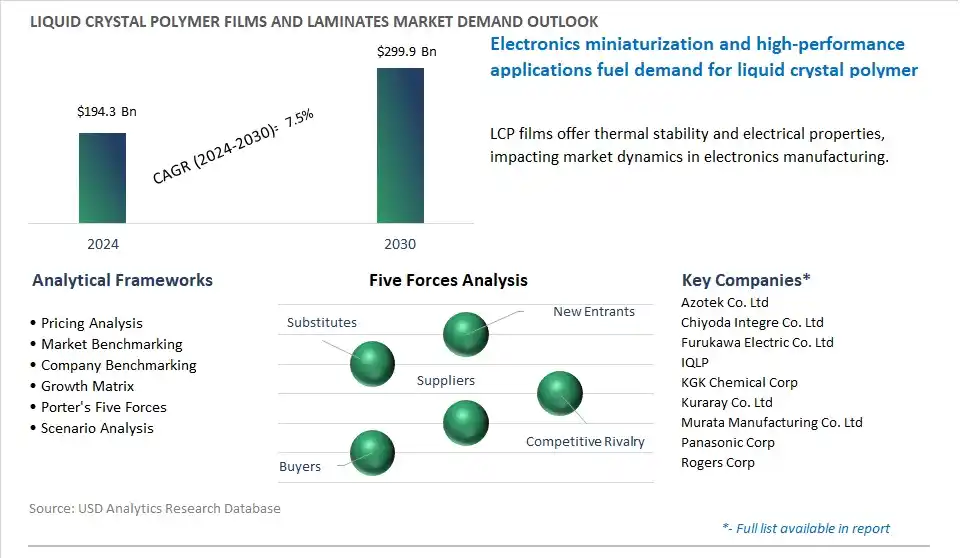

The global Liquid Crystal Polymer Films and Laminates Market is poised to register a 7.5% CAGR from $194.3 Billion in 2024 to $299.9 Billion in 2030.

The global Liquid Crystal Polymer Films and Laminates Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Product (Films, Laminates), By Application (Electrical & Electronics, Packaging, Automotive, Medical Devices, Others).

An Introduction to Global Liquid Crystal Polymer Films and Laminates Market in 2024

The market for liquid crystal polymer (LCP) films and laminates is evolving rapidly driven by their unique combination of properties, including high temperature resistance, chemical inertness, and dimensional stability. Key trends shaping the future of the industry include the increasing demand for miniaturization and lightweighting solutions in electronics, telecommunications, and automotive applications, driving the adoption of LCP films and laminates as high-performance substrates and insulating materials. LCP films, characterized by their low moisture absorption and excellent dielectric properties, are gaining traction in flexible circuitry, antenna systems, and high-frequency applications, enabling the development of compact and high-speed electronic devices. This trend is driving investments in LCP film manufacturing technologies and the development of specialized processing techniques to meet the stringent requirements of electronic packaging and assembly processes. Moreover, the growing demand for high-speed data transmission and 5G infrastructure is fueling the adoption of LCP laminates in printed circuit boards (PCBs) and radio frequency (RF) components, driving innovation in material design and surface treatment technologies to optimize signal integrity and reliability. Additionally, the automotive industry's shift towards electric vehicles and autonomous driving technologies is driving the demand for lightweight and heat-resistant materials, positioning LCP films and laminates as key enablers of innovation in vehicle electronics, sensors, and powertrain systems.

Liquid Crystal Polymer Films and Laminates Market Competitive Landscape

The market report analyses the leading companies in the industry including Azotek Co. Ltd, Chiyoda Integre Co. Ltd, Furukawa Electric Co. Ltd, IQLP, KGK Chemical Corp, Kuraray Co. Ltd, Murata Manufacturing Co. Ltd, Panasonic Corp, Rogers Corp.

Liquid Crystal Polymer Films and Laminates Market Dynamics

Liquid Crystal Polymer Films And Laminates Market Trend: Increased Demand for Miniaturization and High-Performance Electronics

A prominent trend in the liquid crystal polymer (LCP) films and laminates market is the increased demand for miniaturization and high-performance electronics driven by advancements in technology, consumer electronics, and industrial applications. LCP films and laminates offer exceptional properties such as high strength, dimensional stability, chemical resistance, and excellent electrical insulation, making them ideal materials for electronic components, circuitry, and packaging solutions in devices requiring compact designs and reliable performance. With the proliferation of portable electronics, wearables, 5G communication systems, and automotive electronics, there is a growing need for thinner, lighter, and more efficient materials that can withstand high temperatures, harsh environments, and demanding operating conditions. LCP films and laminates address these requirements by providing robust solutions for flexible circuits, antenna systems, thermal management, and electromagnetic shielding, driving market growth and adoption in various industries seeking to optimize electronic designs and enhance product performance.

Liquid Crystal Polymer Films And Laminates Market Driver: Advancements in Flexible and Foldable Display Technologies

A key driver propelling the liquid crystal polymer (LCP) films and laminates market is the advancements in flexible and foldable display technologies driven by consumer demand for innovative and immersive viewing experiences in smartphones, tablets, wearables, and electronic signage. LCP films and laminates serve as essential components in flexible display assemblies, offering superior mechanical properties, thermal stability, and optical clarity compared to traditional materials such as glass and plastic. With the commercialization of foldable smartphones, rollable TVs, and bendable electronic devices, there is a growing need for flexible substrates and protective layers that can withstand repeated bending, twisting, and folding without compromising performance or durability. LCP films and laminates enable the development of thin, lightweight, and bendable displays with high-resolution images, vibrant colors, and responsive touch interfaces, driving market demand and adoption in the rapidly evolving display industry. As flexible display technologies continue to advance and penetrate new markets, the demand for LCP films and laminates is expected to increase, presenting opportunities for manufacturers to capitalize on the growing market for next-generation electronic devices and applications.

Liquid Crystal Polymer Films And Laminates Market Opportunity: Expansion into Automotive and Aerospace Applications

An opportunity for market expansion lies in the expansion into automotive and aerospace applications where liquid crystal polymer (LCP) films and laminates offer potential benefits for lightweighting, high-frequency signal transmission, and thermal management in vehicle interiors, infotainment systems, sensors, antennas, and avionics components. As automotive manufacturers and aerospace companies strive to improve fuel efficiency, reduce emissions, and enhance connectivity in vehicles and aircraft, there is a growing demand for advanced materials that can meet stringent performance requirements while offering weight savings, space efficiency, and reliability. LCP films and laminates, with their combination of mechanical strength, electrical properties, and thermal stability, are well-suited for applications such as radar systems, LiDAR sensors, antenna arrays, power modules, and interior trim panels where lightweight, compact designs and high-performance materials are essential. By leveraging their expertise in material science, engineering, and manufacturing, LCP film and laminate suppliers can collaborate with automotive OEMs, aerospace contractors, and system integrators to develop customized solutions that address specific application needs, driving market penetration and revenue growth in the automotive and aerospace sectors. Additionally, investments in research, testing, and certification can enhance the qualification and acceptance of LCP materials for use in safety-critical and mission-critical applications, further expanding market opportunities and market share in these high-value industries.

Liquid Crystal Polymer Films and Laminates Market Share Analysis: Films segment generated the highest revenue in the industry

The films segment is the largest segment in the liquid crystal polymer (LCP) films and laminates market, primarily due to diverse key factors. LCP films offer a range of unique properties and advantages that make them highly desirable for various applications across industries such as electronics, automotive, aerospace, and healthcare. The LCP films exhibit exceptional mechanical properties, including high tensile strength, stiffness, and dimensional stability, combined with low coefficients of thermal expansion (CTE) and moisture absorption. These properties make LCP films ideal for demanding applications where precision, reliability, and durability are essential, such as flexible printed circuit boards (PCBs), automotive sensors, and medical devices. Additionally, LCP films possess excellent dielectric properties, including low dissipation factor and high insulation resistance, making them suitable for high-frequency and high-speed electronic applications. The films' ability to withstand extreme temperatures, harsh chemical environments, and mechanical stresses further expands their utility in diverse end-use applications. Secondly, LCP films offer exceptional optical clarity, transparency, and heat resistance, making them suitable for use in display technologies, optical films, and light management applications. The films' ability to transmit light efficiently while maintaining dimensional stability and thermal performance is highly valued in applications such as liquid crystal displays (LCDs), touch panels, and optical films for electronic devices. Thirdly, advancements in film manufacturing technologies, including melt extrusion, solvent casting, and stretching techniques, have enabled the production of LCP films with precise thickness, uniformity, and surface characteristics tailored to specific application requirements. Manufacturers can customize LCP films to achieve desired properties such as barrier performance, surface texture, and adhesion compatibility with substrates, further enhancing their versatility and market appeal. In addition, the increasing adoption of miniaturized electronic devices, lightweight automotive components, and high-performance medical devices drives the demand for LCP films as key materials in next-generation product designs. Over the forecast period, the combination of their exceptional mechanical, electrical, thermal, and optical properties, along with ongoing technological advancements and expanding application scope, positions LCP films as the largest segment in the liquid crystal polymer films and laminates market.

Liquid Crystal Polymer Films and Laminates Market Share Analysis: Medical Devices Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The medical devices segment is the fastest-growing segment in the liquid crystal polymer (LCP) films and laminates market, propelled by diverse key factors. The there is a growing demand for high-performance materials in the medical device industry to meet the increasing requirements for miniaturization, precision, and reliability. LCP films and laminates offer unique properties such as exceptional mechanical strength, dimensional stability, and biocompatibility, making them ideal for various medical device applications. These properties are particularly crucial in the fabrication of implantable medical devices, surgical instruments, diagnostic tools, and wearable healthcare devices. Secondly, technological advancements and innovations in medical device design and manufacturing have led to the development of next-generation medical products that leverage the unique properties of LCP films and laminates. For example, LCP films are used as substrates for flexible circuits and sensors in minimally invasive surgical devices, catheters, and neurostimulation implants, where flexibility, durability, and biocompatibility are essential. Additionally, LCP laminates are employed in the production of microfluidic devices, lab-on-a-chip systems, and biosensors for point-of-care diagnostics and personalized medicine applications. Thirdly, the increasing prevalence of chronic diseases, aging populations, and healthcare infrastructure investments drive the demand for advanced medical devices and technologies worldwide. The rising adoption of minimally invasive surgical procedures, remote patient monitoring solutions, and personalized healthcare services further accelerates the demand for LCP-based medical devices and components. In addition, stringent regulatory requirements and quality standards governing the manufacturing and use of medical devices necessitate the selection of materials with superior performance, reliability, and safety profiles. LCP films and laminates meet these requirements, offering manufacturers assurance of compliance and product reliability in medical applications. Additionally, the COVID-19 pandemic has underscored the importance of medical device innovation and technology in healthcare delivery, leading to increased investments in medical research, development, and manufacturing. Over the forecast period, the combination of technological advancements, evolving healthcare needs, regulatory compliance requirements, and market dynamics positions the medical devices segment as the fastest-growing segment in the liquid crystal polymer films and laminates market.

Liquid Crystal Polymer Films and Laminates Market Report Segmentation

By Product

Films

Laminates

By Application

Electrical & Electronics

Packaging

Automotive

Medical Devices

Others

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Liquid Crystal Polymer Films and Laminates Companies Profiled in the Market Study

Azotek Co. Ltd

Chiyoda Integre Co. Ltd

Furukawa Electric Co. Ltd

IQLP

KGK Chemical Corp

Kuraray Co. Ltd

Murata Manufacturing Co. Ltd

Panasonic Corp

Rogers Corp

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Liquid Crystal Polymer Films and Laminates Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Liquid Crystal Polymer Films and Laminates Market Size Outlook, $ Million, 2021 to 2030

3.2 Liquid Crystal Polymer Films and Laminates Market Outlook by Type, $ Million, 2021 to 2030

3.3 Liquid Crystal Polymer Films and Laminates Market Outlook by Product, $ Million, 2021 to 2030

3.4 Liquid Crystal Polymer Films and Laminates Market Outlook by Application, $ Million, 2021 to 2030

3.5 Liquid Crystal Polymer Films and Laminates Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Liquid Crystal Polymer Films and Laminates Industry

4.2 Key Market Trends in Liquid Crystal Polymer Films and Laminates Industry

4.3 Potential Opportunities in Liquid Crystal Polymer Films and Laminates Industry

4.4 Key Challenges in Liquid Crystal Polymer Films and Laminates Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Liquid Crystal Polymer Films and Laminates Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Liquid Crystal Polymer Films and Laminates Market Outlook by Segments

7.1 Liquid Crystal Polymer Films and Laminates Market Outlook by Segments, $ Million, 2021- 2030

By Product

Films

Laminates

By Application

Electrical & Electronics

Packaging

Automotive

Medical Devices

Others

8 North America Liquid Crystal Polymer Films and Laminates Market Analysis and Outlook To 2030

8.1 Introduction to North America Liquid Crystal Polymer Films and Laminates Markets in 2024

8.2 North America Liquid Crystal Polymer Films and Laminates Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Liquid Crystal Polymer Films and Laminates Market size Outlook by Segments, 2021-2030

By Product

Films

Laminates

By Application

Electrical & Electronics

Packaging

Automotive

Medical Devices

Others

9 Europe Liquid Crystal Polymer Films and Laminates Market Analysis and Outlook To 2030

9.1 Introduction to Europe Liquid Crystal Polymer Films and Laminates Markets in 2024

9.2 Europe Liquid Crystal Polymer Films and Laminates Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Liquid Crystal Polymer Films and Laminates Market Size Outlook by Segments, 2021-2030

By Product

Films

Laminates

By Application

Electrical & Electronics

Packaging

Automotive

Medical Devices

Others

10 Asia Pacific Liquid Crystal Polymer Films and Laminates Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Liquid Crystal Polymer Films and Laminates Markets in 2024

10.2 Asia Pacific Liquid Crystal Polymer Films and Laminates Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Liquid Crystal Polymer Films and Laminates Market size Outlook by Segments, 2021-2030

By Product

Films

Laminates

By Application

Electrical & Electronics

Packaging

Automotive

Medical Devices

Others

11 South America Liquid Crystal Polymer Films and Laminates Market Analysis and Outlook To 2030

11.1 Introduction to South America Liquid Crystal Polymer Films and Laminates Markets in 2024

11.2 South America Liquid Crystal Polymer Films and Laminates Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Liquid Crystal Polymer Films and Laminates Market size Outlook by Segments, 2021-2030

By Product

Films

Laminates

By Application

Electrical & Electronics

Packaging

Automotive

Medical Devices

Others

12 Middle East and Africa Liquid Crystal Polymer Films and Laminates Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Liquid Crystal Polymer Films and Laminates Markets in 2024

12.2 Middle East and Africa Liquid Crystal Polymer Films and Laminates Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Liquid Crystal Polymer Films and Laminates Market size Outlook by Segments, 2021-2030

By Product

Films

Laminates

By Application

Electrical & Electronics

Packaging

Automotive

Medical Devices

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Azotek Co. Ltd

Chiyoda Integre Co. Ltd

Furukawa Electric Co. Ltd

IQLP

KGK Chemical Corp

Kuraray Co. Ltd

Murata Manufacturing Co. Ltd

Panasonic Corp

Rogers Corp

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Product

Films

Laminates

By Application

Electrical & Electronics

Packaging

Automotive

Medical Devices

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)