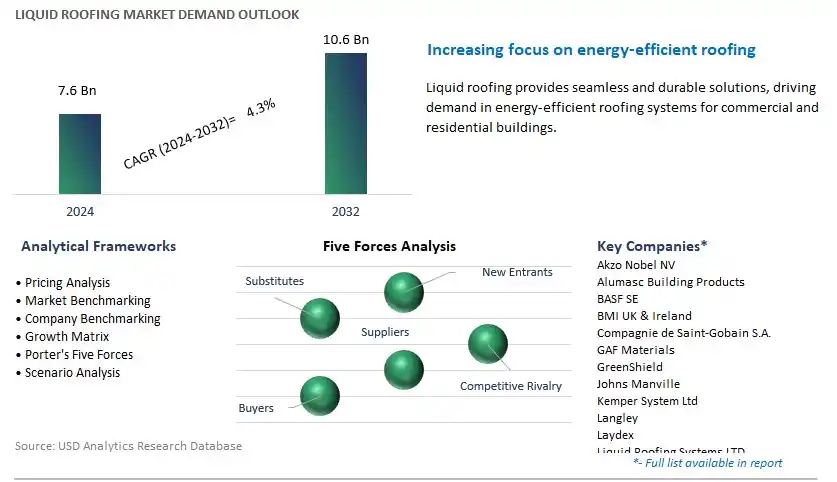

Global Liquid Roofing Market Size is valued at $7.6 Billion in 2024 and is forecast to register a growth rate (CAGR) of 4.3% to reach $10.6 Billion by 2032.

The global Liquid Roofing Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Type (Polyurethane Coatings, Acrylic Coatings, Bituminous Coatings, Silicone Coatings, Epoxy Coatings, Others), By Application (Domed Roofs, Pitched Roof, Flat Roofed), By End-User (Residential, Commercial, Industrial/Institutional, Infrastructure).

An Introduction to Liquid Roofing Market in 2024

Liquid roofing systems offer versatile and cost-effective solutions for waterproofing flat and low-slope roofs in commercial, industrial, and residential buildings. In 2024, the demand for liquid roofing s to rise, driven by the need for durable, energy-efficient, and sustainable roofing solutions. Liquid roofing materials, typically based on bitumen, polyurethane, silicone, or acrylic polymers, are applied as liquid coatings that cure to form seamless, flexible membranes, effectively sealing and protecting roofs from water ingress, UV radiation, and weathering. These systems offer advantages such as ease of application, adaptability to complex roof shapes, and resistance to temperature extremes and thermal cycling. With advancements in formulation technology and the development of eco-friendly and cool roof coatings, liquid roofing systems contribute to energy savings, reduce urban heat island effects, and extend the lifespan of roofing substrates. Further, liquid roofing systems are compatible with various substrates including concrete, metal, asphalt, and single-ply membranes, offering retrofit and restoration options for existing roofs. As building owners and contractors increasingly prioritize sustainability and long-term performance, the market for liquid roofing is expected to growing, driven by its benefits in terms of durability, energy efficiency, and environmental responsibility.

Liquid Roofing Market Competitive Landscape

The market report analyses the leading companies in the industry including Akzo Nobel NV, Alumasc Building Products, BASF SE, BMI UK & Ireland, Compagnie de Saint-Gobain S.A., GAF Materials, GreenShield, Johns Manville, Kemper System Ltd, Langley, Laydex, Liquid Roofing Systems LTD, SIG Design and Technology, Sika AG, and others.

Liquid Roofing Market Dynamics

Market Trend: Increasing Adoption of Sustainable Building Solutions

The most prominent market trend in liquid roofing is the increasing adoption of sustainable building solutions. With a growing focus on environmental conservation and energy efficiency, the construction industry is turning towards roofing systems that offer long-term sustainability and reduced environmental impact. Liquid roofing, known for its versatility, durability, and ability to provide seamless waterproofing, is gaining popularity as a sustainable alternative to traditional roofing materials. As regulations and green building certifications become more stringent, the demand for liquid roofing solutions that contribute to energy savings and minimize carbon footprint is expected to continue rising, driving market growth.

Market Driver: Renovation and Retrofitting Projects in the Construction Industry

A significant market driver for liquid roofing is the surge in renovation and retrofitting projects within the construction industry. As aging infrastructure and existing buildings require refurbishment and maintenance, there is a growing need for cost-effective and efficient roofing solutions that can extend the lifespan of structures and enhance their performance. Liquid roofing offers advantages such as ease of application, compatibility with various substrates, and seamless waterproofing capabilities, making it an ideal choice for renovation projects. Additionally, liquid roofing systems can be applied without the need for extensive tear-off, reducing disruption to ongoing operations and minimizing project timelines, thereby driving demand in the market.

Market Opportunity: Integration of Cool Roofing Technologies

An emerging opportunity within the liquid roofing market lies in the integration of cool roofing technologies. Cool roofing solutions are designed to reflect sunlight and heat away from buildings, reducing indoor temperature fluctuations and lowering cooling energy consumption. By incorporating cool roof coatings into liquid roofing systems, manufacturers can offer enhanced energy efficiency and thermal performance to building owners and operators. This not only helps in reducing energy costs and carbon emissions but also contributes to indoor comfort and occupant satisfaction. As sustainability becomes a key consideration in building design and construction, the demand for liquid roofing solutions with integrated cool roofing technologies is poised to grow, presenting a significant opportunity for market expansion and differentiation.

Liquid Roofing Market Share Analysis: Silicone Coatings is poised to register the fastest CAGR over the forecast period

The Silicone Coatings segment is the fastest-growing segment within the liquid roofing market. Silicone coatings offer numerous advantages, including excellent weather resistance, UV stability, and durability, making them highly sought-after for roofing applications. These coatings provide superior protection against harsh environmental conditions such as rain, snow, and extreme temperatures, ensuring long-term performance and extended roof life. Additionally, silicone coatings are highly flexible, allowing for expansion and contraction of the roof surface without cracking or delamination, which is particularly beneficial in regions prone to temperature variations. Moreover, silicone coatings require minimal maintenance and offer ease of application, reducing overall project costs and downtime. With their exceptional properties and increasing preference for sustainable and long-lasting roofing solutions, the Silicone Coatings segment is experiencing rapid growth and is poised to continue its expansion within the liquid roofing market.

Liquid Roofing Market Share Analysis: Flat Roofed is poised to register the fastest CAGR over the forecast period

The Flat Roofed segment is the fastest-growing segment within the liquid roofing market. Flat roofs are prevalent in commercial and industrial buildings, as well as residential structures, due to their cost-effectiveness and suitability for accommodating HVAC systems, solar panels, and recreational spaces. Liquid roofing solutions offer significant advantages for flat roofs, including seamless application, excellent waterproofing properties, and ease of maintenance. Moreover, flat roofs are more susceptible to water pooling and leakage issues compared to pitched or domed roofs, making them prime candidates for liquid roofing systems to provide enhanced protection and durability. Additionally, the growing trend towards green roofing initiatives, which involve the installation of vegetation and green spaces on flat roofs, further drives the demand for liquid roofing solutions to ensure proper waterproofing and insulation. With their versatility, performance benefits, and increasing adoption in various construction projects, the Flat Roofed segment is experiencing rapid growth and is expected to continue expanding within the liquid roofing market.

Liquid Roofing Market Share Analysis: Commercial segment generated the highest revenue in 2024

The Commercial segment is the largest segment within the liquid roofing market. Commercial buildings, including offices, retail spaces, hotels, and shopping centers, often have expansive roof areas that require robust and long-lasting roofing solutions to protect the structure and its occupants. Liquid roofing systems offer significant advantages for commercial applications, such as seamless application, superior waterproofing capabilities, and ease of maintenance. Additionally, commercial buildings typically undergo frequent foot traffic, equipment installations, and other activities that cause wear and tear on the roof surface, making durability and resilience essential attributes of roofing materials. Liquid roofing solutions meet these requirements effectively, providing a cost-effective and reliable option for commercial property owners and managers. Moreover, the increasing focus on sustainability and energy efficiency in commercial construction further drives the demand for liquid roofing systems, as they can contribute to improved building performance and energy savings. With their suitability for a wide range of commercial applications and ongoing growth in the commercial construction sector, the Commercial segment maintains its position as the largest market segment within the liquid roofing market.

Liquid Roofing Market

By Type

Polyurethane Coatings

Acrylic Coatings

Bituminous Coatings

Silicone Coatings

Epoxy Coatings

Others

By Application

Domed Roofs

Pitched Roof

Flat Roofed

By End-User

Residential

Commercial

Industrial/Institutional

InfrastructureCountries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Liquid Roofing Companies Profiled in the Study

Akzo Nobel NV

Alumasc Building Products

BASF SE

BMI UK & Ireland

Compagnie de Saint-Gobain S.A.

GAF Materials

GreenShield

Johns Manville

Kemper System Ltd

Langley

Laydex

Liquid Roofing Systems LTD

SIG Design and Technology

Sika AG

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Liquid Roofing Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Liquid Roofing Market Size Outlook, $ Million, 2021 to 2032

3.2 Liquid Roofing Market Outlook by Type, $ Million, 2021 to 2032

3.3 Liquid Roofing Market Outlook by Product, $ Million, 2021 to 2032

3.4 Liquid Roofing Market Outlook by Application, $ Million, 2021 to 2032

3.5 Liquid Roofing Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Liquid Roofing Industry

4.2 Key Market Trends in Liquid Roofing Industry

4.3 Potential Opportunities in Liquid Roofing Industry

4.4 Key Challenges in Liquid Roofing Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Liquid Roofing Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Liquid Roofing Market Outlook by Segments

7.1 Liquid Roofing Market Outlook by Segments, $ Million, 2021- 2032

By Type

Polyurethane Coatings

Acrylic Coatings

Bituminous Coatings

Silicone Coatings

Epoxy Coatings

Others

By Application

Domed Roofs

Pitched Roof

Flat Roofed

By End-User

Residential

Commercial

Industrial/Institutional

Infrastructure

8 North America Liquid Roofing Market Analysis and Outlook To 2032

8.1 Introduction to North America Liquid Roofing Markets in 2024

8.2 North America Liquid Roofing Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Liquid Roofing Market size Outlook by Segments, 2021-2032

By Type

Polyurethane Coatings

Acrylic Coatings

Bituminous Coatings

Silicone Coatings

Epoxy Coatings

Others

By Application

Domed Roofs

Pitched Roof

Flat Roofed

By End-User

Residential

Commercial

Industrial/Institutional

Infrastructure

9 Europe Liquid Roofing Market Analysis and Outlook To 2032

9.1 Introduction to Europe Liquid Roofing Markets in 2024

9.2 Europe Liquid Roofing Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Liquid Roofing Market Size Outlook by Segments, 2021-2032

By Type

Polyurethane Coatings

Acrylic Coatings

Bituminous Coatings

Silicone Coatings

Epoxy Coatings

Others

By Application

Domed Roofs

Pitched Roof

Flat Roofed

By End-User

Residential

Commercial

Industrial/Institutional

Infrastructure

10 Asia Pacific Liquid Roofing Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Liquid Roofing Markets in 2024

10.2 Asia Pacific Liquid Roofing Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Liquid Roofing Market size Outlook by Segments, 2021-2032

By Type

Polyurethane Coatings

Acrylic Coatings

Bituminous Coatings

Silicone Coatings

Epoxy Coatings

Others

By Application

Domed Roofs

Pitched Roof

Flat Roofed

By End-User

Residential

Commercial

Industrial/Institutional

Infrastructure

11 South America Liquid Roofing Market Analysis and Outlook To 2032

11.1 Introduction to South America Liquid Roofing Markets in 2024

11.2 South America Liquid Roofing Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Liquid Roofing Market size Outlook by Segments, 2021-2032

By Type

Polyurethane Coatings

Acrylic Coatings

Bituminous Coatings

Silicone Coatings

Epoxy Coatings

Others

By Application

Domed Roofs

Pitched Roof

Flat Roofed

By End-User

Residential

Commercial

Industrial/Institutional

Infrastructure

12 Middle East and Africa Liquid Roofing Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Liquid Roofing Markets in 2024

12.2 Middle East and Africa Liquid Roofing Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Liquid Roofing Market size Outlook by Segments, 2021-2032

By Type

Polyurethane Coatings

Acrylic Coatings

Bituminous Coatings

Silicone Coatings

Epoxy Coatings

Others

By Application

Domed Roofs

Pitched Roof

Flat Roofed

By End-User

Residential

Commercial

Industrial/Institutional

Infrastructure

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

Akzo Nobel NV

Alumasc Building Products

BASF SE

BMI UK & Ireland

Compagnie de Saint-Gobain S.A.

GAF Materials

GreenShield

Johns Manville

Kemper System Ltd

Langley

Laydex

Liquid Roofing Systems LTD

SIG Design and Technology

Sika AG

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Type

Polyurethane Coatings

Acrylic Coatings

Bituminous Coatings

Silicone Coatings

Epoxy Coatings

Others

By Application

Domed Roofs

Pitched Roof

Flat Roofed

By End-User

Residential

Commercial

Industrial/Institutional

Infrastructure

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)