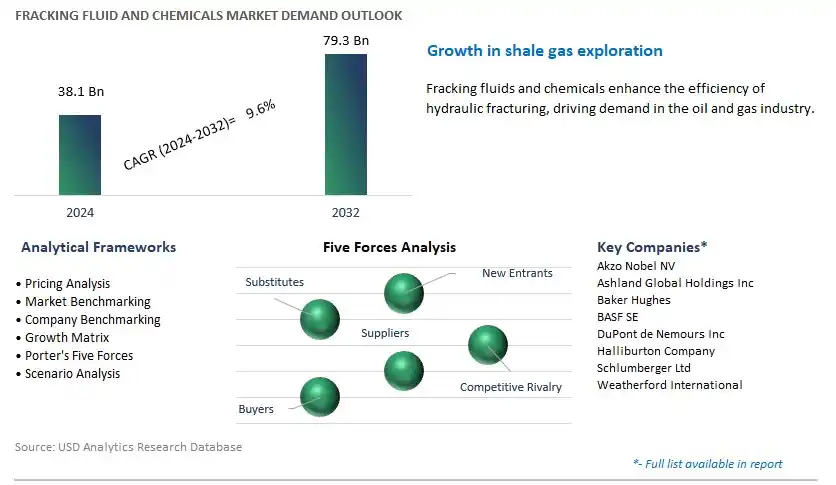

Global Fracking Fluid and Chemicals Market Size is valued at $38.1 Billion in 2024 and is forecast to register a growth rate (CAGR) of 9.6% to reach $79.3 Billion by 2032.

The global Fracking Fluid and Chemicals Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Fluids (Water-Based, Foam-Based, Gelled Oil-Based), By Well (Horizontal, Vertical), By Function (Acid, Surfactant, Biocide, Gelling Agent, Cross linker, Breaker, Scale Inhibitor, Corrosion Inhibitor, Clay Control/Stabilizer, Iron Control, Friction reducer).

An Introduction to Fracking Fluid and Chemicals Market in 2024

Fracking fluids and chemicals play a crucial role in hydraulic fracturing operations, enabling the extraction of oil and natural gas from underground reservoirs. In 2024, the market for fracking fluids and chemicals is witnessing dynamic growth driven by the expansion of unconventional oil and gas production worldwide. These fluids, comprising water, proppants, friction reducers, biocides, and corrosion inhibitors, are tailored to optimize well productivity, mitigate formation damage, and ensure environmental compliance. Further, advancements in fracking fluid formulations, including environmentally friendly additives and recycled water usage, reflect industry efforts to minimize ecological impact and enhance sustainability. As energy demand s to rise and technological innovations reshape the oil and gas sector, the demand for efficient and environmentally responsible fracking fluids and chemicals is expected to escalate, driving further research and development in the field.

Fracking Fluid and Chemicals Market Competitive Landscape

The market report analyses the leading companies in the industry including Akzo Nobel NV, Ashland Global Holdings Inc, Baker Hughes, BASF SE, DuPont de Nemours Inc, Halliburton Company, Schlumberger Ltd, Weatherford International, and others.

Fracking Fluid and Chemicals Market Dynamics

Market Trend: Shift Towards Environmentally Friendly and Sustainable Fracking Fluids

A prominent trend in the fracking fluid and chemicals market is the shift towards environmentally friendly and sustainable fracking fluids. With increasing concerns about the environmental impact of hydraulic fracturing operations, there is a growing demand for fracking fluids and chemicals that minimize water usage, reduce toxicity, and mitigate ecological risks. Companies are developing innovative formulations using biodegradable additives, recycled water, and non-toxic chemicals to address environmental concerns and enhance the sustainability of fracking operations. This trend reflects the industry's commitment to responsible resource extraction and regulatory compliance, driving the adoption of eco-friendly fracking fluids and chemicals across the oil and gas industry.

Market Driver: Expansion of Shale Gas and Tight Oil Exploration

A key driver fueling the demand for fracking fluid and chemicals is the expansion of shale gas and tight oil exploration activities worldwide. With the depletion of conventional oil and gas reserves, energy companies are increasingly turning to unconventional resources such as shale formations and tight reservoirs to meet growing energy demand. Hydraulic fracturing, or fracking, is a key technique used to extract hydrocarbons from these unconventional reservoirs, driving market demand for specialized fluids and chemicals that facilitate the fracturing process, improve well productivity, and enhance hydrocarbon recovery rates. The continued exploration and development of shale gas and tight oil resources create opportunities for suppliers of fracking fluids and chemicals to support drilling and production operations in these unconventional reservoirs.

Market Opportunity: Development of Advanced Friction Reducers and Water Treatment Solutions

Amidst the evolving landscape of the fracking fluid and chemicals market, there exists a significant opportunity for the development of advanced friction reducers and water treatment solutions. Manufacturers can capitalize on this opportunity by innovating friction reducers that improve hydraulic fracturing efficiency, reduce friction pressure, and enhance fluid flow properties while minimizing environmental impact and toxicity. Additionally, there is a growing demand for water treatment solutions that enable the efficient recycling and reuse of produced water from fracking operations, reducing freshwater consumption and wastewater disposal costs. Companies can also offer integrated solutions combining friction reducers, biocides, scale inhibitors, and corrosion inhibitors to optimize fracking fluid performance and mitigate operational risks. By investing in research and development to develop advanced fracking fluid and chemical technologies, companies can address emerging market needs, meet regulatory requirements, and drive sustainable growth in the dynamic fracking fluid and chemicals market.

Fracking Fluid & Chemicals Market Share Analysis: Water-Based segment generated the highest revenue in 2024

The Water-Based segment is the largest in the Fracking Fluid & Chemicals. Water-based fracking fluids are widely used in hydraulic fracturing operations due to their effectiveness, versatility, and environmental compatibility. Water serves as the primary component of these fluids, with additives such as surfactants, friction reducers, biocides, and corrosion inhibitors included to enhance performance and mitigate operational challenges. Water-based fracking fluids offer potential advantages over alternative formulations. In particular, they exhibit excellent compatibility with reservoir formations, facilitating efficient fracturing and well stimulation processes. Additionally, water-based fluids are cost-effective compared to foam-based and gelled oil-based fluids, making them a preferred choice for hydraulic fracturing operations. Moreover, water-based fluids are environmentally friendly, with lower toxicity and reduced environmental impact compared to oil-based fluids. This characteristic aligns with regulatory requirements and industry initiatives aimed at minimizing environmental risks associated with fracking operations. Furthermore, advancements in water-based fluid formulations and technologies continue to improve their performance and reliability in hydraulic fracturing applications, further solidifying their position as the largest segment in the Fracking Fluid & Chemicals Market. Over the forecast period, the effectiveness, cost-efficiency, environmental compatibility, and ongoing technological advancements contribute to the Water-Based segment's dominance in the market.

Fracking Fluid & Chemicals Market Share Analysis: Horizontal is poised to register the fastest CAGR over the forecast period

The Horizontal segment is the fastest-growing segment in the Fracking Fluid & Chemicals Market. Hydraulic fracturing, or fracking, is increasingly being utilized in horizontal wells due to its ability to access unconventional oil and gas resources trapped in shale formations more efficiently than vertical wells. Horizontal drilling involves drilling a wellbore horizontally through the target formation, allowing for greater exposure to the reservoir and maximizing contact with the hydrocarbon-bearing rock. As a result, horizontal wells typically require larger volumes of fracking fluids and chemicals to stimulate production compared to vertical wells. This increased demand for fracking fluids and chemicals in horizontal wells stems from the need to create extensive fracture networks and maintain optimal fluid flow rates throughout the wellbore. Additionally, horizontal drilling enables operators to access previously untapped reserves and enhance recovery rates, driving the adoption of hydraulic fracturing techniques in shale plays and other unconventional reservoirs. Moreover, advancements in horizontal drilling technology, such as multi-stage hydraulic fracturing and extended reach drilling, further boost the growth of the Horizontal segment by enabling operators to maximize reservoir contact and enhance well productivity. Furthermore, the shift towards longer horizontal lateral lengths and more complex well designs necessitates specialized fracking fluid formulations tailored to the specific geological and operational requirements of horizontal wells. Over the forecast period, the increasing prevalence of horizontal drilling and its associated benefits drive the rapid growth of the Horizontal segment in the Fracking Fluid & Chemicals Market.

Fracking Fluid & Chemicals Market Share Analysis: Friction Reducer segment generated the highest revenue in 2024

The Friction Reducer segment is the largest in the Fracking Fluid & Chemicals. Friction reducers play a crucial role in hydraulic fracturing operations by reducing the frictional resistance between the fracking fluid and the wellbore walls as it flows through the wellbore and fractures, enhancing the fluid's ability to carry proppants and maintain optimal flow rates. Friction reducers typically consist of water-soluble polymers, such as polyacrylamides or copolymers, which reduce the viscosity of the fracking fluid and minimize energy losses during pumping. The use of friction reducers helps optimize hydraulic fracturing treatments by maximizing fluid efficiency, improving pump performance, and enhancing fracture propagation and proppant transport. Additionally, friction reducers enable operators to achieve higher pump rates and longer pumping distances, increasing the effectiveness and coverage of the fracturing operation. Moreover, the growing prevalence of horizontal drilling and multi-stage hydraulic fracturing techniques in shale plays and tight reservoirs further drives the demand for friction reducers as they are essential for maintaining fluid flow and pressure across extended lateral sections of the wellbore. Furthermore, advancements in friction reducer formulations and technologies continue to improve their performance, reliability, and environmental compatibility, further solidifying their position as the largest segment in the Fracking Fluid & Chemicals Market. Over the forecast period, the critical role of friction reducers in optimizing hydraulic fracturing operations and their widespread use across various well types and formations contribute to their dominance in the market.

Fracking Fluid and Chemicals Market

By Fluids

Water-Based

Foam-Based

Gelled Oil-Based

By Well

Horizontal

Vertical

By Function

Acid

Surfactant

Biocide

Gelling Agent

Cross linker

Breaker

Scale Inhibitor

Corrosion Inhibitor

Clay Control/Stabilizer

Iron Control

Friction reducerCountries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Fracking Fluid and Chemicals Companies Profiled in the Study

Akzo Nobel NV

Ashland Global Holdings Inc

Baker Hughes

BASF SE

DuPont de Nemours Inc

Halliburton Company

Schlumberger Ltd

Weatherford International

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Fracking Fluid and Chemicals Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Fracking Fluid and Chemicals Market Size Outlook, $ Million, 2021 to 2032

3.2 Fracking Fluid and Chemicals Market Outlook by Type, $ Million, 2021 to 2032

3.3 Fracking Fluid and Chemicals Market Outlook by Product, $ Million, 2021 to 2032

3.4 Fracking Fluid and Chemicals Market Outlook by Application, $ Million, 2021 to 2032

3.5 Fracking Fluid and Chemicals Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Fracking Fluid and Chemicals Industry

4.2 Key Market Trends in Fracking Fluid and Chemicals Industry

4.3 Potential Opportunities in Fracking Fluid and Chemicals Industry

4.4 Key Challenges in Fracking Fluid and Chemicals Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Fracking Fluid and Chemicals Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Fracking Fluid and Chemicals Market Outlook by Segments

7.1 Fracking Fluid and Chemicals Market Outlook by Segments, $ Million, 2021- 2032

By Fluids

Water-Based

Foam-Based

Gelled Oil-Based

By Well

Horizontal

Vertical

By Function

Acid

Surfactant

Biocide

Gelling Agent

Cross linker

Breaker

Scale Inhibitor

Corrosion Inhibitor

Clay Control/Stabilizer

Iron Control

Friction reducer

8 North America Fracking Fluid and Chemicals Market Analysis and Outlook To 2032

8.1 Introduction to North America Fracking Fluid and Chemicals Markets in 2024

8.2 North America Fracking Fluid and Chemicals Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Fracking Fluid and Chemicals Market size Outlook by Segments, 2021-2032

By Fluids

Water-Based

Foam-Based

Gelled Oil-Based

By Well

Horizontal

Vertical

By Function

Acid

Surfactant

Biocide

Gelling Agent

Cross linker

Breaker

Scale Inhibitor

Corrosion Inhibitor

Clay Control/Stabilizer

Iron Control

Friction reducer

9 Europe Fracking Fluid and Chemicals Market Analysis and Outlook To 2032

9.1 Introduction to Europe Fracking Fluid and Chemicals Markets in 2024

9.2 Europe Fracking Fluid and Chemicals Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Fracking Fluid and Chemicals Market Size Outlook by Segments, 2021-2032

By Fluids

Water-Based

Foam-Based

Gelled Oil-Based

By Well

Horizontal

Vertical

By Function

Acid

Surfactant

Biocide

Gelling Agent

Cross linker

Breaker

Scale Inhibitor

Corrosion Inhibitor

Clay Control/Stabilizer

Iron Control

Friction reducer

10 Asia Pacific Fracking Fluid and Chemicals Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Fracking Fluid and Chemicals Markets in 2024

10.2 Asia Pacific Fracking Fluid and Chemicals Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Fracking Fluid and Chemicals Market size Outlook by Segments, 2021-2032

By Fluids

Water-Based

Foam-Based

Gelled Oil-Based

By Well

Horizontal

Vertical

By Function

Acid

Surfactant

Biocide

Gelling Agent

Cross linker

Breaker

Scale Inhibitor

Corrosion Inhibitor

Clay Control/Stabilizer

Iron Control

Friction reducer

11 South America Fracking Fluid and Chemicals Market Analysis and Outlook To 2032

11.1 Introduction to South America Fracking Fluid and Chemicals Markets in 2024

11.2 South America Fracking Fluid and Chemicals Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Fracking Fluid and Chemicals Market size Outlook by Segments, 2021-2032

By Fluids

Water-Based

Foam-Based

Gelled Oil-Based

By Well

Horizontal

Vertical

By Function

Acid

Surfactant

Biocide

Gelling Agent

Cross linker

Breaker

Scale Inhibitor

Corrosion Inhibitor

Clay Control/Stabilizer

Iron Control

Friction reducer

12 Middle East and Africa Fracking Fluid and Chemicals Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Fracking Fluid and Chemicals Markets in 2024

12.2 Middle East and Africa Fracking Fluid and Chemicals Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Fracking Fluid and Chemicals Market size Outlook by Segments, 2021-2032

By Fluids

Water-Based

Foam-Based

Gelled Oil-Based

By Well

Horizontal

Vertical

By Function

Acid

Surfactant

Biocide

Gelling Agent

Cross linker

Breaker

Scale Inhibitor

Corrosion Inhibitor

Clay Control/Stabilizer

Iron Control

Friction reducer

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Akzo Nobel NV

Ashland Global Holdings Inc

Baker Hughes

BASF SE

DuPont de Nemours Inc

Halliburton Company

Schlumberger Ltd

Weatherford International

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Fluids

Water-Based

Foam-Based

Gelled Oil-Based

By Well

Horizontal

Vertical

By Function

Acid

Surfactant

Biocide

Gelling Agent

Cross linker

Breaker

Scale Inhibitor

Corrosion Inhibitor

Clay Control/Stabilizer

Iron Control

Friction reducer

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)