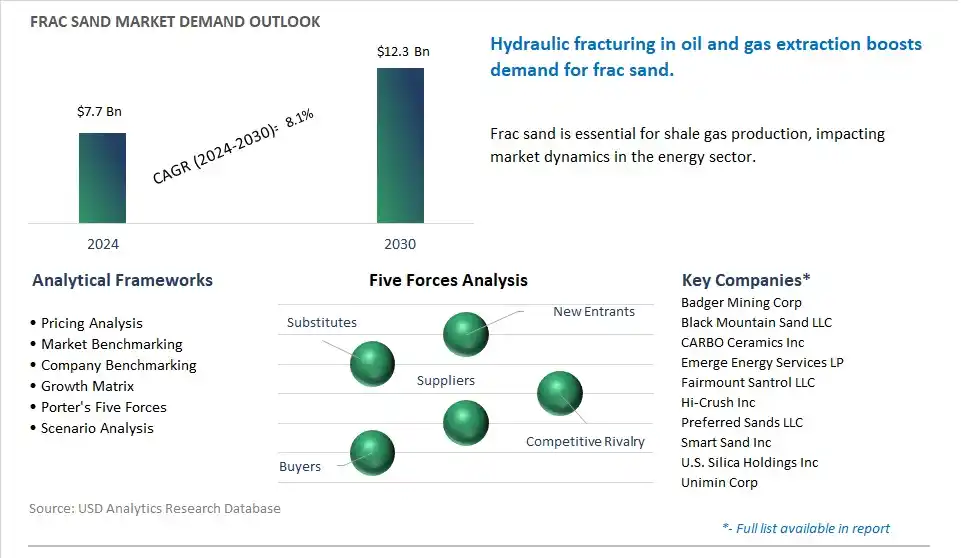

The global Frac Sand Market is poised to register a 8.1% CAGR from $7.7 Billion in 2024 to $12.3 Billion in 2030.

The global Frac Sand Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Application (Oil Exploration, Gas Extraction), By Type (White Sand, Brown Sand, Others).

An Introduction to Global Frac Sand Market in 2024

The frac sand market is experiencing rapid growth driven by its critical role in hydraulic fracturing operations for oil and gas production. Key trends shaping the future of the industry include the increasing demand for high-quality frac sand that offers optimal grain size, shape, and crush resistance while meeting performance specifications and cost requirements for unconventional oil and gas extraction. As energy companies, drilling contractors, and proppant suppliers seek to maximize well productivity, reduce drilling costs, and minimize environmental impact, there's a growing need for frac sand sourced from geologically favorable deposits that provide consistent quality, logistics advantages, and environmental sustainability throughout the hydraulic fracturing process. Moreover, advancements in frac sand mining, processing, and logistics are driving market expansion by improving extraction efficiency, water management, and community engagement while addressing concerns related to land use, air quality, and habitat conservation in frac sand-producing regions. Additionally, the growing adoption of alternative proppants such as ceramic beads, resin-coated sands, and synthetic proppants is fueling demand for innovative solutions that offer enhanced performance, durability, and flowback control in challenging reservoir conditions. Furthermore, the integration of frac sand with digital well modeling, reservoir simulation, and data analytics is driving innovation and market growth in the hydraulic fracturing industry, enabling the development of smarter, more efficient, and more sustainable solutions for oil and gas production in unconventional reservoirs.

Frac Sand Market Competitive Landscape

The market report analyses the leading companies in the industry including Badger Mining Corp, Black Mountain Sand LLC, CARBO Ceramics Inc, Emerge Energy Services LP, Fairmount Santrol LLC, Hi-Crush Inc, Preferred Sands LLC, Smart Sand Inc, U.S. Silica Holdings Inc, Unimin Corp.

Frac Sand Market Dynamics

Frac Sand Market Trend: Shifting Sands: Diversification in Frac Sand Sources

A notable trend in the frac sand market is the diversification of sand sources driven by changing market dynamics and environmental considerations. Traditionally, frac sand was sourced primarily from Midwest regions such as Wisconsin and Minnesota due to their high-quality, fine-grain silica deposits. However, increasing demand and logistical challenges have spurred exploration and development efforts to identify alternative sand sources closer to oil and gas basins. This trend is leading to the emergence of new frac sand deposits in regions like Texas, Oklahoma, and Appalachia, offering proximity advantages, cost savings, and reduced environmental impact through shorter transportation distances and decreased trucking emissions.

Frac Sand Market Driver: Surging Demand for Hydraulic Fracturing in Oil and Gas Exploration

A significant driver fueling the frac sand market is the surging demand for hydraulic fracturing (fracking) in oil and gas exploration and production activities. Hydraulic fracturing, a key technique for extracting hydrocarbons from unconventional reservoirs such as shale formations, relies on frac sand as a proppant to hold open fractures and facilitate the flow of oil and gas to the surface. With the continued expansion of shale oil and gas development in regions like the Permian Basin and the Marcellus Shale, the demand for frac sand is expected to escalate further, driving market growth. Additionally, technological advancements in fracking techniques, such as longer lateral wells and higher proppant volumes per well, are contributing to increased frac sand consumption, amplifying its importance in the energy industry supply chain.

Frac Sand Market Opportunity: Innovation in Sustainable Frac Sand Solutions

An opportunity for market advancement lies in innovation towards sustainable frac sand solutions that address environmental concerns and regulatory requirements. As the environmental footprint of frac sand mining and transportation comes under scrutiny, there is growing interest in sustainable practices and alternative proppants that minimize ecological impact. Manufacturers and suppliers have an opportunity to develop eco-friendly frac sand products, such as recycled or reclaimed sand, ceramic proppants, or resin-coated sands with improved durability and conductivity. Furthermore, there is potential for technological innovation in frac sand processing, logistics, and waste management to optimize resource utilization, reduce water consumption, and mitigate environmental risks, thereby enhancing the sustainability of frac sand operations and meeting the evolving needs of the energy industry.

Frac Sand Market Share Analysis: Oil Exploration segment generated the highest revenue in the industry

The Oil Exploration segment is the largest segment in the Frac Sand Market, driven by diverse key factors that highlight its predominant role in hydraulic fracturing operations within the oil and gas industry. Frac sand, also known as proppant, plays a crucial role in hydraulic fracturing, a well stimulation technique used to extract oil and natural gas from underground reservoirs, particularly shale formations. One primary reason for the dominance of the Oil Exploration segment is the significant demand for frac sand in hydraulic fracturing operations conducted in oil-rich regions worldwide. Frac sand serves as a proppant, a material injected into oil and gas wells at high pressure to create and prop open fractures in the rock formation, allowing hydrocarbons to flow more freely to the wellbore and be extracted to the surface. The use of frac sand as a proppant is essential for enhancing well productivity, maximizing oil and gas recovery, and optimizing production rates in shale oil and gas plays. Additionally, the expansion of hydraulic fracturing activities, particularly in unconventional oil and gas reservoirs such as shale formations, further drives the demand for frac sand as a critical component of the hydraulic fracturing process. In addition, the quality and characteristics of frac sand, including particle size, shape, roundness, and crush resistance, are crucial factors influencing its effectiveness as a proppant in hydraulic fracturing operations. High-quality frac sand with optimal properties enhances well performance, reduces operational costs, and improves Over the forecast period efficiency in oil exploration and production activities. Further, technological advancements in hydraulic fracturing techniques, including horizontal drilling and multi-stage fracturing, have led to increased frac sand consumption per well, further bolstering the demand for frac sand in oil exploration operations. With the continued growth of oil and gas production from unconventional reservoirs and ongoing advancements in hydraulic fracturing technology, the Oil Exploration segment in the Frac Sand Market is expected to maintain its position as the largest and most essential segment, offering manufacturers and suppliers opportunities for sustained growth and market leadership in the global energy industry.

Frac Sand Market Share Analysis: White Sand Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The White Sand segment is the fastest-growing segment in the Frac Sand Market, driven by diverse key factors that reflect changing industry dynamics, technological advancements, and market preferences within the oil and gas sector. White sand, also known as Northern White sand, offers distinct advantages over brown sand and other alternatives, making it increasingly sought after in hydraulic fracturing operations. One primary reason for the rapid growth of the White Sand segment is its superior physical properties, including roundness, sphericity, and crush resistance, which make it highly effective as a proppant in hydraulic fracturing applications. White sand deposits, particularly those found in the Midwest region of the United States, exhibit exceptional purity and uniformity, resulting in proppants with consistent particle size distribution and excellent conductivity properties. These properties enhance the flow of hydrocarbons from the reservoir to the wellbore, improving well productivity and maximizing oil and gas recovery rates. Additionally, technological advancements in hydraulic fracturing techniques, such as longer horizontal wellbores and increased proppant volumes per well, have led to growing demand for high-quality proppants like white sand, which can withstand higher pressures and temperatures encountered in deep and complex formations. In addition, environmental considerations and regulatory requirements have spurred the adoption of white sand proppants, as they produce lower levels of fugitive dust emissions and silica exposure risks compared to brown sand and other alternatives. Further, the preference for white sand proppants among oil and gas operators, particularly in premium shale plays such as the Permian Basin and Eagle Ford Formation, has driven investment in white sand mining and processing facilities, further fueling the growth of the White Sand segment in the Frac Sand Market. With its superior performance characteristics, increasing demand from oil and gas operators, and ongoing investments in production capacity expansion, the White Sand segment is poised for rapid growth, offering manufacturers and suppliers opportunities for market expansion and profitability in the dynamic and competitive frac sand industry.

Frac Sand Market Report Segmentation

By Application

Oil Exploration

Gas Extraction

By Type

White Sand

Brown Sand

Others

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Frac Sand Companies Profiled in the Market Study

Badger Mining Corp

Black Mountain Sand LLC

CARBO Ceramics Inc

Emerge Energy Services LP

Fairmount Santrol LLC

Hi-Crush Inc

Preferred Sands LLC

Smart Sand Inc

U.S. Silica Holdings Inc

Unimin Corp

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Frac Sand Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Frac Sand Market Size Outlook, $ Million, 2021 to 2030

3.2 Frac Sand Market Outlook by Type, $ Million, 2021 to 2030

3.3 Frac Sand Market Outlook by Product, $ Million, 2021 to 2030

3.4 Frac Sand Market Outlook by Application, $ Million, 2021 to 2030

3.5 Frac Sand Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Frac Sand Industry

4.2 Key Market Trends in Frac Sand Industry

4.3 Potential Opportunities in Frac Sand Industry

4.4 Key Challenges in Frac Sand Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Frac Sand Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Frac Sand Market Outlook by Segments

7.1 Frac Sand Market Outlook by Segments, $ Million, 2021- 2030

By Application

Oil Exploration

Gas Extraction

By Type

White Sand

Brown Sand

Others

8 North America Frac Sand Market Analysis and Outlook To 2030

8.1 Introduction to North America Frac Sand Markets in 2024

8.2 North America Frac Sand Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Frac Sand Market size Outlook by Segments, 2021-2030

By Application

Oil Exploration

Gas Extraction

By Type

White Sand

Brown Sand

Others

9 Europe Frac Sand Market Analysis and Outlook To 2030

9.1 Introduction to Europe Frac Sand Markets in 2024

9.2 Europe Frac Sand Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Frac Sand Market Size Outlook by Segments, 2021-2030

By Application

Oil Exploration

Gas Extraction

By Type

White Sand

Brown Sand

Others

10 Asia Pacific Frac Sand Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Frac Sand Markets in 2024

10.2 Asia Pacific Frac Sand Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Frac Sand Market size Outlook by Segments, 2021-2030

By Application

Oil Exploration

Gas Extraction

By Type

White Sand

Brown Sand

Others

11 South America Frac Sand Market Analysis and Outlook To 2030

11.1 Introduction to South America Frac Sand Markets in 2024

11.2 South America Frac Sand Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Frac Sand Market size Outlook by Segments, 2021-2030

By Application

Oil Exploration

Gas Extraction

By Type

White Sand

Brown Sand

Others

12 Middle East and Africa Frac Sand Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Frac Sand Markets in 2024

12.2 Middle East and Africa Frac Sand Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Frac Sand Market size Outlook by Segments, 2021-2030

By Application

Oil Exploration

Gas Extraction

By Type

White Sand

Brown Sand

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Badger Mining Corp

Black Mountain Sand LLC

CARBO Ceramics Inc

Emerge Energy Services LP

Fairmount Santrol LLC

Hi-Crush Inc

Preferred Sands LLC

Smart Sand Inc

U.S. Silica Holdings Inc

Unimin Corp

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Application

Oil Exploration

Gas Extraction

By Type

White Sand

Brown Sand

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)