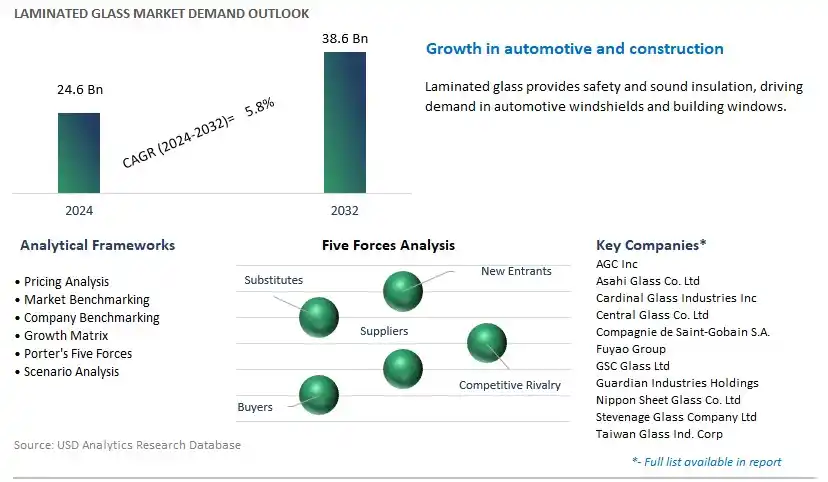

Global Laminated Glass Market Size is valued at $24.6 Billion in 2024 and is forecast to register a growth rate (CAGR) of 5.8% to reach $38.6 Billion by 2032.

The global Laminated Glass Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (Polyvinyl Butyral (PVB), Sentryglas Plus (SGP), Ethylene-vinyl Acetate (EVA), Others), By End-User (Automotive, Building and Construction, Electronics, Others).

An Introduction to Laminated Glass Market in 2024

Laminated glass s to gain prominence in 2024, driven by its superior safety, security, and aesthetic properties in architectural, automotive, and specialty glass applications. Laminated glass consists of two or more glass layers bonded together with a durable interlayer such as polyvinyl butyral (PVB) or ethylene-vinyl acetate (EVA), offering benefits such as impact resistance, sound insulation, UV protection, and enhanced structural integrity. In the architectural sector, laminated glass is used for facades, windows, doors, and skylights in commercial buildings, residential homes, and public infrastructure projects, providing protection against break-ins, natural disasters, and noise pollution while allowing natural light transmission and design flexibility. In the automotive industry, laminated glass is employed for windshields, side windows, and sunroofs, offering occupant safety, crash resistance, and improved acoustic comfort. Further, laminated glass finds applications in specialty markets such as marine, aviation, and security glazing, where stringent safety and performance requirements must be met. With increasing awareness of the benefits of laminated glass and advancements in glass manufacturing technology, the market is poised for further growth, driven by its indispensable role in enhancing safety and aesthetics in diverse applications.

Laminated Glass Market Competitive Landscape

The market report analyses the leading companies in the industry including AGC Inc, Asahi Glass Co. Ltd, Cardinal Glass Industries Inc, Central Glass Co. Ltd, Compagnie de Saint-Gobain S.A., Fuyao Group, GSC Glass Ltd, Guardian Industries Holdings, Nippon Sheet Glass Co. Ltd, Stevenage Glass Company Ltd, Taiwan Glass Ind. Corp, and others.

Laminated Glass Market Dynamics

Market Trend: Growing Demand for Safety and Security Features in Buildings

A significant trend in the laminated glass market is the increasing demand for safety and security features in buildings. With rising concerns about safety, burglary, and natural disasters, consumers, architects, and developers are prioritizing the use of laminated glass for windows, doors, facades, and partitions. Laminated glass offers enhanced strength, durability, and resistance to impact, making it a preferred choice for applications where safety and security are paramount. Additionally, laminated glass can provide protection against UV radiation, noise reduction, and improved energy efficiency, further driving its adoption in residential, commercial, and institutional buildings worldwide.

Market Driver: Stringent Building Codes and Regulations

A key driver of the laminated glass market is the implementation of stringent building codes and regulations governing safety, energy efficiency, and environmental sustainability. Governments and regulatory bodies worldwide are mandating the use of laminated glass in building construction to enhance structural integrity, mitigate the risk of injuries from glass breakage, and improve overall building performance. Moreover, the growing awareness of the environmental impact of buildings has led to the development of green building standards that encourage the use of sustainable materials like laminated glass. As compliance with building codes becomes mandatory, the demand for laminated glass is expected to surge, particularly in regions prone to seismic activity, hurricanes, or high crime rates.

Market Opportunity: Expansion into Automotive and Transportation Sector

A potential opportunity for the laminated glass market lies in expanding its applications beyond the building and construction sector into the automotive and transportation industry. Laminated glass offers several benefits for vehicle safety, including improved impact resistance, reduced risk of shattering, and enhanced sound insulation. With the rising demand for advanced safety features in automobiles and the increasing focus on lightweight materials to improve fuel efficiency, laminated glass presents an attractive alternative to traditional automotive glass. Furthermore, the adoption of electric and autonomous vehicles is driving the need for advanced glazing solutions that provide optimal visibility, comfort, and protection for passengers. By diversifying into the automotive sector and developing innovative laminated glass products tailored to the specific requirements of vehicle manufacturers, laminated glass suppliers can capitalize on new market opportunities and expand their customer base.

Laminated Glass Market Share Analysis: Polyvinyl Butyral (PVB) segment generated the highest revenue in 2024

Within the Laminated Glass Market, the Polyvinyl Butyral (PVB) segment is the largest. PVB is the most commonly used interlayer material in laminated glass manufacturing due to its excellent adhesive properties, clarity, and ability to absorb impact energy, making laminated glass safer and more durable. Laminated glass with PVB interlayers is widely used in applications such as automotive windshields, architectural glazing, and safety glass for buildings, homes, and public spaces. The popularity of PVB in laminated glass is attributed to its ability to hold glass fragments together upon impact, reducing the risk of injury from shattered glass and providing enhanced security and protection against forced entry and break-ins. Additionally, PVB interlayers offer sound insulation properties, UV resistance, and UV blocking capabilities, further enhancing the performance and functionality of laminated glass in various applications. The established infrastructure for PVB production, along with its cost-effectiveness and widespread availability, contributes to the dominance of the PVB segment within the Laminated Glass Market.

Laminated Glass Market Share Analysis: Building and Construction is poised to register the fastest CAGR over the forecast period

Among the end-user segments in the Laminated Glass Market, the Building and Construction segment stands out as the fastest-growing. Laminated glass finds extensive applications in the construction industry for various architectural purposes, including facades, windows, doors, skylights, and balustrades. The growing emphasis on safety, security, and energy efficiency in building design and construction fuels the demand for laminated glass solutions. Laminated glass provides enhanced safety compared to traditional monolithic glass by retaining fragments upon breakage, reducing the risk of injury from shattered glass. Moreover, laminated glass with interlayers incorporating advanced technologies such as acoustic control, solar control, and fire resistance addresses the evolving needs of modern buildings for noise reduction, solar heat gain mitigation, and fire safety compliance. Additionally, the increasing adoption of laminated glass in green building projects, driven by sustainability initiatives and regulatory requirements, further contributes to the segment's rapid growth. As architects, builders, and developers prioritize performance, aesthetics, and sustainability in building design, the demand for laminated glass in the Building and Construction segment is expected to continue experiencing accelerated growth within the Laminated Glass Market.

Laminated Glass Market

By Type

Polyvinyl Butyral (PVB)

Sentryglas Plus (SGP)

Ethylene-vinyl Acetate (EVA)

Others

By End-User

Automotive

Building and Construction

Electronics

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Laminated Glass Companies Profiled in the Study

AGC Inc

Asahi Glass Co. Ltd

Cardinal Glass Industries Inc

Central Glass Co. Ltd

Compagnie de Saint-Gobain S.A.

Fuyao Group

GSC Glass Ltd

Guardian Industries Holdings

Nippon Sheet Glass Co. Ltd

Stevenage Glass Company Ltd

Taiwan Glass Ind. Corp

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Laminated Glass Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Laminated Glass Market Size Outlook, $ Million, 2021 to 2032

3.2 Laminated Glass Market Outlook by Type, $ Million, 2021 to 2032

3.3 Laminated Glass Market Outlook by Product, $ Million, 2021 to 2032

3.4 Laminated Glass Market Outlook by Application, $ Million, 2021 to 2032

3.5 Laminated Glass Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Laminated Glass Industry

4.2 Key Market Trends in Laminated Glass Industry

4.3 Potential Opportunities in Laminated Glass Industry

4.4 Key Challenges in Laminated Glass Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Laminated Glass Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Laminated Glass Market Outlook by Segments

7.1 Laminated Glass Market Outlook by Segments, $ Million, 2021- 2032

By Type

Polyvinyl Butyral (PVB)

Sentryglas Plus (SGP)

Ethylene-vinyl Acetate (EVA)

Others

By End-User

Automotive

Building and Construction

Electronics

Others

8 North America Laminated Glass Market Analysis and Outlook To 2032

8.1 Introduction to North America Laminated Glass Markets in 2024

8.2 North America Laminated Glass Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Laminated Glass Market size Outlook by Segments, 2021-2032

By Type

Polyvinyl Butyral (PVB)

Sentryglas Plus (SGP)

Ethylene-vinyl Acetate (EVA)

Others

By End-User

Automotive

Building and Construction

Electronics

Others

9 Europe Laminated Glass Market Analysis and Outlook To 2032

9.1 Introduction to Europe Laminated Glass Markets in 2024

9.2 Europe Laminated Glass Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Laminated Glass Market Size Outlook by Segments, 2021-2032

By Type

Polyvinyl Butyral (PVB)

Sentryglas Plus (SGP)

Ethylene-vinyl Acetate (EVA)

Others

By End-User

Automotive

Building and Construction

Electronics

Others

10 Asia Pacific Laminated Glass Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Laminated Glass Markets in 2024

10.2 Asia Pacific Laminated Glass Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Laminated Glass Market size Outlook by Segments, 2021-2032

By Type

Polyvinyl Butyral (PVB)

Sentryglas Plus (SGP)

Ethylene-vinyl Acetate (EVA)

Others

By End-User

Automotive

Building and Construction

Electronics

Others

11 South America Laminated Glass Market Analysis and Outlook To 2032

11.1 Introduction to South America Laminated Glass Markets in 2024

11.2 South America Laminated Glass Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Laminated Glass Market size Outlook by Segments, 2021-2032

By Type

Polyvinyl Butyral (PVB)

Sentryglas Plus (SGP)

Ethylene-vinyl Acetate (EVA)

Others

By End-User

Automotive

Building and Construction

Electronics

Others

12 Middle East and Africa Laminated Glass Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Laminated Glass Markets in 2024

12.2 Middle East and Africa Laminated Glass Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Laminated Glass Market size Outlook by Segments, 2021-2032

By Type

Polyvinyl Butyral (PVB)

Sentryglas Plus (SGP)

Ethylene-vinyl Acetate (EVA)

Others

By End-User

Automotive

Building and Construction

Electronics

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

AGC Inc

Asahi Glass Co. Ltd

Cardinal Glass Industries Inc

Central Glass Co. Ltd

Compagnie de Saint-Gobain S.A.

Fuyao Group

GSC Glass Ltd

Guardian Industries Holdings

Nippon Sheet Glass Co. Ltd

Stevenage Glass Company Ltd

Taiwan Glass Ind. Corp

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

Polyvinyl Butyral (PVB)

Sentryglas Plus (SGP)

Ethylene-vinyl Acetate (EVA)

Others

By End-User

Automotive

Building and Construction

Electronics

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)