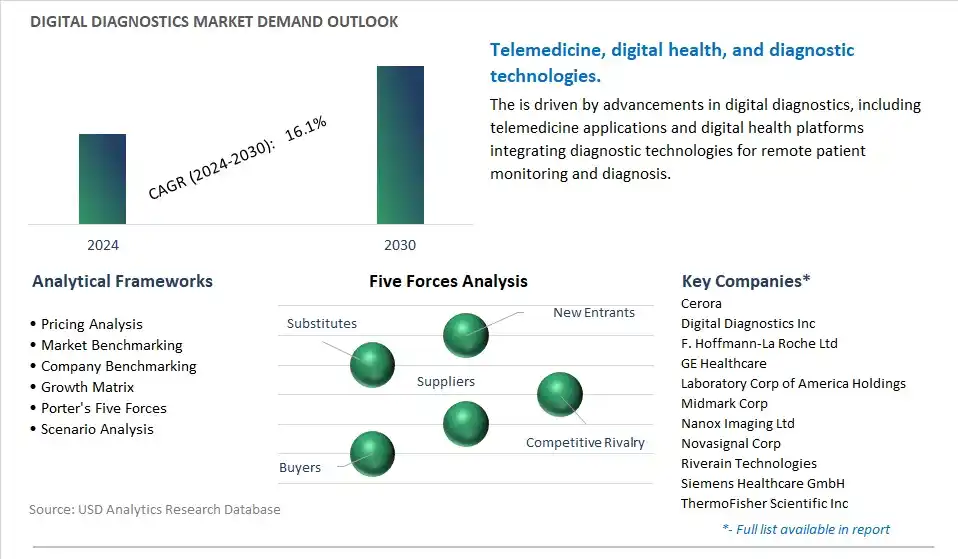

Digital Diagnostics Market is estimated to increase at a Compounded Annual Growth Rate of 16.1% CAGR over the forecast period from 2024 to 2030

The Digital Diagnostics Market study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments- By Product (Hardware, Software, Services), By Diagnosis (Cardiology, Oncology, Neurology, Radiology, Pathology, Others), By End-User (Hospitals and Clinics, Clinical Laboratories, Others).

An Introduction to Digital Diagnostics Market in 2024

In 2024, the market for digital diagnostics addresses the transformative role of digital health technologies in revolutionizing diagnostic testing, disease detection, and patient care delivery, offering innovative solutions, software platforms, and digital health tools for remote monitoring, point-of-care testing, and personalized diagnostics. Digital diagnostics encompass a wide range of technologies including mobile health applications, wearable devices, telemedicine platforms, artificial intelligence (AI) algorithms, and cloud-based analytics, each designed to enable seamless integration of diagnostic data, facilitate real-time clinical decision-making, and empower patients to actively participate in their healthcare management. These digital solutions offer new opportunities for improving access to diagnostic services, optimizing resource utilization, and enhancing healthcare delivery efficiency in diverse clinical settings. With a focus on data security, interoperability, and regulatory compliance, digital diagnostics undergo validation studies, usability testing, and regulatory approval processes to ensure reliability, accuracy, and clinical validity of diagnostic results. Moreover, with advancements in sensor technology, remote monitoring capabilities, and AI-driven diagnostics, the digital diagnostics market continues to innovate, offering new diagnostic modalities, predictive analytics, and personalized medicine solutions for improving patient outcomes, reducing healthcare costs, and transforming the diagnostic landscape in the era of digital healthcare.

Market Trend: Integration of Artificial Intelligence and Machine Learning

A prominent trend in the digital diagnostics market is the integration of artificial intelligence (AI) and machine learning (ML) technologies. These advanced technologies enable digital diagnostic tools to analyze medical images, patient data, and diagnostic test results with greater speed, accuracy, and efficiency. AI and ML algorithms can assist healthcare professionals in interpreting diagnostic images, predicting disease progression, and identifying patterns in patient data that may indicate underlying health conditions. This trend is driven by the growing volume of healthcare data, advancements in computing power, and the need for more personalized and precise diagnostic solutions. As AI and ML continue to evolve, the integration of these technologies into digital diagnostics holds the potential to revolutionize healthcare delivery and improve patient outcomes.

Market Driver: Increasing Demand for Remote Monitoring and Telemedicine

A key driver for the digital diagnostics market is the increasing demand for remote monitoring and telemedicine solutions. With the rise of telehealth services and remote patient monitoring platforms, there is a growing need for digital diagnostic tools that enable healthcare providers to assess patients' health remotely. Digital diagnostics offer the flexibility and convenience of conducting diagnostic tests, analyzing results, and delivering medical advice to patients from a distance, reducing the need for in-person visits and improving access to healthcare services, especially in underserved or remote areas. This driver is fueled by factors such as the COVID-19 pandemic, which accelerated the adoption of telemedicine, as well as the aging population and the prevalence of chronic diseases, which require ongoing monitoring and management. As telemedicine continues to gain traction, the demand for digital diagnostics tools that support remote healthcare delivery is expected to grow, driving market expansion in the segment.

Market Opportunity: Development of Point-of-Care Diagnostic Devices

An opportunity for innovation and market growth in the digital diagnostics market lies in the development of point-of-care (POC) diagnostic devices. POC diagnostic devices enable rapid and accurate diagnosis of medical conditions at the patient's bedside, in clinics, or in other non-laboratory settings. These compact and portable devices leverage digital technology to perform diagnostic tests, analyze samples, and deliver results in real-time, enabling timely clinical decision-making and treatment initiation. With the increasing focus on early disease detection, rapid diagnosis, and decentralized healthcare delivery, there is a growing demand for POC diagnostic devices that offer convenience, accessibility, and reliability. Manufacturers can capitalize on this opportunity by developing digital POC diagnostic devices for a wide range of applications, including infectious disease testing, cardiac biomarker analysis, and chronic disease monitoring. By addressing unmet clinical needs and providing healthcare providers with innovative POC diagnostic solutions, companies can drive market growth and improve patient care outcomes in the digital diagnostics segment.

Digital Diagnostics Market Share Analysis: Software

The Software segment within the Digital Diagnostics market is experiencing rapid growth due to several factors contributing to the increasing adoption of digital solutions for diagnosis and healthcare management. Digital diagnostic software encompasses a wide range of applications, including medical imaging software, diagnostic algorithms, electronic health record (EHR) systems, telemedicine platforms, and healthcare analytics tools. These software solutions offer several advantages, such as improved efficiency, accuracy, and accessibility of diagnostic processes, enabling healthcare providers to make informed decisions and deliver better patient care outcomes. In particular, advancements in artificial intelligence (AI) and machine learning algorithms have revolutionized medical imaging interpretation, facilitating early detection, diagnosis, and treatment planning across various specialties including cardiology, oncology, neurology, radiology, and pathology. Moreover, the integration of digital diagnostic software with electronic health records and clinical decision support systems enhances care coordination, patient engagement, and population health management initiatives. With the increasing adoption of electronic medical records and the growing demand for remote monitoring and telemedicine services, the software segment is poised for significant growth in the Digital Diagnostics market. Hospitals and clinics, clinical laboratories, and other healthcare facilities are increasingly investing in digital diagnostic software to streamline workflows, improve diagnostic accuracy, and enhance patient outcomes in an evolving healthcare landscape.

Digital Diagnostics Competitive Analysis

The market research study provides in-depth insights into leading companies including the SWOT analyses, product profile, financial details, and recent developments acrossCerora, Digital Diagnostics Inc, F. Hoffmann-La Roche Ltd, GE Healthcare, Laboratory Corp of America Holdings, Midmark Corp, Nanox Imaging Ltd, Novasignal Corp, Riverain Technologies, Siemens Healthcare GmbH, ThermoFisher Scientific Inc, Vuno Inc

Digital Diagnostics Market Segmentation

By Product

Hardware

Software

Services

By Diagnosis

Cardiology

Oncology

Neurology

Radiology

Pathology

Others

By End-User

Hospitals and Clinics

Clinical Laboratories

Others

Geographical Analysis

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Digital Diagnostics Market Companies

Cerora

Digital Diagnostics Inc

F. Hoffmann-La Roche Ltd

GE Healthcare

Laboratory Corp of America Holdings

Midmark Corp

Nanox Imaging Ltd

Novasignal Corp

Riverain Technologies

Siemens Healthcare GmbH

ThermoFisher Scientific Inc

Vuno Inc

Reasons to Buy the Digital Diagnostics Market Study

• Deepen your industry insights and navigate uncertainties for strategy formulation, CAPEX, and Operational decisions

• Gain access to detailed insights on the Digital Diagnostics Market, encompassing current market size, growth trends, and forecasts till 2030.

• Access detailed competitor analysis, enabling competitive advantage through a thorough understanding of market players, strategies, and potential differentiation opportunities

• Stay ahead of the curve with insights on technological advancements, innovations, and upcoming trends

• Identify lucrative investment avenues and expansion opportunities within the Digital Diagnostics Market industry, guided by robust, data-backed analysis.

• Understand regional and global markets through country-wise analysis, regional market potential, regulatory nuances, and dynamics

• Execute strategies with confidence and speed through information, analytics, and insights on the industry value chain

• Corporate leaders, strategists, financial experts, shareholders, asset managers, and governmental representatives can make long-term planning scenarios and build an integrated and timely understanding of market dynamics

• Benefit from tailored solutions and expert consultation based on report insights, providing personalized strategies aligned with specific business needs.

TABLE OF CONTENTS

1 Introduction to 2024 Digital Diagnostics Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Digital Diagnostics Market Size Outlook, $ Million, 2021 to 2030

3.2 Digital Diagnostics Market Outlook by Type, $ Million, 2021 to 2030

3.3 Digital Diagnostics Market Outlook by Product, $ Million, 2021 to 2030

3.4 Digital Diagnostics Market Outlook by Application, $ Million, 2021 to 2030

3.5 Digital Diagnostics Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Digital Diagnostics Industry

4.2 Key Market Trends in Digital Diagnostics Industry

4.3 Potential Opportunities in Digital Diagnostics Industry

4.4 Key Challenges in Digital Diagnostics Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Digital Diagnostics Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Digital Diagnostics Market Outlook by Segments

7.1 Digital Diagnostics Market Outlook by Segments, $ Million, 2021- 2030

By Product

Hardware

Software

Services

By Diagnosis

Cardiology

Oncology

Neurology

Radiology

Pathology

Others

By End-User

Hospitals and Clinics

Clinical Laboratories

Others

8 North America Digital Diagnostics Market Analysis and Outlook To 2030

8.1 Introduction to North America Digital Diagnostics Markets in 2024

8.2 North America Digital Diagnostics Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Digital Diagnostics Market size Outlook by Segments, 2021-2030

By Product

Hardware

Software

Services

By Diagnosis

Cardiology

Oncology

Neurology

Radiology

Pathology

Others

By End-User

Hospitals and Clinics

Clinical Laboratories

Others

9 Europe Digital Diagnostics Market Analysis and Outlook To 2030

9.1 Introduction to Europe Digital Diagnostics Markets in 2024

9.2 Europe Digital Diagnostics Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Digital Diagnostics Market Size Outlook by Segments, 2021-2030

By Product

Hardware

Software

Services

By Diagnosis

Cardiology

Oncology

Neurology

Radiology

Pathology

Others

By End-User

Hospitals and Clinics

Clinical Laboratories

Others

10 Asia Pacific Digital Diagnostics Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Digital Diagnostics Markets in 2024

10.2 Asia Pacific Digital Diagnostics Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Digital Diagnostics Market size Outlook by Segments, 2021-2030

By Product

Hardware

Software

Services

By Diagnosis

Cardiology

Oncology

Neurology

Radiology

Pathology

Others

By End-User

Hospitals and Clinics

Clinical Laboratories

Others

11 South America Digital Diagnostics Market Analysis and Outlook To 2030

11.1 Introduction to South America Digital Diagnostics Markets in 2024

11.2 South America Digital Diagnostics Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Digital Diagnostics Market size Outlook by Segments, 2021-2030

By Product

Hardware

Software

Services

By Diagnosis

Cardiology

Oncology

Neurology

Radiology

Pathology

Others

By End-User

Hospitals and Clinics

Clinical Laboratories

Others

12 Middle East and Africa Digital Diagnostics Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Digital Diagnostics Markets in 2024

12.2 Middle East and Africa Digital Diagnostics Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Digital Diagnostics Market size Outlook by Segments, 2021-2030

By Product

Hardware

Software

Services

By Diagnosis

Cardiology

Oncology

Neurology

Radiology

Pathology

Others

By End-User

Hospitals and Clinics

Clinical Laboratories

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

List of Companies

Cerora

Digital Diagnostics Inc

F. Hoffmann-La Roche Ltd

GE Healthcare

Laboratory Corp of America Holdings

Midmark Corp

Nanox Imaging Ltd

Novasignal Corp

Riverain Technologies

Siemens Healthcare GmbH

ThermoFisher Scientific Inc

Vuno Inc

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Product

Hardware

Software

Services

By Diagnosis

Cardiology

Oncology

Neurology

Radiology

Pathology

Others

By End-User

Hospitals and Clinics

Clinical Laboratories

Others

Countries Analyzed

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)