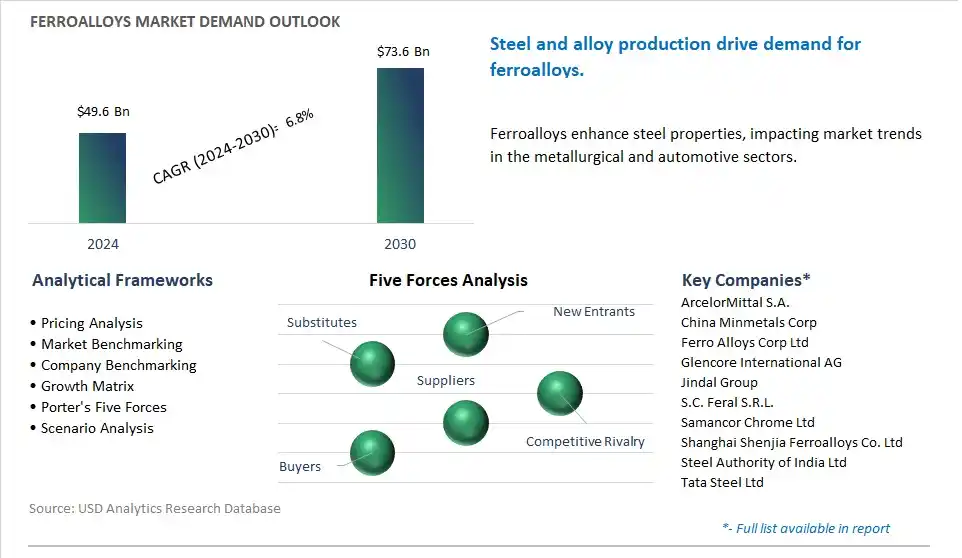

The global Ferroalloys Market is poised to register a 6.8% CAGR from $49.6 Billion in 2024 to $73.6 Billion in 2030.

The global Ferroalloys Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Product (Ferrochrome, Ferromanganese, Ferro Silico Manganese, Ferrosilicon), By Application (Carbon & Low Alloy Steel, Stainless Steel, Alloy Steel, Cast Iron, Others).

An Introduction to Global Ferroalloys Market in 2024

The ferroalloys market is witnessing robust growth driven by the increasing demand for alloying elements such as chromium, manganese, silicon, and molybdenum in steelmaking, foundry, and metallurgical industries. Key trends shaping the future of the industry include the rising demand for high-performance alloys with specific composition, purity, and metallurgical properties tailored for different steel grades, casting processes, and end-use applications. As steel producers seek to improve product quality, strength, and corrosion resistance, there's a growing need for ferroalloys that offer precise control over alloy composition, inclusion content, and microstructure while optimizing alloy recovery and refining processes. Moreover, advancements in ferroalloy production technologies, including smelting, alloying, and casting techniques, are driving market expansion by improving energy efficiency, process flexibility, and environmental performance of ferroalloy manufacturing facilities. Additionally, the growing adoption of ferroalloys in specialty steel, stainless steel, and superalloy applications is fueling demand for innovative alloys and alloying agents that enhance mechanical properties, heat resistance, and weldability of steel products in automotive, aerospace, and construction sectors. Furthermore, the integration of ferroalloys with additive manufacturing, powder metallurgy, and advanced steelmaking processes is driving innovation and market growth in the ferroalloys industry, enabling the development of next-generation materials and alloys for high-performance engineering applications and advanced manufacturing technologies.

Ferroalloys Market Competitive Landscape

The market report analyses the leading companies in the industry including ArcelorMittal S.A., China Minmetals Corp, Ferro Alloys Corp Ltd, Glencore International AG, Jindal Group, S.C. Feral S.R.L., Samancor Chrome Ltd, Shanghai Shenjia Ferroalloys Co. Ltd, Steel Authority of India Ltd, Tata Steel Ltd.

Ferroalloys Market Dynamics

Ferroalloys Market Trend: Growing Demand for High-performance Steel Alloys Drives Ferroalloys Market Growth

One prominent trend in the ferroalloys market is the growing demand for high-performance steel alloys in various industrial sectors. Ferroalloys, such as ferromanganese, ferrosilicon, and ferrochrome, are essential additives used in the production of specialty steels and alloys with specific properties such as corrosion resistance, heat resistance, and strength. With increasing urbanization, infrastructure development, and industrialization worldwide, there is a rising demand for steel products in construction, automotive manufacturing, aerospace, energy, and infrastructure sectors. This drives the need for ferroalloys as key components in the production of specialty steels used in critical applications such as bridges, buildings, pipelines, automotive components, and machinery, contributing to the market trend towards increased consumption of ferroalloys.

Ferroalloys Market Driver: Growth of Steel Industry and Infrastructure Development Stimulates Ferroalloys Market Expansion

The growth of the ferroalloys market is driven by the expansion of the steel industry and infrastructure development projects globally. Steel remains a fundamental material in construction, manufacturing, and infrastructure sectors due to its versatility, durability, and recyclability. As countries invest in infrastructure upgrades, urban development projects, and transportation networks, there is a corresponding increase in demand for steel products and alloys to support construction activities, machinery manufacturing, and transportation infrastructure. Ferroalloys play a crucial role in enhancing the performance and properties of steel, enabling the production of high-strength, corrosion-resistant, and heat-resistant alloys that meet the stringent requirements of modern industrial applications. The growth of the steel industry and infrastructure development projects serves as a key driver propelling the demand for ferroalloys in the global market.

Ferroalloys Market Opportunity: Diversification into Specialty Ferroalloys and Alloy Formulations

A potential opportunity in the ferroalloys market lies in the diversification into specialty ferroalloys and alloy formulations to meet evolving customer needs and industry requirements. While traditional ferroalloys such as ferromanganese, ferrosilicon, and ferrochrome remain essential components in steelmaking, there is a growing demand for specialty ferroalloys tailored to specific applications and end-user requirements. Manufacturers can capitalize on this opportunity by developing innovative ferroalloy formulations with customized alloy compositions, particle sizes, and impurity levels to optimize steel performance and processing characteristics. Additionally, there is an opportunity to explore niche markets and emerging applications such as electrical steels, high-strength alloys, and specialty stainless steels, where specialized ferroalloys can provide added value and competitive advantage. By expanding their product portfolios and offering specialized ferroalloy solutions, manufacturers can enhance their market presence, address customer demands, and capitalize on growth opportunities in the global ferroalloys market.

Ferroalloys Market Share Analysis: Ferrosilicon segment generated the highest revenue in the industry

Ferrosilicon is the largest segment in the Ferroalloys Market due to diverse key reasons. Ferrosilicon is a ferroalloy composed primarily of iron and silicon, with varying concentrations of other elements such as manganese and calcium. It is widely used in steelmaking as a deoxidizer, desulfurizing agent, and alloying element to enhance the mechanical properties and performance of steel. Additionally, ferrosilicon is utilized in the production of various other alloys, including stainless steel, cast iron, and specialty alloys, due to its ability to impart desirable properties such as hardness, corrosion resistance, and thermal stability. In addition, ferrosilicon finds applications in the manufacturing of silicon-based chemicals, abrasives, and refractory materials, further contributing to its demand across diverse industrial sectors. Further, the abundance of raw materials and cost-effective production processes make ferrosilicon a preferred choice for steelmakers and alloy producers worldwide. With its essential role in steelmaking and versatile applications in various industries, ferrosilicon maintains its dominance as the largest segment in the Ferroalloys Market.

Ferroalloys Market Share Analysis: Stainless Steel Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The stainless steel segment is the fastest-growing segment in the Ferroalloys Market due to diverse key factors propelling its rapid expansion. Stainless steel is widely used in various industries such as automotive, construction, aerospace, and household appliances due to its exceptional corrosion resistance, strength, and aesthetic appeal. Ferroalloys play a crucial role in stainless steel production as alloying agents, providing essential elements such as chromium, nickel, and molybdenum that impart specific properties to the final steel product. Additionally, the increasing demand for stainless steel in applications requiring high durability, hygiene standards, and aesthetic appearance drives the growth of the segment. With rising urbanization, infrastructure development, and consumer preferences for modern and sustainable materials, the demand for stainless steel continues to grow globally. In addition, advancements in stainless steel manufacturing technologies, along with innovations in alloy compositions and production processes, further support the growth of the segment. Further, the growing emphasis on environmental sustainability and energy efficiency favors the use of stainless steel in green building projects, renewable energy systems, and electric vehicles, driving its demand and the growth of the stainless steel segment in the Ferroalloys Market.

Ferroalloys Market Report Segmentation

By Product

Ferrochrome

Ferromanganese

Ferro Silico Manganese

Ferrosilicon

By Application

Carbon & Low Alloy Steel

Stainless Steel

Alloy Steel

Cast Iron

Others

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Ferroalloys Companies Profiled in the Market Study

ArcelorMittal S.A.

China Minmetals Corp

Ferro Alloys Corp Ltd

Glencore International AG

Jindal Group

S.C. Feral S.R.L.

Samancor Chrome Ltd

Shanghai Shenjia Ferroalloys Co. Ltd

Steel Authority of India Ltd

Tata Steel Ltd

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Ferroalloys Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Ferroalloys Market Size Outlook, $ Million, 2021 to 2030

3.2 Ferroalloys Market Outlook by Type, $ Million, 2021 to 2030

3.3 Ferroalloys Market Outlook by Product, $ Million, 2021 to 2030

3.4 Ferroalloys Market Outlook by Application, $ Million, 2021 to 2030

3.5 Ferroalloys Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Ferroalloys Industry

4.2 Key Market Trends in Ferroalloys Industry

4.3 Potential Opportunities in Ferroalloys Industry

4.4 Key Challenges in Ferroalloys Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Ferroalloys Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Ferroalloys Market Outlook by Segments

7.1 Ferroalloys Market Outlook by Segments, $ Million, 2021- 2030

By Product

Ferrochrome

Ferromanganese

Ferro Silico Manganese

Ferrosilicon

By Application

Carbon & Low Alloy Steel

Stainless Steel

Alloy Steel

Cast Iron

Others

8 North America Ferroalloys Market Analysis and Outlook To 2030

8.1 Introduction to North America Ferroalloys Markets in 2024

8.2 North America Ferroalloys Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Ferroalloys Market size Outlook by Segments, 2021-2030

By Product

Ferrochrome

Ferromanganese

Ferro Silico Manganese

Ferrosilicon

By Application

Carbon & Low Alloy Steel

Stainless Steel

Alloy Steel

Cast Iron

Others

9 Europe Ferroalloys Market Analysis and Outlook To 2030

9.1 Introduction to Europe Ferroalloys Markets in 2024

9.2 Europe Ferroalloys Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Ferroalloys Market Size Outlook by Segments, 2021-2030

By Product

Ferrochrome

Ferromanganese

Ferro Silico Manganese

Ferrosilicon

By Application

Carbon & Low Alloy Steel

Stainless Steel

Alloy Steel

Cast Iron

Others

10 Asia Pacific Ferroalloys Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Ferroalloys Markets in 2024

10.2 Asia Pacific Ferroalloys Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Ferroalloys Market size Outlook by Segments, 2021-2030

By Product

Ferrochrome

Ferromanganese

Ferro Silico Manganese

Ferrosilicon

By Application

Carbon & Low Alloy Steel

Stainless Steel

Alloy Steel

Cast Iron

Others

11 South America Ferroalloys Market Analysis and Outlook To 2030

11.1 Introduction to South America Ferroalloys Markets in 2024

11.2 South America Ferroalloys Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Ferroalloys Market size Outlook by Segments, 2021-2030

By Product

Ferrochrome

Ferromanganese

Ferro Silico Manganese

Ferrosilicon

By Application

Carbon & Low Alloy Steel

Stainless Steel

Alloy Steel

Cast Iron

Others

12 Middle East and Africa Ferroalloys Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Ferroalloys Markets in 2024

12.2 Middle East and Africa Ferroalloys Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Ferroalloys Market size Outlook by Segments, 2021-2030

By Product

Ferrochrome

Ferromanganese

Ferro Silico Manganese

Ferrosilicon

By Application

Carbon & Low Alloy Steel

Stainless Steel

Alloy Steel

Cast Iron

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

ArcelorMittal S.A.

China Minmetals Corp

Ferro Alloys Corp Ltd

Glencore International AG

Jindal Group

S.C. Feral S.R.L.

Samancor Chrome Ltd

Shanghai Shenjia Ferroalloys Co. Ltd

Steel Authority of India Ltd

Tata Steel Ltd

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Product

Ferrochrome

Ferromanganese

Ferro Silico Manganese

Ferrosilicon

By Application

Carbon & Low Alloy Steel

Stainless Steel

Alloy Steel

Cast Iron

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)