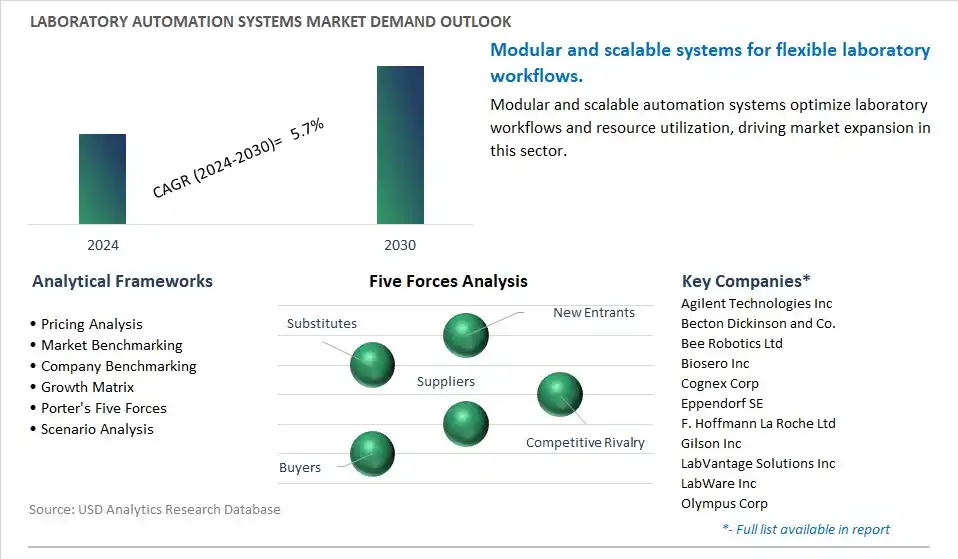

Laboratory Automation Systems Market is estimated to increase at a growth rate of 5.7% CAGR over the forecast period from 2024 to 2030.

The global Laboratory Automation Systems Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments including By End-User (Pharmaceutical and biotechnology companies, Clinical and reference laboratories, Academic institutions and research organizations, Others), By Type (Equipment, Software and services).

An Introduction to Laboratory Automation Systems Market in 2024

The Laboratory Automation Systems Market encompasses robotic systems, integrated platforms, and software solutions used to automate laboratory workflows, sample processing, and data analysis in scientific research, diagnostics, and drug discovery. These automation systems include liquid handling robots, assay platforms, plate readers, sample management systems, and laboratory information management systems (LIMS) used in high-throughput screening, genomics, proteomics, and clinical laboratories. The market serves pharmaceutical companies, biotechnology firms, academic research centers, and clinical labs aiming to increase efficiency, reduce manual errors, and accelerate scientific discoveries. Innovations in laboratory automation systems focus on modularity, scalability, flexibility, artificial intelligence, machine learning, and cloud-based solutions, enabling streamlined and cost-effective laboratory operations across various scientific disciplines.

Laboratory Automation Systems Market Competitive Landscape

The global Laboratory Automation Systems Industry is highly competitive with a large number of companies focusing on niche market segments. Amidst intense competitive conditions, Laboratory Automation Systems Companies are investing in new product launches and strengthening distribution channels. Key companies operating in the Laboratory Automation Systems Industry include- Agilent Technologies Inc, Becton Dickinson and Co., Bee Robotics Ltd, Biosero Inc, Cognex Corp, Eppendorf SE, F. Hoffmann La Roche Ltd, Gilson Inc, LabVantage Solutions Inc, LabWare Inc, Olympus Corp, PerkinElmer Inc, QIAGEN N.V., SCINOMIX, Siemens AG, SPT Labtech Ltd, Tecan Trading AG, Thermo Fisher Scientific Inc.

Laboratory Automation Systems Market Trend: Integration of Robotics and Artificial Intelligence (AI)

A prominent trend in the laboratory automation systems market is the integration of robotics and artificial intelligence (AI) technologies to enhance automation, efficiency, and productivity in laboratory workflows. Modern laboratory automation systems are equipped with robotic arms, grippers, and workstations capable of performing a wide range of repetitive tasks, such as sample handling, liquid dispensing, and plate manipulation, with high precision and accuracy. Additionally, AI algorithms are utilized for intelligent task scheduling, optimization of experimental protocols, and adaptive decision-making based on real-time data analysis. The integration of robotics and AI enables laboratories to streamline operations, reduce manual intervention, and increase throughput, making automation systems indispensable tools for high-throughput screening, drug discovery, and clinical diagnostics. This trend towards advanced automation solutions revolutionizes laboratory workflows, driving market demand for next-generation automation systems that offer seamless integration, scalability, and flexibility to meet the evolving needs of research and industry.

Laboratory Automation Systems Market Driver: Demand for Increased Efficiency and Reproducibility

The primary driver of the laboratory automation systems market is the growing demand for increased efficiency and reproducibility in laboratory workflows across various industries, including pharmaceuticals, biotechnology, and academic research. Laboratories face challenges associated with manual handling of samples, reagents, and consumables, leading to errors, inconsistencies, and inefficiencies in experimental procedures. Automation systems address these challenges by providing standardized, reproducible, and reliable workflows, minimizing variability and improving data quality. Moreover, automation enables laboratories to achieve higher throughput, faster turnaround times, and greater experimental precision, facilitating scientific discoveries, accelerating drug development processes, and enhancing diagnostic accuracy. As laboratories strive to improve efficiency, reduce costs, and enhance research outcomes, the demand for laboratory automation systems continues to grow, driving market expansion and innovation in automated solutions tailored to diverse applications and workflows.

Laboratory Automation Systems Market Opportunity: Expansion into Emerging Applications and Markets

An opportunity in the laboratory automation systems market lies in the expansion into emerging applications and markets with unmet needs for advanced automation solutions. Emerging applications, such as personalized medicine, single-cell analysis, and synthetic biology, present unique challenges and requirements for automation systems capable of handling complex experimental workflows and diverse sample types. Moreover, there is an opportunity to target emerging markets, such as Asia-Pacific and Latin America, where rapid economic growth, increasing investments in research infrastructure, and rising healthcare expenditures drive demand for laboratory automation technologies. By addressing the specific needs of emerging applications and markets, manufacturers can expand their customer base, diversify their product portfolios, and capture new growth opportunities in the laboratory automation systems market. Furthermore, there is an opportunity to develop specialized automation solutions for niche applications, such as cell therapy manufacturing, genomics research, and high-content screening, catering to the unique requirements of researchers and industry professionals in specialized fields.

Laboratory Automation Systems Market Share Analysis: Pharmaceutical and Biotechnology Companies is the fastest growing market segment over the forecast period to 2030

Among laboratory automation systems, the segment experiencing the fastest growth is "Pharmaceutical and Biotechnology Companies." This growth can be attributed to several factors. Firstly, pharmaceutical and biotechnology companies are increasingly investing in laboratory automation to streamline their research and development processes, aiming to accelerate drug discovery and development timelines. Automated workstations, liquid handlers, plate handlers, and robotic arms enable these companies to perform high-throughput screening, compound management, and assay development with greater efficiency and reproducibility. Additionally, the growing emphasis on precision medicine and personalized therapeutics has led to an expansion in genomic and proteomic studies, driving the demand for advanced automation solutions in these sectors. Furthermore, regulatory requirements for stringent quality control and data integrity in drug development necessitate the adoption of automated systems to ensure compliance and enhance productivity. As pharmaceutical and biotechnology companies continue to prioritize innovation and efficiency in their operations, the demand for laboratory automation systems in this segment is poised for significant growth.

Laboratory Automation Systems Market Segmentation

By End-User

Pharmaceutical and biotechnology companies

Clinical and reference laboratories

Academic institutions and research organizations

Others

By Type

Equipment

-Automated Workstations

-Automated Storage & Retrieval Systems

-Automated Liquid Handlers

-Automated Plate Handlers

-Robotic Arms

Software and services

Geographical Analysis

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Laboratory Automation Systems Companies

Agilent Technologies Inc

Becton Dickinson and Co.

Bee Robotics Ltd

Biosero Inc

Cognex Corp

Eppendorf SE

F. Hoffmann La Roche Ltd

Gilson Inc

LabVantage Solutions Inc

LabWare Inc

Olympus Corp

PerkinElmer Inc

QIAGEN N.V.

SCINOMIX

Siemens AG

SPT Labtech Ltd

Tecan Trading AG

Thermo Fisher Scientific Inc

* List not Exhaustive

Reasons to Buy the Laboratory Automation Systems Market Study

• Deepen your industry insights and navigate uncertainties for strategy formulation, CAPEX, and Operational decisions

• Gain access to detailed insights on the Laboratory Automation Systems Market, encompassing current market size, growth trends, and forecasts till 2030.

• Access detailed competitor analysis, enabling competitive advantage through a thorough understanding of market players, strategies, and potential differentiation opportunities

• Stay ahead of the curve with insights on technological advancements, innovations, and upcoming trends

• Identify lucrative investment avenues and expansion opportunities within the Laboratory Automation Systems Industry, guided by robust, data-backed analysis.

• Understand regional and global markets through country-wise analysis, regional market potential, regulatory nuances, and dynamics

• Execute strategies with confidence and speed through information, analytics, and insights on the industry value chain

• Corporate leaders, strategists, financial experts, shareholders, asset managers, and governmental representatives can make long-term planning scenarios and build an integrated and timely understanding of market dynamics

• Benefit from tailored solutions and expert consultation based on report insights, providing personalized strategies aligned with specific business needs.

TABLE OF CONTENTS

1 Introduction to 2024 Laboratory Automation Systems Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Analyzed

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Laboratory Automation Systems Market Size Outlook, $ Million, 2021 to 2030

3.2 Laboratory Automation Systems Market Outlook by Type, $ Million, 2021 to 2030

3.3 Laboratory Automation Systems Market Outlook by Product, $ Million, 2021 to 2030

3.4 Laboratory Automation Systems Market Outlook by Application, $ Million, 2021 to 2030

3.5 Laboratory Automation Systems Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Laboratory Automation Systems Industry

4.2 Key Market Trends in Laboratory Automation Systems Industry

4.3 Potential Opportunities in Laboratory Automation Systems Industry

4.4 Key Challenges in Laboratory Automation Systems Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Laboratory Automation Systems Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Laboratory Automation Systems Market Outlook by Segments

7.1 Laboratory Automation Systems Market Outlook by Segments, $ Million, 2021- 2030

By End-User

Pharmaceutical and biotechnology companies

Clinical and reference laboratories

Academic institutions and research organizations

Others

By Type

Equipment

-Automated Workstations

-Automated Storage & Retrieval Systems

-Automated Liquid Handlers

-Automated Plate Handlers

-Robotic Arms

Software and services

8 North America Laboratory Automation Systems Market Analysis and Outlook To 2030

8.1 Introduction to North America Laboratory Automation Systems Markets in 2024

8.2 North America Laboratory Automation Systems Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Laboratory Automation Systems Market size Outlook by Segments, 2021-2030

By End-User

Pharmaceutical and biotechnology companies

Clinical and reference laboratories

Academic institutions and research organizations

Others

By Type

Equipment

-Automated Workstations

-Automated Storage & Retrieval Systems

-Automated Liquid Handlers

-Automated Plate Handlers

-Robotic Arms

Software and services

9 Europe Laboratory Automation Systems Market Analysis and Outlook To 2030

9.1 Introduction to Europe Laboratory Automation Systems Markets in 2024

9.2 Europe Laboratory Automation Systems Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Laboratory Automation Systems Market Size Outlook by Segments, 2021-2030

By End-User

Pharmaceutical and biotechnology companies

Clinical and reference laboratories

Academic institutions and research organizations

Others

By Type

Equipment

-Automated Workstations

-Automated Storage & Retrieval Systems

-Automated Liquid Handlers

-Automated Plate Handlers

-Robotic Arms

Software and services

10 Asia Pacific Laboratory Automation Systems Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Laboratory Automation Systems Markets in 2024

10.2 Asia Pacific Laboratory Automation Systems Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Laboratory Automation Systems Market size Outlook by Segments, 2021-2030

By End-User

Pharmaceutical and biotechnology companies

Clinical and reference laboratories

Academic institutions and research organizations

Others

By Type

Equipment

-Automated Workstations

-Automated Storage & Retrieval Systems

-Automated Liquid Handlers

-Automated Plate Handlers

-Robotic Arms

Software and services

11 South America Laboratory Automation Systems Market Analysis and Outlook To 2030

11.1 Introduction to South America Laboratory Automation Systems Markets in 2024

11.2 South America Laboratory Automation Systems Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Laboratory Automation Systems Market size Outlook by Segments, 2021-2030

By End-User

Pharmaceutical and biotechnology companies

Clinical and reference laboratories

Academic institutions and research organizations

Others

By Type

Equipment

-Automated Workstations

-Automated Storage & Retrieval Systems

-Automated Liquid Handlers

-Automated Plate Handlers

-Robotic Arms

Software and services

12 Middle East and Africa Laboratory Automation Systems Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Laboratory Automation Systems Markets in 2024

12.2 Middle East and Africa Laboratory Automation Systems Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Laboratory Automation Systems Market size Outlook by Segments, 2021-2030

By End-User

Pharmaceutical and biotechnology companies

Clinical and reference laboratories

Academic institutions and research organizations

Others

By Type

Equipment

-Automated Workstations

-Automated Storage & Retrieval Systems

-Automated Liquid Handlers

-Automated Plate Handlers

-Robotic Arms

Software and services

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

List of Companies

Agilent Technologies Inc

Becton Dickinson and Co.

Bee Robotics Ltd

Biosero Inc

Cognex Corp

Eppendorf SE

F. Hoffmann La Roche Ltd

Gilson Inc

LabVantage Solutions Inc

LabWare Inc

Olympus Corp

PerkinElmer Inc

QIAGEN N.V.

SCINOMIX

Siemens AG

SPT Labtech Ltd

Tecan Trading AG

Thermo Fisher Scientific Inc

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise