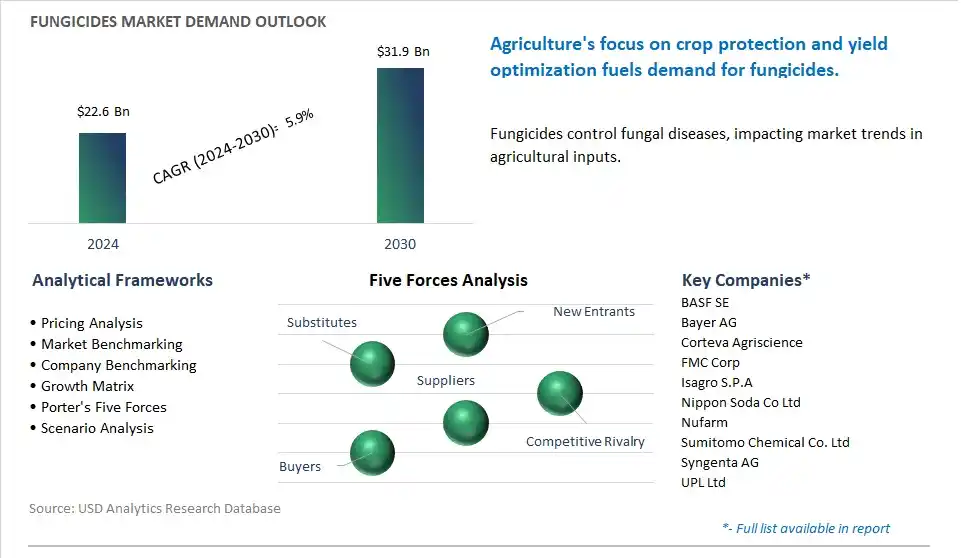

The global Fungicides Market is poised to register a 5.9% CAGR from $22.6 Billion in 2024 to $31.9 Billion in 2030.

The global Fungicides Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (Chemical, Biological), By Application (Seed Treatment, Soil Treatment, Foliar Spray, Post-Harvest, Others), By Mode Of Action (Contact, Systemic), By Form (Liquid, Dry), By Crop (Cereals & Grains, Oilseeds & Pulses, Fruits & Vegetables, Others).

An Introduction to Global Fungicides Market in 2024

The fungicides market is witnessing steady growth driven by the increasing demand for crop protection solutions to combat fungal diseases and improve agricultural productivity. Key trends shaping the future of the industry include the development of innovative fungicide formulations, application techniques, and resistance management strategies to address evolving challenges such as fungicide resistance, regulatory restrictions, and environmental concerns. As farmers and agrochemical companies seek effective and sustainable disease management solutions, there's a growing need for fungicides that offer broad-spectrum activity, systemic protection, and reduced environmental impact while ensuring crop yield stability and food security. Moreover, advancements in fungicide chemistry, biopesticides, and integrated pest management (IPM) practices are driving market expansion by providing growers with more options for disease control, rotation strategies, and sustainable farming practices that minimize pesticide residues, soil degradation, and off-target effects. Additionally, the growing adoption of precision agriculture technologies, remote sensing, and digital farming tools is fueling demand for fungicides that can be applied in a targeted and efficient manner to optimize treatment efficacy, minimize input costs, and reduce environmental footprint associated with conventional spray applications. Furthermore, the integration of fungicides with biological control agents, genetic resistance traits, and predictive modeling is driving innovation and market growth in the crop protection industry, enabling the development of smarter, more sustainable, and more resilient solutions for the future of disease management and crop protection in global agriculture.

Fungicides Market Competitive Landscape

The market report analyses the leading companies in the industry including BASF SE, Bayer AG, Corteva Agriscience, FMC Corp, Isagro S.P.A, Nippon Soda Co Ltd, Nufarm, Sumitomo Chemical Co. Ltd, Syngenta AG, UPL Ltd.

Fungicides Market Dynamics

Fungicides Market Trend: Increasing Demand for Sustainable and Bio-based Fungicides

A significant trend in the fungicides market is the rising demand for sustainable and bio-based fungicides driven by environmental concerns and regulatory pressure. With growing awareness of the adverse effects of chemical pesticides on ecosystems, human health, and food safety, there is a shifting preference towards eco-friendly alternatives in agriculture. Bio-based fungicides derived from natural sources such as plants, microbes, and botanical extracts offer effective pest control while minimizing environmental impact and reducing chemical residues in crops. This trend is reshaping the fungicides market towards more sustainable and environmentally responsible solutions that meet the needs of farmers, consumers, and regulatory authorities.

Fungicides Market Driver: Increasing Incidence of Crop Diseases and Fungal Pathogens

A key driver propelling the fungicides market is the increasing incidence of crop diseases and fungal pathogens threatening global food security and agricultural productivity. Climate change, globalization, and intensive agricultural practices have contributed to the spread of fungal diseases, posing significant challenges to crop production and yield. Fungicides play a crucial role in disease management by controlling fungal pathogens and preventing crop losses, thereby ensuring food supply stability and economic viability for farmers. The escalating threat of fungal diseases and the need for effective disease management strategies drive market demand for fungicides with broad-spectrum activity, systemic properties, and resistance management capabilities.

Fungicides Market Opportunity: Development of Precision and Targeted Delivery Systems

An opportunity for market advancement lies in the development of precision and targeted delivery systems for fungicides, offering improved efficacy, reduced environmental impact, and enhanced sustainability in crop protection. Precision agriculture technologies such as drones, sensors, and GPS-guided equipment enable farmers to apply fungicides with greater accuracy, optimizing dosage rates and timing based on real-time data and crop conditions. Additionally, advances in nanotechnology, encapsulation, and formulation chemistry allow for the development of controlled-release formulations and targeted delivery systems that enhance fungicide efficacy while minimizing off-target effects and environmental contamination. By investing in research and innovation towards precision delivery solutions, fungicide manufacturers can address emerging challenges in disease management, meet the evolving needs of modern agriculture, and capitalize on opportunities for growth and differentiation in the fungicides market.

Fungicides Market Share Analysis: Chemical segment generated the highest revenue in the industry

The Chemical segment is the largest segment in the Fungicides Market, driven by diverse key factors that underscore the widespread use, effectiveness, and versatility of chemical fungicides in crop protection and disease management. Chemical fungicides are synthetic compounds formulated to control and prevent fungal diseases in crops, plants, and agricultural environments, offering reliable and targeted solutions for farmers to safeguard their yields and maximize productivity. One primary reason for the dominance of the Chemical segment is the extensive portfolio of chemical fungicides available in the market, offering a wide range of active ingredients, formulations, and application methods tailored to combat various fungal pathogens and disease pressures in different crops and growing conditions. Chemical fungicides exhibit rapid action, systemic distribution, and residual activity, providing immediate protection and long-lasting control against a broad spectrum of fungal diseases, including powdery mildew, downy mildew, rust, blight, and damping-off diseases, among others. Additionally, chemical fungicides offer flexibility in application timing, dosage rates, and treatment strategies, allowing farmers to adapt their disease management programs based on specific crop needs, disease cycles, and weather conditions, thereby optimizing disease control and minimizing yield losses. In addition, advancements in fungicide chemistry, formulation technologies, and delivery systems have led to the development of next-generation chemical fungicides with improved efficacy, environmental safety, and application convenience, addressing regulatory requirements and consumer preferences for sustainable agriculture practices. Further, the growing demand for high-quality, disease-free crops, coupled with the increasing prevalence of fungal diseases and emerging pathogens worldwide, has fueled the adoption of chemical fungicides as essential tools for integrated pest management (IPM) programs and crop protection strategies in modern agriculture. With the continuous innovation and investment in chemical fungicide research and development, along with the expanding global agriculture market, the Chemical segment of the Fungicides Market is expected to maintain its leadership position, offering farmers, agrochemical companies, and stakeholders opportunities for product innovation, market expansion, and value creation in the dynamic and competitive crop protection industry landscape.

Fungicides Market Share Analysis: Seed Treatment Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The Seed Treatment segment is the fastest-growing segment in the Fungicides Market, propelled by diverse key factors that highlight the increasing adoption of seed treatment technologies, regulatory support, and benefits in crop protection and yield enhancement. Seed treatment involves the application of fungicidal treatments to seeds before planting to protect against soil-borne and seed-borne fungal diseases, thereby promoting seedling vigor, stand establishment, and crop health from the earliest stages of plant growth. One primary reason for the rapid growth of the Seed Treatment segment is the rising awareness among farmers and agricultural stakeholders about the advantages of seed-applied fungicides in mitigating disease risks, improving plant health, and maximizing yield potential, particularly in high-value crops and intensive cropping systems. Seed treatment technologies offer targeted and localized protection to seeds and seedlings, ensuring efficient use of fungicidal active ingredients while minimizing environmental impact and exposure to non-target organisms. Additionally, seed-applied fungicides provide a cost-effective and convenient method for disease management, reducing the need for multiple foliar applications and minimizing labor, equipment, and application costs associated with traditional spray methods. In addition, regulatory approvals and industry initiatives supporting sustainable agriculture practices, integrated pest management (IPM) strategies, and seed health standards have encouraged the adoption of seed treatment technologies as integral components of modern seed production and crop protection programs. Further, advancements in seed coating formulations, encapsulation technologies, and application equipment have improved the efficacy, safety, and ease of use of seed-applied fungicides, enhancing their acceptance and adoption by farmers worldwide. With the increasing demand for high-quality, disease-resistant seeds, along with the expansion of commercial seed markets and biotechnology-driven crop improvement efforts, the Seed Treatment segment of the Fungicides Market is expected to experience significant growth, offering seed companies, agrochemical manufacturers, and farmers opportunities for innovation, market expansion, and value creation in the dynamic and competitive agricultural industry landscape.

Fungicides Market Share Analysis: Systemic Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The Systemic segment is the fastest-growing segment in the Fungicides Market, driven by diverse key factors that highlight the increasing demand for fungicides with systemic modes of action, efficacy, and sustainability benefits in crop protection and disease management. Systemic fungicides are absorbed by plants and translocated internally, providing long-lasting and broad-spectrum protection against fungal diseases through systemic circulation within plant tissues, including leaves, stems, and roots. One primary reason for the rapid growth of the Systemic segment is the effectiveness of systemic fungicides in controlling a wide range of fungal pathogens and diseases, including those that are difficult to manage with contact fungicides or traditional control methods. Systemic fungicides offer preventive and curative action against internal fungal infections, reducing disease incidence, severity, and economic losses in crops while promoting Over the forecast period plant health, growth, and productivity. Additionally, systemic fungicides provide extended residual activity and rainfastness, ensuring consistent disease protection and performance under varying environmental conditions, including periods of high humidity, rainfall, and disease pressure. In addition, advancements in fungicide chemistry, formulation technologies, and delivery systems have led to the development of novel systemic fungicides with improved efficacy, environmental safety, and application flexibility, addressing regulatory requirements and consumer preferences for sustainable agriculture practices. Further, the growing emphasis on integrated pest management (IPM) strategies, resistance management, and reduced pesticide inputs has fueled the demand for systemic fungicides as essential tools for disease control and resistance prevention in modern agriculture. With the increasing adoption of high-value crops, intensive cropping systems, and climate-resilient agricultural practices, the Systemic segment of the Fungicides Market is expected to experience significant growth, offering farmers, agrochemical companies, and stakeholders opportunities for product innovation, market expansion, and value creation in the dynamic and competitive crop protection industry landscape.

Fungicides Market Report Segmentation

By Type

Chemical

-Triazole

-Strobilurins

-Dithiocarbamates

-Chloronitriles

-Phenylamides

-Others

Biological

-Microbials

-Biochemical

-Macrobials

By Application

Seed Treatment

Soil Treatment

Foliar Spray

Post-Harvest

Others

By Mode Of Action

Contact

Systemic

By Form

Liquid

Dry

By Crop

Cereals & Grains

Oilseeds & Pulses

Fruits & Vegetables

Others

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Fungicides Companies Profiled in the Market Study

BASF SE

Bayer AG

Corteva Agriscience

FMC Corp

Isagro S.P.A

Nippon Soda Co Ltd

Nufarm

Sumitomo Chemical Co. Ltd

Syngenta AG

UPL Ltd

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Fungicides Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Fungicides Market Size Outlook, $ Million, 2021 to 2030

3.2 Fungicides Market Outlook by Type, $ Million, 2021 to 2030

3.3 Fungicides Market Outlook by Product, $ Million, 2021 to 2030

3.4 Fungicides Market Outlook by Application, $ Million, 2021 to 2030

3.5 Fungicides Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Fungicides Industry

4.2 Key Market Trends in Fungicides Industry

4.3 Potential Opportunities in Fungicides Industry

4.4 Key Challenges in Fungicides Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Fungicides Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Fungicides Market Outlook by Segments

7.1 Fungicides Market Outlook by Segments, $ Million, 2021- 2030

By Type

Chemical

-Triazole

-Strobilurins

-Dithiocarbamates

-Chloronitriles

-Phenylamides

-Others

Biological

-Microbials

-Biochemical

-Macrobials

By Application

Seed Treatment

Soil Treatment

Foliar Spray

Post-Harvest

Others

By Mode Of Action

Contact

Systemic

By Form

Liquid

Dry

By Crop

Cereals & Grains

Oilseeds & Pulses

Fruits & Vegetables

Others

8 North America Fungicides Market Analysis and Outlook To 2030

8.1 Introduction to North America Fungicides Markets in 2024

8.2 North America Fungicides Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Fungicides Market size Outlook by Segments, 2021-2030

By Type

Chemical

-Triazole

-Strobilurins

-Dithiocarbamates

-Chloronitriles

-Phenylamides

-Others

Biological

-Microbials

-Biochemical

-Macrobials

By Application

Seed Treatment

Soil Treatment

Foliar Spray

Post-Harvest

Others

By Mode Of Action

Contact

Systemic

By Form

Liquid

Dry

By Crop

Cereals & Grains

Oilseeds & Pulses

Fruits & Vegetables

Others

9 Europe Fungicides Market Analysis and Outlook To 2030

9.1 Introduction to Europe Fungicides Markets in 2024

9.2 Europe Fungicides Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Fungicides Market Size Outlook by Segments, 2021-2030

By Type

Chemical

-Triazole

-Strobilurins

-Dithiocarbamates

-Chloronitriles

-Phenylamides

-Others

Biological

-Microbials

-Biochemical

-Macrobials

By Application

Seed Treatment

Soil Treatment

Foliar Spray

Post-Harvest

Others

By Mode Of Action

Contact

Systemic

By Form

Liquid

Dry

By Crop

Cereals & Grains

Oilseeds & Pulses

Fruits & Vegetables

Others

10 Asia Pacific Fungicides Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Fungicides Markets in 2024

10.2 Asia Pacific Fungicides Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Fungicides Market size Outlook by Segments, 2021-2030

By Type

Chemical

-Triazole

-Strobilurins

-Dithiocarbamates

-Chloronitriles

-Phenylamides

-Others

Biological

-Microbials

-Biochemical

-Macrobials

By Application

Seed Treatment

Soil Treatment

Foliar Spray

Post-Harvest

Others

By Mode Of Action

Contact

Systemic

By Form

Liquid

Dry

By Crop

Cereals & Grains

Oilseeds & Pulses

Fruits & Vegetables

Others

11 South America Fungicides Market Analysis and Outlook To 2030

11.1 Introduction to South America Fungicides Markets in 2024

11.2 South America Fungicides Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Fungicides Market size Outlook by Segments, 2021-2030

By Type

Chemical

-Triazole

-Strobilurins

-Dithiocarbamates

-Chloronitriles

-Phenylamides

-Others

Biological

-Microbials

-Biochemical

-Macrobials

By Application

Seed Treatment

Soil Treatment

Foliar Spray

Post-Harvest

Others

By Mode Of Action

Contact

Systemic

By Form

Liquid

Dry

By Crop

Cereals & Grains

Oilseeds & Pulses

Fruits & Vegetables

Others

12 Middle East and Africa Fungicides Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Fungicides Markets in 2024

12.2 Middle East and Africa Fungicides Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Fungicides Market size Outlook by Segments, 2021-2030

By Type

Chemical

-Triazole

-Strobilurins

-Dithiocarbamates

-Chloronitriles

-Phenylamides

-Others

Biological

-Microbials

-Biochemical

-Macrobials

By Application

Seed Treatment

Soil Treatment

Foliar Spray

Post-Harvest

Others

By Mode Of Action

Contact

Systemic

By Form

Liquid

Dry

By Crop

Cereals & Grains

Oilseeds & Pulses

Fruits & Vegetables

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

BASF SE

Bayer AG

Corteva Agriscience

FMC Corp

Isagro S.P.A

Nippon Soda Co Ltd

Nufarm

Sumitomo Chemical Co. Ltd

Syngenta AG

UPL Ltd

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise