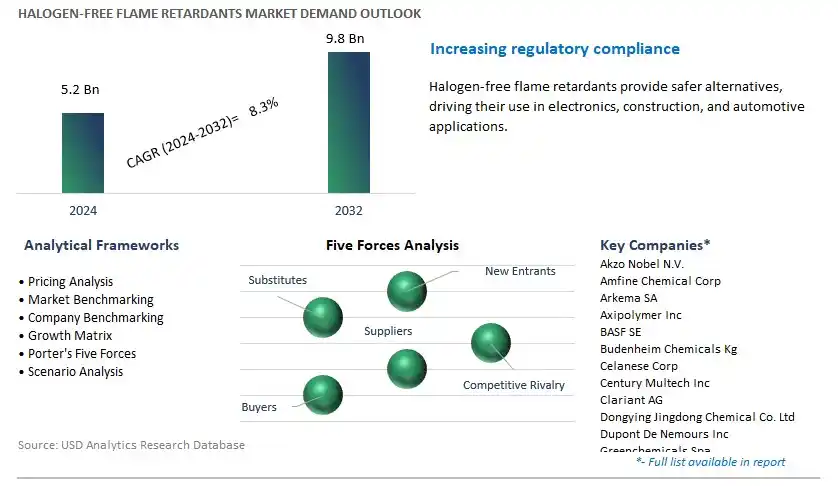

Global Halogen-Free Flame Retardants Market Size is valued at $5.2 Billion in 2024 and is forecast to register a growth rate (CAGR) of 8.3% to reach $9.8 Billion by 2032.

The global Halogen-Free Flame Retardants Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (Aluminum hydroxide, Organophosphorous, Others), By Application (Polyolefins, Epoxy resin, Unsaturated polyester, Polyvinyl chloride, Rubber, Engineered thermoplastic, Styrenics, Others), By End-User (Electrical & electronics, Building & construction, Transportation, Others).

An Introduction to Halogen-Free Flame Retardants Market in 2024

Halogen-free flame retardants represent a class of additives used to impart flame resistance to various polymers and materials without relying on halogen compounds such as bromine and chlorine, which pose environmental and health concerns. In 2024, the market for halogen-free flame retardants is experiencing rapid growth driven by increasing regulatory restrictions on halogenated flame retardants, as well as growing awareness of their adverse effects on human health and the environment. These flame retardants, based on phosphorus, nitrogen, or mineral compounds, offer advantages such as reduced smoke emission, improved fire safety performance, and compliance with eco-label certifications. Further, advancements in halogen-free flame retardant formulations and processing technologies ensure compatibility with diverse polymers and applications, fostering adoption across industries such as electronics, construction, and automotive. As stakeholders prioritize sustainability and safety in material selection and product development, the demand for halogen-free flame retardants is expected to soar, driving further research and market expansion.

Halogen-Free Flame Retardants Market Competitive Landscape

The market report analyses the leading companies in the industry including Akzo Nobel N.V., Amfine Chemical Corp, Arkema SA, Axipolymer Inc, BASF SE, Budenheim Chemicals Kg, Celanese Corp, Century Multech Inc, Clariant AG, Dongying Jingdong Chemical Co. Ltd, Dupont De Nemours Inc, Greenchemicals Spa, Gulec Chemicals GmbH, Huber Engineered Materials, Israel Chemicals Ltd, Italmatch Chemicals S.P.A., Kisuma Chemicals Bv, Lanxess AG, Nabaltec AG, Polyplastics Co. Ltd, Presafer Phosphor Chemical Co. Ltd, Qingdao Fundchem Co. Ltd, Rtp Company, Stahl Holdings B.V., Thor Company, and others.

Halogen-Free Flame Retardants Market Dynamics

Market Trend: Shift Towards Sustainable and Environmentally Friendly Solutions

One prominent trend in the market for Halogen-Free Flame Retardants is the notable shift towards sustainable and environmentally friendly alternatives across various industries. With increasing awareness of the environmental and health hazards associated with halogenated flame retardants, there's a growing demand for safer and more sustainable options. Halogen-free flame retardants offer comparable fire protection performance without the harmful effects of halogens, making them increasingly preferred by manufacturers and consumers alike. This trend is driven by stringent regulations, consumer preferences for eco-friendly products, and corporate sustainability initiatives, shaping the market towards greener solutions that meet fire safety requirements while minimizing environmental impact.

Market Driver: Regulatory Pressure and Compliance Mandates

A significant driver propelling the growth of the market for Halogen-Free Flame Retardants is the regulatory pressure and compliance mandates aimed at reducing the use of halogenated flame retardants in various applications. Governments worldwide are implementing stricter regulations and bans on halogen-containing chemicals due to concerns about their persistence, bioaccumulation, and toxicity. Regulatory frameworks such as REACH in the European Union and regulations like California's TB117-2013 and TB133 drive the adoption of safer alternatives, spurring the demand for halogen-free flame retardants. Manufacturers are compelled to reformulate their products to meet these regulatory requirements, creating opportunities for innovation and market expansion in the halogen-free flame retardant industry.

Market Opportunity: Expansion in Building and Construction Sector

An opportunity within the market for Halogen-Free Flame Retardants lies in the expansion into the building and construction sector, where fire safety regulations and green building standards drive the demand for safer and environmentally friendly materials. Halogen-free flame retardants offer a viable solution for architects, builders, and developers seeking to meet stringent fire safety codes while adhering to sustainability goals. With the construction industry embracing eco-friendly practices and certifications such as LEED (Leadership in Energy and Environmental Design), there's a growing market opportunity for halogen-free flame retardants in applications such as insulation, flooring, coatings, and textiles. By targeting this sector and offering innovative flame retardant solutions tailored to the specific needs of the construction industry, manufacturers can capitalize on the increasing demand for sustainable building materials and contribute to safer, greener construction practices.

Halogen-Free Flame Retardants Market Share Analysis: Aluminum Hydroxide segment generated the highest revenue in 2024

The aluminum hydroxide segment stands as the largest in the Halogen-Free Flame Retardants Market. In particular, aluminum hydroxide is one of the most commonly used halogen-free flame retardants due to its excellent flame retardant properties, environmental safety, and wide availability. Aluminum hydroxide functions as a flame retardant by releasing water vapor and inert gases when exposed to high temperatures, diluting the combustible gases and suppressing the flame. Additionally, aluminum hydroxide acts as a heat sink, absorbing heat from the surrounding environment and reducing the temperature of the material, further inhibiting the spread of fire. This mechanism of action makes aluminum hydroxide highly effective in improving the fire safety performance of various materials, including plastics, rubbers, textiles, and coatings. Moreover, aluminum hydroxide is non-toxic, non-corrosive, and environmentally friendly, making it suitable for use in applications where safety, health, and environmental concerns are paramount. Furthermore, aluminum hydroxide is cost-effective and readily available in large quantities, ensuring a stable and reliable supply chain for manufacturers and end-users. As industries continue to prioritize fire safety and environmental sustainability, the demand for halogen-free flame retardants such as aluminum hydroxide is expected to remain strong, solidifying the segment's position as the largest in the market.

Halogen-Free Flame Retardants Market Share Analysis: Polyolefins is poised to register the fastest CAGR over the forecast period

The polyolefins segment is the fastest-growing segment in the Halogen-Free Flame Retardants Market. In particular, polyolefins, such as polyethylene (PE) and polypropylene (PP), are widely used in various industries due to their excellent mechanical properties, chemical resistance, and versatility. However, polyolefins are highly flammable materials, making them susceptible to fire hazards. Therefore, there is a growing demand for halogen-free flame retardants to enhance the fire safety performance of polyolefin-based products. Additionally, stringent regulations and standards mandate the use of flame retardant additives in polyolefin applications, especially in building and construction, transportation, and electronics sectors where fire safety is critical. Moreover, halogen-free flame retardants offer advantages such as low toxicity, reduced smoke generation, and environmental compatibility compared to halogenated flame retardants, making them suitable for applications where safety, health, and environmental concerns are paramount. Furthermore, advancements in flame retardant technologies and formulations have led to the development of highly efficient and cost-effective solutions specifically tailored for polyolefins, ensuring optimal performance without compromising material properties or processing characteristics. As industries continue to prioritize fire safety, regulatory compliance, and environmental sustainability, the demand for halogen-free flame retardants in polyolefin applications is expected to continue growing rapidly, making it the fastest-growing segment in the market.

Halogen-Free Flame Retardants Market Share Analysis: Electrical & Electronics segment generated the highest revenue in 2024

The electrical & electronics segment stands as the largest in the Halogen-Free Flame Retardants Market. In particular, electrical and electronic products require flame retardant materials to comply with safety standards and regulations, as they are susceptible to fire hazards due to the presence of electrical components and circuits. Halogen-free flame retardants are preferred in this sector due to their superior fire safety performance and environmental compatibility compared to halogenated alternatives. Additionally, the electrical and electronics industry encompasses a wide range of products such as consumer electronics, appliances, wiring cables, circuit boards, and automotive electronics, all of which require flame retardant materials to mitigate the risk of fire accidents. Moreover, the miniaturization and increasing complexity of electronic devices require flame retardant solutions that offer high performance without compromising other material properties such as mechanical strength, thermal conductivity, and electrical insulation. Furthermore, stringent regulations and standards such as RoHS (Restriction of Hazardous Substances) and WEEE (Waste Electrical and Electronic Equipment) drive the adoption of halogen-free flame retardants in the electrical and electronics sector, ensuring compliance with environmental and health regulations. As the demand for electronic products continues to grow globally, the need for halogen-free flame retardants in this sector is expected to remain strong, solidifying the electrical & electronics segment as the largest in the market.

Halogen-Free Flame Retardants Market Share Analysis: Building & Construction segment generated the highest revenue in 2024

The building & construction segment stands as the largest in the Halogen-Free Flame Retardants Market. In particular, building materials and construction products require flame retardant additives to meet safety regulations and standards, as buildings are susceptible to fire hazards during construction, occupancy, and in the event of fire incidents. Halogen-free flame retardants are preferred in the construction industry due to their superior fire safety performance and environmental compatibility compared to halogenated alternatives. Additionally, the building & construction sector encompasses a wide range of applications such as insulation materials, coatings, sealants, adhesives, and structural components, all of which require flame retardant properties to enhance fire safety. Moreover, with increasing urbanization, population growth, and infrastructure development projects worldwide, there is a growing demand for flame retardant materials in building and construction applications to ensure the safety and durability of structures. Furthermore, regulatory requirements and building codes mandate the use of flame retardant additives in construction materials to minimize the risk of fire accidents and protect lives and property. As the construction industry continues to expand globally, the demand for halogen-free flame retardants in building and construction applications is expected to remain strong, solidifying the building & construction segment as the largest in the market.

Halogen-Free Flame Retardants Market

By Type

Aluminum hydroxide

Organophosphorous

Others

By Application

Polyolefins

Epoxy resin

Unsaturated polyester

Polyvinyl chloride

Rubber

Engineered thermoplastic

Styrenics

Others

By End-User

Electrical & electronics

Building & construction

Transportation

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Halogen Free Flame Retardants Companies Profiled in the Study

Akzo Nobel N.V.

Amfine Chemical Corp

Arkema SA

Axipolymer Inc

BASF SE

Budenheim Chemicals Kg

Celanese Corp

Century Multech Inc

Clariant AG

Dongying Jingdong Chemical Co. Ltd

Dupont De Nemours Inc

Greenchemicals Spa

Gulec Chemicals GmbH

Huber Engineered Materials

Israel Chemicals Ltd

Italmatch Chemicals S.P.A.

Kisuma Chemicals Bv

Lanxess AG

Nabaltec AG

Polyplastics Co. Ltd

Presafer Phosphor Chemical Co. Ltd

Qingdao Fundchem Co. Ltd

Rtp Company

Stahl Holdings B.V.

Thor Company

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Halogen Free Flame Retardants Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Halogen Free Flame Retardants Market Size Outlook, $ Million, 2021 to 2032

3.2 Halogen Free Flame Retardants Market Outlook by Type, $ Million, 2021 to 2032

3.3 Halogen Free Flame Retardants Market Outlook by Product, $ Million, 2021 to 2032

3.4 Halogen Free Flame Retardants Market Outlook by Application, $ Million, 2021 to 2032

3.5 Halogen Free Flame Retardants Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Halogen Free Flame Retardants Industry

4.2 Key Market Trends in Halogen Free Flame Retardants Industry

4.3 Potential Opportunities in Halogen Free Flame Retardants Industry

4.4 Key Challenges in Halogen Free Flame Retardants Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Halogen Free Flame Retardants Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Halogen Free Flame Retardants Market Outlook by Segments

7.1 Halogen Free Flame Retardants Market Outlook by Segments, $ Million, 2021- 2032

By Type

Aluminum hydroxide

Organophosphorous

Others

By Application

Polyolefins

Epoxy resin

Unsaturated polyester

Polyvinyl chloride

Rubber

Engineered thermoplastic

Styrenics

Others

By End-User

Electrical & electronics

Building & construction

Transportation

Others

8 North America Halogen Free Flame Retardants Market Analysis and Outlook To 2032

8.1 Introduction to North America Halogen Free Flame Retardants Markets in 2024

8.2 North America Halogen Free Flame Retardants Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Halogen Free Flame Retardants Market size Outlook by Segments, 2021-2032

By Type

Aluminum hydroxide

Organophosphorous

Others

By Application

Polyolefins

Epoxy resin

Unsaturated polyester

Polyvinyl chloride

Rubber

Engineered thermoplastic

Styrenics

Others

By End-User

Electrical & electronics

Building & construction

Transportation

Others

9 Europe Halogen Free Flame Retardants Market Analysis and Outlook To 2032

9.1 Introduction to Europe Halogen Free Flame Retardants Markets in 2024

9.2 Europe Halogen Free Flame Retardants Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Halogen Free Flame Retardants Market Size Outlook by Segments, 2021-2032

By Type

Aluminum hydroxide

Organophosphorous

Others

By Application

Polyolefins

Epoxy resin

Unsaturated polyester

Polyvinyl chloride

Rubber

Engineered thermoplastic

Styrenics

Others

By End-User

Electrical & electronics

Building & construction

Transportation

Others

10 Asia Pacific Halogen Free Flame Retardants Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Halogen Free Flame Retardants Markets in 2024

10.2 Asia Pacific Halogen Free Flame Retardants Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Halogen Free Flame Retardants Market size Outlook by Segments, 2021-2032

By Type

Aluminum hydroxide

Organophosphorous

Others

By Application

Polyolefins

Epoxy resin

Unsaturated polyester

Polyvinyl chloride

Rubber

Engineered thermoplastic

Styrenics

Others

By End-User

Electrical & electronics

Building & construction

Transportation

Others

11 South America Halogen Free Flame Retardants Market Analysis and Outlook To 2032

11.1 Introduction to South America Halogen Free Flame Retardants Markets in 2024

11.2 South America Halogen Free Flame Retardants Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Halogen Free Flame Retardants Market size Outlook by Segments, 2021-2032

By Type

Aluminum hydroxide

Organophosphorous

Others

By Application

Polyolefins

Epoxy resin

Unsaturated polyester

Polyvinyl chloride

Rubber

Engineered thermoplastic

Styrenics

Others

By End-User

Electrical & electronics

Building & construction

Transportation

Others

12 Middle East and Africa Halogen Free Flame Retardants Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Halogen Free Flame Retardants Markets in 2024

12.2 Middle East and Africa Halogen Free Flame Retardants Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Halogen Free Flame Retardants Market size Outlook by Segments, 2021-2032

By Type

Aluminum hydroxide

Organophosphorous

Others

By Application

Polyolefins

Epoxy resin

Unsaturated polyester

Polyvinyl chloride

Rubber

Engineered thermoplastic

Styrenics

Others

By End-User

Electrical & electronics

Building & construction

Transportation

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Akzo Nobel N.V.

Amfine Chemical Corp

Arkema SA

Axipolymer Inc

BASF SE

Budenheim Chemicals Kg

Celanese Corp

Century Multech Inc

Clariant AG

Dongying Jingdong Chemical Co. Ltd

Dupont De Nemours Inc

Greenchemicals Spa

Gulec Chemicals GmbH

Huber Engineered Materials

Israel Chemicals Ltd

Italmatch Chemicals S.P.A.

Kisuma Chemicals Bv

Lanxess AG

Nabaltec AG

Polyplastics Co. Ltd

Presafer Phosphor Chemical Co. Ltd

Qingdao Fundchem Co. Ltd

Rtp Company

Stahl Holdings B.V.

Thor Company

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

Aluminum hydroxide

Organophosphorous

Others

By Application

Polyolefins

Epoxy resin

Unsaturated polyester

Polyvinyl chloride

Rubber

Engineered thermoplastic

Styrenics

Others

By End-User

Electrical & electronics

Building & construction

Transportation

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)