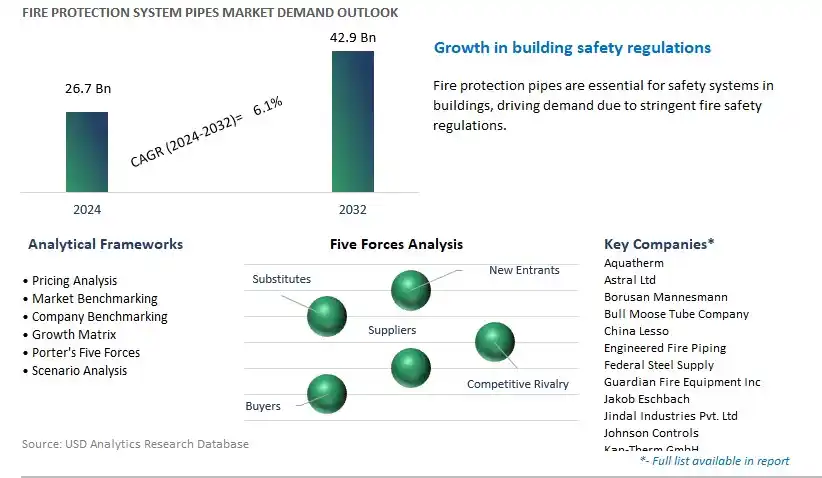

Global Fire Protection System Pipes Market Size is valued at $26.7 Billion in 2024 and is forecast to register a growth rate (CAGR) of 6.1% to reach $42.9 Billion by 2032.

The global Fire Protection System Pipes Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (Seamless Pipes, Welded Pipes), By Material (Steel, CPVC, Copper, Others), By Application (Fire Suppression System, Fire Sprinkler System), By End-User (Residential, Industrial, Commercial).

An Introduction to Fire Protection System Pipes Market in 2024

Fire protection system pipes play a critical role in safeguarding lives and property by delivering water or firefighting agents to suppress fires effectively. In 2024, the market for fire protection system pipes is witnessing robust growth driven by stringent regulatory standards, increasing awareness of fire safety, and infrastructure development activities. These pipes are typically constructed from materials such as steel, copper, or plastic, selected based on factors such as pressure rating, corrosion resistance, and installation requirements. Further, advancements in pipe manufacturing processes, including corrosion-resistant coatings and pre-fabrication techniques, enhance system reliability and reduce maintenance costs over the operational lifespan. With growing investments in commercial, residential, and industrial projects worldwide, the demand for fire protection system pipes is expected to remain buoyant, ensuring comprehensive fire protection measures in built environments.

Fire Protection System Pipes Market Competitive Landscape

The market report analyses the leading companies in the industry including Aquatherm, Astral Ltd, Borusan Mannesmann, Bull Moose Tube Company, China Lesso, Engineered Fire Piping, Federal Steel Supply, Guardian Fire Equipment Inc, Jakob Eschbach, Jindal Industries Pvt. Ltd, Johnson Controls, Kan-Therm GmbH, Mercedes Textiles, Minimax, Newage Fire Protection Industries Pvt. Ltd, Octal Steel, Rawhide Fire Hose LLC, Simona AG, Tata Steel, Tpmcsteel, Triangle Fire Systems, Weifang East Steel Pipe, Zekelman Industries, Zinchitalia Spa, and others.

Fire Protection System Pipes Market Dynamics

Market Trend: Increasing Adoption of Advanced Materials in Fire Protection System Pipes

A prominent trend in the fire protection system pipes market is the increasing adoption of advanced materials for enhanced performance and durability. Fire protection system pipes are critical components in building infrastructure for conveying water, foam, or other fire suppression agents to control and extinguish fires. With advancements in material science and engineering, there is a growing demand for fire protection system pipes made from corrosion-resistant materials such as stainless steel, CPVC (Chlorinated Polyvinyl Chloride), and PEX (Cross-linked Polyethylene). These advanced materials offer superior resistance to corrosion, high temperatures, and chemical degradation, ensuring reliable performance and extended service life in fire protection applications. This trend reflects the industry's response to evolving safety standards, regulatory requirements, and the need for robust fire suppression systems in commercial, industrial, and residential buildings.

Market Driver: Stringent Fire Safety Regulations and Building Codes

A key driver fueling the demand for fire protection system pipes is the implementation of stringent fire safety regulations and building codes worldwide. Governments and regulatory bodies mandate the installation of fire protection systems in buildings to safeguard lives, property, and assets from the risk of fire-related incidents. Fire protection system pipes play a crucial role in these systems by providing a reliable means of delivering water or fire suppression agents to fire sprinklers, hydrants, and standpipes. Additionally, the enforcement of fire safety standards, such as NFPA (National Fire Protection Association) codes, FM Global standards, and local building codes, drives investments in fire protection infrastructure and fuels market growth for fire protection system pipes. The commitment to ensuring fire safety in buildings and facilities creates a consistent demand for high-quality, code-compliant piping solutions, supporting market expansion and innovation in fire protection technologies.

Market Opportunity: Integration of Smart Technologies and IoT in Fire Protection Systems

Amidst the evolving landscape of the fire protection system pipes market, there exists a significant opportunity for integration of smart technologies and IoT (Internet of Things) in fire protection systems. Manufacturers and system integrators can capitalize on this opportunity by developing intelligent fire protection solutions that leverage sensor technology, data analytics, and connectivity to enhance detection, monitoring, and response capabilities. Smart fire protection systems can provide real-time alerts, remote monitoring, and predictive maintenance, improving overall system reliability and effectiveness in detecting and suppressing fires. By embracing innovation in smart technologies, companies can offer differentiated solutions that meet the evolving needs of building owners, facility managers, and fire safety professionals for proactive fire protection measures. This opportunity aligns with the industry's focus on leveraging digitalization and connectivity to enhance safety, efficiency, and sustainability in fire protection systems, driving market growth and competitiveness in the global fire protection system pipes market.

Fire Protection System Pipes Market Share Analysis: Seamless Pipes is poised to register the fastest CAGR over the forecast period

Seamless pipes are expected to be the largest and fastest-growing segment in the Fire Protection System Pipes Market. Seamless pipes are manufactured through a process that involves the extrusion of steel to create a solid, continuous tube without any welded seams. This manufacturing method results in a pipe that has a uniform structure and is free from any potential weak points or defects that could be present in welded pipes. Consequently, seamless pipes offer superior strength, durability, and resistance to high pressure, making them highly suitable for critical fire protection applications where reliability is paramount. Additionally, the seamless construction minimizes the risk of leaks and failures, ensuring the integrity of fire suppression systems. The increasing awareness of fire safety regulations and the demand for robust fire protection systems in various industries, including residential, commercial, and industrial sectors, further drive the preference for seamless pipes. As a result, seamless pipes are increasingly being adopted for their enhanced performance, safety, and long-term reliability in fire protection systems.

Fire Protection System Pipes Market Share Analysis: CPVC Pipes is poised to register the fastest CAGR over the forecast period

CPVC (Chlorinated Polyvinyl Chloride) pipes are emerging as the fastest-growing segment in the Fire Protection System Pipes Market by material. The rapid growth of CPVC pipes can be attributed to potential advantages they offer over traditional materials like steel and copper. CPVC pipes are known for their excellent corrosion resistance, making them highly durable and suitable for a wide range of environmental conditions, including both hot and cold water systems. Unlike steel pipes, CPVC does not rust, scale, or pit over time, which significantly extends the lifespan of the fire protection system and reduces maintenance costs. Additionally, CPVC pipes are lightweight, easy to handle, and simpler to install, which translates to lower labor costs and faster project completion times. They also possess superior hydraulic performance due to their smoother internal surface, which reduces friction and enhances water flow. Moreover, CPVC pipes are inherently resistant to combustion, and their chemical resistance ensures they do not degrade when exposed to harsh substances. These attributes, combined with increasing regulatory approvals and certifications for CPVC pipes in fire protection applications, make them a preferred choice in the industry, driving their fast adoption and market growth. The rising awareness of fire safety and the need for cost-effective, reliable fire protection solutions further bolster the demand for CPVC pipes, positioning them as a leading material in the market.

Fire Protection System Pipes Market Share Analysis: Fire Sprinkler System is poised to register the fastest CAGR over the forecast period

The Fire Sprinkler System segment is the largest and fastest-growing application in the Fire Protection System Pipes Market. Fire sprinkler systems are a critical component in building safety protocols, designed to automatically detect and suppress fires, thereby minimizing damage and saving lives. The increased implementation of stringent fire safety regulations and building codes globally has mandated the installation of fire sprinkler systems in residential, commercial, and industrial buildings. This regulatory push is a major catalyst for market growth. Furthermore, advancements in sprinkler system technologies, such as the development of more efficient and reliable sprinkler heads and control systems, have enhanced their effectiveness and reliability, making them a preferred choice for fire protection. The growing awareness among building owners and occupants about the benefits of installing fire sprinkler systems, including reduced insurance premiums and enhanced property protection, has also contributed to their widespread adoption. Additionally, the ongoing urbanization and construction boom, especially in emerging economies, have fuelled the demand for fire sprinkler systems. These systems are increasingly being incorporated into new construction projects as part of comprehensive fire safety solutions. As a result, the fire sprinkler system segment continues to dominate the market, driven by regulatory compliance, technological advancements, and heightened awareness of fire safety.

Fire Protection System Pipes Market Share Analysis: Commercial is poised to register the fastest CAGR over the forecast period

The Commercial segment is the fastest-growing end-user in the Fire Protection System Pipes Market. This rapid growth is driven by the increasing construction of commercial buildings, such as offices, shopping centers, hotels, hospitals, and educational institutions, which demand robust fire protection systems. The rise in commercial infrastructure projects globally, particularly in emerging economies, has significantly boosted the need for advanced fire protection solutions. Commercial buildings typically host a large number of occupants and valuable assets, making fire safety a critical concern. Consequently, stringent fire safety regulations and codes are enforced to ensure the protection of life and property, necessitating the installation of comprehensive fire protection systems, including pipes for sprinklers and suppression systems. Additionally, there is a growing awareness among commercial property owners about the importance of fire safety, leading to increased investments in high-quality fire protection systems. Technological advancements in fire protection equipment and the development of integrated building management systems that include fire safety components further drive the adoption of these systems in commercial buildings. The commercial sector's emphasis on minimizing operational disruptions and protecting assets from fire damage also fuels the demand for reliable and efficient fire protection solutions. As businesses strive to meet safety standards and enhance their resilience against fire hazards, the commercial segment continues to exhibit robust growth, outpacing other end-user segments in the fire protection system pipes market.

Fire Protection System Pipes Market

By Type

Seamless Pipes

Welded Pipes

By Material

Steel

CPVC

Copper

Others

By Application

Fire Suppression System

Fire Sprinkler System

By End-User

Residential

Industrial

CommercialCountries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Fire Protection System Pipes Companies Profiled in the Study

Aquatherm

Astral Ltd

Borusan Mannesmann

Bull Moose Tube Company

China Lesso

Engineered Fire Piping

Federal Steel Supply

Guardian Fire Equipment Inc

Jakob Eschbach

Jindal Industries Pvt. Ltd

Johnson Controls

Kan-Therm GmbH

Mercedes Textiles

Minimax

Newage Fire Protection Industries Pvt. Ltd

Octal Steel

Rawhide Fire Hose LLC

Simona AG

Tata Steel

Tpmcsteel

Triangle Fire Systems

Weifang East Steel Pipe

Zekelman Industries

Zinchitalia Spa

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Fire Protection System Pipes Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Fire Protection System Pipes Market Size Outlook, $ Million, 2021 to 2032

3.2 Fire Protection System Pipes Market Outlook by Type, $ Million, 2021 to 2032

3.3 Fire Protection System Pipes Market Outlook by Product, $ Million, 2021 to 2032

3.4 Fire Protection System Pipes Market Outlook by Application, $ Million, 2021 to 2032

3.5 Fire Protection System Pipes Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Fire Protection System Pipes Industry

4.2 Key Market Trends in Fire Protection System Pipes Industry

4.3 Potential Opportunities in Fire Protection System Pipes Industry

4.4 Key Challenges in Fire Protection System Pipes Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Fire Protection System Pipes Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Fire Protection System Pipes Market Outlook by Segments

7.1 Fire Protection System Pipes Market Outlook by Segments, $ Million, 2021- 2032

By Type

Seamless Pipes

Welded Pipes

By Material

Steel

CPVC

Copper

Others

By Application

Fire Suppression System

Fire Sprinkler System

By End-User

Residential

Industrial

Commercial

8 North America Fire Protection System Pipes Market Analysis and Outlook To 2032

8.1 Introduction to North America Fire Protection System Pipes Markets in 2024

8.2 North America Fire Protection System Pipes Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Fire Protection System Pipes Market size Outlook by Segments, 2021-2032

By Type

Seamless Pipes

Welded Pipes

By Material

Steel

CPVC

Copper

Others

By Application

Fire Suppression System

Fire Sprinkler System

By End-User

Residential

Industrial

Commercial

9 Europe Fire Protection System Pipes Market Analysis and Outlook To 2032

9.1 Introduction to Europe Fire Protection System Pipes Markets in 2024

9.2 Europe Fire Protection System Pipes Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Fire Protection System Pipes Market Size Outlook by Segments, 2021-2032

By Type

Seamless Pipes

Welded Pipes

By Material

Steel

CPVC

Copper

Others

By Application

Fire Suppression System

Fire Sprinkler System

By End-User

Residential

Industrial

Commercial

10 Asia Pacific Fire Protection System Pipes Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Fire Protection System Pipes Markets in 2024

10.2 Asia Pacific Fire Protection System Pipes Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Fire Protection System Pipes Market size Outlook by Segments, 2021-2032

By Type

Seamless Pipes

Welded Pipes

By Material

Steel

CPVC

Copper

Others

By Application

Fire Suppression System

Fire Sprinkler System

By End-User

Residential

Industrial

Commercial

11 South America Fire Protection System Pipes Market Analysis and Outlook To 2032

11.1 Introduction to South America Fire Protection System Pipes Markets in 2024

11.2 South America Fire Protection System Pipes Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Fire Protection System Pipes Market size Outlook by Segments, 2021-2032

By Type

Seamless Pipes

Welded Pipes

By Material

Steel

CPVC

Copper

Others

By Application

Fire Suppression System

Fire Sprinkler System

By End-User

Residential

Industrial

Commercial

12 Middle East and Africa Fire Protection System Pipes Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Fire Protection System Pipes Markets in 2024

12.2 Middle East and Africa Fire Protection System Pipes Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Fire Protection System Pipes Market size Outlook by Segments, 2021-2032

By Type

Seamless Pipes

Welded Pipes

By Material

Steel

CPVC

Copper

Others

By Application

Fire Suppression System

Fire Sprinkler System

By End-User

Residential

Industrial

Commercial

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Aquatherm

Astral Ltd

Borusan Mannesmann

Bull Moose Tube Company

China Lesso

Engineered Fire Piping

Federal Steel Supply

Guardian Fire Equipment Inc

Jakob Eschbach

Jindal Industries Pvt. Ltd

Johnson Controls

Kan-Therm GmbH

Mercedes Textiles

Minimax

Newage Fire Protection Industries Pvt. Ltd

Octal Steel

Rawhide Fire Hose LLC

Simona AG

Tata Steel

Tpmcsteel

Triangle Fire Systems

Weifang East Steel Pipe

Zekelman Industries

Zinchitalia Spa

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

Seamless Pipes

Welded Pipes

By Material

Steel

CPVC

Copper

Others

By Application

Fire Suppression System

Fire Sprinkler System

By End-User

Residential

Industrial

Commercial

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)