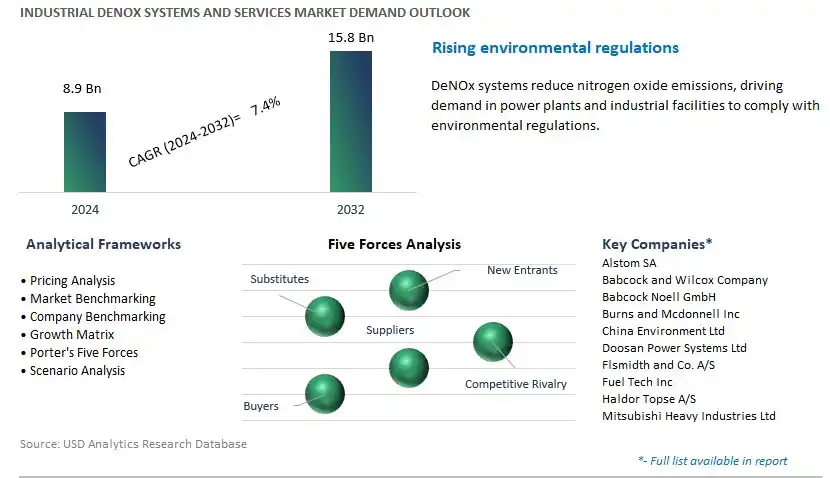

Global Industrial DeNOx Systems and Services Market Size is valued at $8.9 Billion in 2024 and is forecast to register a growth rate (CAGR) of 7.4% to reach $15.8 Billion by 2032.

The global Industrial DeNOx Systems and Services Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (Selective Catalytic Reduction (SCR), Selective Non-Catalytic Reduction (SNCR)), By Application (Utilities, Industries).

An Introduction to Industrial DeNOx Systems and Services Market in 2024

In 2024, the market for industrial DeNOx systems and services s to grow, driven by stringent environmental regulations aimed at reducing nitrogen oxide (NOx) emissions from industrial sources such as power plants, refineries, chemical plants, and manufacturing facilities. DeNOx systems are designed to remove NOx pollutants from flue gases through selective catalytic reduction (SCR), non-selective catalytic reduction (NSCR), or other advanced technologies. With increasing concerns about air quality and the impact of NOx emissions on human health and the environment, there is a heightened demand for effective DeNOx solutions. Manufacturers and service providers are offering a range of turnkey solutions, including catalysts, reactors, monitoring systems, and maintenance services, to help industries comply with regulatory requirements and achieve emission reduction targets. Further, advancements in catalyst technology, process optimization, and digitalization are driving innovation and efficiency in DeNOx systems, enabling cost-effective NOx abatement while minimizing operational impacts and downtime.

Industrial DeNOx Systems and Services Market Competitive Landscape

The market report analyses the leading companies in the industry including Alstom SA, Babcock and Wilcox Company, Babcock Noell GmbH, Burns and Mcdonnell Inc, China Environment Ltd, Doosan Power Systems Ltd, Flsmidth and Co. A/S, Fuel Tech Inc, Haldor Topse A/S, Mitsubishi Heavy Industries Ltd, and others.

Industrial DeNOx Systems and Services Market Dynamics

Market Trend: Increased Focus on Air Quality Regulations and Emission Reduction

The market for Industrial DeNOx Systems and Services is witnessing a prominent trend towards an increased focus on air quality regulations and emission reduction. Governments and regulatory bodies worldwide are implementing stricter emissions standards to address air pollution and mitigate the environmental impact of industrial activities. Industrial DeNOx systems, which utilize selective catalytic reduction (SCR) or selective non-catalytic reduction (SNCR) technologies, play a crucial role in reducing nitrogen oxide (NOx) emissions from industrial sources such as power plants, refineries, and manufacturing facilities. As regulations become more stringent, industries are investing in DeNOx systems and services to ensure compliance, minimize environmental impact, and improve public health.

Market Driver: Growing Awareness of Environmental Sustainability and Corporate Responsibility

A key driver fueling the growth of the Industrial DeNOx Systems and Services market is the growing awareness of environmental sustainability and corporate responsibility. Stakeholders, including governments, communities, investors, and consumers, are increasingly concerned about the environmental footprint of industrial operations and demand action to reduce emissions and protect air quality. As a result, industries are proactively investing in DeNOx systems and services to demonstrate their commitment to environmental stewardship, comply with regulations, and enhance their corporate image. The drive towards sustainability and social responsibility is a significant driver of market demand for DeNOx solutions, stimulating innovation, and investment in the industry.

Market Opportunity: Expansion into Emerging Markets and Technology Integration

An emerging opportunity in the Industrial DeNOx Systems and Services market lies in the expansion into emerging markets and technology integration. Emerging economies experiencing rapid industrialization and urbanization are facing increasing challenges related to air pollution and NOx emissions. These markets present significant opportunities for the adoption of DeNOx technologies and services to address environmental concerns and meet regulatory requirements. Additionally, there's a growing demand for integrated DeNOx solutions that combine SCR or SNCR systems with other air pollution control technologies such as particulate matter (PM) removal, mercury control, and volatile organic compound (VOC) abatement. By offering comprehensive emission control solutions tailored to the specific needs of different industries and regions, manufacturers and service providers can capitalize on this market opportunity and drive further growth and market penetration. Expanding market presence in emerging economies, investing in technology development and innovation, and providing customized solutions and services are key strategies for success in this evolving market segment.

Industrial DeNOx Systems & Services Market Share Analysis: Selective Catalytic Reduction (SCR) segment generated the highest revenue in 2024

Among the segments delineated in the Industrial DeNOx Systems & Services Market by type, the largest segment is the Selective Catalytic Reduction (SCR) category. SCR systems are widely used in industrial applications for the reduction of nitrogen oxides (NOx) emissions from flue gases generated by combustion processes, such as those in power plants, industrial boilers, and cement kilns. SCR systems utilize catalysts, typically based on vanadium or titanium oxides, to facilitate the chemical reaction between NOx and ammonia or urea reductants at elevated temperatures, converting NOx into nitrogen (N2) and water vapor (H2O). These systems offer high efficiency and NOx removal rates, typically exceeding 90%, and can achieve compliance with stringent emission regulations and standards. Moreover, SCR systems are well-established technologies with proven performance and reliability in various industrial sectors. Additionally, SCR systems can be tailored to specific emission control requirements and operating conditions, offering flexibility and versatility in application. Furthermore, the increasing stringency of environmental regulations and the growing emphasis on air quality improvement drive the demand for SCR systems as preferred solutions for NOx abatement in industrial processes. As industries prioritize emissions reduction, regulatory compliance, and environmental sustainability, the SCR segment maintains its dominance within the industrial DeNOx systems market, positioning it as the largest and most significant market segment.

Industrial DeNOx Systems & Services Market Share Analysis: Utilities is poised to register the fastest CAGR over the forecast period

Among the segments delineated in the Industrial DeNOx Systems & Services Market by application, the Utilities category is the fastest-growing segment. Utilities, including power plants and energy generation facilities, are significant sources of nitrogen oxides (NOx) emissions due to the combustion of fossil fuels such as coal, natural gas, and oil. As governments worldwide implement stringent regulations and emission standards to combat air pollution and mitigate environmental impact, utilities face increasing pressure to reduce NOx emissions from their operations. Industrial DeNOx systems, such as Selective Catalytic Reduction (SCR) and Selective Non-Catalytic Reduction (SNCR), offer effective solutions for NOx abatement in utility applications. SCR systems, in particular, are favored for their high efficiency and NOx removal rates, making them ideal for utilities seeking to achieve compliance with emission limits. Additionally, the shift towards cleaner energy sources and the integration of renewable energy technologies in utility operations further drive the demand for DeNOx systems to ensure environmental sustainability and regulatory compliance. Moreover, advancements in DeNOx system technology, including catalyst formulations, process optimization, and integration with existing infrastructure, enhance performance and reliability, driving adoption in utility applications. Furthermore, utilities prioritize investments in emissions control technologies to safeguard public health, mitigate environmental impact, and maintain operational efficiency. As utilities strive to meet regulatory requirements and reduce their environmental footprint, the Utilities segment experiences rapid growth, positioning it as the fastest-growing segment in the industrial DeNOx systems market.

Industrial DeNOx Systems and Services Market

By Type

Selective Catalytic Reduction (SCR)

Selective Non-Catalytic Reduction (SNCR)

By Application

Utilities

IndustriesCountries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Industrial DeNOx Systems and Services Companies Profiled in the Study

Alstom SA

Babcock and Wilcox Company

Babcock Noell GmbH

Burns and Mcdonnell Inc

China Environment Ltd

Doosan Power Systems Ltd

Flsmidth and Co. A/S

Fuel Tech Inc

Haldor Topse A/S

Mitsubishi Heavy Industries Ltd

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Industrial DeNOx Systems and Services Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Industrial DeNOx Systems and Services Market Size Outlook, $ Million, 2021 to 2032

3.2 Industrial DeNOx Systems and Services Market Outlook by Type, $ Million, 2021 to 2032

3.3 Industrial DeNOx Systems and Services Market Outlook by Product, $ Million, 2021 to 2032

3.4 Industrial DeNOx Systems and Services Market Outlook by Application, $ Million, 2021 to 2032

3.5 Industrial DeNOx Systems and Services Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Industrial DeNOx Systems and Services Industry

4.2 Key Market Trends in Industrial DeNOx Systems and Services Industry

4.3 Potential Opportunities in Industrial DeNOx Systems and Services Industry

4.4 Key Challenges in Industrial DeNOx Systems and Services Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Industrial DeNOx Systems and Services Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Industrial DeNOx Systems and Services Market Outlook by Segments

7.1 Industrial DeNOx Systems and Services Market Outlook by Segments, $ Million, 2021- 2032

By Type

Selective Catalytic Reduction (SCR)

Selective Non-Catalytic Reduction (SNCR)

By Application

Utilities

Industries

8 North America Industrial DeNOx Systems and Services Market Analysis and Outlook To 2032

8.1 Introduction to North America Industrial DeNOx Systems and Services Markets in 2024

8.2 North America Industrial DeNOx Systems and Services Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Industrial DeNOx Systems and Services Market size Outlook by Segments, 2021-2032

By Type

Selective Catalytic Reduction (SCR)

Selective Non-Catalytic Reduction (SNCR)

By Application

Utilities

Industries

9 Europe Industrial DeNOx Systems and Services Market Analysis and Outlook To 2032

9.1 Introduction to Europe Industrial DeNOx Systems and Services Markets in 2024

9.2 Europe Industrial DeNOx Systems and Services Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Industrial DeNOx Systems and Services Market Size Outlook by Segments, 2021-2032

By Type

Selective Catalytic Reduction (SCR)

Selective Non-Catalytic Reduction (SNCR)

By Application

Utilities

Industries

10 Asia Pacific Industrial DeNOx Systems and Services Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Industrial DeNOx Systems and Services Markets in 2024

10.2 Asia Pacific Industrial DeNOx Systems and Services Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Industrial DeNOx Systems and Services Market size Outlook by Segments, 2021-2032

By Type

Selective Catalytic Reduction (SCR)

Selective Non-Catalytic Reduction (SNCR)

By Application

Utilities

Industries

11 South America Industrial DeNOx Systems and Services Market Analysis and Outlook To 2032

11.1 Introduction to South America Industrial DeNOx Systems and Services Markets in 2024

11.2 South America Industrial DeNOx Systems and Services Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Industrial DeNOx Systems and Services Market size Outlook by Segments, 2021-2032

By Type

Selective Catalytic Reduction (SCR)

Selective Non-Catalytic Reduction (SNCR)

By Application

Utilities

Industries

12 Middle East and Africa Industrial DeNOx Systems and Services Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Industrial DeNOx Systems and Services Markets in 2024

12.2 Middle East and Africa Industrial DeNOx Systems and Services Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Industrial DeNOx Systems and Services Market size Outlook by Segments, 2021-2032

By Type

Selective Catalytic Reduction (SCR)

Selective Non-Catalytic Reduction (SNCR)

By Application

Utilities

Industries

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Alstom SA

Babcock and Wilcox Company

Babcock Noell GmbH

Burns and Mcdonnell Inc

China Environment Ltd

Doosan Power Systems Ltd

Flsmidth and Co. A/S

Fuel Tech Inc

Haldor Topse A/S

Mitsubishi Heavy Industries Ltd

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

Selective Catalytic Reduction (SCR)

Selective Non-Catalytic Reduction (SNCR)

By Application

Utilities

Industries

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)