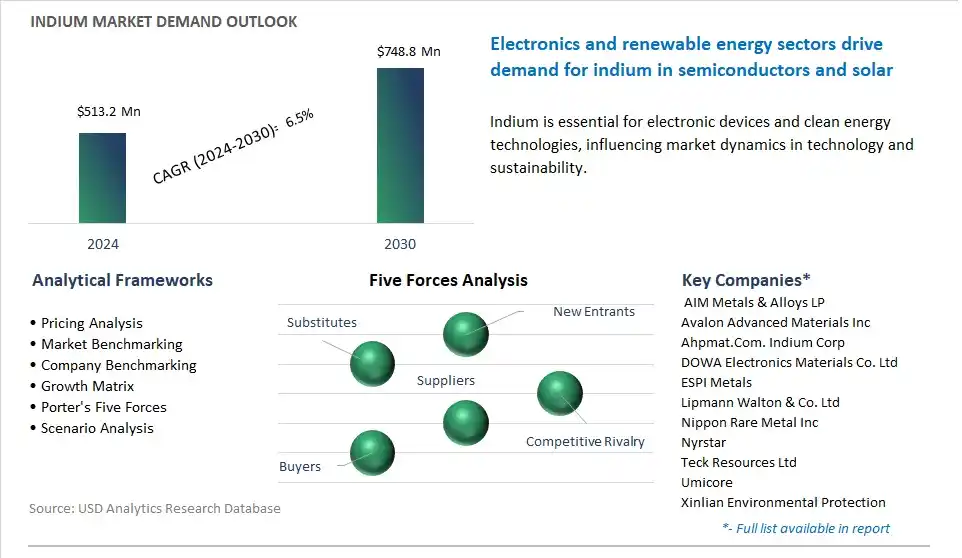

The global Indium Market is poised to register a 6.5% CAGR from $513.2 Million in 2024 to $748.8 Million in 2030.

The global Indium Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Product (Primary, Secondary, Type III), By Application (Flat Panel Displays, Semiconductor Materials, Photovoltaics, Solders, Alloys, Thermal Interface Materials, Batteries).

An Introduction to Global Indium Market in 2024

Indium, a critical material in the electronics industry, is experiencing significant shifts in demand dynamics and supply chain resilience. With the proliferation of electronic devices and the rapid expansion of technologies such as 5G and Internet of Things (IoT), the demand for indium in the production of touchscreens, thin-film solar cells, and semiconductors is escalating. This surge in demand is driving efforts to explore alternative indium sources and enhance recycling technologies to ensure a sustainable supply chain. Moreover, emerging applications in areas such as flexible electronics and organic light-emitting diodes (OLEDs) are opening up new avenues for indium consumption. However, geopolitical tensions and trade policies affecting indium-rich regions could pose challenges to the industry's growth, necessitating strategic diversification of supply sources and investments in research and development to optimize indium usage and mitigate supply risks.

Indium Market Competitive Landscape

The market report analyses the leading companies in the industry including AIM Metals & Alloys LP, Avalon Advanced Materials Inc Ahpmat.Com. Indium Corp, DOWA Electronics Materials Co. Ltd, ESPI Metals, Lipmann Walton & Co. Ltd, Nippon Rare Metal Inc, Nyrstar, Teck Resources Ltd, Umicore, Xinlian Environmental Protection Technology Co. Ltd, Zhuzhou Keneng New Material Co. Ltd Inc.

Indium Market Dynamics

Indium Market Trend: Increasing Demand for Indium in Electronics Manufacturing

A significant trend in the indium market is the increasing demand for indium in electronics manufacturing driven by the proliferation of electronic devices, advancements in display technologies, and the rise of emerging applications such as flexible electronics and optoelectronic devices. Indium, a rare and valuable metal known for its unique properties such as high electrical conductivity, low melting point, and optical transparency, is a critical component in the production of flat panel displays, touchscreens, solar cells, and semiconductors. With the growing consumer demand for smartphones, tablets, laptops, and smart TVs, there is a corresponding increase in the consumption of indium for manufacturing indium tin oxide (ITO) coatings used in transparent conductive films for electronic displays and touchscreens. Additionally, the development of new display technologies such as OLED (organic light-emitting diode) and flexible displays further drives market demand for indium as a key material for producing high-performance electronic components. This trend is reshaping the indium market towards increased utilization in electronics manufacturing and emerging applications, positioning indium as a vital resource for the digital age.

Indium Market Driver: Growth in Renewable Energy Technologies and Green Technologies

A key driver propelling the indium market is the growth in renewable energy technologies and green technologies that rely on indium-based materials for their performance and efficiency advantages. Indium is an essential component in the production of thin-film solar cells, where it is used as a transparent conductive layer to enhance sunlight absorption and electricity generation efficiency. Additionally, indium gallium nitride (InGaN) alloys are utilized in light-emitting diodes (LEDs) for energy-efficient lighting applications, contributing to energy savings and environmental sustainability. With increasing global efforts to mitigate climate change and transition towards renewable energy sources, there is a growing demand for indium in solar photovoltaics and LED lighting systems as key enablers of clean energy technologies. Furthermore, indium's properties make it suitable for various green technologies such as thermoelectric devices, smart windows, and transparent heating elements, driving market demand for indium as a critical material in the transition to a low-carbon economy.

Indium Market Opportunity: Exploration of New Applications and Recycling Technologies

An opportunity for market expansion lies in the exploration of new applications and recycling technologies that expand the use of indium and enhance its sustainability across various industries. With advancements in materials science and engineering, there is potential to develop novel indium-based materials and applications in areas such as flexible electronics, wearable devices, medical imaging, and aerospace technologies. By investing in research and development, indium manufacturers can innovate and create value-added products that address emerging market needs and unlock new revenue streams. Additionally, the development of indium recycling technologies presents opportunities to recover indium from end-of-life electronic devices, manufacturing waste streams, and scrap materials, reducing reliance on primary indium production and mitigating supply chain risks. By investing in recycling infrastructure and collaborating with electronics manufacturers and recycling companies, the indium industry can promote circular economy principles, reduce environmental impact, and secure a sustainable supply of indium resources for future generations, driving growth and resilience in the indium market.

Indium Market Share Analysis: Primary segment generated the highest revenue in the industry

The primary segment is the largest segment in the indium market, primarily due to diverse factors. The primary indium refers to indium sourced directly from ore deposits through mining and extraction processes. This primary indium is of higher purity and quality compared to secondary indium, which is recovered from recycled sources such as electronic waste or scrap materials. The demand for primary indium is driven by its essential role in various high-technology applications, including electronics, semiconductors, and photovoltaics. Indium is a critical component in the production of indium tin oxide (ITO), a transparent conductive material used in flat-panel displays, touch screens, and solar panels. As the electronics and renewable energy sectors continue to grow, so does the demand for primary indium as a key raw material for these applications. Additionally, primary indium is used in other advanced technologies such as thin-film coatings, solders, and alloys, where its unique properties, including high electrical conductivity, low melting point, and excellent thermal stability, are highly valued. In addition, primary indium production is primarily concentrated in a few key mining regions globally, which contributes to its dominance in the market. These factors combined make the primary segment the largest segment in the indium market.

Indium Market Report Segmentation

By Product

Primary

Secondary

Type III

By Application

Flat Panel Displays

Semiconductor Materials

Photovoltaics

Solders

Alloys

Thermal Interface Materials

Batteries

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Indium Companies Profiled in the Market Study

AIM Metals & Alloys LP

Avalon Advanced Materials Inc Ahpmat.Com. Indium Corp

DOWA Electronics Materials Co. Ltd

ESPI Metals

Lipmann Walton & Co. Ltd

Nippon Rare Metal Inc

Nyrstar

Teck Resources Ltd

Umicore

Xinlian Environmental Protection Technology Co. Ltd

Zhuzhou Keneng New Material Co. Ltd Inc

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Indium Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Indium Market Size Outlook, $ Million, 2021 to 2030

3.2 Indium Market Outlook by Type, $ Million, 2021 to 2030

3.3 Indium Market Outlook by Product, $ Million, 2021 to 2030

3.4 Indium Market Outlook by Application, $ Million, 2021 to 2030

3.5 Indium Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Indium Industry

4.2 Key Market Trends in Indium Industry

4.3 Potential Opportunities in Indium Industry

4.4 Key Challenges in Indium Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Indium Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Indium Market Outlook by Segments

7.1 Indium Market Outlook by Segments, $ Million, 2021- 2030

By Product

Primary

Secondary

Type III

By Application

Flat Panel Displays

Semiconductor Materials

Photovoltaics

Solders

Alloys

Thermal Interface Materials

Batteries

8 North America Indium Market Analysis and Outlook To 2030

8.1 Introduction to North America Indium Markets in 2024

8.2 North America Indium Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Indium Market size Outlook by Segments, 2021-2030

By Product

Primary

Secondary

Type III

By Application

Flat Panel Displays

Semiconductor Materials

Photovoltaics

Solders

Alloys

Thermal Interface Materials

Batteries

9 Europe Indium Market Analysis and Outlook To 2030

9.1 Introduction to Europe Indium Markets in 2024

9.2 Europe Indium Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Indium Market Size Outlook by Segments, 2021-2030

By Product

Primary

Secondary

Type III

By Application

Flat Panel Displays

Semiconductor Materials

Photovoltaics

Solders

Alloys

Thermal Interface Materials

Batteries

10 Asia Pacific Indium Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Indium Markets in 2024

10.2 Asia Pacific Indium Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Indium Market size Outlook by Segments, 2021-2030

By Product

Primary

Secondary

Type III

By Application

Flat Panel Displays

Semiconductor Materials

Photovoltaics

Solders

Alloys

Thermal Interface Materials

Batteries

11 South America Indium Market Analysis and Outlook To 2030

11.1 Introduction to South America Indium Markets in 2024

11.2 South America Indium Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Indium Market size Outlook by Segments, 2021-2030

By Product

Primary

Secondary

Type III

By Application

Flat Panel Displays

Semiconductor Materials

Photovoltaics

Solders

Alloys

Thermal Interface Materials

Batteries

12 Middle East and Africa Indium Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Indium Markets in 2024

12.2 Middle East and Africa Indium Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Indium Market size Outlook by Segments, 2021-2030

By Product

Primary

Secondary

Type III

By Application

Flat Panel Displays

Semiconductor Materials

Photovoltaics

Solders

Alloys

Thermal Interface Materials

Batteries

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

AIM Metals & Alloys LP

Avalon Advanced Materials Inc Ahpmat.Com. Indium Corp

DOWA Electronics Materials Co. Ltd

ESPI Metals

Lipmann Walton & Co. Ltd

Nippon Rare Metal Inc

Nyrstar

Teck Resources Ltd

Umicore

Xinlian Environmental Protection Technology Co. Ltd

Zhuzhou Keneng New Material Co. Ltd Inc

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Product

Primary

Secondary

Type III

By Application

Flat Panel Displays

Semiconductor Materials

Photovoltaics

Solders

Alloys

Thermal Interface Materials

Batteries

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)