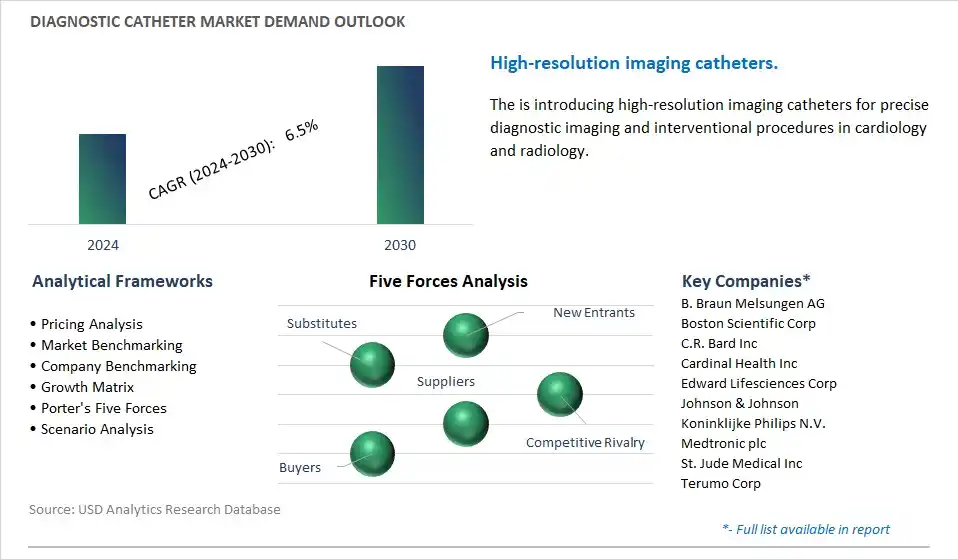

Diagnostic Catheter Market is estimated to increase at a Compounded Annual Growth Rate of 6.5% CAGR over the forecast period from 2024 to 2030

The Diagnostic Catheter Market study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments- By Type (Diagnostic Imaging Catheters, Non-Imaging Diagnostic Catheter), By Application (Cardiology, Urology, Gastroenterology, Neurology, Others), By End-User (Hospitals, Diagnostic and Imaging Centers, Others).

An Introduction to Diagnostic Catheter Market in 2024

Diagnostic catheters are medical devices used in interventional cardiology, radiology, and electrophysiology procedures to access, visualize, and diagnose cardiovascular conditions and anatomical structures. In 2024, diagnostic catheters play a crucial role in the diagnosis and treatment of cardiovascular diseases, including coronary artery disease, valvular heart disease, and arrhythmias. These catheters are inserted into blood vessels through minimally invasive procedures, such as cardiac catheterization or angiography, allowing healthcare providers to perform diagnostic tests, measure hemodynamic parameters, and obtain imaging of the heart and blood vessels. Diagnostic catheters may include various types, such as angiographic catheters, intravascular ultrasound (IVUS) catheters, pressure-sensing catheters, and electrophysiology catheters, each designed for specific diagnostic purposes and procedural requirements. With advancements in catheter design, imaging technology, and navigational systems, diagnostic catheters offer improved maneuverability, visualization, and diagnostic accuracy, enabling clinicians to precisely assess cardiovascular anatomy, identify pathological conditions, and plan appropriate treatment strategies. By facilitating early diagnosis and intervention for cardiovascular diseases, diagnostic catheters contribute to improved patient outcomes, reduced procedural risks, and enhanced quality of care in cardiology practice.

Market Trend: Advancements in Minimally Invasive Diagnostic Procedures

A significant trend in the diagnostic catheter market is the continuous advancements in minimally invasive diagnostic procedures. Technological innovations in catheter design, imaging modalities, and navigation systems have enabled healthcare providers to perform a wide range of diagnostic procedures with greater precision and less invasiveness. Diagnostic catheters equipped with advanced imaging technologies such as intravascular ultrasound (IVUS), optical coherence tomography (OCT), and fluoroscopy allow for detailed visualization of blood vessels and organs, facilitating accurate diagnosis of cardiovascular, neurological, and gastrointestinal conditions. Additionally, the development of robotic-assisted catheterization systems and navigational tools enhances procedural efficiency and patient outcomes, driving the adoption of minimally invasive diagnostic catheterization techniques in clinical practice.

Market Driver: Growing Incidence of Cardiovascular Diseases

A key driver fueling the diagnostic catheter market is the growing incidence of cardiovascular diseases (CVDs) worldwide. Cardiovascular diseases, including coronary artery disease, arrhythmias, and heart failure, continue to be a leading cause of morbidity and mortality globally. The increasing prevalence of risk factors such as obesity, hypertension, diabetes, and sedentary lifestyles contributes to the rising burden of CVDs, necessitating timely and accurate diagnostic interventions. Diagnostic catheterization procedures play a crucial role in the diagnosis and management of cardiovascular conditions by providing essential information on cardiac anatomy, function, and hemodynamics. As the demand for diagnostic catheterization services grows with the rising incidence of CVDs, healthcare providers invest in advanced catheterization technologies to improve diagnostic accuracy, guide treatment decisions, and optimize patient outcomes, thereby driving market growth and innovation in diagnostic catheter systems.

Market Opportunity: Expansion into Interventional Diagnostic Catheterization

An opportunity within the diagnostic catheter market lies in the expansion into interventional diagnostic catheterization. While traditional diagnostic catheters are primarily used for imaging and assessment purposes, there is a growing demand for catheter-based interventions that combine diagnosis with therapeutic procedures. Interventional diagnostic catheterization techniques such as fractional flow reserve (FFR), intracardiac echocardiography (ICE), and transesophageal echocardiography (TEE) enable healthcare providers to perform minimally invasive treatments such as angioplasty, stent placement, and valve repair under real-time imaging guidance. By expanding into interventional diagnostic catheterization, manufacturers can offer comprehensive solutions that address both diagnostic and therapeutic needs, providing healthcare providers with versatile tools for the diagnosis and treatment of cardiovascular and other diseases. This opportunity allows manufacturers to capitalize on the growing demand for integrated diagnostic and interventional catheterization technologies, driving market expansion and differentiation in the diagnostic catheter segment.

Diagnostic Catheter Market Share Analysis: Diagnostic Imaging Catheters is the fastest growing segment over the forecast period to 2030

In the Diagnostic Catheter Market, the Diagnostic Imaging Catheters segment emerges as the fastest-growing segment. This growth is propelled by several key factors. Firstly, diagnostic imaging catheters offer advanced visualization capabilities that enable clinicians to obtain detailed real-time images of the internal structures and vasculature during diagnostic procedures. These catheters are equipped with imaging modalities such as fluoroscopy, intravascular ultrasound (IVUS), optical coherence tomography (OCT), and magnetic resonance imaging (MRI), allowing for precise localization of lesions, assessment of vessel morphology, and guidance of interventional procedures. Additionally, diagnostic imaging catheters provide valuable insights into cardiac anatomy, coronary artery disease, urological disorders, gastrointestinal abnormalities, and neurological conditions, facilitating accurate diagnosis and treatment planning. Moreover, advancements in imaging technology and catheter design have led to the development of high-resolution imaging catheters with enhanced image quality, improved maneuverability, and increased patient safety. Furthermore, the growing prevalence of cardiovascular diseases, neurological disorders, and other chronic conditions, coupled with the rising demand for minimally invasive diagnostic procedures, drive the adoption of diagnostic imaging catheters in hospitals, diagnostic and imaging centers, and other healthcare facilities. As clinicians increasingly rely on advanced imaging modalities to guide diagnostic and interventional procedures, the Diagnostic Imaging Catheters segment is experiencing rapid growth and is expected to continue expanding in the Diagnostic Catheter Market.

Diagnostic Catheter Competitive Analysis

The market research study provides in-depth insights into leading companies including the SWOT analyses, product profile, financial details, and recent developments acrossB. Braun Melsungen AG, Boston Scientific Corp, C.R. Bard Inc, Cardinal Health Inc, Edward Lifesciences Corp, Johnson & Johnson , Koninklijke Philips N.V., Medtronic plc, St. Jude Medical Inc, Terumo Corp

Diagnostic Catheter Market Segmentation

By Type

Diagnostic Imaging Catheters

Non-Imaging Diagnostic Catheter

By Application

Cardiology

Urology

Gastroenterology

Neurology

Others

By End-User

Hospitals

Diagnostic and Imaging Centers

Others

Geographical Analysis

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Diagnostic Catheter Market Companies

B. Braun Melsungen AG

Boston Scientific Corp

C.R. Bard Inc

Cardinal Health Inc

Edward Lifesciences Corp

Johnson & Johnson

Koninklijke Philips N.V.

Medtronic plc

St. Jude Medical Inc

Terumo Corp

Reasons to Buy the Diagnostic Catheter Market Study

• Deepen your industry insights and navigate uncertainties for strategy formulation, CAPEX, and Operational decisions

• Gain access to detailed insights on the Diagnostic Catheter Market, encompassing current market size, growth trends, and forecasts till 2030.

• Access detailed competitor analysis, enabling competitive advantage through a thorough understanding of market players, strategies, and potential differentiation opportunities

• Stay ahead of the curve with insights on technological advancements, innovations, and upcoming trends

• Identify lucrative investment avenues and expansion opportunities within the Diagnostic Catheter Market industry, guided by robust, data-backed analysis.

• Understand regional and global markets through country-wise analysis, regional market potential, regulatory nuances, and dynamics

• Execute strategies with confidence and speed through information, analytics, and insights on the industry value chain

• Corporate leaders, strategists, financial experts, shareholders, asset managers, and governmental representatives can make long-term planning scenarios and build an integrated and timely understanding of market dynamics

• Benefit from tailored solutions and expert consultation based on report insights, providing personalized strategies aligned with specific business needs.

TABLE OF CONTENTS

1 Introduction to 2024 Diagnostic Catheter Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Diagnostic Catheter Market Size Outlook, $ Million, 2021 to 2030

3.2 Diagnostic Catheter Market Outlook by Type, $ Million, 2021 to 2030

3.3 Diagnostic Catheter Market Outlook by Product, $ Million, 2021 to 2030

3.4 Diagnostic Catheter Market Outlook by Application, $ Million, 2021 to 2030

3.5 Diagnostic Catheter Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Diagnostic Catheter Industry

4.2 Key Market Trends in Diagnostic Catheter Industry

4.3 Potential Opportunities in Diagnostic Catheter Industry

4.4 Key Challenges in Diagnostic Catheter Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Diagnostic Catheter Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Diagnostic Catheter Market Outlook by Segments

7.1 Diagnostic Catheter Market Outlook by Segments, $ Million, 2021- 2030

By Type

Diagnostic Imaging Catheters

Non-Imaging Diagnostic Catheter

By Application

Cardiology

Urology

Gastroenterology

Neurology

Others

By End-User

Hospitals

Diagnostic and Imaging Centers

Others

8 North America Diagnostic Catheter Market Analysis and Outlook To 2030

8.1 Introduction to North America Diagnostic Catheter Markets in 2024

8.2 North America Diagnostic Catheter Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Diagnostic Catheter Market size Outlook by Segments, 2021-2030

By Type

Diagnostic Imaging Catheters

Non-Imaging Diagnostic Catheter

By Application

Cardiology

Urology

Gastroenterology

Neurology

Others

By End-User

Hospitals

Diagnostic and Imaging Centers

Others

9 Europe Diagnostic Catheter Market Analysis and Outlook To 2030

9.1 Introduction to Europe Diagnostic Catheter Markets in 2024

9.2 Europe Diagnostic Catheter Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Diagnostic Catheter Market Size Outlook by Segments, 2021-2030

By Type

Diagnostic Imaging Catheters

Non-Imaging Diagnostic Catheter

By Application

Cardiology

Urology

Gastroenterology

Neurology

Others

By End-User

Hospitals

Diagnostic and Imaging Centers

Others

10 Asia Pacific Diagnostic Catheter Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Diagnostic Catheter Markets in 2024

10.2 Asia Pacific Diagnostic Catheter Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Diagnostic Catheter Market size Outlook by Segments, 2021-2030

By Type

Diagnostic Imaging Catheters

Non-Imaging Diagnostic Catheter

By Application

Cardiology

Urology

Gastroenterology

Neurology

Others

By End-User

Hospitals

Diagnostic and Imaging Centers

Others

11 South America Diagnostic Catheter Market Analysis and Outlook To 2030

11.1 Introduction to South America Diagnostic Catheter Markets in 2024

11.2 South America Diagnostic Catheter Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Diagnostic Catheter Market size Outlook by Segments, 2021-2030

By Type

Diagnostic Imaging Catheters

Non-Imaging Diagnostic Catheter

By Application

Cardiology

Urology

Gastroenterology

Neurology

Others

By End-User

Hospitals

Diagnostic and Imaging Centers

Others

12 Middle East and Africa Diagnostic Catheter Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Diagnostic Catheter Markets in 2024

12.2 Middle East and Africa Diagnostic Catheter Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Diagnostic Catheter Market size Outlook by Segments, 2021-2030

By Type

Diagnostic Imaging Catheters

Non-Imaging Diagnostic Catheter

By Application

Cardiology

Urology

Gastroenterology

Neurology

Others

By End-User

Hospitals

Diagnostic and Imaging Centers

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

List of Companies

B. Braun Melsungen AG

Boston Scientific Corp

C.R. Bard Inc

Cardinal Health Inc

Edward Lifesciences Corp

Johnson & Johnson

Koninklijke Philips N.V.

Medtronic plc

St. Jude Medical Inc

Terumo Corp

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

Diagnostic Imaging Catheters

Non-Imaging Diagnostic Catheter

By Application

Cardiology

Urology

Gastroenterology

Neurology

Others

By End-User

Hospitals

Diagnostic and Imaging Centers

Others

Countries Analyzed

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)