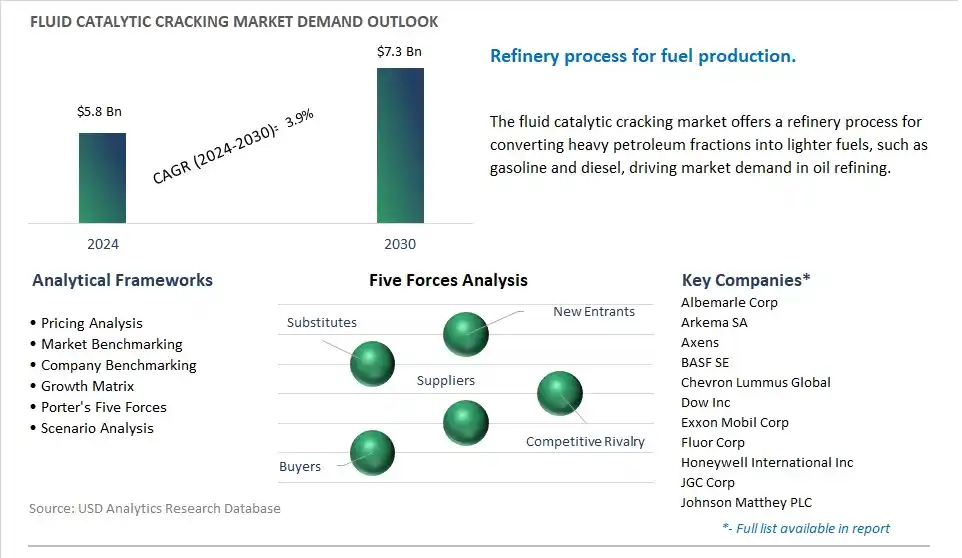

The global Fluid Catalytic Cracking Market is poised to register a 3.9% CAGR from $5.8 Billion in 2024 to $7.3 Billion in 2030.

The global Fluid Catalytic Cracking Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (Lanthanum Oxide, Zeolite), By Category (LVR-60, ORBIT-3600, CHV-1, RAG-7), By Technical Configuration (Side-By-Side, Stacked), By Application (Chemical, Others).

An Introduction to Global Fluid Catalytic Cracking Market in 2024

The future of the fluid catalytic cracking (FCC) market is influenced by trends such as petroleum refining, environmental regulations, and technological advancements driving innovation in catalyst formulations, process optimization, and product quality. Fluid catalytic cracking is a key process in petroleum refining used to convert heavy hydrocarbons into lighter, more valuable products such as gasoline, diesel, and olefins. Key trends shaping this market include advancements in catalyst technologies such as zeolites, rare earth metals, and additives to enhance cracking activity, selectivity, and stability in FCC units, the development of advanced process control strategies and simulation tools to optimize reactor performance, product yields, and energy efficiency in FCC operations, and the adoption of sustainable practices such as catalyst regeneration, emissions control, and waste minimization to reduce environmental impact and comply with regulatory requirements. As refineries strive to maximize production efficiency, upgrade product quality, and minimize environmental footprint, the demand for fluid catalytic cracking solutions that offer high performance, reliability, and sustainability is expected to drive market growth and stimulate further innovation in FCC technology and applications.

Fluid Catalytic Cracking Market Competitive Landscape

The market report analyses the leading companies in the industry including Albemarle Corp, Arkema SA, Axens, BASF SE, Chevron Lummus Global, Dow Inc, Exxon Mobil Corp, Fluor Corp, Honeywell International Inc, JGC Corp, Johnson Matthey PLC, Kuwait Catalyst Company, Magma Ceramics & Catalysts, McDermott International Inc, N.E. Chemcat Corp, Porocel Corp, Shell plc, W.R. Grace & Co., Yueyang Sciensun Chemical Co. Ltd.

Fluid Catalytic Cracking Market Dynamics

Fluid Catalytic Cracking Market Trend: Increasing Demand for Fluid Catalytic Cracking (FCC) Units in Petroleum Refining Industry

A significant trend in the fluid catalytic cracking market is the increasing demand for FCC units in the petroleum refining industry. With the growing global demand for transportation fuels and petrochemical feedstocks, refineries are expanding their capacity and upgrading their operations to meet market demands. FCC units play a crucial role in converting heavy hydrocarbon feedstocks into lighter, high-value products such as gasoline, diesel, and olefins through catalytic cracking processes. This is driving the efforts to optimize refinery operations, enhance product yields, and maximize profitability amidst evolving market dynamics and regulatory requirements in the energy sector.

Fluid Catalytic Cracking Market Driver: Rising Demand for Transportation Fuels and Petrochemical Feedstocks

The primary driver for the fluid catalytic cracking market is the rising demand for transportation fuels and petrochemical feedstocks globally. As population growth, urbanization, and economic development drive energy consumption and mobility, there is an increasing need for refined petroleum products to fuel vehicles, power industries, and support economic activities. FCC units enable refineries to process heavy crude oils and residual fractions into lighter, higher-value products that meet stringent quality specifications and market demands. The growing demand for gasoline, diesel, jet fuel, and petrochemical intermediates drives market demand for FCC units as essential components of petroleum refining operations.

Fluid Catalytic Cracking Market Opportunity: Technological Advancements and Retrofitting Opportunities for FCC Units

An opportunity exists for technological advancements and retrofitting opportunities in the fluid catalytic cracking market. While FCC technology has been widely used in petroleum refining for decades, there is a potential to innovate and improve FCC unit performance, energy efficiency, and environmental sustainability through advancements in catalyst formulations, process optimization, and equipment design. Additionally, with stricter environmental regulations and evolving market preferences for cleaner fuels and reduced emissions, there is a growing demand for retrofitting existing FCC units with advanced emissions control technologies, such as selective catalytic reduction (SCR) and flue gas desulfurization (FGD) systems, to comply with regulatory requirements and improve environmental performance. By investing in research and development, engineering expertise, and project management capabilities, companies can capitalize on opportunities to enhance FCC unit efficiency, reliability, and environmental compliance while meeting evolving market demands for refined petroleum products.

Fluid Catalytic Cracking Market Ecosystem

The Fluid Catalytic Cracking (FCC) Market Ecosystem encompasses diverse key stages, with catalyst manufacturing. Companies including BASF SE and Albemarle Corporation develop and produce FCC catalysts crucial for optimizing the cracking process efficiency and yielding valuable petroleum products. Engineering firms including Axens and Technip Energies contribute to the engineering and design of FCC units, while refinery equipment suppliers including Honeywell International Inc. and Linde plc manufacture essential equipment including reactors and fractionation towers.

During construction and commissioning, Engineering, Procurement, and Construction (EPC) contractors including Fluor Corporation manage project lifecycles for building or revamping FCC units. Oil refineries, including Exxon Mobil Corporation and Royal Dutch Shell plc, utilize FCC units to process crude oil and convert heavy fractions into valuable products, overseeing operations and maintenance for optimal performance. Further, oil and gas marketing companies including Shell plc and Exxon Mobil Corporation distribute refined products including gasoline, diesel, and olefins through established channels, completing the Market Ecosystem.

Fluid Catalytic Cracking Market Share Analysis: Zeolite held the dominant revenue share in 2024

The Zeolite segment is the largest segment in the Fluid Catalytic Cracking (FCC) Market, driven by diverse pivotal factors. Zeolite catalysts, specifically zeolite Y and zeolite ZSM-5, are extensively used in the fluid catalytic cracking process due to their exceptional catalytic properties, including high surface area, acidity, and selectivity. These properties make zeolite catalysts highly effective in promoting the cracking of heavy hydrocarbon molecules into lighter products such as gasoline, diesel, and olefins. Additionally, zeolite catalysts exhibit excellent stability and resistance to deactivation, prolonging their lifespan and ensuring consistent performance over extended operating periods. In addition, advancements in zeolite synthesis techniques and catalyst formulation technologies continue to improve the efficiency and selectivity of zeolite catalysts, further driving their widespread adoption in FCC units worldwide. Further, as the demand for transportation fuels and petrochemical feedstocks continues to grow, the Zeolite segment is expected to maintain its dominance in the Fluid Catalytic Cracking Market.

Fluid Catalytic Cracking Market Share Analysis: ORBIT-3600 is the fastest growing market segment over the forecast period to 2030

The ORBIT-3600 segment is the fastest-growing segment in the Fluid Catalytic Cracking (FCC) Market, driven by diverse key factors. ORBIT-3600 is an advanced FCC catalyst technology developed by Albemarle Corporation, designed to enhance the performance and efficiency of FCC units in petroleum refineries. This catalyst technology offers superior activity, selectivity, and stability compared to conventional catalysts, allowing for increased conversion of heavy hydrocarbons into high-value products such as gasoline and propylene. Additionally, ORBIT-3600 catalysts feature innovative particle engineering and surface modification techniques that optimize the catalytic cracking process, resulting in improved yields, reduced coke formation, and lower catalyst circulation rates. Further, as refineries seek to maximize profitability and minimize environmental impact, the adoption of advanced catalyst technologies like ORBIT-3600 is expected to accelerate, driving the rapid growth of this segment in the Fluid Catalytic Cracking Market.

Fluid Catalytic Cracking Market Share Analysis: Stacked is the fastest growing market segment over the forecast period to 2030

The Stacked segment is the fastest-growing segment in the Fluid Catalytic Cracking (FCC) Market, driven by diverse key factors. Stacked configuration refers to the arrangement of catalyst regeneration and reaction zones in a vertically stacked configuration within the FCC unit. This configuration offers diverse advantages over the traditional side-by-side configuration, including improved heat integration, enhanced catalyst circulation, and greater flexibility in process control. Additionally, stacked FCC units enable higher catalyst-to-oil ratios and more efficient heat recovery, leading to increased conversion rates and product yields. Further, advancements in engineering design and process optimization have further enhanced the performance and reliability of stacked FCC units, making them increasingly preferred by refineries seeking to maximize throughput and profitability. As refineries continue to invest in upgrading and expanding their FCC units to meet growing demand for transportation fuels and petrochemical feedstocks, the Stacked segment is expected to experience rapid growth in the Fluid Catalytic Cracking Market.

Fluid Catalytic Cracking Market Report Scope-

By Type

Lanthanum Oxide

Zeolite

By Category

LVR-60

ORBIT-3600

CHV-1

RAG-7

By Technical Configuration

Side-By-Side Type

Stacked Type

By Application

Chemical

Others

Fluid Catalytic Cracking Market Companies Profiled

Albemarle Corp

Arkema SA

Axens

BASF SE

Chevron Lummus Global

Dow Inc

Exxon Mobil Corp

Fluor Corp

Honeywell International Inc

JGC Corp

Johnson Matthey PLC

Kuwait Catalyst Company

Magma Ceramics & Catalysts

McDermott International Inc

N.E. Chemcat Corp

Porocel Corp

Shell plc

W.R. Grace & Co.

Yueyang Sciensun Chemical Co. Ltd

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Fluid Catalytic Cracking Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Fluid Catalytic Cracking Market Size Outlook, $ Million, 2021 to 2030

3.2 Fluid Catalytic Cracking Market Outlook by Type, $ Million, 2021 to 2030

3.3 Fluid Catalytic Cracking Market Outlook by Product, $ Million, 2021 to 2030

3.4 Fluid Catalytic Cracking Market Outlook by Application, $ Million, 2021 to 2030

3.5 Fluid Catalytic Cracking Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Fluid Catalytic Cracking Industry

4.2 Key Market Trends in Fluid Catalytic Cracking Industry

4.3 Potential Opportunities in Fluid Catalytic Cracking Industry

4.4 Key Challenges in Fluid Catalytic Cracking Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Fluid Catalytic Cracking Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Fluid Catalytic Cracking Market Outlook by Segments

7.1 Fluid Catalytic Cracking Market Outlook by Segments, $ Million, 2021- 2030

By Type

Lanthanum Oxide

Zeolite

By Category

LVR-60

ORBIT-3600

CHV-1

RAG-7

By Technical Configuration

Side-By-Side Type

Stacked Type

By Application

Chemical

Others

8 North America Fluid Catalytic Cracking Market Analysis and Outlook To 2030

8.1 Introduction to North America Fluid Catalytic Cracking Markets in 2024

8.2 North America Fluid Catalytic Cracking Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Fluid Catalytic Cracking Market size Outlook by Segments, 2021-2030

By Type

Lanthanum Oxide

Zeolite

By Category

LVR-60

ORBIT-3600

CHV-1

RAG-7

By Technical Configuration

Side-By-Side Type

Stacked Type

By Application

Chemical

Others

9 Europe Fluid Catalytic Cracking Market Analysis and Outlook To 2030

9.1 Introduction to Europe Fluid Catalytic Cracking Markets in 2024

9.2 Europe Fluid Catalytic Cracking Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Fluid Catalytic Cracking Market Size Outlook by Segments, 2021-2030

By Type

Lanthanum Oxide

Zeolite

By Category

LVR-60

ORBIT-3600

CHV-1

RAG-7

By Technical Configuration

Side-By-Side Type

Stacked Type

By Application

Chemical

Others

10 Asia Pacific Fluid Catalytic Cracking Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Fluid Catalytic Cracking Markets in 2024

10.2 Asia Pacific Fluid Catalytic Cracking Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Fluid Catalytic Cracking Market size Outlook by Segments, 2021-2030

By Type

Lanthanum Oxide

Zeolite

By Category

LVR-60

ORBIT-3600

CHV-1

RAG-7

By Technical Configuration

Side-By-Side Type

Stacked Type

By Application

Chemical

Others

11 South America Fluid Catalytic Cracking Market Analysis and Outlook To 2030

11.1 Introduction to South America Fluid Catalytic Cracking Markets in 2024

11.2 South America Fluid Catalytic Cracking Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Fluid Catalytic Cracking Market size Outlook by Segments, 2021-2030

By Type

Lanthanum Oxide

Zeolite

By Category

LVR-60

ORBIT-3600

CHV-1

RAG-7

By Technical Configuration

Side-By-Side Type

Stacked Type

By Application

Chemical

Others

12 Middle East and Africa Fluid Catalytic Cracking Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Fluid Catalytic Cracking Markets in 2024

12.2 Middle East and Africa Fluid Catalytic Cracking Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Fluid Catalytic Cracking Market size Outlook by Segments, 2021-2030

By Type

Lanthanum Oxide

Zeolite

By Category

LVR-60

ORBIT-3600

CHV-1

RAG-7

By Technical Configuration

Side-By-Side Type

Stacked Type

By Application

Chemical

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Albemarle Corp

Arkema SA

Axens

BASF SE

Chevron Lummus Global

Dow Inc

Exxon Mobil Corp

Fluor Corp

Honeywell International Inc

JGC Corp

Johnson Matthey PLC

Kuwait Catalyst Company

Magma Ceramics & Catalysts

McDermott International Inc

N.E. Chemcat Corp

Porocel Corp

Shell plc

W.R. Grace & Co.

Yueyang Sciensun Chemical Co. Ltd

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

Lanthanum Oxide

Zeolite

By Category

LVR-60

ORBIT-3600

CHV-1

RAG-7

By Technical Configuration

Side-By-Side Type

Stacked Type

By Application

Chemical

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)