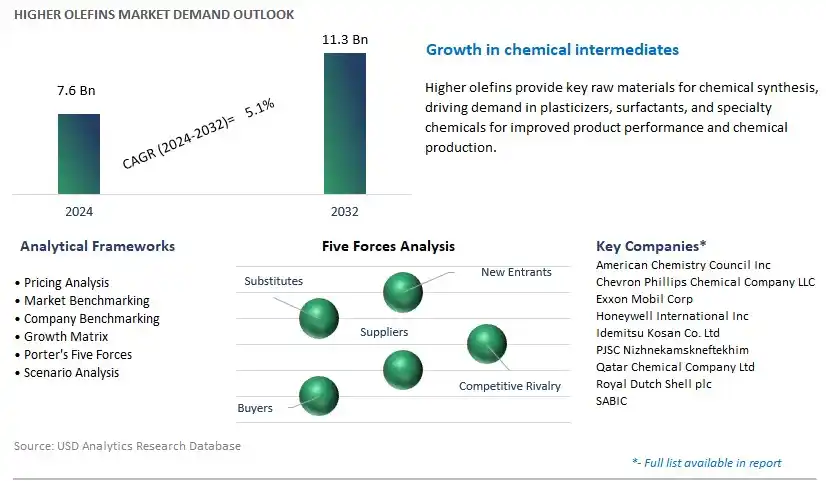

Global Higher Olefins Market Size is valued at $7.6 Billion in 2024 and is forecast to register a growth rate (CAGR) of 5.1% to reach $11.3 Billion by 2032.

The global Higher Olefins Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Application (Lubricant Additives, Surfactants, Agricultural Chemicals, Paints and Coatings, Corrosion Inhibitors, Others), By Grade (4N HPA, 5N HPA, 6N HPA), By Technology (Hydrolysis, Hydrochloric Acid Leaching (HCL)).

An Introduction to Higher Olefins Market in 2024

Higher olefins are a group of linear alpha olefins (LAOs) with carbon chain lengths ranging from C10 to C20 in 2024. These versatile chemicals are primarily derived from the oligomerization or polymerization of ethylene or propylene and are used as intermediate feedstocks in the production of various specialty chemicals, polymers, lubricants, and surfactants. Higher olefins find applications in diverse industries, including plastics, detergents, lubricants, adhesives, coatings, and personal care products. In the plastics industry, higher olefins are used as comonomers in the production of high-density polyethylene (HDPE), linear low-density polyethylene (LLDPE), and specialty polymers with tailored properties such as flexibility, toughness, and chemical resistance. In the detergent industry, higher olefins serve as key raw materials for the synthesis of alcohol ethoxylates and alkylbenzene sulfonates (ABS), which are widely used as surfactants and cleaning agents in household and industrial cleaning products. In the lubricants industry, higher olefins are utilized as base oils or viscosity modifiers to improve the lubricity, stability, and performance of engine oils, industrial lubricants, and metalworking fluids. With their unique chemical properties and versatile applications, higher olefins play a vital role in driving innovation and value creation across multiple sectors of the chemical industry.

Higher Olefins Market Competitive Landscape

The market report analyses the leading companies in the industry including American Chemistry Council Inc, Chevron Phillips Chemical Company LLC, Exxon Mobil Corp, Honeywell International Inc, Idemitsu Kosan Co. Ltd, PJSC Nizhnekamskneftekhim, Qatar Chemical Company Ltd, Royal Dutch Shell plc, SABIC, and others.

Higher Olefins Market Dynamics

Market Trend: Shift Towards Sustainable Feedstocks and Processes

A significant trend in the higher olefins market is the shift towards sustainable feedstocks and processes. With increasing environmental concerns and the push for sustainability, there is a growing preference for olefin production methods that utilize renewable resources and minimize carbon footprint. Higher olefins, which are key building blocks for various chemical products including detergents, plastics, and lubricants, are being produced from renewable feedstocks such as bio-based oils and fats, as well as through innovative catalytic processes that reduce energy consumption and greenhouse gas emissions. This trend towards sustainability in olefin production is driving market growth and shaping industry dynamics.

Market Driver: Growing Demand for Polyethylene and Polypropylene

A key driver fueling the higher olefins market is the growing demand for polyethylene and polypropylene. Higher olefins serve as essential intermediates in the production of polyethylene and polypropylene, two of the most widely used plastics in various industries including packaging, automotive, construction, and consumer goods. With increasing population, urbanization, and disposable income levels worldwide, the demand for polyethylene and polypropylene continues to rise, driving the need for higher olefins as raw materials. The versatility and functionality of these plastics in applications such as packaging films, pipes, automotive components, and household products create a steady demand for higher olefins, supporting market growth.

Market Opportunity: Expansion into Specialty Chemicals and Lubricants

A promising opportunity for the higher olefins market lies in expansion into specialty chemicals and lubricants. Higher olefins, with their unique chemical properties and versatility, can be used as precursors for manufacturing a wide range of specialty chemicals and lubricants. Specialty chemicals derived from higher olefins find applications in industries such as personal care, pharmaceuticals, agrochemicals, and textiles. Additionally, higher olefin-based lubricants offer superior performance in automotive, industrial, and marine applications due to their high viscosity index, thermal stability, and anti-wear properties. By diversifying into specialty chemicals and lubricants markets and developing innovative formulations, olefin producers can capitalize on new opportunities, expand their product portfolios, and drive growth in the higher olefins market.

Higher Olefins Market Share Analysis: Lubricant Additives segment generated the highest revenue in 2024

Lubricant additives emerge as the largest segment in the higher olefins market. Higher olefins are extensively utilized as key ingredients in lubricant additives, enhancing the performance and longevity of lubricants across diverse applications. Lubricant additives formulated with higher olefins offer improved lubricity, thermal stability, and wear resistance, enabling machinery and automotive components to operate efficiently and prolonging their service life. Moreover, the growing demand for high-performance lubricants in industries such as automotive, manufacturing, and aerospace, driven by increasing machinery complexity and the need for enhanced efficiency, propels the demand for higher olefins in lubricant additives. Additionally, stringent environmental regulations promoting the use of eco-friendly lubricants further bolster the demand for higher olefins as sustainable alternatives to traditional additives. As industries continue to prioritize equipment reliability and sustainability, the demand for lubricant additives formulated with higher olefins is expected to remain robust, solidifying their leadership position in the market.

Higher Olefins Market Share Analysis: 6N HPA is poised to register the fastest CAGR over the forecast period

The "6N HPA" grade is the fastest-growing segment in the higher olefins market, propelled by its widespread adoption. 6N HPA, or 99.9999% pure alumina, offers superior purity levels compared to lower grades, making it highly desirable for a wide range of advanced applications. In industries such as electronics, semiconductor manufacturing, and optics, 6N HPA serves as a critical material for producing high-performance components and devices. Its exceptional purity and chemical properties make it ideal for use in the production of LEDs, semiconductors, and sapphire substrates, where even trace impurities can adversely affect performance and yield. Additionally, the rapid growth of emerging technologies such as electric vehicles, renewable energy systems, and advanced lighting solutions further drives the demand for 6N HPA, as it plays a vital role in enabling technological advancements and innovation in these sectors. As industries continue to evolve and demand higher levels of purity and performance, the growth trajectory of the 6N HPA segment in the higher olefins market is expected to remain strong, solidifying its position as the fastest-growing grade.

Higher Olefins Market Share Analysis: Hydrolysis segment generated the highest revenue in 2024

The "Hydrolysis" technology is the largest segment in the higher olefins market, commanding a significant share due to its widespread adoption and advantages. Hydrolysis involves the chemical reaction of higher olefins with water to produce valuable products such as alcohols, esters, and acids. This technology offers potential advantages, including versatility in product output and the ability to utilize various feedstocks. Hydrolysis processes can be tailored to produce a wide range of chemical intermediates and end products, catering to diverse industrial applications such as pharmaceuticals, cosmetics, and detergents. Moreover, hydrolysis is considered a more environmentally friendly process compared to hydrochloric acid leaching, as it does not involve the use of hazardous chemicals. Additionally, advancements in hydrolysis technology, such as the development of novel catalysts and process optimization techniques, further contribute to its dominance in the higher olefins market. As industries continue to prioritize sustainability and flexibility in manufacturing processes, the demand for hydrolysis technology in producing higher olefins is expected to remain robust, solidifying its leadership position in the market.

Higher Olefins Market

By Application

Lubricant Additives

Surfactants

Agricultural Chemicals

Paints and Coatings

Corrosion Inhibitors

Others

By Grade

4N HPA

5N HPA

6N HPA

By Technology

Hydrolysis

Hydrochloric Acid Leaching (HCL)Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Higher Olefins Companies Profiled in the Study

American Chemistry Council Inc

Chevron Phillips Chemical Company LLC

Exxon Mobil Corp

Honeywell International Inc

Idemitsu Kosan Co. Ltd

PJSC Nizhnekamskneftekhim

Qatar Chemical Company Ltd

Royal Dutch Shell plc

SABIC

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Higher Olefins Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Higher Olefins Market Size Outlook, $ Million, 2021 to 2032

3.2 Higher Olefins Market Outlook by Type, $ Million, 2021 to 2032

3.3 Higher Olefins Market Outlook by Product, $ Million, 2021 to 2032

3.4 Higher Olefins Market Outlook by Application, $ Million, 2021 to 2032

3.5 Higher Olefins Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Higher Olefins Industry

4.2 Key Market Trends in Higher Olefins Industry

4.3 Potential Opportunities in Higher Olefins Industry

4.4 Key Challenges in Higher Olefins Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Higher Olefins Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Higher Olefins Market Outlook by Segments

7.1 Higher Olefins Market Outlook by Segments, $ Million, 2021- 2032

By Application

Lubricant Additives

Surfactants

Agricultural Chemicals

Paints and Coatings

Corrosion Inhibitors

Others

By Grade

4N HPA

5N HPA

6N HPA

By Technology

Hydrolysis

Hydrochloric Acid Leaching (HCL)

8 North America Higher Olefins Market Analysis and Outlook To 2032

8.1 Introduction to North America Higher Olefins Markets in 2024

8.2 North America Higher Olefins Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Higher Olefins Market size Outlook by Segments, 2021-2032

By Application

Lubricant Additives

Surfactants

Agricultural Chemicals

Paints and Coatings

Corrosion Inhibitors

Others

By Grade

4N HPA

5N HPA

6N HPA

By Technology

Hydrolysis

Hydrochloric Acid Leaching (HCL)

9 Europe Higher Olefins Market Analysis and Outlook To 2032

9.1 Introduction to Europe Higher Olefins Markets in 2024

9.2 Europe Higher Olefins Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Higher Olefins Market Size Outlook by Segments, 2021-2032

By Application

Lubricant Additives

Surfactants

Agricultural Chemicals

Paints and Coatings

Corrosion Inhibitors

Others

By Grade

4N HPA

5N HPA

6N HPA

By Technology

Hydrolysis

Hydrochloric Acid Leaching (HCL)

10 Asia Pacific Higher Olefins Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Higher Olefins Markets in 2024

10.2 Asia Pacific Higher Olefins Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Higher Olefins Market size Outlook by Segments, 2021-2032

By Application

Lubricant Additives

Surfactants

Agricultural Chemicals

Paints and Coatings

Corrosion Inhibitors

Others

By Grade

4N HPA

5N HPA

6N HPA

By Technology

Hydrolysis

Hydrochloric Acid Leaching (HCL)

11 South America Higher Olefins Market Analysis and Outlook To 2032

11.1 Introduction to South America Higher Olefins Markets in 2024

11.2 South America Higher Olefins Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Higher Olefins Market size Outlook by Segments, 2021-2032

By Application

Lubricant Additives

Surfactants

Agricultural Chemicals

Paints and Coatings

Corrosion Inhibitors

Others

By Grade

4N HPA

5N HPA

6N HPA

By Technology

Hydrolysis

Hydrochloric Acid Leaching (HCL)

12 Middle East and Africa Higher Olefins Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Higher Olefins Markets in 2024

12.2 Middle East and Africa Higher Olefins Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Higher Olefins Market size Outlook by Segments, 2021-2032

By Application

Lubricant Additives

Surfactants

Agricultural Chemicals

Paints and Coatings

Corrosion Inhibitors

Others

By Grade

4N HPA

5N HPA

6N HPA

By Technology

Hydrolysis

Hydrochloric Acid Leaching (HCL)

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

American Chemistry Council Inc

Chevron Phillips Chemical Company LLC

Exxon Mobil Corp

Honeywell International Inc

Idemitsu Kosan Co. Ltd

PJSC Nizhnekamskneftekhim

Qatar Chemical Company Ltd

Royal Dutch Shell plc

SABIC

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Application

Lubricant Additives

Surfactants

Agricultural Chemicals

Paints and Coatings

Corrosion Inhibitors

Others

By Grade

4N HPA

5N HPA

6N HPA

By Technology

Hydrolysis

Hydrochloric Acid Leaching (HCL)

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)