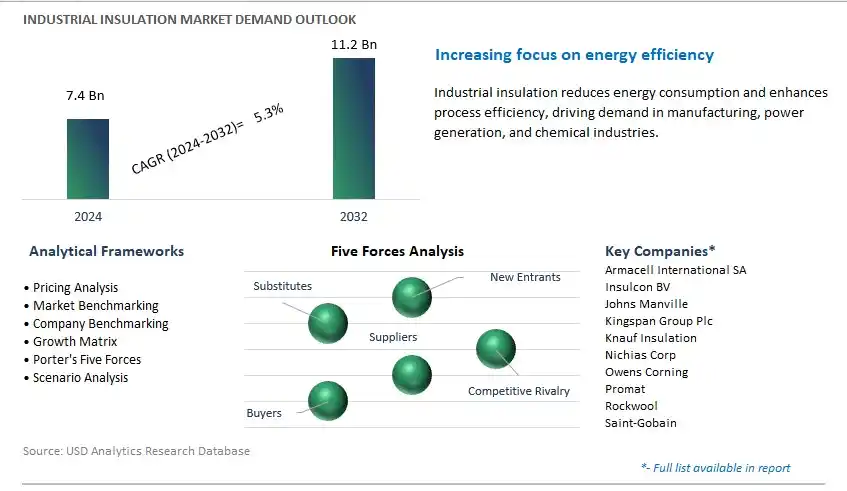

Global Industrial Insulation Market Size is valued at $7.4 Billion in 2024 and is forecast to register a growth rate (CAGR) of 5.3% to reach $11.2 Billion by 2032.

The global Industrial Insulation Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Form (Pipe, Blanket, Board, Others), By Material (Mineral wool, Calcium silicate, Plastic foams, Others), By End-User (Power, Oil & petrochemical, Gas, Chemical, Cement, Food & beverage, Others).

An Introduction to Industrial Insulation Market in 2024

In 2024, the industrial insulation market s to expand, driven by the increasing need for energy efficiency, thermal management, and process optimization in industries such as petrochemicals, manufacturing, power generation, and construction. Industrial insulation materials play a crucial role in reducing heat transfer, preventing energy loss, and maintaining temperature stability in equipment, pipelines, ducts, and buildings. With a focus on sustainability and cost-effectiveness, there is a growing adoption of advanced insulation materials such as mineral wool, foam plastics, aerogels, and reflective coatings, offering superior thermal performance, fire resistance, and durability. Manufacturers are investing in research and development to develop innovative insulation solutions that address specific application requirements, comply with regulatory standards, and minimize environmental impact. Additionally, the market is driven by factors such as infrastructure development projects, retrofitting activities, and increasing awareness of the benefits of energy-efficient insulation systems, driving demand across various industrial sectors.

Industrial Insulation Market Competitive Landscape

The market report analyses the leading companies in the industry including Armacell International SA, Insulcon BV, Johns Manville, Kingspan Group Plc, Knauf Insulation, Nichias Corp, Owens Corning, Promat, Rockwool, Saint-Gobain, and others.

Industrial Insulation Market Dynamics

Market Trend: Growing Emphasis on Energy Efficiency and Sustainability

The market for Industrial Insulation is experiencing a prominent trend towards a growing emphasis on energy efficiency and sustainability across various industries. Industrial insulation plays a crucial role in reducing heat transfer, preventing energy loss, and maintaining process temperatures in industrial facilities such as power plants, refineries, chemical plants, and manufacturing facilities. With increasing energy costs, environmental regulations, and corporate sustainability initiatives, there's a rising demand for insulation materials that offer superior thermal performance, durability, and environmental compatibility. Industries are investing in insulation solutions that help minimize heat loss, reduce greenhouse gas emissions, and improve overall energy efficiency, reflecting the industry's commitment to sustainability and resource conservation.

Market Driver: Regulatory Compliance and Energy Conservation Initiatives

A key driver fueling the growth of the Industrial Insulation market is regulatory compliance and energy conservation initiatives. Governments, regulatory agencies, and industry organizations worldwide are implementing stricter regulations and standards to promote energy efficiency, reduce carbon emissions, and mitigate climate change. Industries are required to comply with building codes, environmental regulations, and energy efficiency mandates that mandate the use of insulation to minimize heat loss and improve thermal performance in industrial processes and facilities. Additionally, energy conservation initiatives and incentive programs encourage industries to invest in insulation upgrades and retrofits to reduce energy consumption, lower operating costs, and enhance competitiveness. The need for regulatory compliance and energy conservation drives the demand for industrial insulation solutions, providing opportunities for insulation manufacturers, contractors, and service providers.

Market Opportunity: Adoption of Advanced Insulation Materials and Technologies

An emerging opportunity in the Industrial Insulation market lies in the adoption of advanced insulation materials and technologies. With advancements in materials science, manufacturing processes, and insulation technologies, there's a growing market for innovative insulation solutions that offer superior performance, durability, and ease of installation. Manufacturers are developing advanced insulation materials such as aerogels, vacuum insulated panels (VIPs), and phase change materials (PCMs) that provide higher thermal resistance, thinner profiles, and improved fire resistance compared to traditional insulation materials. Additionally, there's a rising demand for insulation systems that offer enhanced acoustic insulation, moisture resistance, and corrosion protection in harsh industrial environments. By leveraging advanced insulation materials and technologies, manufacturers can address evolving customer needs, differentiate their products, and capture new market opportunities in the industrial insulation sector. Investing in research and development, product innovation, and market education are key strategies for success in this evolving market segment.

Industrial Insulation Market Share Analysis: Pipe Insulation segment generated the highest revenue in 2024

The Pipe Insulation segment is the largest segment in the Industrial Insulation Market. Pipe insulation is essential for maintaining the temperature of fluid-carrying pipelines in industrial settings, preventing heat loss or gain and minimizing energy consumption. Industries such as oil and gas, chemical processing, and power generation rely heavily on pipe insulation to ensure the efficient operation of their pipelines and equipment. Additionally, stringent regulations regarding energy efficiency and environmental sustainability have heightened the demand for pipe insulation solutions, as they help industries reduce greenhouse gas emissions and comply with regulatory requirements. Moreover, the growing emphasis on safety and asset protection in industrial facilities further drives the adoption of pipe insulation to prevent accidents and prolong the lifespan of equipment. Furthermore, advancements in insulation materials and installation techniques have enhanced the performance and durability of pipe insulation, further solidifying its position as the largest segment in the industrial insulation market. Over the forecast period, the Pipe Insulation segment's critical role in maintaining operational efficiency, safety, and regulatory compliance positions it as the dominant segment in the industrial insulation market.

Industrial Insulation Market Share Analysis: Plastic Foams is poised to register the fastest CAGR over the forecast period

The Plastic Foams segment is experiencing the fastest growth within the Industrial Insulation Market. Plastic foams, such as expanded polystyrene (EPS) and extruded polystyrene (XPS), offer a combination of excellent insulation properties, lightweight construction, and ease of installation, making them increasingly popular choices for industrial insulation applications. These materials provide superior thermal resistance, moisture resistance, and durability, making them suitable for a wide range of industrial environments, including commercial buildings, warehouses, and manufacturing facilities. Moreover, plastic foams are highly versatile and can be molded or shaped to fit various insulation requirements, allowing for greater flexibility in design and installation. Additionally, the growing emphasis on energy efficiency and sustainability in industrial operations has driven the demand for plastic foam insulation solutions, as they help reduce energy consumption and greenhouse gas emissions. Furthermore, advancements in plastic foam manufacturing technologies have led to the development of innovative products with enhanced performance characteristics, further fuelling the growth of this segment in the industrial insulation market. Over the forecast period, the Plastic Foams segment's rapid growth is driven by its superior insulation properties, versatility, and alignment with evolving industry trends towards energy efficiency and sustainability.

Industrial Insulation Market Share Analysis: Oil & Petrochemical generated the highest revenue in 2024

The largest segment in the Industrial Insulation Market is the Oil & Petrochemical sector, and Oil and petrochemical facilities encompass a wide range of equipment and processes that require insulation to maintain optimal operating conditions and ensure safety. In these industries, insulation plays a critical role in preventing heat loss or gain, minimizing energy consumption, and protecting personnel and equipment from extreme temperatures. Additionally, the oil and petrochemical sectors operate in harsh environments with high temperatures, corrosive chemicals, and flammable materials, making effective insulation crucial for mitigating risks and ensuring regulatory compliance. Moreover, the global demand for oil and petrochemical products remains consistently high, driving investments in new facilities, expansions, and maintenance activities, which sustain the demand for industrial insulation solutions in this sector. Furthermore, advancements in insulation materials and technologies tailored to meet the specific challenges of oil and petrochemical applications further reinforce the dominance of this segment in the industrial insulation market. Over the forecast period, the Oil & Petrochemical sector's extensive use of industrial insulation and its critical role in maintaining operational efficiency and safety solidify its position as the largest segment in the market.

Industrial Insulation Market

By Form

Pipe

Blanket

Board

Others

By Material

Mineral wool

Calcium silicate

Plastic foams

Others

By End-User

Power

Oil & petrochemical

Gas

Chemical

Cement

Food & beverage

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Industrial Insulation Companies Profiled in the Study

Armacell International SA

Insulcon BV

Johns Manville

Kingspan Group Plc

Knauf Insulation

Nichias Corp

Owens Corning

Promat

Rockwool

Saint-Gobain

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Industrial Insulation Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Industrial Insulation Market Size Outlook, $ Million, 2021 to 2032

3.2 Industrial Insulation Market Outlook by Type, $ Million, 2021 to 2032

3.3 Industrial Insulation Market Outlook by Product, $ Million, 2021 to 2032

3.4 Industrial Insulation Market Outlook by Application, $ Million, 2021 to 2032

3.5 Industrial Insulation Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Industrial Insulation Industry

4.2 Key Market Trends in Industrial Insulation Industry

4.3 Potential Opportunities in Industrial Insulation Industry

4.4 Key Challenges in Industrial Insulation Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Industrial Insulation Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Industrial Insulation Market Outlook by Segments

7.1 Industrial Insulation Market Outlook by Segments, $ Million, 2021- 2032

By Form

Pipe

Blanket

Board

Others

By Material

Mineral wool

Calcium silicate

Plastic foams

Others

By End-User

Power

Oil & petrochemical

Gas

Chemical

Cement

Food & beverage

Others

8 North America Industrial Insulation Market Analysis and Outlook To 2032

8.1 Introduction to North America Industrial Insulation Markets in 2024

8.2 North America Industrial Insulation Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Industrial Insulation Market size Outlook by Segments, 2021-2032

By Form

Pipe

Blanket

Board

Others

By Material

Mineral wool

Calcium silicate

Plastic foams

Others

By End-User

Power

Oil & petrochemical

Gas

Chemical

Cement

Food & beverage

Others

9 Europe Industrial Insulation Market Analysis and Outlook To 2032

9.1 Introduction to Europe Industrial Insulation Markets in 2024

9.2 Europe Industrial Insulation Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Industrial Insulation Market Size Outlook by Segments, 2021-2032

By Form

Pipe

Blanket

Board

Others

By Material

Mineral wool

Calcium silicate

Plastic foams

Others

By End-User

Power

Oil & petrochemical

Gas

Chemical

Cement

Food & beverage

Others

10 Asia Pacific Industrial Insulation Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Industrial Insulation Markets in 2024

10.2 Asia Pacific Industrial Insulation Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Industrial Insulation Market size Outlook by Segments, 2021-2032

By Form

Pipe

Blanket

Board

Others

By Material

Mineral wool

Calcium silicate

Plastic foams

Others

By End-User

Power

Oil & petrochemical

Gas

Chemical

Cement

Food & beverage

Others

11 South America Industrial Insulation Market Analysis and Outlook To 2032

11.1 Introduction to South America Industrial Insulation Markets in 2024

11.2 South America Industrial Insulation Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Industrial Insulation Market size Outlook by Segments, 2021-2032

By Form

Pipe

Blanket

Board

Others

By Material

Mineral wool

Calcium silicate

Plastic foams

Others

By End-User

Power

Oil & petrochemical

Gas

Chemical

Cement

Food & beverage

Others

12 Middle East and Africa Industrial Insulation Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Industrial Insulation Markets in 2024

12.2 Middle East and Africa Industrial Insulation Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Industrial Insulation Market size Outlook by Segments, 2021-2032

By Form

Pipe

Blanket

Board

Others

By Material

Mineral wool

Calcium silicate

Plastic foams

Others

By End-User

Power

Oil & petrochemical

Gas

Chemical

Cement

Food & beverage

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Armacell International SA

Insulcon BV

Johns Manville

Kingspan Group Plc

Knauf Insulation

Nichias Corp

Owens Corning

Promat

Rockwool

Saint-Gobain

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Form

Pipe

Blanket

Board

Others

By Material

Mineral wool

Calcium silicate

Plastic foams

Others

By End-User

Power

Oil & petrochemical

Gas

Chemical

Cement

Food & beverage

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)