Online

Others

Chapter 10. Europe Dehydrated Pet Food Analysis and Outlook

10.1. Europe Dehydrated Pet Food Revenue (USD Million), by Segments (USD Million) (2021-2032)

10.1.1. Europe Dehydrated Pet Food Revenue (USD Million) by Type (2021-2032)

10.1.2. Europe Dehydrated Pet Food Revenue (USD Million) by Application (2021-2032)

10.1.3. Europe Dehydrated Pet Food Revenue (USD Million) by Product (2021-2032)

By Nature

Natural

Conventional

By Pet

Cat

Dog

Birds

By Application

Pet Shops

Veterinary Clinics

Online

Others

Chapter 11. Asia Pacific Dehydrated Pet Food Analysis and Outlook

11.1. Asia Pacific Dehydrated Pet Food Revenue (USD Million), and Revenue (USD Million) by Segments (2021-2032)

11.1.1. Asia Pacific Dehydrated Pet Food Revenue (USD Million) by Type (2021-2032)

11.1.2. Asia Pacific Dehydrated Pet Food Revenue (USD Million) by Application (2021-2032)

11.1.3. Asia Pacific Dehydrated Pet Food Revenue (USD Million) by Product (2021-2032)

By Nature

Natural

Conventional

By Pet

Cat

Dog

Birds

By Application

Pet Shops

Veterinary Clinics

Online

Others

Chapter 12. South America Dehydrated Pet Food Analysis and Outlook

12.1. South America Dehydrated Pet Food Revenue (USD Million), by Segments (2021-2032)

12.1.1. South America Dehydrated Pet Food Revenue (USD Million) by Type (2021-2032)

12.1.2. South America Dehydrated Pet Food Revenue (USD Million) by Application (2021-2032)

12.1.3. South America Dehydrated Pet Food Revenue (USD Million) by Product (2021-2032)

By Nature

Natural

Conventional

By Pet

Cat

Dog

Birds

By Application

Pet Shops

Veterinary Clinics

Online

Others

Chapter 13. Middle East and Africa Dehydrated Pet Food Analysis and Outlook

13.1. Middle East and Africa Dehydrated Pet Food Revenue (USD Million), by Segments (2021-2032)

13.1.1. Middle East and Africa Dehydrated Pet Food Revenue (USD Million) by Type (2021-2032)

13.1.2. Middle East and Africa Dehydrated Pet Food Revenue (USD Million) by Application (2021-2032)

13.1.3. Middle East and Africa Dehydrated Pet Food Revenue (USD Million) by Product (2021-2032)

By Nature

Natural

Conventional

By Pet

Cat

Dog

Birds

By Application

Pet Shops

Veterinary Clinics

Online

Others

Chapter 14. Dehydrated Pet Food Company Profiles

14.1 Business Overview

14.2 Product Profiles

14.3 SWOT Profiles

14.5 Recent Developments

14.6 Financial Profile

List of Companies

Affinity Petcare SA

Big Heart Pet Brands (The J.M. Smucker Company)

Blue Buffalo Company Ltd (General Mills Inc)

Butcher’s Pet Care Ltd

Colgate-Palmolive Company

Diamond Pet Foods Inc

Heristo AG

Mars Inc

Mogiana Alimentos SA

Moonshine Animal Nutrition Ltd

Nestlé Purina PetCare Company

Nisshin Pet Food Inc

Ramical SA

Total Alimentos SA

Unicharm Corp

15. Methodology and Data Sources

15.1 Customization Offerings

15.2 Subscription Services

15.3 Related Reports

15.4 Publisher Expertise

LIST OF TABLES

Table 1 Market Segmentation Analysis

Table 2 Global Dehydrated Pet Food Market Share of Leading Companies, 2023

Table 3 Product Offerings of Leading Companies

Table 4 Low Growth Scenario Forecasts

Table 5 Reference Case Growth Scenario

Table 6 High Growth Case Scenario

Table 7 Global Dehydrated Pet Food Revenue (USD Million) And CAGR (%) By Type (2021-2032)

Table 8 Global Dehydrated Pet Food Revenue (USD Million) And CAGR (%) By Application (2021-2032)

Table 9 Global Dehydrated Pet Food Revenue (USD Million) And CAGR (%) By Product (2021-2032)

Table 10 Global Dehydrated Pet Food Market Revenue (USD Million) By Regions (2021-2032)

Table 11 Global Dehydrated Pet Food Market Share (%) By Regions (2021-2032)

Table 12 North America Dehydrated Pet Food Revenue (USD Million) By Country (2021-2032)

Table 13 Europe Dehydrated Pet Food Revenue (USD Million) By Country (2021-2032)

Table 14 Asia Pacific Dehydrated Pet Food Revenue (USD Million) By Country (2021-2032)

Table 15 South America Dehydrated Pet Food Revenue (USD Million) By Country (2021-2032)

Table 16 Middle East and Africa Dehydrated Pet Food Revenue (USD Million) By Region (2021-2032)

Table 17 North America Dehydrated Pet Food Revenue (USD Million) By Type (2021-2032)

Table 18 North America Dehydrated Pet Food Revenue (USD Million) By Application (2021-2032)

Table 19 North America Dehydrated Pet Food Revenue (USD Million) By Product (2021-2032)

Table 20 Europe Dehydrated Pet Food Revenue (USD Million) By Type (2021-2032)

Table 21 Europe Dehydrated Pet Food Revenue (USD Million) By Application (2021-2032)

Table 22 Europe Dehydrated Pet Food Revenue (USD Million) By Product (2021-2032)

Table 23 Asia Pacific Dehydrated Pet Food Revenue (USD Million) By Type (2021-2032)

Table 24 Asia Pacific Dehydrated Pet Food Revenue (USD Million) By Application (2021-2032)

Table 25 Asia Pacific Dehydrated Pet Food Revenue (USD Million) By Product (2021-2032)

Table 26 South America Dehydrated Pet Food Revenue (USD Million) By Type (2021-2032)

Table 27 South America Dehydrated Pet Food Revenue (USD Million) By Application (2021-2032)

Table 28 South America Dehydrated Pet Food Revenue (USD Million) By Product (2021-2032)

Table 29 Middle East and Africa Dehydrated Pet Food Revenue (USD Million) By Type (2021-2032)

Table 30 Middle East and Africa Dehydrated Pet Food Revenue (USD Million) By Application (2021-2032)

Table 31 Middle East and Africa Dehydrated Pet Food Revenue (USD Million) By Product (2021-2032)

LIST OF FIGURES

Figure 1. Market Scope

Figure 2. Pricing Forecasts Per Unit, 2023- 2032

Figure 3. Porter’s Five Forces

Figure 4. Global Dehydrated Pet Food Market Revenue (USD Million) By Regions (2021-2032)

Figure 5. Global Dehydrated Pet Food Market Share (%) By Regions (2023)

Figure 6. North America Dehydrated Pet Food Revenue (USD Million) By Country (2021-2032)

Figure 7. United States Dehydrated Pet Food Revenue (USD Million) By Country (2021-2032)

Figure 8. Canada Dehydrated Pet Food Revenue (USD Million) By Country (2021-2032)

Figure 9. Mexico Dehydrated Pet Food Revenue (USD Million) By Country (2021-2032)

Figure 10. Europe Dehydrated Pet Food Revenue (USD Million) By Country (2021-2032)

Figure 11. Germany Dehydrated Pet Food Revenue (USD Million) By Country (2021-2032)

Figure 12. France Dehydrated Pet Food Revenue (USD Million) By Country (2021-2032)

Figure 13. United Kingdom Dehydrated Pet Food Revenue (USD Million) By Country (2021-2032)

Figure 14. Spain Dehydrated Pet Food Revenue (USD Million) By Country (2021-2032)

Figure 15. Italy Dehydrated Pet Food Revenue (USD Million) By Country (2021-2032)

Figure 16. Russia Dehydrated Pet Food Revenue (USD Million) By Country (2021-2032)

Figure 17. Rest of Europe Dehydrated Pet Food Revenue (USD Million) By Country (2021-2032)

Figure 11. Asia Pacific Dehydrated Pet Food Revenue (USD Million) By Country (2021-2032)

Figure 12. China Dehydrated Pet Food Revenue (USD Million) By Country (2021-2032)

Figure 13. Japan Dehydrated Pet Food Revenue (USD Million) By Country (2021-2032)

Figure 14. India Dehydrated Pet Food Revenue (USD Million) By Country (2021-2032)

Figure 15. South Korea Dehydrated Pet Food Revenue (USD Million) By Country (2021-2032)

Figure 16. Australia Dehydrated Pet Food Revenue (USD Million) By Country (2021-2032)

Figure 17. South East Asia Dehydrated Pet Food Revenue (USD Million) By Country (2021-2032)

Figure 18. South America Dehydrated Pet Food Revenue (USD Million) By Country (2021-2032)

Figure 19. Brazil Dehydrated Pet Food Revenue (USD Million) By Country (2021-2032)

Figure 20. Argentina Dehydrated Pet Food Revenue (USD Million) By Country (2021-2032)

Figure 21. Rest of Asia Pacific Dehydrated Pet Food Revenue (USD Million) By Country (2021-2032)

Figure 22. Middle East and Africa Dehydrated Pet Food Revenue (USD Million) By Region (2021-2032)

Figure 23. Saudi Arabia Dehydrated Pet Food Revenue (USD Million) By Region (2021-2032)

Figure 24. The UAE Dehydrated Pet Food Revenue (USD Million) By Region (2021-2032)

Figure 25. Rest of Middle East Dehydrated Pet Food Revenue (USD Million) By Region (2021-2032)

Figure 26. South Africa Dehydrated Pet Food Revenue (USD Million) By Region (2021-2032)

Figure 27. Africa Dehydrated Pet Food Revenue (USD Million) By Region (2021-2032)

Figure 28. North America Dehydrated Pet Food Revenue (USD Million) By Type (2021-2032)

Figure 29. North America Dehydrated Pet Food Revenue (USD Million) By Application (2021-2032)

Figure 30. North America Dehydrated Pet Food Revenue (USD Million) By Product (2021-2032)

Figure 31. Europe Dehydrated Pet Food Revenue (USD Million) By Type (2021-2032)

Figure 32. Europe Dehydrated Pet Food Revenue (USD Million) By Application (2021-2032)

Figure 33. Europe Dehydrated Pet Food Revenue (USD Million) By Product (2021-2032)

Figure 34. Asia Pacific Dehydrated Pet Food Revenue (USD Million) By Type (2021-2032)

Figure 35. Asia Pacific Dehydrated Pet Food Revenue (USD Million) By Application (2021-2032)

Figure 36. Asia Pacific Dehydrated Pet Food Revenue (USD Million) By Product (2021-2032)

Figure 37. South America Dehydrated Pet Food Revenue (USD Million) By Type (2021-2032)

Figure 38. South America Dehydrated Pet Food Revenue (USD Million) By Application (2021-2032)

Figure 39. South America Dehydrated Pet Food Revenue (USD Million) By Product (2021-2032)

Figure 40. Middle East and Africa Dehydrated Pet Food Revenue (USD Million) By Type (2021-2032)

Figure 41. Middle East and Africa Dehydrated Pet Food Revenue (USD Million) By Application (2021-2032)

Figure 42. Middle East and Africa Dehydrated Pet Food Revenue (USD Million) By Product (2021-2032)

By Nature

Natural

Conventional

By Pet

Cat

Dog

Birds

By Application

Pet Shops

Veterinary Clinics

Online

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)