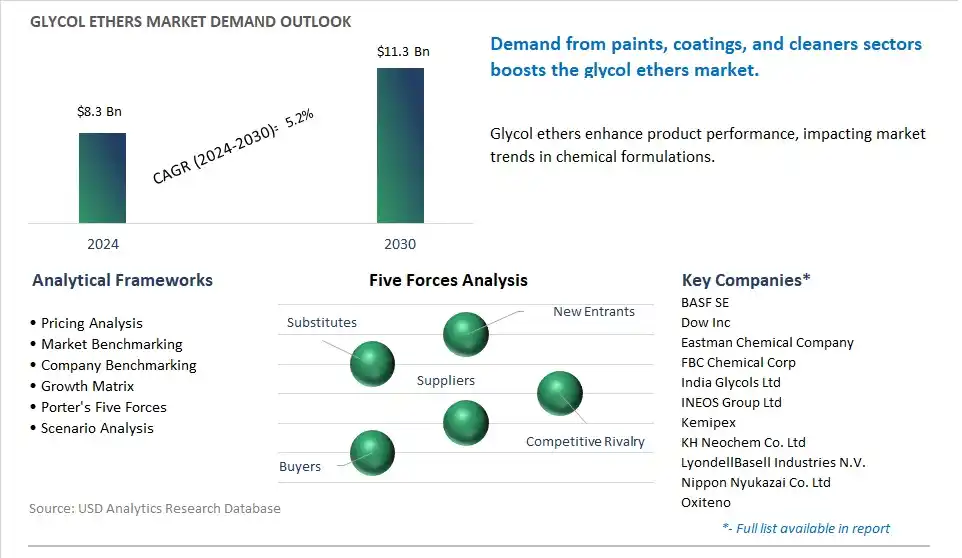

The global Glycol Ethers Market is poised to register a 5.2% CAGR from $8.3 Billion in 2024 to $11.3 Billion in 2030.

The global Glycol Ethers Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (E-Series, P-Series ), By Application (Solvent, Anti-Icing Agent, Hydraulic and Brake Fluid, Chemical Intermediate), By End-User (Paints and Coatings, Printing, Pharmaceuticals, Cosmetics and Personal Care, Adhesives, Others).

An Introduction to Global Glycol Ethers Market in 2024

The glycol ethers market is witnessing a significant shift towards environmentally friendly products, driven by increasing awareness about sustainability and stringent regulations regarding VOC emissions. Manufacturers are investing in research and development to create glycol ethers with improved performance and lower toxicity profiles. Moreover, the demand for glycol ethers is rising in various applications such as paints and coatings, adhesives, and cosmetics, fueled by expanding construction and automotive industries globally. Additionally, the market is experiencing a surge in demand for bio-based glycol ethers as consumers prioritize eco-friendly alternatives, leading to collaborations between manufacturers and bio-based chemical companies to develop sustainable solutions.

Glycol Ethers Market Competitive Landscape

The market report analyses the leading companies in the industry including BASF SE, Dow Inc, Eastman Chemical Company, FBC Chemical Corp, India Glycols Ltd, INEOS Group Ltd, Kemipex, KH Neochem Co. Ltd, LyondellBasell Industries N.V., Nippon Nyukazai Co. Ltd, Oxiteno, Recochem Inc, Royal Dutch Shell plc, Sasol Ltd.

Glycol Ethers Market Dynamics

Glycol Ethers Market Trend: Shift Towards Environmentally Friendly Solvents

A significant trend in the glycol ethers market is the shift towards environmentally friendly solvents driven by regulatory pressure, increasing awareness of health and safety concerns, and the adoption of sustainable manufacturing practices. Glycol ethers, widely used as solvents in various industrial applications including paints, coatings, cleaners, and adhesives, are facing scrutiny due to their potential health and environmental impacts. As a result, there is a growing demand for alternative solvents that offer comparable performance while posing fewer risks to human health and the environment. Manufacturers are increasingly investing in the development of eco-friendly glycol ethers with low volatility, reduced toxicity, and improved biodegradability to meet regulatory requirements and address customer concerns. This trend is reshaping the glycol ethers market towards the production and adoption of safer and more sustainable solvent solutions that align with regulatory standards and industry best practices.

Glycol Ethers Market Driver: Growth in Paints, Coatings, and Personal Care Industries

A key driver propelling the glycol ethers market is the growth in paints, coatings, and personal care industries where glycol ethers are used as essential ingredients in formulations for their solvent properties, viscosity control, and performance enhancing capabilities. In the paints and coatings sector, glycol ethers serve as effective solvents for dissolving resins, pigments, and additives, facilitating application, film formation, and drying characteristics. With the increasing demand for decorative, protective, and specialty coatings in construction, automotive, and industrial sectors, there is a steady market demand for glycol ethers as critical components in paint formulations. Similarly, in the personal care industry, glycol ethers are utilized in cosmetics, skincare, and hair care products as solvents, emulsifiers, and viscosity modifiers to enhance product stability, texture, and sensory attributes. The growth of these industries, driven by consumer preferences for high-performance and aesthetically pleasing products, fuels market demand for glycol ethers, driving growth and opportunities for manufacturers and suppliers.

Glycol Ethers Market Opportunity: Development of Bio-based and Renewable Glycol Ethers

An opportunity for market expansion lies in the development of bio-based and renewable glycol ethers as sustainable alternatives to petroleum-derived solvents, offering solutions for environmental sustainability and reducing dependence on fossil fuels. With increasing regulatory focus on reducing volatile organic compound (VOC) emissions and promoting green chemistry practices, there is growing interest in bio-based glycol ethers derived from renewable feedstocks such as biomass, sugars, and plant oils. Bio-based glycol ethers can be produced through fermentation, enzymatic processes, or chemical conversion technologies, offering similar performance characteristics to petroleum-derived glycol ethers while reducing environmental impact and carbon footprint. By investing in research and development and collaborating with biotechnology and chemical engineering partners, glycol ethers manufacturers can capitalize on opportunities to develop bio-based solvents, enter sustainable markets, and meet the growing demand for environmentally friendly and renewable solutions, driving growth and innovation in the glycol ethers market.

Glycol Ethers Market Share Analysis: E-Series segment generated the highest revenue in the industry

The E-series segment is the largest segment in the glycol ethers market, primarily due to its wider range of applications and higher demand across various industries. E-series glycol ethers are derived from ethylene oxide and are characterized by their excellent solvency and compatibility with a wide range of materials. They are commonly used as solvents in paints, coatings, cleaning products, and industrial processes due to their ability to dissolve a variety of organic and inorganic compounds. E-series glycol ethers offer advantages such as fast evaporation rates, low odor, and low volatility, making them suitable for use in formulations where rapid drying, minimal odor, and low emissions are desired. Additionally, E-series glycol ethers exhibit good surface wetting properties, which improve the spread and adhesion of coatings and formulations, enhancing their performance and durability. In addition, E-series glycol ethers are cost-effective and readily available, further contributing to their dominance in the glycol ethers market. Over the forecast period, the versatile solvency, compatibility, and cost-effectiveness of E-series glycol ethers make them the preferred choice for a wide range of industrial applications, leading to their dominance as the largest segment in the glycol ethers market.

Glycol Ethers Market Share Analysis: Anti-Icing Agent Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The anti-icing agent segment is the fastest-growing segment in the glycol ethers market, driven by diverse key factors. The there is a growing demand for anti-icing agents, particularly in regions where cold temperatures and winter weather conditions pose challenges to transportation and infrastructure. Glycol ethers, such as ethylene glycol and propylene glycol, are widely used as key components in anti-icing and de-icing solutions applied to roads, airport runways, and aircraft surfaces to prevent the formation of ice and snow buildup. As the need for effective ice control measures increases to ensure safety and maintain operational efficiency, the demand for glycol ethers as anti-icing agents is also on the rise. Secondly, advancements in anti-icing technologies and formulations are driving the adoption of glycol ethers with enhanced performance characteristics, such as improved ice-melting capabilities, reduced environmental impact, and increased longevity. Glycol ethers offer advantages such as low freezing points, high solubility in water, and compatibility with corrosion inhibitors, making them effective and versatile components in anti-icing formulations. Additionally, stringent regulations and environmental concerns regarding the use of traditional salt-based de-icing agents are prompting the development and adoption of alternative solutions based on glycol ethers, which offer safer and more environmentally friendly alternatives. In addition, the expansion of transportation infrastructure, including airports, highways, and railways, further drives the demand for anti-icing agents and glycol ethers as essential components in ice control systems. Over the forecast period, the combination of increasing demand for effective ice control measures, technological advancements, and regulatory pressures positions the anti-icing agent segment as the fastest-growing segment in the glycol ethers market.

Glycol Ethers Market Share Analysis: Paints and Coatings Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The paints and coatings segment is the fastest-growing segment in the glycol ethers market, driven by diverse key factors. The there is a growing demand for paints and coatings across various industries, including construction, automotive, aerospace, and manufacturing. Paints and coatings are essential for protecting surfaces, enhancing aesthetics, and providing functional properties such as corrosion resistance, weatherability, and durability. Glycol ethers, particularly E-series glycol ethers, are widely used as solvents and coalescing agents in paint and coating formulations due to their excellent solvency, compatibility, and performance characteristics. They help to dissolve resins, pigments, and additives, improve film formation, and enhance the flow and leveling properties of coatings, resulting in high-quality finishes and coatings with superior performance properties. Secondly, advancements in paint and coating technologies, such as waterborne and high-solids formulations, are driving the adoption of glycol ethers with enhanced environmental and performance benefits. Glycol ethers offer advantages such as low volatility, low odor, and low toxicity, making them suitable for use in eco-friendly and low-VOC (volatile organic compound) coatings that comply with stringent environmental regulations. Additionally, glycol ethers contribute to the development of coatings with improved adhesion, flexibility, and resistance to chemicals and abrasion, meeting the evolving needs of end-users across diverse industries. In addition, the expansion of construction and infrastructure projects, as well as the automotive and aerospace industries, further fuels the demand for paints and coatings and drives the growth of the glycol ethers market. Over the forecast period, the combination of increasing demand for high-performance coatings, technological advancements, and environmental regulations positions the paints and coatings segment as the fastest-growing segment in the glycol ethers market.

Glycol Ethers Market Report Segmentation

By Type

E-Series

-Methyl Glycol Ether

-Ethyl Glycol Ether

-Butyl Glycol Ether

P-Series

-Propylene Glycol Monomethyl Ether (PM)

-Dipropylene Glycol Monomethyl Ether (DPM)

-Tripropylene Glycol Monomethyl Ether (TPM)

-Others

By Application

Solvent

Anti-Icing Agent

Hydraulic and Brake Fluid

Chemical Intermediate

By End-User

Paints and Coatings

Printing

Pharmaceuticals

Cosmetics and Personal Care

Adhesives

Others

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Glycol Ethers Companies Profiled in the Market Study

BASF SE

Dow Inc

Eastman Chemical Company

FBC Chemical Corp

India Glycols Ltd

INEOS Group Ltd

Kemipex

KH Neochem Co. Ltd

LyondellBasell Industries N.V.

Nippon Nyukazai Co. Ltd

Oxiteno

Recochem Inc

Royal Dutch Shell plc

Sasol Ltd

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Glycol Ethers Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Glycol Ethers Market Size Outlook, $ Million, 2021 to 2030

3.2 Glycol Ethers Market Outlook by Type, $ Million, 2021 to 2030

3.3 Glycol Ethers Market Outlook by Product, $ Million, 2021 to 2030

3.4 Glycol Ethers Market Outlook by Application, $ Million, 2021 to 2030

3.5 Glycol Ethers Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Glycol Ethers Industry

4.2 Key Market Trends in Glycol Ethers Industry

4.3 Potential Opportunities in Glycol Ethers Industry

4.4 Key Challenges in Glycol Ethers Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Glycol Ethers Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Glycol Ethers Market Outlook by Segments

7.1 Glycol Ethers Market Outlook by Segments, $ Million, 2021- 2030

By Type

E-Series

-Methyl Glycol Ether

-Ethyl Glycol Ether

-Butyl Glycol Ether

P-Series

-Propylene Glycol Monomethyl Ether (PM)

-Dipropylene Glycol Monomethyl Ether (DPM)

-Tripropylene Glycol Monomethyl Ether (TPM)

-Others

By Application

Solvent

Anti-Icing Agent

Hydraulic and Brake Fluid

Chemical Intermediate

By End-User

Paints and Coatings

Printing

Pharmaceuticals

Cosmetics and Personal Care

Adhesives

Others

8 North America Glycol Ethers Market Analysis and Outlook To 2030

8.1 Introduction to North America Glycol Ethers Markets in 2024

8.2 North America Glycol Ethers Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Glycol Ethers Market size Outlook by Segments, 2021-2030

By Type

E-Series

-Methyl Glycol Ether

-Ethyl Glycol Ether

-Butyl Glycol Ether

P-Series

-Propylene Glycol Monomethyl Ether (PM)

-Dipropylene Glycol Monomethyl Ether (DPM)

-Tripropylene Glycol Monomethyl Ether (TPM)

-Others

By Application

Solvent

Anti-Icing Agent

Hydraulic and Brake Fluid

Chemical Intermediate

By End-User

Paints and Coatings

Printing

Pharmaceuticals

Cosmetics and Personal Care

Adhesives

Others

9 Europe Glycol Ethers Market Analysis and Outlook To 2030

9.1 Introduction to Europe Glycol Ethers Markets in 2024

9.2 Europe Glycol Ethers Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Glycol Ethers Market Size Outlook by Segments, 2021-2030

By Type

E-Series

-Methyl Glycol Ether

-Ethyl Glycol Ether

-Butyl Glycol Ether

P-Series

-Propylene Glycol Monomethyl Ether (PM)

-Dipropylene Glycol Monomethyl Ether (DPM)

-Tripropylene Glycol Monomethyl Ether (TPM)

-Others

By Application

Solvent

Anti-Icing Agent

Hydraulic and Brake Fluid

Chemical Intermediate

By End-User

Paints and Coatings

Printing

Pharmaceuticals

Cosmetics and Personal Care

Adhesives

Others

10 Asia Pacific Glycol Ethers Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Glycol Ethers Markets in 2024

10.2 Asia Pacific Glycol Ethers Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Glycol Ethers Market size Outlook by Segments, 2021-2030

By Type

E-Series

-Methyl Glycol Ether

-Ethyl Glycol Ether

-Butyl Glycol Ether

P-Series

-Propylene Glycol Monomethyl Ether (PM)

-Dipropylene Glycol Monomethyl Ether (DPM)

-Tripropylene Glycol Monomethyl Ether (TPM)

-Others

By Application

Solvent

Anti-Icing Agent

Hydraulic and Brake Fluid

Chemical Intermediate

By End-User

Paints and Coatings

Printing

Pharmaceuticals

Cosmetics and Personal Care

Adhesives

Others

11 South America Glycol Ethers Market Analysis and Outlook To 2030

11.1 Introduction to South America Glycol Ethers Markets in 2024

11.2 South America Glycol Ethers Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Glycol Ethers Market size Outlook by Segments, 2021-2030

By Type

E-Series

-Methyl Glycol Ether

-Ethyl Glycol Ether

-Butyl Glycol Ether

P-Series

-Propylene Glycol Monomethyl Ether (PM)

-Dipropylene Glycol Monomethyl Ether (DPM)

-Tripropylene Glycol Monomethyl Ether (TPM)

-Others

By Application

Solvent

Anti-Icing Agent

Hydraulic and Brake Fluid

Chemical Intermediate

By End-User

Paints and Coatings

Printing

Pharmaceuticals

Cosmetics and Personal Care

Adhesives

Others

12 Middle East and Africa Glycol Ethers Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Glycol Ethers Markets in 2024

12.2 Middle East and Africa Glycol Ethers Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Glycol Ethers Market size Outlook by Segments, 2021-2030

By Type

E-Series

-Methyl Glycol Ether

-Ethyl Glycol Ether

-Butyl Glycol Ether

P-Series

-Propylene Glycol Monomethyl Ether (PM)

-Dipropylene Glycol Monomethyl Ether (DPM)

-Tripropylene Glycol Monomethyl Ether (TPM)

-Others

By Application

Solvent

Anti-Icing Agent

Hydraulic and Brake Fluid

Chemical Intermediate

By End-User

Paints and Coatings

Printing

Pharmaceuticals

Cosmetics and Personal Care

Adhesives

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

BASF SE

Dow Inc

Eastman Chemical Company

FBC Chemical Corp

India Glycols Ltd

INEOS Group Ltd

Kemipex

KH Neochem Co. Ltd

LyondellBasell Industries N.V.

Nippon Nyukazai Co. Ltd

Oxiteno

Recochem Inc

Royal Dutch Shell plc

Sasol Ltd

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

E-Series

-Methyl Glycol Ether

-Ethyl Glycol Ether

-Butyl Glycol Ether

P-Series

-Propylene Glycol Monomethyl Ether (PM)

-Dipropylene Glycol Monomethyl Ether (DPM)

-Tripropylene Glycol Monomethyl Ether (TPM)

-Others

By Application

Solvent

Anti-Icing Agent

Hydraulic and Brake Fluid

Chemical Intermediate

By End-User

Paints and Coatings

Printing

Pharmaceuticals

Cosmetics and Personal Care

Adhesives

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)