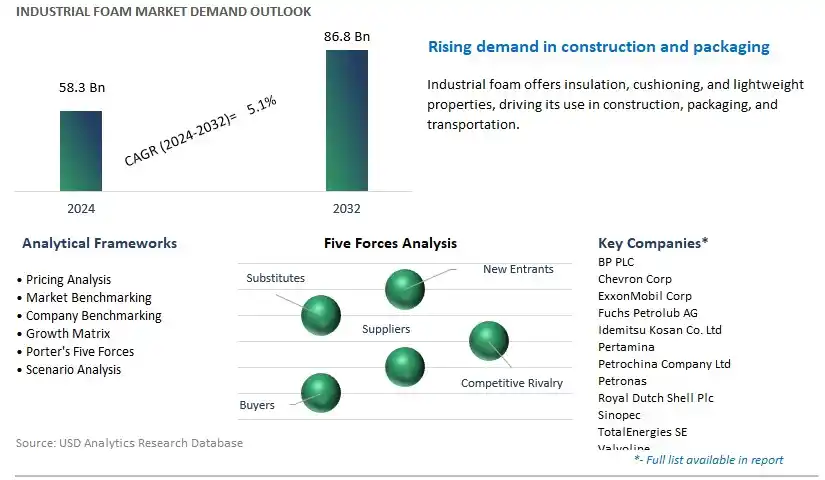

Global Industrial Foam Market Size is valued at $58.3 Billion in 2024 and is forecast to register a growth rate (CAGR) of 5.1% to reach $86.8 Billion by 2032.

The global Industrial Foam Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Base Oil (Mineral Oil, Synthetic Oil, Bio-based Oil), By Point of Sale (OEM, AfterMarket), By End-User (Construction, Metal & Mining, Agriculture, Oil & Gas, Transportation, Cement Production, Others).

An Introduction to Industrial Foam Market in 2024

In 2024, the industrial foam market demonstrates robust growth propelled by increasing demand from industries such as construction, packaging, automotive, and furniture. Industrial foam refers to a wide range of polymeric materials with cellular structures, including polyurethane (PU), polystyrene (PS), polyethylene (PE), and polypropylene (PP) foams, among others. These foams are used for insulation, cushioning, sound absorption, and flotation applications in various industrial sectors. In the construction industry, industrial foams are utilized for thermal insulation, roofing, and sealing applications, offering energy efficiency and moisture resistance. Similarly, in the packaging sector, foams are used for protective packaging, cushioning fragile goods during shipping and handling. Additionally, in the automotive industry, foams are employed for manufacturing vehicle interiors, seating, and acoustic insulation, providing comfort and noise reduction. Further, in the furniture sector, foams are utilized for upholstery, padding, and mattresses, offering comfort and support. With increasing emphasis on energy efficiency, lightweighting, and sustainability, manufacturers are developing innovative foam materials with improved performance, recyclability, and environmental impact. As industries to adopt advanced materials and technologies for their products, the demand for industrial foam is expected to drive further innovation and market expansion, catering to the evolving needs of diverse industries for versatile and sustainable foam solutions.

Industrial Foam Market Competitive Landscape

The market report analyses the leading companies in the industry including BP PLC, Chevron Corp, ExxonMobil Corp, Fuchs Petrolub AG, Idemitsu Kosan Co. Ltd, Pertamina, Petrochina Company Ltd, Petronas, Royal Dutch Shell Plc, Sinopec, TotalEnergies SE, Valvoline, and others.

Industrial Foam Market Dynamics

Market Trend: Increasing Demand for Lightweight and Versatile Materials

The market for Industrial Foam is witnessing a prominent trend towards the increasing demand for lightweight and versatile materials across various industries such as automotive, construction, and packaging. With a focus on enhancing efficiency, performance, and sustainability, there's a growing adoption of industrial foam products that offer high strength-to-weight ratios, excellent thermal and acoustic insulation properties, and versatility in application. Industrial foams, including polyurethane, polystyrene, and polyethylene foams, are being utilized in diverse applications such as insulation, cushioning, sealing, and packaging to address the evolving needs of manufacturers seeking lightweight solutions without compromising on quality or performance. This trend is driven by the need for innovative materials that enable product differentiation, cost savings, and environmental sustainability, reshaping the market landscape for industrial foam products.

Market Driver: Advancements in Manufacturing Technologies and Material Science

A key driver fueling the growth of the Industrial Foam market is the continuous advancements in manufacturing technologies and material science. Innovations such as foam extrusion, injection molding, and chemical formulations have revolutionized the production process, enabling the development of customized foam products with tailored properties to meet specific application requirements. Manufacturers are investing in research and development to innovate new foam formulations, additives, and production techniques that offer enhanced performance characteristics such as improved fire resistance, thermal stability, and eco-friendliness. The drive towards automation, digitization, and sustainability in manufacturing processes is accelerating the adoption of industrial foam products across various industries, driving market growth and differentiation.

Market Opportunity: Expansion in E-commerce Packaging and Insulation Solutions

An emerging opportunity in the Industrial Foam market lies in the expansion into e-commerce packaging and insulation solutions. With the rapid growth of online shopping and the need for efficient and sustainable packaging materials, there's a significant demand for foam-based packaging solutions that offer protection, cushioning, and branding opportunities. Industrial foam products such as foam sheets, inserts, and molded packaging provide excellent shock absorption, vibration dampening, and customization options for e-commerce companies looking to enhance product presentation and ensure safe delivery to customers. Additionally, in the construction sector, there's a growing demand for foam insulation materials to improve energy efficiency, thermal comfort, and building performance. By targeting the e-commerce packaging and insulation segments with innovative foam solutions tailored for specific applications, manufacturers can capitalize on this market opportunity and drive further growth and innovation. Expanding product portfolios to include foam packaging and insulation solutions, investing in e-commerce logistics and distribution channels, and providing value-added services such as design consultation and customization are key strategies for success in these burgeoning market segments.

Industrial Foam Market Share Analysis: Synthetic Oil segment generated the highest revenue in 2024

The Industrial Foam Market's largest segment is the Synthetic Oil category. Synthetic oils have gained prominence due to potential advantages over other base oils. In particular, synthetic oils offer enhanced thermal stability and oxidation resistance compared to mineral oils, making them suitable for a wide range of industrial applications where high temperatures and harsh operating conditions are prevalent. Additionally, synthetic oils exhibit superior lubricating properties and viscosity stability, resulting in improved performance and longer service life for industrial foam products. Furthermore, synthetic oils can be formulated to meet specific application requirements, offering flexibility and versatility to manufacturers. As industries prioritize efficiency, sustainability, and performance, synthetic oil-based industrial foams are increasingly favored, driving their dominance in the market.

Industrial Foam Market Share Analysis: AfterMarket is poised to register the fastest CAGR over the forecast period

Among the segments delineated in the Industrial Foam Market by Point of Sale, the AfterMarket category is the fastest-growing segment. The aftermarket segment refers to the sale of industrial foam products after the initial sale of the equipment or machinery they are used in, as replacements or upgrades. This segment experiences rapid growth due to various reasons. In particular, industrial equipment and machinery often require periodic maintenance and replacement of foam components due to wear and tear, damage, or deterioration over time. As machinery ages or undergoes heavy use, the need for replacement foam parts increases, leading to a higher demand for aftermarket foam products. Additionally, technological advancements and innovations in foam materials and manufacturing processes result in improved foam products with enhanced performance characteristics. Consequently, industrial users opt to upgrade to newer, more advanced foam components, further driving aftermarket sales. Moreover, aftermarket foam suppliers often offer customized solutions and quick turnaround times to meet specific customer requirements, catering to the diverse needs of industrial end-users. As industries strive to maintain operational efficiency, productivity, and safety, the aftermarket segment of the industrial foam market experiences significant growth, positioning it as the fastest-growing segment.

Industrial Foam Market Share Analysis: Construction segment generated the highest revenue in 2024

Among the segments delineated in the Industrial Foam Market by end-user, the Construction category is the largest segment. The construction industry is a significant consumer of industrial foam products due to their diverse applications in various construction activities. Foam materials are commonly used in construction for insulation, sealing, cushioning, and soundproofing purposes. For example, foam insulation boards are utilized to improve energy efficiency and thermal performance in residential, commercial, and industrial buildings. Additionally, foam sealants and adhesives are employed for sealing gaps and joints in construction assemblies, preventing air and moisture infiltration. Moreover, foam materials find applications in concrete production and construction foam products such as expansion joint fillers and void fillers. As urbanization and infrastructure development continue to drive construction activities globally, the demand for industrial foam products in the construction sector remains robust, positioning it as the largest and most significant market segment.

Industrial Foam Market

By Base Oil

Mineral Oil

Synthetic Oil

Bio-based Oil

By Point of Sale

OEM

AfterMarket

By End-User

Construction

Metal & Mining

Agriculture

Oil & Gas

Transportation

Cement Production

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Industrial Foam Companies Profiled in the Study

BP PLC

Chevron Corp

ExxonMobil Corp

Fuchs Petrolub AG

Idemitsu Kosan Co. Ltd

Pertamina

Petrochina Company Ltd

Petronas

Royal Dutch Shell Plc

Sinopec

TotalEnergies SE

Valvoline

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Industrial Foam Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Industrial Foam Market Size Outlook, $ Million, 2021 to 2032

3.2 Industrial Foam Market Outlook by Type, $ Million, 2021 to 2032

3.3 Industrial Foam Market Outlook by Product, $ Million, 2021 to 2032

3.4 Industrial Foam Market Outlook by Application, $ Million, 2021 to 2032

3.5 Industrial Foam Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Industrial Foam Industry

4.2 Key Market Trends in Industrial Foam Industry

4.3 Potential Opportunities in Industrial Foam Industry

4.4 Key Challenges in Industrial Foam Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Industrial Foam Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Industrial Foam Market Outlook by Segments

7.1 Industrial Foam Market Outlook by Segments, $ Million, 2021- 2032

By Base Oil

Mineral Oil

Synthetic Oil

Bio-based Oil

By Point of Sale

OEM

AfterMarket

By End-User

Construction

Metal & Mining

Agriculture

Oil & Gas

Transportation

Cement Production

Others

8 North America Industrial Foam Market Analysis and Outlook To 2032

8.1 Introduction to North America Industrial Foam Markets in 2024

8.2 North America Industrial Foam Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Industrial Foam Market size Outlook by Segments, 2021-2032

By Base Oil

Mineral Oil

Synthetic Oil

Bio-based Oil

By Point of Sale

OEM

AfterMarket

By End-User

Construction

Metal & Mining

Agriculture

Oil & Gas

Transportation

Cement Production

Others

9 Europe Industrial Foam Market Analysis and Outlook To 2032

9.1 Introduction to Europe Industrial Foam Markets in 2024

9.2 Europe Industrial Foam Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Industrial Foam Market Size Outlook by Segments, 2021-2032

By Base Oil

Mineral Oil

Synthetic Oil

Bio-based Oil

By Point of Sale

OEM

AfterMarket

By End-User

Construction

Metal & Mining

Agriculture

Oil & Gas

Transportation

Cement Production

Others

10 Asia Pacific Industrial Foam Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Industrial Foam Markets in 2024

10.2 Asia Pacific Industrial Foam Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Industrial Foam Market size Outlook by Segments, 2021-2032

By Base Oil

Mineral Oil

Synthetic Oil

Bio-based Oil

By Point of Sale

OEM

AfterMarket

By End-User

Construction

Metal & Mining

Agriculture

Oil & Gas

Transportation

Cement Production

Others

11 South America Industrial Foam Market Analysis and Outlook To 2032

11.1 Introduction to South America Industrial Foam Markets in 2024

11.2 South America Industrial Foam Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Industrial Foam Market size Outlook by Segments, 2021-2032

By Base Oil

Mineral Oil

Synthetic Oil

Bio-based Oil

By Point of Sale

OEM

AfterMarket

By End-User

Construction

Metal & Mining

Agriculture

Oil & Gas

Transportation

Cement Production

Others

12 Middle East and Africa Industrial Foam Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Industrial Foam Markets in 2024

12.2 Middle East and Africa Industrial Foam Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Industrial Foam Market size Outlook by Segments, 2021-2032

By Base Oil

Mineral Oil

Synthetic Oil

Bio-based Oil

By Point of Sale

OEM

AfterMarket

By End-User

Construction

Metal & Mining

Agriculture

Oil & Gas

Transportation

Cement Production

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

BP PLC

Chevron Corp

ExxonMobil Corp

Fuchs Petrolub AG

Idemitsu Kosan Co. Ltd

Pertamina

Petrochina Company Ltd

Petronas

Royal Dutch Shell Plc

Sinopec

TotalEnergies SE

Valvoline

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Base Oil

Mineral Oil

Synthetic Oil

Bio-based Oil

By Point of Sale

OEM

AfterMarket

By End-User

Construction

Metal & Mining

Agriculture

Oil & Gas

Transportation

Cement Production

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)