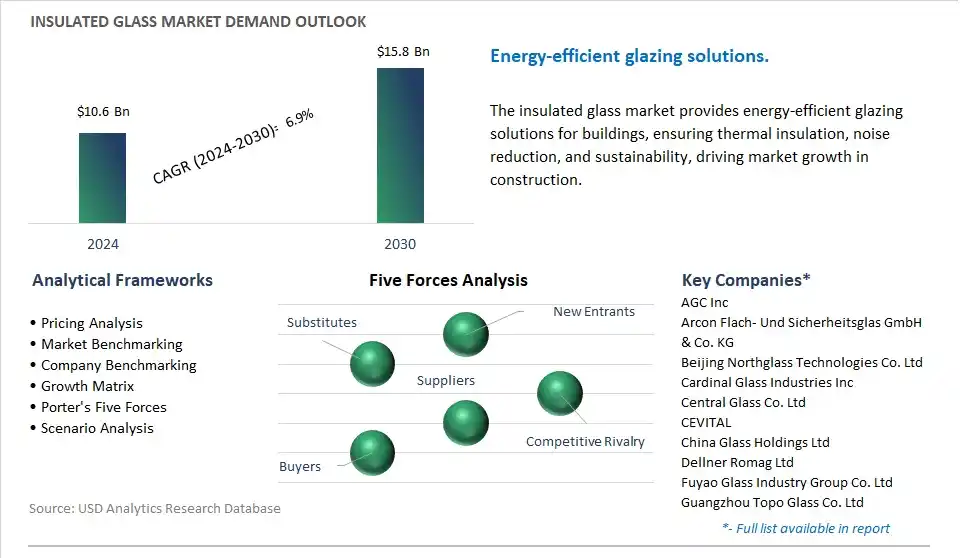

The global Insulated Glass Market is poised to register a 6.9% CAGR from $10.6 Billion in 2024 to $15.8 Billion in 2030.

The global Insulated Glass Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (Heated Insulating Glass, Tempering Insulating Glass, Custom Insulated Glass, Others), By End-User (Residential Buildings, Commercial and Institutional Buildings, Industries Users), By Application (Door Partitions, Furniture and Curtain Walls, Kitchen Appliances and Cabinets, Railings and Bolted Structure, Floors and Ceilings, Automotive Glasses).

An Introduction to Global Insulated Glass Market in 2024

Insulated glass, also known as double glazing or double-pane glass, is a type of window or glass unit composed of two or more glass panes separated by an air or gas-filled space, providing thermal insulation, noise reduction, and energy efficiency in buildings. One key trend shaping the future of insulated glass is the development of advanced glass coatings, spacer materials, and assembly techniques to improve thermal performance, durability, and sustainability while meeting increasingly stringent energy codes and green building standards. Glass manufacturers and glazing companies are innovating new low-emissivity (low-E) coatings, gas fillings (such as argon or krypton), and warm-edge spacer materials, enhancing thermal resistance and reducing heat transfer through the window assembly, resulting in lower energy consumption for heating and cooling in buildings. Additionally, advancements in glass fabrication technologies, such as vacuum insulating glass (VIG) and suspended particle devices (SPD), are enabling the production of high-performance insulated glass units with enhanced optical clarity, solar control, and dynamic shading capabilities, improving occupant comfort and building aesthetics while maximizing daylighting and views. Moreover, the integration of smart glass technologies, such as electrochromic and thermochromic glazing, is enabling dynamic control of light transmission and solar heat gain, optimizing energy efficiency and occupant comfort in response to changing environmental conditions and user preferences. As building owners and architects seek to design energy-efficient, sustainable, and comfortable environments, the market for insulated glass is poised for innovation and growth, with opportunities for collaboration, research, and market expansion to meet the evolving needs of the construction industry and regulatory stakeholders.

Insulated Glass Market Competitive Landscape

The market report analyses the leading companies in the industry including AGC Inc, Arcon Flach- Und Sicherheitsglas GmbH & Co. KG, Beijing Northglass Technologies Co. Ltd, Cardinal Glass Industries Inc, Central Glass Co. Ltd, CEVITAL, China Glass Holdings Ltd, Dellner Romag Ltd, Fuyao Glass Industry Group Co. Ltd, Guangzhou Topo Glass Co. Ltd, Guardian Industries, Nippon Sheet Glass Co. Ltd, Qingdao Tsing Glass Co. Ltd, Saint-Gobain, SCHOTT AG, Sisecam, Taiwan Glass Ind. Corp, Xinyi Glass Holdings Ltd.

Insulated Glass Market Dynamics

Insulated Glass Market Trend: Growing Demand for Energy-Efficient Building Solutions

A prominent trend in the market for insulated glass is the growing demand for energy-efficient building solutions. With increasing concerns about energy consumption, greenhouse gas emissions, and climate change, there is a rising preference for building materials that improve thermal performance, reduce heat loss or gain, and enhance overall energy efficiency in buildings. Insulated glass, also known as double or triple glazing, consists of multiple glass panes separated by insulating spacers and sealed with inert gas, providing superior thermal insulation compared to single-pane windows. The shift towards energy-efficient buildings is driving the adoption of insulated glass in residential, commercial, and institutional construction projects worldwide.

Insulated Glass Market Driver: Stringent Building Energy Codes and Regulations

A key driver propelling the market for insulated glass is the implementation of stringent building energy codes and regulations. Governments, building codes, and regulatory agencies worldwide are mandating energy efficiency requirements for new construction and renovations to reduce energy consumption, combat climate change, and promote sustainable development. Building energy codes typically require minimum levels of thermal performance for windows and glazing systems, driving the demand for insulated glass as a preferred solution to meet these requirements. Additionally, incentives such as tax credits, rebates, and grants are offered to encourage the adoption of energy-efficient building materials and technologies, further stimulating market demand for insulated glass. The need to comply with energy codes, achieve green building certifications, and optimize building performance is driving the adoption of insulated glass as an essential component of energy-efficient building envelopes.

Insulated Glass Market Opportunity: Expansion into Smart and Dynamic Glass Technologies

An opportunity for growth in the market for insulated glass lies in the expansion into smart and dynamic glass technologies. While traditional insulated glass provides thermal insulation and daylighting benefits, there is potential to integrate smart glass technologies that offer additional functionalities such as dynamic tinting, solar control, and glare reduction. Smart glass, also known as switchable glass or electrochromic glass, can change its optical properties in response to external stimuli such as light, heat, or electrical signals, allowing for on-demand control of transparency, shading, and thermal performance. By incorporating smart glass technologies into insulated glass units, manufacturers can offer innovative solutions that enhance occupant comfort, energy efficiency, and building aesthetics. Additionally, partnerships with technology providers, research institutions, and building automation companies can facilitate the development and commercialization of smart glass products, enabling companies to capitalize on the opportunity to provide advanced glazing solutions for the evolving needs of the construction industry.

Insulated Glass Market Ecosystem

The insulated glass market involves a series of stages, with raw material acquisition where float glass manufacturers including AGC Inc. and Saint-Gobain provide the primary flat glass used for insulated glass units. Chemical manufacturers including DuPont de Nemours, Inc. and Solvay SA contribute spacer and desiccant materials for IG units. Glass processing follows, with coating companies including PPG Industries Inc. and Nippon Paint Holdings Co., Ltd. producing low-emissivity coatings for enhanced energy efficiency. Insulated glass unit (IGU) manufacturing is then characterized by the presence of companies including Guardian Industries Corp and Asahi Glass Co., Ltd., assembling float glass pieces with spacers and desiccants, and sealing them with secondary sealants.

Distribution channels include building material distributors including Builders FirstSource and specialized glass distributors providing IG units and related components to window manufacturers and installers. Window and door manufacturing, handled by companies including Marvin Companies and VELUX Group, incorporates IG units into their products, while glazing contractors and window installers specialize in installing IG units into window frames and building facades. The end-users span residential and commercial construction sectors, including single-family homes, multi-unit dwellings, office buildings, and retail spaces, where insulated glass units are essential for energy-efficient windows and building envelopes.

Insulated Glass Market Share Analysis: Tempering Insulating Glass held the dominant revenue share in 2024

The tempering insulating glass segment stands as the largest sector in the Insulated Glass Market, driven by diverse pivotal factors contributing to its dominance. Tempering insulating glass, also known as double-glazed or double-pane glass, consists of two or more panes of glass separated by a sealed air space filled with an insulating gas such as argon or krypton. One of the primary reasons for the dominance of tempering insulating glass in the market is its widespread application in commercial and residential buildings for energy efficiency and thermal performance. The double-pane design of tempering insulating glass provides superior thermal insulation properties, reducing heat transfer between indoor and outdoor environments and helping to maintain comfortable interior temperatures year-round. Additionally, tempering insulating glass enhances acoustic insulation, reducing noise transmission from outside sources and enhancing occupant comfort in buildings located in noisy urban areas or near transportation hubs. In addition, tempering insulating glass offers enhanced safety and security features compared to single-pane glass, as the multiple layers provide added strength and resistance to impact, breakage, and forced entry attempts. Further, tempering insulating glass can be customized to meet specific performance requirements, including low-emissivity coatings for improved energy efficiency, tinted or reflective coatings for solar control, and decorative finishes for aesthetic appeal. Additionally, the growing emphasis on sustainability and green building practices drives the adoption of tempering insulating glass in construction projects seeking to achieve energy efficiency certifications such as LEED (Leadership in Energy and Environmental Design) and BREEAM (Building Research Establishment Environmental Assessment Method). Further, the increasing awareness of the importance of energy conservation, coupled with rising energy costs and government incentives for energy-efficient building materials, further propels the demand for tempering insulating glass in both new construction and retrofit projects. As architects, designers, builders, and property owners prioritize energy performance, comfort, and sustainability in building design and construction, the tempering insulating glass segment of the insulated glass market is expected to maintain its leading position and witness sustained growth in the foreseeable future.

Insulated Glass Market Share Analysis: Residential Buildings is the fastest growing market segment over the forecast period to 2030

The residential buildings segment is the fastest-growing sector in the Insulated Glass Market, driven by diverse critical factors propelling its rapid expansion. One of the primary reasons for the rapid growth of insulated glass usage in residential buildings is the increasing awareness and demand for energy-efficient and sustainable building solutions among homeowners, architects, and developers. Insulated glass, also known as double-glazed or triple-glazed windows, plays a crucial role in improving the energy performance of residential buildings by reducing heat loss in winter and heat gain in summer, thus lowering heating and cooling costs and enhancing indoor comfort. Additionally, insulated glass enhances acoustic insulation, reducing noise transmission from outside sources such as traffic, construction, or neighbors, and improving the overall quality of life for residents. In addition, the growing trend toward eco-friendly and green building practices, driven by concerns about climate change, environmental sustainability, and energy conservation, drives the adoption of insulated glass in residential construction projects seeking to achieve green building certifications such as LEED (Leadership in Energy and Environmental Design) and Energy Star. Further, government initiatives, incentives, and regulations promoting energy-efficient building materials and practices further encourage the adoption of insulated glass in residential buildings. Additionally, the increasing availability and affordability of insulated glass products, coupled with advancements in manufacturing technologies and installation methods, make it easier and more cost-effective for homeowners and builders to incorporate insulated glass into new construction and renovation projects. In addition, the COVID-19 pandemic, which has led to increased time spent at home and a greater emphasis on home comfort and wellness, has further fueled the demand for energy-efficient and soundproofing solutions such as insulated glass windows and doors in residential buildings. As homeowners increasingly prioritize energy savings, comfort, and sustainability in their homes, the residential buildings segment of the insulated glass market is expected to experience robust growth, presenting lucrative opportunities for manufacturers, suppliers, and installers of insulated glass products tailored for residential applications.

Insulated Glass Market Share Analysis: Automotive Glasses is the fastest growing market segment over the forecast period to 2030

The automotive glasses segment is the fastest-growing sector in the Insulated Glass Market, driven by diverse critical factors propelling its rapid expansion. One of the primary reasons for the rapid growth of insulated glass usage in automotive applications is the increasing demand for advanced safety, comfort, and energy efficiency features in modern vehicles. Insulated glass, also known as laminated or tempered automotive glass, plays a crucial role in improving the overall performance and comfort of vehicles by providing enhanced thermal insulation, soundproofing, and UV protection. Additionally, insulated glass contributes to occupant safety by providing greater structural integrity and impact resistance compared to traditional single-pane glass windows. In addition, the growing trend toward electric and hybrid vehicles, which require efficient climate control systems to maximize battery range and performance, drives the adoption of insulated glass windows and sunroofs in automotive interiors. Further, technological advancements in automotive glass manufacturing, such as lightweighting, thin-film coatings, and smart glass technologies, enhance the functionality and aesthetic appeal of insulated glass products, further driving their adoption in the automotive industry. Additionally, stringent regulations and safety standards mandating the use of laminated and tempered glass in automotive applications to protect occupants from injuries during collisions and rollover accidents further fuel the demand for insulated glass in the automotive sector. In addition, the increasing focus on interior comfort and luxury features in premium and luxury vehicles, including panoramic sunroofs, privacy glass, and acoustic laminated glass, drives the adoption of insulated glass solutions tailored for automotive applications. Additionally, the growing popularity of autonomous and connected vehicles, which require advanced sensor and communication technologies integrated into the vehicle's glass surfaces, further accelerates the adoption of insulated glass in automotive design and engineering. As automotive manufacturers and consumers prioritize safety, comfort, and sustainability in vehicle design and manufacturing, the automotive glasses segment of the insulated glass market is expected to experience robust growth, presenting lucrative opportunities for manufacturers, suppliers, and technology providers in the automotive and glass industries.

Insulated Glass Market Report Scope-

By Type

Heated Insulating Glass

Tempering Insulating Glass

Custom Insulated Glass

Others

By End-User

Residential Buildings

Commercial and Institutional Buildings

Industries Users

By Application

Door Partitions

Furniture and Curtain Walls

Kitchen Appliances and Cabinets

Railings and Bolted Structure

Floors and Ceilings

Automotive Glasses

Insulated Glass Market Companies Profiled

AGC Inc

Arcon Flach- Und Sicherheitsglas GmbH & Co. KG

Beijing Northglass Technologies Co. Ltd

Cardinal Glass Industries Inc

Central Glass Co. Ltd

CEVITAL

China Glass Holdings Ltd

Dellner Romag Ltd

Fuyao Glass Industry Group Co. Ltd

Guangzhou Topo Glass Co. Ltd

Guardian Industries

Nippon Sheet Glass Co. Ltd

Qingdao Tsing Glass Co. Ltd

Saint-Gobain

SCHOTT AG

Sisecam

Taiwan Glass Ind. Corp

Xinyi Glass Holdings Ltd

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Insulated Glass Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Insulated Glass Market Size Outlook, $ Million, 2021 to 2030

3.2 Insulated Glass Market Outlook by Type, $ Million, 2021 to 2030

3.3 Insulated Glass Market Outlook by Product, $ Million, 2021 to 2030

3.4 Insulated Glass Market Outlook by Application, $ Million, 2021 to 2030

3.5 Insulated Glass Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Insulated Glass Industry

4.2 Key Market Trends in Insulated Glass Industry

4.3 Potential Opportunities in Insulated Glass Industry

4.4 Key Challenges in Insulated Glass Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Insulated Glass Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Insulated Glass Market Outlook by Segments

7.1 Insulated Glass Market Outlook by Segments, $ Million, 2021- 2030

By Type

Heated Insulating Glass

Tempering Insulating Glass

Custom Insulated Glass

Others

By End-User

Residential Buildings

Commercial and Institutional Buildings

Industries Users

By Application

Door Partitions

Furniture and Curtain Walls

Kitchen Appliances and Cabinets

Railings and Bolted Structure

Floors and Ceilings

Automotive Glasses

8 North America Insulated Glass Market Analysis and Outlook To 2030

8.1 Introduction to North America Insulated Glass Markets in 2024

8.2 North America Insulated Glass Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Insulated Glass Market size Outlook by Segments, 2021-2030

By Type

Heated Insulating Glass

Tempering Insulating Glass

Custom Insulated Glass

Others

By End-User

Residential Buildings

Commercial and Institutional Buildings

Industries Users

By Application

Door Partitions

Furniture and Curtain Walls

Kitchen Appliances and Cabinets

Railings and Bolted Structure

Floors and Ceilings

Automotive Glasses

9 Europe Insulated Glass Market Analysis and Outlook To 2030

9.1 Introduction to Europe Insulated Glass Markets in 2024

9.2 Europe Insulated Glass Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Insulated Glass Market Size Outlook by Segments, 2021-2030

By Type

Heated Insulating Glass

Tempering Insulating Glass

Custom Insulated Glass

Others

By End-User

Residential Buildings

Commercial and Institutional Buildings

Industries Users

By Application

Door Partitions

Furniture and Curtain Walls

Kitchen Appliances and Cabinets

Railings and Bolted Structure

Floors and Ceilings

Automotive Glasses

10 Asia Pacific Insulated Glass Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Insulated Glass Markets in 2024

10.2 Asia Pacific Insulated Glass Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Insulated Glass Market size Outlook by Segments, 2021-2030

By Type

Heated Insulating Glass

Tempering Insulating Glass

Custom Insulated Glass

Others

By End-User

Residential Buildings

Commercial and Institutional Buildings

Industries Users

By Application

Door Partitions

Furniture and Curtain Walls

Kitchen Appliances and Cabinets

Railings and Bolted Structure

Floors and Ceilings

Automotive Glasses

11 South America Insulated Glass Market Analysis and Outlook To 2030

11.1 Introduction to South America Insulated Glass Markets in 2024

11.2 South America Insulated Glass Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Insulated Glass Market size Outlook by Segments, 2021-2030

By Type

Heated Insulating Glass

Tempering Insulating Glass

Custom Insulated Glass

Others

By End-User

Residential Buildings

Commercial and Institutional Buildings

Industries Users

By Application

Door Partitions

Furniture and Curtain Walls

Kitchen Appliances and Cabinets

Railings and Bolted Structure

Floors and Ceilings

Automotive Glasses

12 Middle East and Africa Insulated Glass Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Insulated Glass Markets in 2024

12.2 Middle East and Africa Insulated Glass Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Insulated Glass Market size Outlook by Segments, 2021-2030

By Type

Heated Insulating Glass

Tempering Insulating Glass

Custom Insulated Glass

Others

By End-User

Residential Buildings

Commercial and Institutional Buildings

Industries Users

By Application

Door Partitions

Furniture and Curtain Walls

Kitchen Appliances and Cabinets

Railings and Bolted Structure

Floors and Ceilings

Automotive Glasses

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

AGC Inc

Arcon Flach- Und Sicherheitsglas GmbH & Co. KG

Beijing Northglass Technologies Co. Ltd

Cardinal Glass Industries Inc

Central Glass Co. Ltd

CEVITAL

China Glass Holdings Ltd

Dellner Romag Ltd

Fuyao Glass Industry Group Co. Ltd

Guangzhou Topo Glass Co. Ltd

Guardian Industries

Nippon Sheet Glass Co. Ltd

Qingdao Tsing Glass Co. Ltd

Saint-Gobain

SCHOTT AG

Sisecam

Taiwan Glass Ind. Corp

Xinyi Glass Holdings Ltd

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise