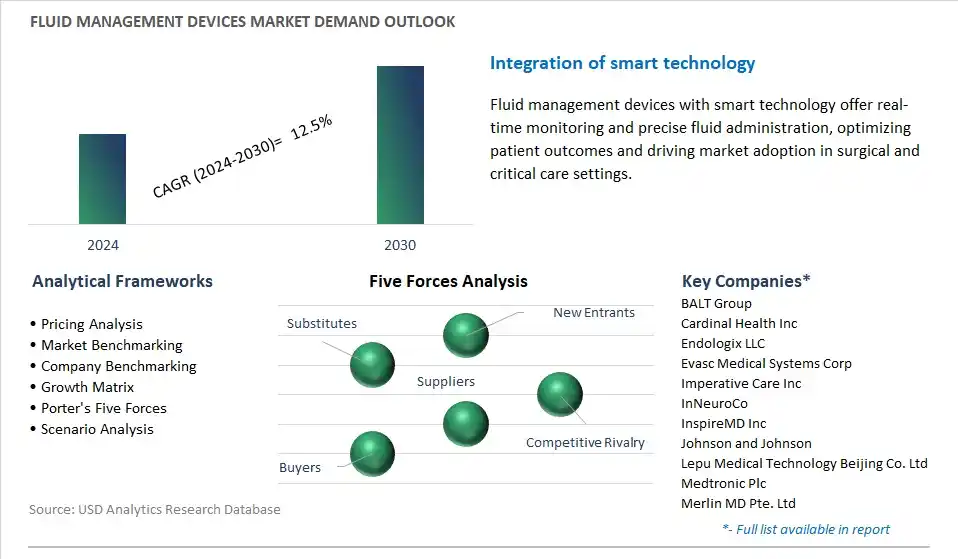

Fluid Management Devices Market is estimated to increase at a growth rate of 12.5% CAGR over the forecast period from 2024 to 2030.

The global Fluid Management Devices Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments including By Product (Systems, Accessories), By Application (Urology, Hysteroscopy, Laparoscopy, Arthroscopy, Others), By End-User (Hospitals, Clinics, Others).

An Introduction to Fluid Management Devices Market in 2024

The Fluid Management Devices Market encompasses medical devices and systems used for fluid administration, monitoring, and regulation in healthcare settings. These devices include infusion pumps, intravenous (IV) sets, catheters, pressure monitoring systems, and fluid warming systems, among others. They play a crucial role in maintaining fluid balance, administering medications, and delivering essential fluids like blood, saline, and contrast agents during surgeries, critical care, and other medical procedures.

Fluid Management Devices Market Competitive Landscape

The global Fluid Management Devices Industry is highly competitive with a large number of companies focusing on niche market segments. Amidst intense competitive conditions, Fluid Management Devices Companies are investing in new product launches and strengthening distribution channels. Key companies operating in the Fluid Management Devices Industry include- BALT Group, Cardinal Health Inc, Endologix LLC, Evasc Medical Systems Corp, Imperative Care Inc, InNeuroCo, InspireMD Inc, Johnson and Johnson, Lepu Medical Technology Beijing Co. Ltd, Medtronic Plc, Merlin MD Pte. Ltd, MicroPort Scientific Corp, Oxford Endovascular Ltd, Penumbra Inc, Rapid Medical Ltd, Siemens AG, Stryker Corp, Terumo Corp, WallBy Medical LLC.

Fluid Management Devices Market Trend: Rise in Minimally Invasive Surgeries

A significant trend in the fluid management devices market is the increasing adoption of minimally invasive surgical procedures across various medical specialties, driving the demand for advanced fluid management technologies. Minimally invasive surgeries require precise control and management of fluid levels within the patient's body to optimize visualization, maintain hemodynamic stability, and prevent complications such as hypovolemia or fluid overload. This trend reflects the shift towards less invasive treatment options that offer faster recovery times, reduced postoperative pain, and improved patient outcomes, thereby spurring innovation and growth in fluid management device technologies tailored for minimally invasive procedures.

Fluid Management Devices Market Driver: Growing Aging Population and Surgical Demand

A key driver in the fluid management devices market is the growing aging population worldwide, coupled with an increasing prevalence of chronic diseases and surgical interventions necessitating advanced fluid management solutions. As the population ages, the incidence of age-related medical conditions such as cardiovascular diseases, cancer, and orthopedic disorders rises, driving demand for surgical interventions to address these health concerns. Fluid management devices play a critical role in supporting perioperative care, optimizing fluid balance, and minimizing surgical complications, thereby meeting the clinical needs of an aging population and driving market growth in fluid management technologies.

Fluid Management Devices Market Opportunity: Integration of Smart Technology and Connectivity

One Market Opportunity in the fluid management devices market lies in the integration of smart technology and connectivity features to enhance device functionality, data monitoring, and interoperability with hospital information systems. By incorporating sensors, algorithms, and wireless connectivity, fluid management devices can provide real-time monitoring of fluid parameters, automate infusion rate adjustments, and facilitate remote monitoring and data sharing with healthcare providers. This integration of smart technology offers opportunities to improve clinical decision-making, enhance patient safety, and streamline workflow efficiency in healthcare settings, thereby driving adoption and market expansion of next-generation fluid management solutions.

Fluid Management Devices Market Share Analysis: Fluid Management Systems is the fastest growing market segment over the forecast period to 2030

Among fluid management devices, fluid management systems are experiencing the fastest growth. Fluid management systems encompass a comprehensive range of devices and equipment designed to regulate and monitor fluid levels and flow rates during medical procedures, particularly in surgical and interventional settings. These systems include components such as pumps, tubing sets, pressure monitoring devices, and disposables, all integrated into a cohesive platform for efficient fluid administration and control. In contrast, intrasaccular flow disruption devices are specific to neurovascular interventions and are not as widely utilized across different medical specialties as fluid management systems. The increasing demand for fluid management systems is driven by several factors, including the rising prevalence of minimally invasive procedures, the growing complexity of surgeries requiring precise fluid management, and the emphasis on patient safety and outcomes. Hospitals and specialty clinics are the primary end-users of fluid management systems, where they are utilized in a wide range of procedures, including laparoscopic surgeries, endoscopic interventions, and interventional radiology procedures. As healthcare facilities strive to optimize procedural efficiency, minimize complications, and improve patient outcomes, the market for fluid management systems is expected to continue its rapid growth trajectory, offering advanced solutions for fluid administration and control in various medical disciplines.

Fluid Management Devices Market Segmentation

By Product

Fluid management systems

Fluid management accessories

By Application

Urology

Hysteroscopy

Laparoscopy

Arthroscopy

Others

By End-User

Hospitals

Clinics

Others

Geographical Analysis

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Fluid Management Devices Companies

BALT Group

Cardinal Health Inc

Endologix LLC

Evasc Medical Systems Corp

Imperative Care Inc

InNeuroCo

InspireMD Inc

Johnson and Johnson

Lepu Medical Technology Beijing Co. Ltd

Medtronic Plc

Merlin MD Pte. Ltd

MicroPort Scientific Corp

Oxford Endovascular Ltd

Penumbra Inc

Rapid Medical Ltd

Siemens AG

Stryker Corp

Terumo Corp

WallBy Medical LLC

* List not Exhaustive

Reasons to Buy the Fluid Management Devices Market Study

• Deepen your industry insights and navigate uncertainties for strategy formulation, CAPEX, and Operational decisions

• Gain access to detailed insights on the Fluid Management Devices Market, encompassing current market size, growth trends, and forecasts till 2030.

• Access detailed competitor analysis, enabling competitive advantage through a thorough understanding of market players, strategies, and potential differentiation opportunities

• Stay ahead of the curve with insights on technological advancements, innovations, and upcoming trends

• Identify lucrative investment avenues and expansion opportunities within the Fluid Management Devices Industry, guided by robust, data-backed analysis.

• Understand regional and global markets through country-wise analysis, regional market potential, regulatory nuances, and dynamics

• Execute strategies with confidence and speed through information, analytics, and insights on the industry value chain

• Corporate leaders, strategists, financial experts, shareholders, asset managers, and governmental representatives can make long-term planning scenarios and build an integrated and timely understanding of market dynamics

• Benefit from tailored solutions and expert consultation based on report insights, providing personalized strategies aligned with specific business needs.

TABLE OF CONTENTS

1 Introduction to 2024 Fluid Management Devices Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Analyzed

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Fluid Management Devices Market Size Outlook, $ Million, 2021 to 2030

3.2 Fluid Management Devices Market Outlook by Type, $ Million, 2021 to 2030

3.3 Fluid Management Devices Market Outlook by Product, $ Million, 2021 to 2030

3.4 Fluid Management Devices Market Outlook by Application, $ Million, 2021 to 2030

3.5 Fluid Management Devices Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Fluid Management Devices Industry

4.2 Key Market Trends in Fluid Management Devices Industry

4.3 Potential Opportunities in Fluid Management Devices Industry

4.4 Key Challenges in Fluid Management Devices Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Fluid Management Devices Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Fluid Management Devices Market Outlook by Segments

7.1 Fluid Management Devices Market Outlook by Segments, $ Million, 2021- 2030

By Product

Fluid management systems

Fluid management accessories

By Application

Urology

Hysteroscopy

Laparoscopy

Arthroscopy

Others

By End-User

Hospitals

Clinics

Others

8 North America Fluid Management Devices Market Analysis and Outlook To 2030

8.1 Introduction to North America Fluid Management Devices Markets in 2024

8.2 North America Fluid Management Devices Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Fluid Management Devices Market size Outlook by Segments, 2021-2030

By Product

Fluid management systems

Fluid management accessories

By Application

Urology

Hysteroscopy

Laparoscopy

Arthroscopy

Others

By End-User

Hospitals

Clinics

Others

9 Europe Fluid Management Devices Market Analysis and Outlook To 2030

9.1 Introduction to Europe Fluid Management Devices Markets in 2024

9.2 Europe Fluid Management Devices Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Fluid Management Devices Market Size Outlook by Segments, 2021-2030

By Product

Fluid management systems

Fluid management accessories

By Application

Urology

Hysteroscopy

Laparoscopy

Arthroscopy

Others

By End-User

Hospitals

Clinics

Others

10 Asia Pacific Fluid Management Devices Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Fluid Management Devices Markets in 2024

10.2 Asia Pacific Fluid Management Devices Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Fluid Management Devices Market size Outlook by Segments, 2021-2030

By Product

Fluid management systems

Fluid management accessories

By Application

Urology

Hysteroscopy

Laparoscopy

Arthroscopy

Others

By End-User

Hospitals

Clinics

Others

11 South America Fluid Management Devices Market Analysis and Outlook To 2030

11.1 Introduction to South America Fluid Management Devices Markets in 2024

11.2 South America Fluid Management Devices Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Fluid Management Devices Market size Outlook by Segments, 2021-2030

By Product

Fluid management systems

Fluid management accessories

By Application

Urology

Hysteroscopy

Laparoscopy

Arthroscopy

Others

By End-User

Hospitals

Clinics

Others

12 Middle East and Africa Fluid Management Devices Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Fluid Management Devices Markets in 2024

12.2 Middle East and Africa Fluid Management Devices Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Fluid Management Devices Market size Outlook by Segments, 2021-2030

By Product

Fluid management systems

Fluid management accessories

By Application

Urology

Hysteroscopy

Laparoscopy

Arthroscopy

Others

By End-User

Hospitals

Clinics

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

List of Companies

BALT Group

Cardinal Health Inc

Endologix LLC

Evasc Medical Systems Corp

Imperative Care Inc

InNeuroCo

InspireMD Inc

Johnson and Johnson

Lepu Medical Technology Beijing Co. Ltd

Medtronic Plc

Merlin MD Pte. Ltd

MicroPort Scientific Corp

Oxford Endovascular Ltd

Penumbra Inc

Rapid Medical Ltd

Siemens AG

Stryker Corp

Terumo Corp

WallBy Medical LLC

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise