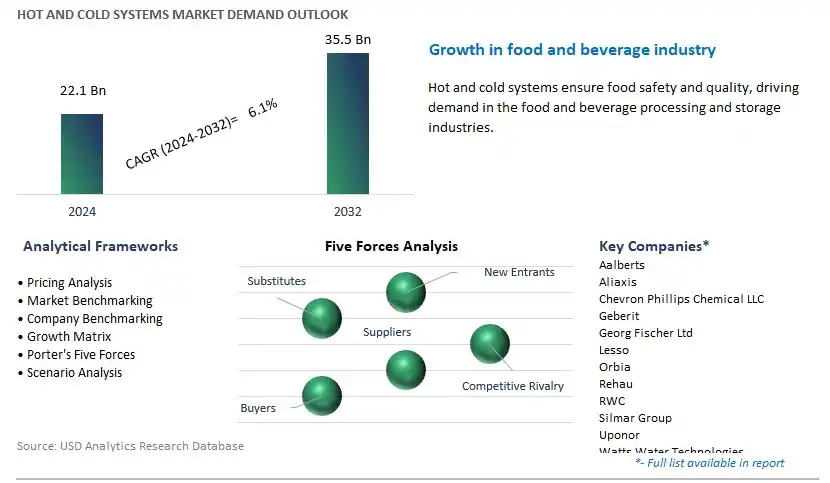

Global Hot and Cold Systems Market Size is valued at $22.1 Billion in 2024 and is forecast to register a growth rate (CAGR) of 6.1% to reach $35.5 Billion by 2032.

The global Hot and Cold Systems Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Raw Material (Plastic, Metallic, Metalized Plastic), By Component (Pipe, Fixtures & connectors, Multifold, Temperature Control, Local distribution, Solvent Cement, Others), By Application (Water plumbing pipes, Radiator connection pipes, Underfloor surface heating & cooling, Others), By End-User (Residential, Commercial, Industrial).

An Introduction to Hot and Cold Systems Market in 2024

In 2024, the market for hot and cold systems experiences steady growth driven by increasing demand from industries such as HVAC, refrigeration, food and beverage, and pharmaceuticals. Hot and cold systems encompass a wide range of equipment and solutions designed for heating, cooling, and temperature control applications in various industrial processes and commercial environments. These systems include boilers, chillers, heat exchangers, refrigeration units, and HVAC systems, among others, which play a crucial role in maintaining optimal temperature conditions for production processes, storage facilities, and comfort control in buildings. In the HVAC sector, hot and cold systems are utilized for heating, ventilation, and air conditioning applications in residential, commercial, and industrial buildings, providing occupants with comfortable indoor environments while optimizing energy efficiency and operational performance. Similarly, in the refrigeration industry, these systems are employed for cooling and preservation of perishable goods, pharmaceuticals, and temperature-sensitive products during storage, transportation, and distribution. Further, in the food and beverage sector, hot and cold systems are essential for food processing, packaging, and storage, ensuring product quality, safety, and compliance with regulatory standards. With ongoing advancements in system design, energy efficiency, and digitalization, the market is witnessing the development of integrated solutions that offer enhanced performance, reliability, and sustainability. As industries to prioritize energy conservation, environmental sustainability, and operational efficiency, the demand for hot and cold systems is expected to drive further innovation and market expansion, addressing the evolving needs of diverse sectors for temperature control solutions.

Hot and Cold Systems Market Competitive Landscape

The market report analyses the leading companies in the industry including Aalberts, Aliaxis, Chevron Phillips Chemical LLC, Geberit, Georg Fischer Ltd, Lesso, Orbia, Rehau, RWC, Silmar Group, Uponor, Watts Water Technologies, Wienerberger, Zurn, and others.

Hot and Cold Systems Market Dynamics

Market Trend: Integration of Smart Technology for Energy Efficiency

The market for Hot and Cold Systems is experiencing a prominent trend towards the integration of smart technology for improved energy efficiency and control. With increasing concerns about energy consumption and environmental sustainability, there's a growing demand for heating and cooling systems that can adapt to varying conditions and optimize energy usage. Smart thermostats, IoT-enabled sensors, and energy management systems are being integrated into hot and cold systems to monitor, analyze, and adjust temperature settings in real-time, resulting in reduced energy costs and enhanced comfort for users. This trend towards smart, energy-efficient solutions is reshaping the market dynamics for hot and cold systems across residential, commercial, and industrial sectors.

Market Driver: Regulatory Compliance and Energy Efficiency Standards

A key driver fueling the growth of the Hot and Cold Systems market is the increasing emphasis on regulatory compliance and energy efficiency standards. Governments and regulatory bodies worldwide are implementing stringent regulations and mandates to curb greenhouse gas emissions, promote energy conservation, and improve indoor air quality. As a result, there's a heightened demand for heating, ventilation, air conditioning (HVAC), and refrigeration systems that meet or exceed energy efficiency requirements and environmental standards. Manufacturers are compelled to develop innovative hot and cold systems with advanced technologies such as variable-speed compressors, heat recovery, and eco-friendly refrigerants to comply with regulations and meet the evolving needs of customers.

Market Opportunity: Expansion in Renewable Energy Integration and Green Buildings

An emerging opportunity in the Hot and Cold Systems market lies in the expansion of renewable energy integration and green building initiatives. With the increasing focus on sustainable development and carbon footprint reduction, there's a significant demand for hot and cold systems that leverage renewable energy sources such as solar, geothermal, and biomass for heating and cooling applications. Additionally, the growing adoption of green building practices, certifications, and standards such as LEED (Leadership in Energy and Environmental Design) presents opportunities for the integration of energy-efficient HVAC and refrigeration systems in eco-friendly buildings. By offering innovative solutions that align with renewable energy integration and green building requirements, manufacturers can capitalize on this market opportunity and drive further growth and differentiation. Expanding into emerging markets with favorable regulatory frameworks and investing in research and development for sustainable hot and cold system solutions can unlock new avenues for business expansion and market leadership.

Hot & Cold Systems Market Share Analysis: Metallic segment generated the highest revenue in 2024

The largest segment in the Hot & Cold Systems Market is the Metallic segment. metallic materials, such as stainless steel and aluminum, offer superior thermal conductivity, durability, and corrosion resistance compared to plastic and metalized plastic materials. These properties make metallic materials well-suited for applications in hot and cold systems, where efficient heat transfer, mechanical strength, and long-term reliability are critical. Additionally, metallic components provide excellent resistance to high temperatures, pressures, and environmental factors, making them suitable for use in demanding environments such as industrial processes, HVAC systems, automotive cooling systems, and refrigeration units. In addition, metallic materials offer versatility in design and fabrication, allowing for the production of complex shapes, sizes, and configurations to meet specific application requirements. Manufacturers can customize metallic hot and cold systems components through processes such as stamping, machining, welding, and brazing, enabling precise control over thermal performance, dimensional accuracy, and mechanical properties. Furthermore, advancements in metallurgy, surface treatment, and joining technologies have enhanced the performance and functionality of metallic hot and cold systems, driving their widespread adoption in various industries. As industries continue to prioritize energy efficiency, product reliability, and sustainability, the Metallic segment in the Hot & Cold Systems Market is expected to maintain its dominance.

Hot & Cold Systems Market Share Analysis: Temperature Control is poised to register the fastest CAGR over the forecast period

Among the segments within the Hot & Cold Systems Market categorized by component, the fastest-growing segment is the Temperature Control segment. In particular, temperature control components, such as thermostatic valves, thermostats, and temperature sensors, play a crucial role in regulating the flow and temperature of hot and cold fluids within heating, ventilation, air conditioning (HVAC), and plumbing systems. These components ensure optimal comfort, efficiency, and safety by maintaining desired temperature levels and preventing overheating or freezing of fluids in piping networks, equipment, and appliances. Additionally, temperature control components enable energy-saving strategies such as setback and modulating control, which help reduce energy consumption, operating costs, and environmental impact. In addition, advancements in temperature control technology, such as digitalization, wireless connectivity, and smart automation, have led to the development of intelligent and integrated temperature control systems that offer enhanced functionality, performance, and user experience. Smart temperature control systems allow users to remotely monitor and adjust temperature settings, schedule operations, and receive alerts or notifications for potential issues, improving convenience, comfort, and peace of mind. Furthermore, the increasing adoption of renewable energy sources such as solar thermal, geothermal, and heat pump systems further drives the demand for temperature control components to optimize energy harvesting, storage, and distribution. As building owners, operators, and occupants seek more efficient and sustainable solutions for heating and cooling, the Temperature Control segment in the Hot & Cold Systems Market is expected to experience rapid growth.

Hot & Cold Systems Market Share Analysis: Water plumbing pipes segment generated the highest revenue in 2024

The largest segment in the Hot & Cold Systems Market is the Water plumbing pipes segment. water plumbing pipes are essential components of residential, commercial, and industrial plumbing systems, responsible for conveying hot and cold water to various fixtures, appliances, and equipment for drinking, sanitation, heating, and cooling purposes. Water plumbing pipes are widely used in buildings, infrastructure, and utilities to ensure reliable and efficient water distribution, circulation, and drainage, meeting basic human needs and building code requirements. Additionally, water plumbing pipes are available in a variety of materials, including copper, PVC (polyvinyl chloride), CPVC (chlorinated polyvinyl chloride), PEX (cross-linked polyethylene), and stainless steel, offering options for different application requirements, budget considerations, and environmental conditions. In addition, water plumbing pipes are subjected to high-pressure, high-temperature, and corrosive environments, requiring durable, leak-proof, and corrosion-resistant materials to ensure long-term performance and safety. Metallic pipes such as copper and stainless steel are preferred for hot water distribution due to their excellent thermal conductivity, resistance to scaling, and ability to withstand high temperatures without degradation. Furthermore, advancements in pipe manufacturing technologies, such as extrusion, injection molding, and compression molding, have improved the efficiency, quality, and reliability of water plumbing pipes, driving their widespread adoption in construction, renovation, and infrastructure projects. As the global population grows, urbanization expands, and infrastructure investment increases, the demand for water plumbing pipes in residential, commercial, and municipal applications is expected to remain robust, sustaining the dominance of the Water plumbing pipes segment in the Hot & Cold Systems Market.

Hot & Cold Systems Market Share Analysis: Residential is poised to register the fastest CAGR over the forecast period

Among the segments within the Hot & Cold Systems Market categorized by end-user, the fastest-growing segment is the Residential segment. In particular, the residential sector is experiencing rapid urbanization, population growth, and housing demand, particularly in emerging economies and urban areas, driving the construction of new residential buildings and the renovation of existing ones. As a result, there is a significant increase in the installation of hot and cold systems in residential properties, including single-family homes, apartments, condominiums, and townhouses, to provide essential services such as water heating, space heating, and air conditioning for occupants' comfort and well-being. Additionally, rising standards of living, disposable incomes, and awareness of energy efficiency and environmental sustainability contribute to the adoption of advanced hot and cold systems with higher efficiency ratings, smart controls, and eco-friendly features in residential buildings. In addition, government initiatives, building codes, and regulations aimed at promoting energy conservation, green building practices, and climate resilience drive the implementation of energy-efficient heating, cooling, and plumbing solutions in residential construction projects. Incentives such as tax credits, subsidies, and rebates encourage homeowners and developers to invest in energy-saving technologies and renewable energy systems, including solar thermal, geothermal, and heat pump systems, for hot and cold applications. Furthermore, advancements in building materials, construction methods, and smart home technologies enable the integration of hot and cold systems into intelligent and connected residential environments, enhancing comfort, convenience, and sustainability for residents. As homeowners and builders prioritize energy-efficient, comfortable, and environmentally responsible living spaces, the Residential segment in the Hot & Cold Systems Market is expected to experience robust growth.

Hot and Cold Systems Market

By Raw Material

Plastic

Metallic

Metalized Plastic

By Component

Pipe

Fixtures & connectors

Multifold

Temperature Control

Local distribution

Solvent Cement

Others

By Application

Water plumbing pipes

Radiator connection pipes

Underfloor surface heating & cooling

Others

By End-User

Residential

Commercial

IndustrialCountries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Hot and Cold Systems Companies Profiled in the Study

Aalberts

Aliaxis

Chevron Phillips Chemical LLC

Geberit

Georg Fischer Ltd

Lesso

Orbia

Rehau

RWC

Silmar Group

Uponor

Watts Water Technologies

Wienerberger

Zurn

*- List Not Exhaustive