The global Heat Meter Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (Static, Mechanical), By Connectivity (Wired, Wireless), By End-User (Residential, Commercial, Industrial).

Heat meters play a crucial role in measuring and billing energy usage in heating systems, district heating networks, and renewable energy installations, enabling efficient energy management and cost allocation. One key trend shaping the future of the heat meter industry is the integration of advanced metering technologies and smart communication systems to enable real-time monitoring, data analytics, and remote management of heat consumption. Manufacturers are developing ultrasonic heat meters, electromagnetic flow meters, and thermal mass flow meters with high accuracy and reliability, capable of measuring heat energy usage with precision in diverse applications and operating conditions. Additionally, the implementation of wireless communication protocols such as LoRaWAN and NB-IoT is facilitating seamless integration of heat meters into smart grid infrastructure, enabling automated meter reading, demand response, and energy optimization initiatives. Moreover, the emphasis on energy efficiency and sustainability is driving the adoption of heat meters in green building projects, eco-districts, and renewable energy systems, enabling stakeholders to monitor and optimize energy consumption, reduce carbon footprint, and meet sustainability goals. As governments and utilities worldwide prioritize energy conservation and carbon reduction initiatives, the heat meter industry is poised for growth, with opportunities for innovation, standardization, and market expansion to support the transition towards a more sustainable and efficient energy future.

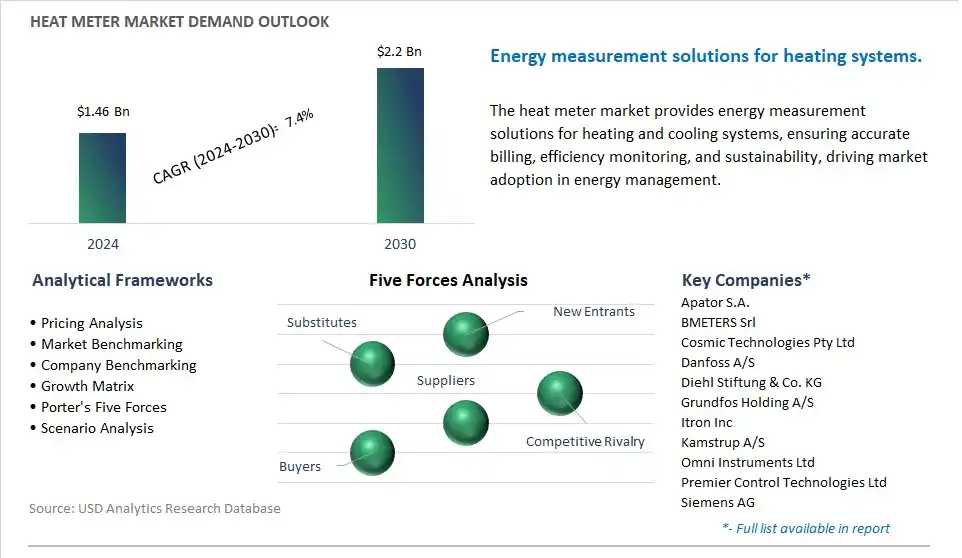

The market report analyses the leading companies in the industry including Apator S.A., BMETERS Srl, Cosmic Technologies Pty Ltd, Danfoss A/S, Diehl Stiftung & Co. KG, Grundfos Holding A/S, Itron Inc, Kamstrup A/S, Omni Instruments Ltd, Premier Control Technologies Ltd, Siemens AG, Spire Metering Technology LLC, Sycous Ltd, Trend Control Systems Ltd, Zenner International GmbH & Co. KG.

A prominent trend in the market for Heat Meters is the increasing demand for energy efficiency solutions in residential, commercial, and industrial buildings. As concerns about energy consumption, environmental sustainability, and utility costs continue to rise, there is growing interest in monitoring and optimizing heating systems to improve energy efficiency and reduce carbon emissions. Heat meters play a crucial role in accurately measuring and monitoring heat energy consumption, providing valuable data for energy management, billing, and conservation efforts. This is driven by regulatory initiatives, building energy efficiency standards, and incentives for energy conservation, leading to increased adoption of heat meters in heating, ventilation, and air conditioning (HVAC) systems across various sectors.

The market for Heat Meters is being driven by regulatory mandates and energy management initiatives that promote the use of heat meters for energy efficiency and conservation. Governments, utilities, and building owners are implementing policies and programs to encourage the installation of heat meters in new and existing buildings to comply with energy efficiency regulations, track energy consumption, and incentivize energy conservation measures. Additionally, energy management initiatives such as building automation systems, smart grid technologies, and district heating networks rely on heat meters to accurately measure and allocate heat energy usage, optimize heating system performance, and reduce energy waste. This driver is further fueled by advancements in heat meter technology, metering accuracy, and data analytics capabilities, which enable real-time monitoring, analysis, and optimization of heating systems for energy savings and environmental sustainability.

An exciting opportunity within the market for Heat Meters lies in the integration with smart building and IoT (Internet of Things) technologies to enable data-driven energy management and optimization solutions. Companies can leverage advancements in wireless communication, sensor technology, and cloud-based platforms to develop smart heat metering systems that provide real-time data analytics, remote monitoring, and predictive maintenance capabilities. By integrating heat meters with building automation systems, energy management software, and smart home devices, building owners and operators can gain insights into heating system performance, identify energy-saving opportunities, and adjust heating settings based on occupancy patterns, weather conditions, and energy demand. Furthermore, there is potential to offer value-added services such as energy audits, demand response programs, and energy performance contracting to help customers achieve their energy efficiency goals and reduce operational costs. By embracing innovation and collaboration with technology partners, companies can capitalize on the growing demand for smart heat metering solutions and unlock opportunities in the evolving market for energy management and sustainability.

The largest segment in the Heat Meter Market is the "Static" type segment. This is because static heat meters, also known as ultrasonic heat meters, have gained significant popularity and market share in recent years due to their advanced technology and numerous advantages over mechanical heat meters. Static heat meters utilize ultrasonic sensors to measure the flow rate and temperature difference of the heat transfer fluid, allowing for highly accurate and reliable measurement of energy consumption in heating and cooling systems. Additionally, static heat meters are non-intrusive, meaning they do not contain moving parts that can wear out over time, leading to increased durability and longevity. In addition, static heat meters offer benefits such as low maintenance requirements, high precision, wide measurement range, and compatibility with various heat transfer fluids and system configurations. Further, static heat meters are often equipped with advanced features such as data logging, remote monitoring, and communication interfaces, enabling integration with building energy management systems and facilitating energy efficiency initiatives. As a result of these advantages, static heat meters have become the preferred choice for utilities, property managers, and building owners seeking accurate, reliable, and cost-effective solutions for heat energy measurement and billing. Therefore, the Static type segment is the largest in the Heat Meter Market due to its widespread adoption and superior performance compared to mechanical heat meters.

The fastest-growing segment in the Heat Meter Market is the "Wireless Connectivity" segment. This growth is driven by wireless connectivity offers numerous advantages over traditional wired connections, including flexibility, scalability, and ease of installation. Wireless heat meters eliminate the need for complex wiring infrastructure, making them ideal for retrofitting existing buildings and installations where wired connections may be challenging or impractical. Additionally, wireless connectivity enables real-time data transmission and remote monitoring of heat energy consumption, providing building owners, facility managers, and utilities with valuable insights into energy usage patterns and trends. This facilitates proactive energy management strategies, including demand response, load balancing, and energy optimization, leading to improved efficiency and cost savings. In addition, the increasing adoption of smart building technologies and Internet of Things (IoT) solutions drives the demand for wireless heat meters, as they can seamlessly integrate with other building systems and sensors to create interconnected and intelligent environments. Further, advancements in wireless communication protocols, such as Zigbee, Wi-Fi, and LoRaWAN, enhance the reliability, range, and security of wireless heat metering systems, further fueling their adoption in various applications. As a result, the Wireless Connectivity segment in the Heat Meter Market is expected to experience rapid growth, driven by increasing demand for flexible, efficient, and connected solutions for heat energy measurement and management in buildings and industrial installations.

The fastest-growing segment in the Heat Meter Market is the "Commercial" segment. This growth is driven by commercial buildings, such as office complexes, retail centers, and hotels, have high energy consumption levels due to their large size, extensive HVAC systems, and round-the-clock operation. As a result, there is a growing demand for heat meters in commercial buildings to accurately measure and monitor energy usage for heating and cooling purposes. Additionally, commercial buildings are subject to stringent energy efficiency regulations and sustainability goals, driving the adoption of heat metering systems as part of energy management strategies to optimize resource utilization and reduce operating costs. Further, the increasing focus on occupant comfort, indoor air quality, and building performance in commercial facilities necessitates the implementation of advanced metering and monitoring solutions, including heat meters, to ensure optimal thermal comfort and energy efficiency. In addition, advancements in technology, such as the integration of wireless connectivity, data analytics, and cloud-based platforms, make heat metering systems more accessible, scalable, and cost-effective for commercial building owners and operators. Further, the trend toward smart buildings and IoT-enabled solutions accelerates the adoption of heat meters in commercial settings, as they enable real-time monitoring, remote management, and predictive maintenance of HVAC systems. As a result, the Commercial segment in the Heat Meter Market is expected to experience rapid growth, driven by increasing demand for energy-efficient and sustainable solutions in the commercial building sector.

By Type

Static

Mechanical

By Connectivity

Wired

Wireless

By End-User

Residential

Commercial

Industrial

Apator S.A.

BMETERS Srl

Cosmic Technologies Pty Ltd

Danfoss A/S

Diehl Stiftung & Co. KG

Grundfos Holding A/S

Itron Inc

Kamstrup A/S

Omni Instruments Ltd

Premier Control Technologies Ltd

Siemens AG

Spire Metering Technology LLC

Sycous Ltd

Trend Control Systems Ltd

Zenner International GmbH & Co. KG

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Heat Meter Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Heat Meter Market Size Outlook, $ Million, 2021 to 2030

3.2 Heat Meter Market Outlook by Type, $ Million, 2021 to 2030

3.3 Heat Meter Market Outlook by Product, $ Million, 2021 to 2030

3.4 Heat Meter Market Outlook by Application, $ Million, 2021 to 2030

3.5 Heat Meter Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Heat Meter Industry

4.2 Key Market Trends in Heat Meter Industry

4.3 Potential Opportunities in Heat Meter Industry

4.4 Key Challenges in Heat Meter Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Heat Meter Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Heat Meter Market Outlook by Segments

7.1 Heat Meter Market Outlook by Segments, $ Million, 2021- 2030

By Type

Static

Mechanical

By Connectivity

Wired

Wireless

By End-User

Residential

Commercial

Industrial

8 North America Heat Meter Market Analysis and Outlook To 2030

8.1 Introduction to North America Heat Meter Markets in 2024

8.2 North America Heat Meter Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Heat Meter Market size Outlook by Segments, 2021-2030

By Type

Static

Mechanical

By Connectivity

Wired

Wireless

By End-User

Residential

Commercial

Industrial

9 Europe Heat Meter Market Analysis and Outlook To 2030

9.1 Introduction to Europe Heat Meter Markets in 2024

9.2 Europe Heat Meter Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Heat Meter Market Size Outlook by Segments, 2021-2030

By Type

Static

Mechanical

By Connectivity

Wired

Wireless

By End-User

Residential

Commercial

Industrial

10 Asia Pacific Heat Meter Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Heat Meter Markets in 2024

10.2 Asia Pacific Heat Meter Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Heat Meter Market size Outlook by Segments, 2021-2030

By Type

Static

Mechanical

By Connectivity

Wired

Wireless

By End-User

Residential

Commercial

Industrial

11 South America Heat Meter Market Analysis and Outlook To 2030

11.1 Introduction to South America Heat Meter Markets in 2024

11.2 South America Heat Meter Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Heat Meter Market size Outlook by Segments, 2021-2030

By Type

Static

Mechanical

By Connectivity

Wired

Wireless

By End-User

Residential

Commercial

Industrial

12 Middle East and Africa Heat Meter Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Heat Meter Markets in 2024

12.2 Middle East and Africa Heat Meter Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Heat Meter Market size Outlook by Segments, 2021-2030

By Type

Static

Mechanical

By Connectivity

Wired

Wireless

By End-User

Residential

Commercial

Industrial

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Apator S.A.

BMETERS Srl

Cosmic Technologies Pty Ltd

Danfoss A/S

Diehl Stiftung & Co. KG

Grundfos Holding A/S

Itron Inc

Kamstrup A/S

Omni Instruments Ltd

Premier Control Technologies Ltd

Siemens AG

Spire Metering Technology LLC

Sycous Ltd

Trend Control Systems Ltd

Zenner International GmbH & Co. KG

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

Static

Mechanical

By Connectivity

Wired

Wireless

By End-User

Residential

Commercial

Industrial

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Global Heat Meter is forecast to reach $2.2 Billion in 2030 from $1.46 Billion in 2024, registering a CAGR of 7.4% over the outlook period

Emerging Markets across Asia Pacific, Europe, and Americas present robust growth prospects.

Apator S.A., BMETERS Srl, Cosmic Technologies Pty Ltd, Danfoss A/S, Diehl Stiftung & Co. KG, Grundfos Holding A/S, Itron Inc, Kamstrup A/S, Omni Instruments Ltd, Premier Control Technologies Ltd, Siemens AG, Spire Metering Technology LLC, Sycous Ltd, Trend Control Systems Ltd, Zenner International GmbH & Co. KG

Base Year- 2023; Estimated Year- 2024; Historic Period- 2018-2023; Forecast period- 2024 to 2030; Currency: Revenue (USD); Volume