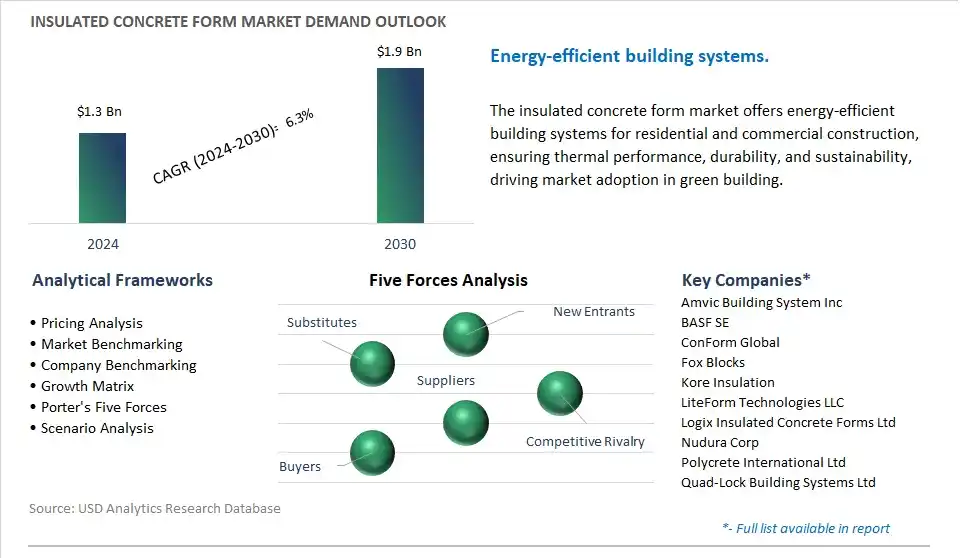

Global Insulated Concrete Form Market is expected to reach 1.9 Billion USD by 2034 from 1.3 Billion USD in 2025, at a CAGR of 6.3%.

The global Insulated Concrete Form Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Product (Polystyrene Foam, Polyurethane Foam, Cement-Bonded Wood Fiber, Others), By Application (Residential, Non-Residential).

An Introduction to Global Insulated Concrete Form Market in 2025

Insulated concrete forms (ICFs) are construction materials used in residential, commercial, and industrial building projects to create insulated walls, floors, and roofs, providing energy efficiency, structural stability, and thermal comfort. One key trend shaping the future of insulated concrete forms is the adoption of advanced materials and construction techniques to improve building performance, durability, and sustainability while reducing construction costs, energy consumption, and environmental impact. ICF manufacturers and builders are innovating new form designs, such as stay-in-place modular blocks, interlocking panels, and composite materials, with enhanced insulation properties, ease of installation, and compatibility with diverse architectural designs and building codes, ensuring superior thermal performance and air-tightness in constructed structures. Additionally, advancements in insulation materials, such as expanded polystyrene (EPS), extruded polystyrene (XPS), and polyurethane foam, are improving thermal resistance, moisture resistance, and fire resistance of ICF systems, enabling year-round energy savings, indoor comfort, and resilience to extreme weather conditions. Moreover, the integration of digital design tools, prefabrication technologies, and sustainable construction practices is optimizing ICF construction processes, reducing material waste, labor costs, and construction time, while enhancing building performance and occupant satisfaction. As the construction industry seeks to build more energy-efficient, resilient, and sustainable structures, the market for insulated concrete forms is poised for innovation and growth, with opportunities for collaboration, research, and market expansion to meet the evolving needs of architects, builders, and property developers.

Insulated Concrete Form Market Competitive Landscape

The market report analyses the leading companies in the industry including Amvic Building System Inc, BASF SE, ConForm Global, Fox Blocks, Kore Insulation, LiteForm Technologies LLC, Logix Insulated Concrete Forms Ltd, Nudura Corp, Polycrete International Ltd, Quad-Lock Building Systems Ltd.

Insulated Concrete Form Market Dynamics

Insulated Concrete Form Market Trend: Growing Demand for Energy-Efficient and Sustainable Construction Materials

A prominent trend in the market for insulated concrete forms (ICFs) is the growing demand for energy-efficient and sustainable construction materials. With increasing emphasis on green building practices, energy conservation, and environmental sustainability, there is a rising preference for building materials that offer superior insulation properties, thermal performance, and durability. Insulated concrete forms, which consist of rigid foam insulation sandwiched between concrete panels, provide excellent thermal resistance, air tightness, and structural strength, making them ideal for constructing energy-efficient and resilient buildings. The trend towards sustainable construction materials supports the drive to reducing carbon footprint, improving indoor comfort, and meeting energy efficiency standards, driving the adoption of ICFs in residential, commercial, and industrial construction projects worldwide.

Insulated Concrete Form Market Driver: Regulations and Incentives Promoting Energy-Efficient Construction

A key driver propelling the market for insulated concrete forms (ICFs) is the regulations and incentives promoting energy-efficient construction. Governments, building codes, and regulatory agencies worldwide are implementing stringent energy efficiency standards and green building codes to reduce greenhouse gas emissions, combat climate change, and promote sustainable development. Incentive programs such as tax credits, grants, and rebates are also offered to encourage the adoption of energy-efficient building materials and construction practices. Insulated concrete forms, which contribute to improved thermal performance, reduced energy consumption, and lower carbon emissions in buildings, are increasingly mandated or incentivized by regulations, driving the demand for ICFs in the construction industry. Additionally, growing consumer awareness of the benefits of energy-efficient buildings and the long-term cost savings associated with reduced energy bills further support the adoption of ICFs as a preferred construction solution.

Insulated Concrete Form Market Opportunity: Expansion into High-Rise and Commercial Construction Projects

An opportunity for growth in the market for insulated concrete forms (ICFs) lies in the expansion into high-rise and commercial construction projects. While ICFs have traditionally been used in residential construction for single-family homes, low-rise buildings, and multifamily dwellings, there is potential to penetrate the commercial construction sector for high-rise buildings, offices, hotels, schools, and institutional buildings. By offering enhanced structural performance, fire resistance, sound insulation, and energy efficiency, ICFs can address the stringent requirements of commercial buildings and meet the diverse needs of developers, architects, and building owners. Additionally, advancements in ICF technology, including larger panel sizes, improved interlocking systems, and integrated reinforcement options, are making ICFs more suitable for high-rise construction applications. By targeting the commercial construction market and positioning ICFs as a cost-effective, sustainable, and high-performance building solution, manufacturers can capitalize on the opportunity to expand their market presence and capture new revenue streams in the construction industry.

Insulated Concrete Form Market Ecosystem

The insulated concrete form (ICF) market encompasses various stages, with raw material acquisition from chemical manufacturers including BASF SE and Dow Chemical Company, which produce base chemicals for polystyrene and foam used in ICFs. Additionally, oil and gas companies including ExxonMobil and Shell plc contribute raw materials for specific types of plastic foams used in these forms. ICF manufacturing involves companies including Fox Blocks and NUDURA Corporation, which produce various types of ICF blocks from polystyrene or other insulating foam materials.

Building material distributors including Builders FirstSource and Ferguson plc play a crucial role in distributing ICFs and related accessories to builders and contractors. Structural engineers are involved in complex ICF projects to ensure structural integrity, while specialized construction crews or general contractors handle the construction of ICF walls. End-users of ICFs include residential, commercial, and public/institutional construction projects seeking energy-efficient and durable building solutions.

Insulated Concrete Form (ICF) Market Share Analysis: Polystyrene Foam held the dominant revenue share in 2024

The polystyrene foam segment stands as the largest sector in the Insulated Concrete Form (ICF) Market, driven by diverse pivotal factors contributing to its dominance. Polystyrene foam, particularly expanded polystyrene (EPS) and extruded polystyrene (XPS), is widely used in insulated concrete forms due to its excellent thermal insulation properties, ease of handling, versatility, and cost-effectiveness. Polystyrene foam ICFs consist of hollow foam blocks or panels that are interconnected and filled with concrete to create a structural wall system with integrated insulation. One of the primary advantages of polystyrene foam ICFs is their high thermal resistance (R-value), which helps improve energy efficiency and reduce heating and cooling costs in buildings. Additionally, polystyrene foam ICFs offer superior strength, durability, and impact resistance, making them suitable for various construction applications, including residential, commercial, and industrial buildings. In addition, polystyrene foam ICFs are lightweight and easy to install, reducing construction time and labor costs. Further, polystyrene foam ICFs provide excellent sound insulation properties, enhancing occupant comfort and reducing noise transmission between rooms and floors. Additionally, polystyrene foam ICFs are resistant to moisture, mold, and pests, contributing to the longevity and durability of the building envelope. In addition, polystyrene foam ICFs are compatible with a wide range of architectural styles and building designs, allowing for creative and customizable construction solutions. Further, the growing demand for energy-efficient and sustainable building materials, coupled with stringent building energy codes and regulations, drives the adoption of polystyrene foam ICFs in the construction industry. As builders, developers, and homeowners prioritize energy performance, comfort, and resilience in their buildings, the polystyrene foam segment of the insulated concrete form market is expected to maintain its leading position and witness sustained growth in the foreseeable future.

Insulated Concrete Form (ICF) Market Share Analysis: Non-Residential is the fastest growing market segment over the forecast period to 2030

The non-residential segment is the fastest-growing sector in the Insulated Concrete Form (ICF) Market, driven by diverse critical factors propelling its rapid expansion. Non-residential applications of insulated concrete forms include commercial buildings, institutional facilities, industrial structures, and infrastructure projects such as bridges and retaining walls. One of the primary reasons for the rapid growth of ICF usage in non-residential applications is the increasing recognition of the benefits of ICF construction in the commercial and institutional sectors. Insulated concrete forms offer numerous advantages for non-residential buildings, including enhanced energy efficiency, thermal comfort, durability, and resilience. These benefits are particularly attractive to building owners, developers, and occupants seeking sustainable and high-performance building solutions. Additionally, non-residential buildings often have higher energy demands and operational requirements compared to residential structures, making energy-efficient construction methods such as ICFs increasingly desirable. In addition, the design flexibility and versatility of ICF systems allow for the construction of a wide range of non-residential building types and architectural styles, accommodating diverse project requirements and design preferences. Further, the growing emphasis on green building practices, energy conservation, and environmental stewardship drives the adoption of ICF construction in non-residential projects seeking to achieve green building certifications such as LEED (Leadership in Energy and Environmental Design) and BREEAM (Building Research Establishment Environmental Assessment Method). Additionally, the construction industry's shift toward off-site manufacturing and prefabrication methods aligns well with the modular and panelized nature of ICF systems, facilitating faster construction timelines and cost savings for non-residential projects. Further, the increasing investment in infrastructure development and the renovation of existing non-residential buildings present significant opportunities for the adoption of ICF construction methods. As architects, engineers, contractors, and building owners recognize the economic, environmental, and performance benefits of ICFs in non-residential construction, the non-residential segment of the ICF market is expected to experience robust growth, presenting lucrative opportunities for manufacturers and suppliers of ICF systems tailored for commercial and institutional applications.

Insulated Concrete Form Market Report Scope-

By Product

Polystyrene Foam

Polyurethane Foam

Cement-Bonded Wood Fiber

Others

By Application

Residential

Non-Residential

Insulated Concrete Form Market Companies Profiled

Amvic Building System Inc

BASF SE

ConForm Global

Fox Blocks

Kore Insulation

LiteForm Technologies LLC

Logix Insulated Concrete Forms Ltd

Nudura Corp

Polycrete International Ltd

Quad-Lock Building Systems Ltd

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Insulated Concrete Form Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Insulated Concrete Form Market Size Outlook, $ Million, 2021 to 2030

3.2 Insulated Concrete Form Market Outlook by Type, $ Million, 2021 to 2030

3.3 Insulated Concrete Form Market Outlook by Product, $ Million, 2021 to 2030

3.4 Insulated Concrete Form Market Outlook by Application, $ Million, 2021 to 2030

3.5 Insulated Concrete Form Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Insulated Concrete Form Industry

4.2 Key Market Trends in Insulated Concrete Form Industry

4.3 Potential Opportunities in Insulated Concrete Form Industry

4.4 Key Challenges in Insulated Concrete Form Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Insulated Concrete Form Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Insulated Concrete Form Market Outlook by Segments

7.1 Insulated Concrete Form Market Outlook by Segments, $ Million, 2021- 2030

By Product

Polystyrene Foam

Polyurethane Foam

Cement-Bonded Wood Fiber

Others

By Application

Residential

Non-Residential

8 North America Insulated Concrete Form Market Analysis and Outlook To 2030

8.1 Introduction to North America Insulated Concrete Form Markets in 2024

8.2 North America Insulated Concrete Form Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Insulated Concrete Form Market size Outlook by Segments, 2021-2030

By Product

Polystyrene Foam

Polyurethane Foam

Cement-Bonded Wood Fiber

Others

By Application

Residential

Non-Residential

9 Europe Insulated Concrete Form Market Analysis and Outlook To 2030

9.1 Introduction to Europe Insulated Concrete Form Markets in 2024

9.2 Europe Insulated Concrete Form Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Insulated Concrete Form Market Size Outlook by Segments, 2021-2030

By Product

Polystyrene Foam

Polyurethane Foam

Cement-Bonded Wood Fiber

Others

By Application

Residential

Non-Residential

10 Asia Pacific Insulated Concrete Form Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Insulated Concrete Form Markets in 2024

10.2 Asia Pacific Insulated Concrete Form Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Insulated Concrete Form Market size Outlook by Segments, 2021-2030

By Product

Polystyrene Foam

Polyurethane Foam

Cement-Bonded Wood Fiber

Others

By Application

Residential

Non-Residential

11 South America Insulated Concrete Form Market Analysis and Outlook To 2030

11.1 Introduction to South America Insulated Concrete Form Markets in 2024

11.2 South America Insulated Concrete Form Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Insulated Concrete Form Market size Outlook by Segments, 2021-2030

By Product

Polystyrene Foam

Polyurethane Foam

Cement-Bonded Wood Fiber

Others

By Application

Residential

Non-Residential

12 Middle East and Africa Insulated Concrete Form Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Insulated Concrete Form Markets in 2024

12.2 Middle East and Africa Insulated Concrete Form Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Insulated Concrete Form Market size Outlook by Segments, 2021-2030

By Product

Polystyrene Foam

Polyurethane Foam

Cement-Bonded Wood Fiber

Others

By Application

Residential

Non-Residential

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Amvic Building System Inc

BASF SE

ConForm Global

Fox Blocks

Kore Insulation

LiteForm Technologies LLC

Logix Insulated Concrete Forms Ltd

Nudura Corp

Polycrete International Ltd

Quad-Lock Building Systems Ltd

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Product

Polystyrene Foam

Polyurethane Foam

Cement-Bonded Wood Fiber

Others

By Application

Residential

Non-Residential

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)