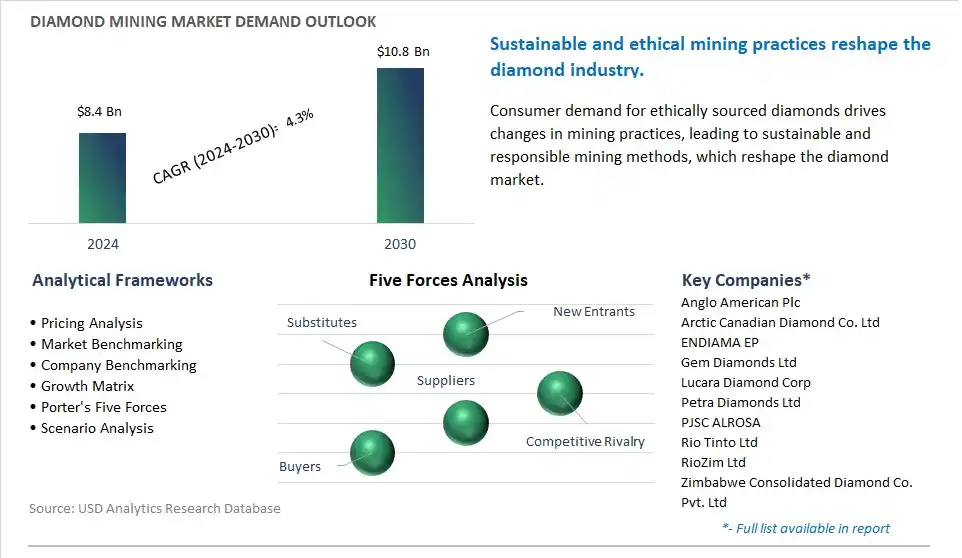

The global Diamond Mining Market is poised to register a 4.3% CAGR from $8.4 Billion in 2024 to $10.8 Billion in 2030.

The global Diamond Mining Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (Gem Grade, Industrial Grade).

An Introduction to Global Diamond Mining Market in 2024

The market for diamond mining is witnessing steady growth, driven by the enduring demand for diamonds in jewelry, industrial applications, and technological innovations. Key trends shaping the future of the industry include advancements in mining technology, exploration techniques, and sustainable practices to meet the evolving needs of the diamond market while addressing environmental concerns and social responsibilities. Mining companies are investing in innovative technologies such as automated drilling, autonomous haulage systems, and remote sensing to improve efficiency, safety, and environmental performance in diamond extraction and processing. Additionally, there is a growing emphasis on responsible sourcing, ethical mining practices, and community engagement in diamond mining operations, driven by consumer awareness, regulatory requirements, and industry initiatives such as the Kimberley Process Certification Scheme. Moreover, advancements in geophysical surveys, geological modeling, and data analytics are driving innovation in diamond exploration, enabling the discovery of new diamond deposits and the optimization of resource extraction and recovery processes. Furthermore, collaborations between mining companies, governments, and local communities are shaping the development of sustainable mining practices, environmental stewardship programs, and social development initiatives that promote responsible resource management, economic growth, and inclusive development in diamond-producing regions. Overall, the future of diamond mining lies in continuous innovation, collaboration, and sustainability initiatives to address emerging market trends, technological challenges, and stakeholder expectations while ensuring the long-term viability and value of the diamond industry.

Diamond Mining Market Competitive Landscape

The market report analyses the leading companies in the industry including Anglo American Plc, Arctic Canadian Diamond Co. Ltd, ENDIAMA EP, Gem Diamonds Ltd, Lucara Diamond Corp, Petra Diamonds Ltd, PJSC ALROSA, Rio Tinto Ltd, RioZim Ltd, Zimbabwe Consolidated Diamond Co. Pvt. Ltd.

Diamond Mining Market Dynamics

Diamond Mining Market Trend: Increasing Demand for Ethically Sourced Diamonds

A prominent trend in the Diamond Mining market is the increasing demand for ethically sourced diamonds. Consumers are becoming more socially and environmentally conscious, leading to a growing preference for diamonds that are mined and processed in ways that adhere to ethical and sustainable practices. This trend is driven by factors such as concerns about human rights violations, environmental degradation, and the impact of mining on local communities. As a result, there's a rising market demand for diamonds that are certified as conflict-free, responsibly sourced, and traceable throughout the supply chain. Diamond mining companies are responding by implementing ethical sourcing initiatives, investing in community development projects, and obtaining certifications such as the Kimberley Process Certification Scheme and Responsible Jewellery Council certification. By meeting consumer expectations for ethically sourced diamonds, companies can enhance their brand reputation, build trust with customers, and capitalize on the growing market trend.

Diamond Mining Market Driver: Growth in Luxury Goods and Jewelry Markets

A significant driver in the Diamond Mining market is the growth in luxury goods and jewelry markets worldwide. Diamonds are widely sought after for their beauty, rarity, and symbolic value, making them a key component in luxury jewelry and high-end accessories. As disposable incomes rise and consumer preferences shift towards luxury and aspirational products, there's an increasing demand for diamonds across various demographics, including affluent consumers and emerging middle-class populations. This driver is fueled by factors such as urbanization, globalization, and the growing influence of social media and celebrity culture, which drive demand for luxury goods and status symbols. As jewelry brands and retailers seek to meet market demand and cater to evolving consumer tastes, there's a corresponding market demand for high-quality diamonds sourced from reputable mining operations, driving growth and investment in the diamond mining industry.

Diamond Mining Market Opportunity: Adoption of Sustainable Mining Practices

A promising opportunity within the Diamond Mining market lies in the adoption of sustainable mining practices. Opportunities exist for diamond mining companies to implement environmentally responsible methods, reduce carbon footprint, and minimize ecological impact throughout the mining lifecycle, from exploration to closure and rehabilitation. Additionally, there's potential for growth in the development of innovative technologies and processes that improve energy efficiency, water management, and waste reduction in diamond mining operations. By embracing sustainability initiatives, mining companies can mitigate environmental risks, comply with regulatory requirements, and enhance stakeholder engagement. Moreover, adopting sustainable practices can lead to cost savings, operational efficiencies, and long-term viability of mining operations. As consumers and investors increasingly prioritize sustainability, companies that demonstrate a commitment to responsible mining practices can differentiate themselves in the market, attract socially responsible investors, and capitalize on emerging market opportunities.

Diamond Mining Market Share Analysis: The Gem Grade generated the highest revenue in 2024

The largest segment in the Diamond Mining Market is the Gem Grade category. Gem-grade diamonds are highly valued for their exceptional clarity, color, and brilliance, making them sought after for use in jewelry and luxury goods. These diamonds undergo rigorous sorting and grading processes to ensure they meet stringent quality standards set by the gemstone industry. Gem-grade diamonds command premium prices in the market due to their rarity and aesthetic appeal, driving significant revenue for diamond mining companies. Additionally, the demand for gem-grade diamonds remains consistently strong, fueled by consumer preferences for luxury jewelry items and the enduring appeal of diamonds as symbols of love, status, and prestige. Accordingly, diamond mining operations often prioritize the extraction of gem-grade diamonds to capitalize on their high market value and profitability. With continued demand from the global jewelry market and emerging economies, the gem-grade segment is expected to maintain its dominance as the largest segment in the Diamond Mining Market.

Diamond Mining Market Report Segmentation

By Type

Gem Grade

Industrial Grade

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Diamond Mining Companies Profiled in the Market Study

Anglo American Plc

Arctic Canadian Diamond Co. Ltd

ENDIAMA EP

Gem Diamonds Ltd

Lucara Diamond Corp

Petra Diamonds Ltd

PJSC ALROSA

Rio Tinto Ltd

RioZim Ltd

Zimbabwe Consolidated Diamond Co. Pvt. Ltd

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Diamond Mining Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Diamond Mining Market Size Outlook, $ Million, 2021 to 2030

3.2 Diamond Mining Market Outlook by Type, $ Million, 2021 to 2030

3.3 Diamond Mining Market Outlook by Product, $ Million, 2021 to 2030

3.4 Diamond Mining Market Outlook by Application, $ Million, 2021 to 2030

3.5 Diamond Mining Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Diamond Mining Industry

4.2 Key Market Trends in Diamond Mining Industry

4.3 Potential Opportunities in Diamond Mining Industry

4.4 Key Challenges in Diamond Mining Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Diamond Mining Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Diamond Mining Market Outlook by Segments

7.1 Diamond Mining Market Outlook by Segments, $ Million, 2021- 2030

By Type

Gem Grade

Industrial Grade

8 North America Diamond Mining Market Analysis and Outlook To 2030

8.1 Introduction to North America Diamond Mining Markets in 2024

8.2 North America Diamond Mining Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Diamond Mining Market size Outlook by Segments, 2021-2030

By Type

Gem Grade

Industrial Grade

9 Europe Diamond Mining Market Analysis and Outlook To 2030

9.1 Introduction to Europe Diamond Mining Markets in 2024

9.2 Europe Diamond Mining Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Diamond Mining Market Size Outlook by Segments, 2021-2030

By Type

Gem Grade

Industrial Grade

10 Asia Pacific Diamond Mining Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Diamond Mining Markets in 2024

10.2 Asia Pacific Diamond Mining Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Diamond Mining Market size Outlook by Segments, 2021-2030

By Type

Gem Grade

Industrial Grade

11 South America Diamond Mining Market Analysis and Outlook To 2030

11.1 Introduction to South America Diamond Mining Markets in 2024

11.2 South America Diamond Mining Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Diamond Mining Market size Outlook by Segments, 2021-2030

By Type

Gem Grade

Industrial Grade

12 Middle East and Africa Diamond Mining Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Diamond Mining Markets in 2024

12.2 Middle East and Africa Diamond Mining Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Diamond Mining Market size Outlook by Segments, 2021-2030

By Type

Gem Grade

Industrial Grade

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Anglo American Plc

Arctic Canadian Diamond Co. Ltd

ENDIAMA EP

Gem Diamonds Ltd

Lucara Diamond Corp

Petra Diamonds Ltd

PJSC ALROSA

Rio Tinto Ltd

RioZim Ltd

Zimbabwe Consolidated Diamond Co. Pvt. Ltd

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

Gem Grade

Industrial Grade

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)